Why SBA 7a and 504? Access to Capital vs. Incentive Financing 7a

25 Slides182.50 KB

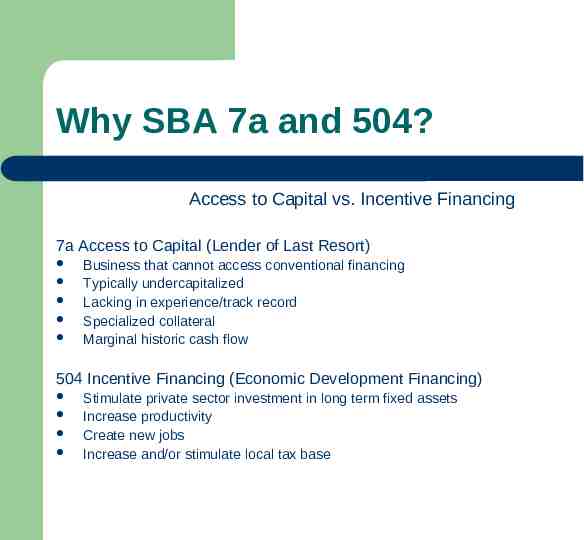

Why SBA 7a and 504? Access to Capital vs. Incentive Financing 7a Access to Capital (Lender of Last Resort) Business that cannot access conventional financing Typically undercapitalized Lacking in experience/track record Specialized collateral Marginal historic cash flow 504 Incentive Financing (Economic Development Financing) Stimulate private sector investment in long term fixed assets Increase productivity Create new jobs Increase and/or stimulate local tax base

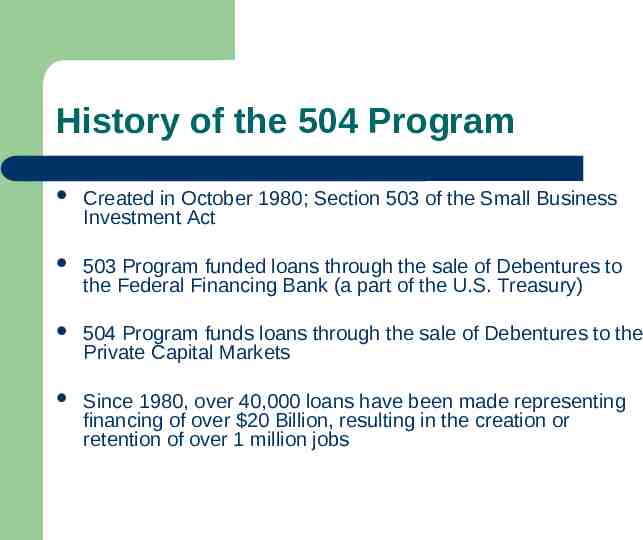

History of the 504 Program Created in October 1980; Section 503 of the Small Business Investment Act 503 Program funded loans through the sale of Debentures to the Federal Financing Bank (a part of the U.S. Treasury) 504 Program funds loans through the sale of Debentures to the Private Capital Markets Since 1980, over 40,000 loans have been made representing financing of over 20 Billion, resulting in the creation or retention of over 1 million jobs

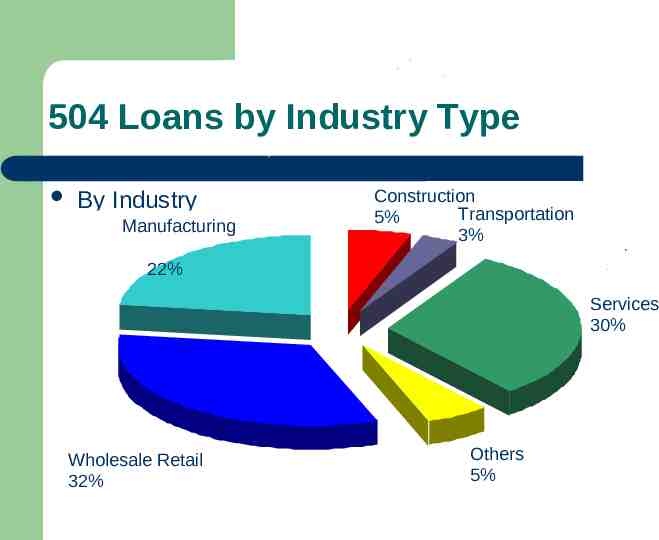

504 Loans by Industry Type By Industry Manufacturing Construction Transportation 5% 3% 22% Services 30% Wholesale Retail 32% Others 5%

Certified Development Companies (CDC) Licensed and regulated by the Small Business Administration (SBA) Most are non-profit organizations Some are affiliated with public entities, or other nonprofits CDC’s have a Public Purpose-Economic Development

Goals of the 504 Program Create Economic Development Opportunity in a Community Provide Affordable Long Term Financing for Business Expansion Give a Financial Incentive to encourage Private Lender Participation Give a Financial Incentive to Stimulate Business Capital Investment Provide Access to Public Capital Markets for Small Business

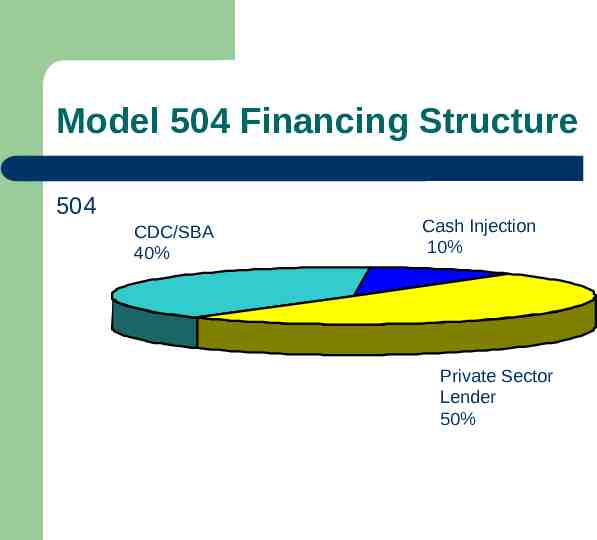

Model 504 Financing Structure 504 CDC/SBA 40% Cash Injection 10% Private Sector Lender 50%

Structure Guidelines Equity – – – – – or Local Injection Minimum is usually 10% Limited use or Start Up 15%; Both 20% In the form of cash or equity in real estate Usually required of the borrower May be a loan from CDC or other lender (rate); if secured, it must be subordinate to CDC/SBA and private sector lender. (Term should be same or longer)

Advantage of a 504 Loan For – – – – – – the Borrower Low Down Payment Fixed interest rate second mortgage loan Long Term Financing Rate of private sector financing usually more favorable (Low LTV) In credit crunch – getting a loan at all Collateral usually limited to project assets

Basic Eligibility for 504 Financing Be an Operating Business (Except for loans to Eligible Passive Concerns) Be organized for Profit Be Located within the United States Be “Small” Under the Program Size Standards Demonstrate the need for the desired financing Meet an economic development objective of the program (504 only)

Maximum Loan Amount An eligible entity may borrow up to 40% of the project or a total SBA guaranteed portion of 1,000,000. If applicant (or affiliates) has existing SBA loans, the total guaranteed portion must not exceed the maximums stated above. – – 504 loans carry 100% guaranty 7a loans usually carry 75-80% guaranty

Minimum Loan Amount The debenture should be no less than 50,000. That translates to a project size of about 125,000. With special permission from District Office, the debenture can be less, but can never be less than 25,000.

504 Size Standards Tangible Net Worth of no more than 7 million AND Net Profit after Tax (2 year average) of no more than 2.5 million - OrUse 7a size standards as an alternative (Size standards increase by 25% in Labor Surplus Areas)

Ineligible Types of Businesses Non-Profit Institutions Finance Business (Banks, Finance Companies, Insurance Companies, etc) Real Estate Development and other Speculative Business Business Located in a Foreign Country ( Legal Permanent Resident-LPR) Pyramid Sales Distributions Business deriving more than 1/3 of Gross Annual Revenue from Legal Gambling Businesses that limit membership for reasons other than capacity

Ineligible Types of Businesses Government Owned Entities (Except Tribal) Businesses Principally engaged in Teaching, Instructing, Counseling or Indoctrinating Religion or Religious Beliefs Consumer Marketing Co-ops (Producers Co-Ops Ok) Businesses earnings more than 1/3 of income from packaging of SBA loans Businesses in which the Lender or CDC or any of its associates owns an equity interest Businesses primarily involved in political or lobbying activites

Ineligible Types of Businesses Businesses which present live performances of a Prurient Sexual Nature or derive more than de minimus gross revenue from the sale of products or services of a prurient sexual nature Unless, waived by SBA, Businesses that have previously defaulted on a Federal loan or Federallyassisted financing Businesses where an associate is incarcerated, on probation or parole, or has been indicted for a Felony or crime of moral turpitude Businesses engaged in any illegal activity

Eligible Use of Proceeds Acquisition of Land Land Improvements Remodel, convert, expand or renovate existing building(s) Purchase of one or more existing buildings – – OC must occupy 51% 504 Projects funds cannot make tenant improvements

Eligible Use of Proceeds Construction – of New Building OC needs to occupy at least 60% with plans to occupy 80% within 10 years. Can lease up to 20% indefinitely. Must plan to utilize the remaining 20% within 3 years

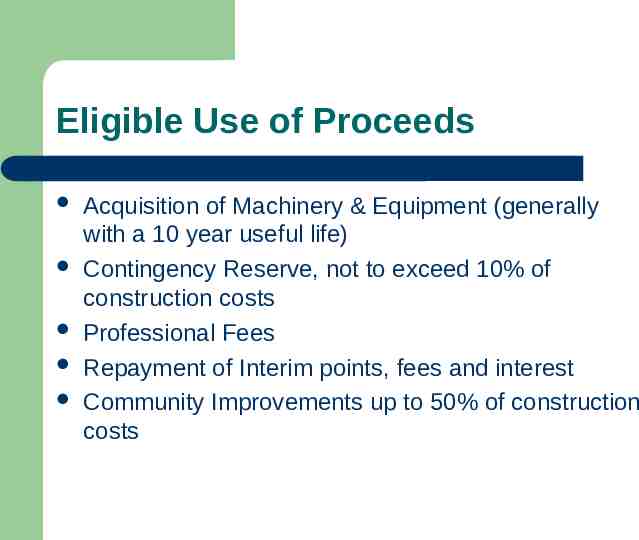

Eligible Use of Proceeds Acquisition of Machinery & Equipment (generally with a 10 year useful life) Contingency Reserve, not to exceed 10% of construction costs Professional Fees Repayment of Interim points, fees and interest Community Improvements up to 50% of construction costs

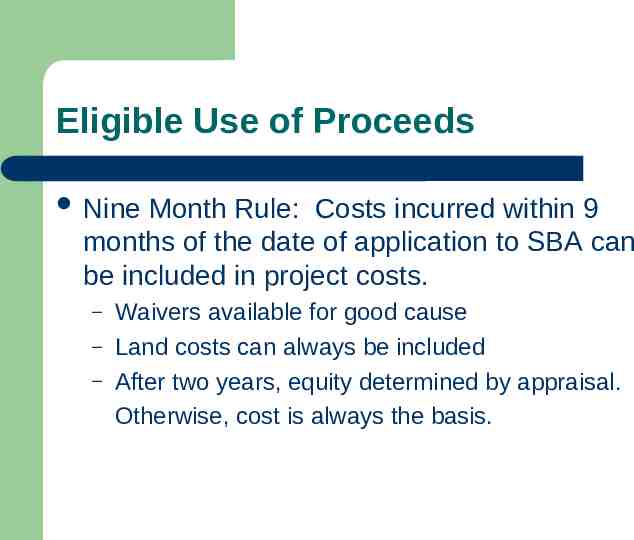

Eligible Use of Proceeds Nine Month Rule: Costs incurred within 9 months of the date of application to SBA can be included in project costs. – – – Waivers available for good cause Land costs can always be included After two years, equity determined by appraisal. Otherwise, cost is always the basis.

Ineligible Use of Proceeds Debt Refinance (except for eligible interim financing) Counseling Fees Incorporation or Other Organizational Costs Franchise Fees Commitment Fees; Finance Broker Fees; Origination Fees for Private Sector Financing

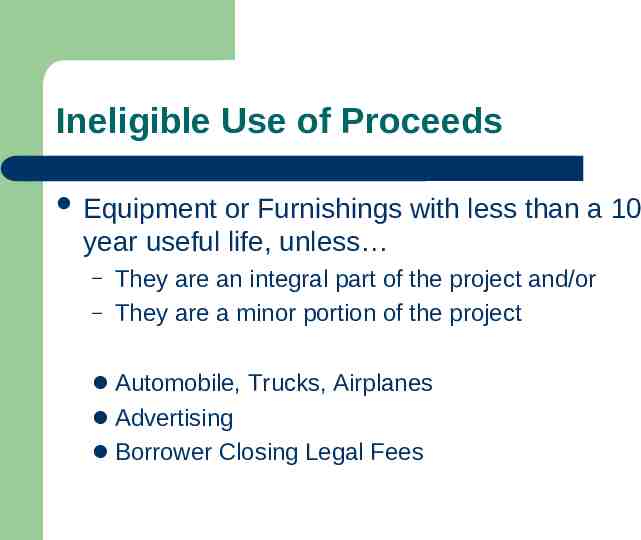

Ineligible Use of Proceeds Equipment or Furnishings with less than a 10 year useful life, unless – – They are an integral part of the project and/or They are a minor portion of the project Automobile, Trucks, Airplanes Advertising Borrower Closing Legal Fees

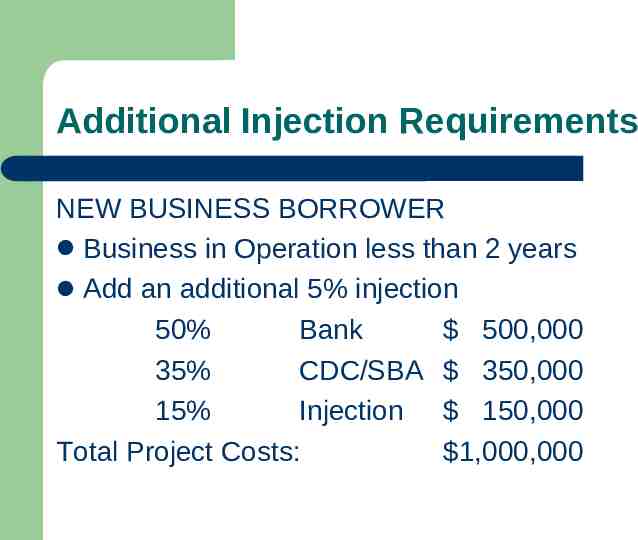

Additional Injection Requirements NEW BUSINESS BORROWER Business in Operation less than 2 years Add an additional 5% injection 50% Bank 500,000 35% CDC/SBA 350,000 15% Injection 150,000 Total Project Costs: 1,000,000

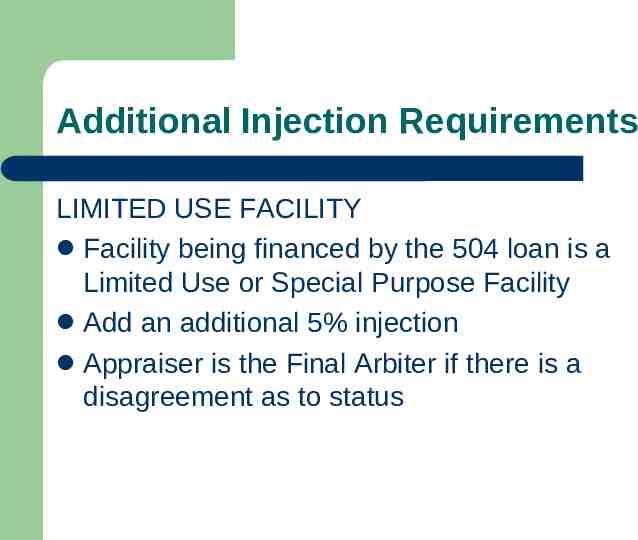

Additional Injection Requirements LIMITED USE FACILITY Facility being financed by the 504 loan is a Limited Use or Special Purpose Facility Add an additional 5% injection Appraiser is the Final Arbiter if there is a disagreement as to status

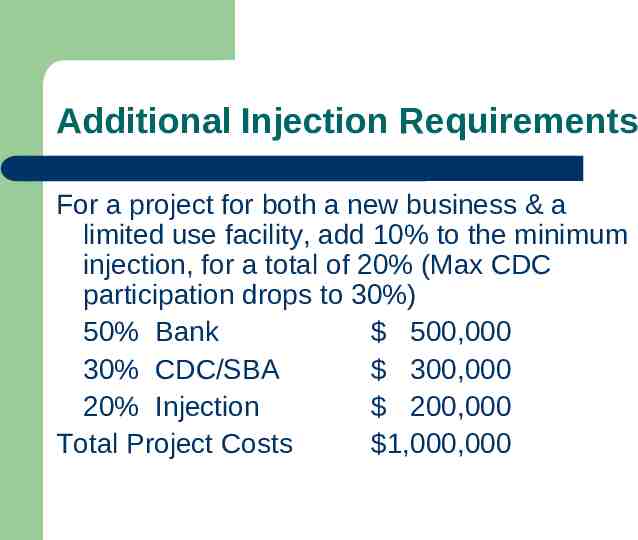

Additional Injection Requirements For a project for both a new business & a limited use facility, add 10% to the minimum injection, for a total of 20% (Max CDC participation drops to 30%) 50% Bank 500,000 30% CDC/SBA 300,000 20% Injection 200,000 Total Project Costs 1,000,000

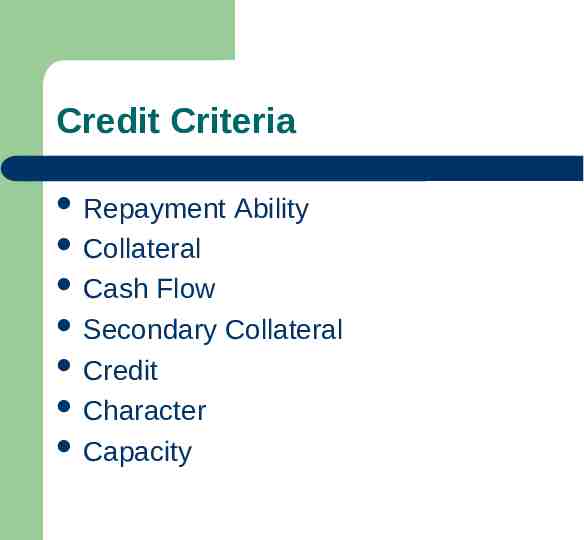

Credit Criteria Repayment Ability Collateral Cash Flow Secondary Collateral Credit Character Capacity