PROPERTY RIGHTS IN GB, FRANCE AND GERMANY Mortgages By: Zuzanna

21 Slides3.25 MB

PROPERTY RIGHTS IN GB, FRANCE AND GERMANY Mortgages By: Zuzanna Wawrzyniak LL.B

A property right the exclusive authority to determine how a resource is used, whether that resource is owned by government or by individuals. Laws created by governments in regards to how individuals can control, benefit from and transfer property.

Private property rights The three basic elements of private property are exclusivity of rights to choose the use of a resource, exclusivity of rights to the services of a resource, rights to exchange the resource at mutually agreeable terms.

Great Britain The United Kingdom is considered as the largest reverse mortgage market in the world and the largest market in the European Union (the value of loans is estimated at over 205 billion pounds). There are offered two types of annuities: those based on the sale and purchase agreement, as well as those based on the loan contract (called. lifetime mortgage). The most important informations connected with mortgages and registers are included in Law of Property Act 1925 Part III Mortgages, Rentcharges, and Powers of Attorney articles 85 – 120.

Great Britain – types of mortgages Legal Mortgage - occurs when the owner gives legal title of property to a creditor to secure payment of the owner's debt. In a typical mortgage, once the debtor pays off the debt, legal title to the property will revert to the original owner. Equitable Mortgage - courts of equity evolved to redress injustices caused by legal courts' strict adherence to the law. Courts of equity thus recognize "equitable" mortgages, which occur when a transaction does not fulfill all legal requirements of a mortgage, but still looks and operates like a mortgage; in other words, property is offered to a creditor to secure debt.

The creation of legal mortgage in GB 1. LONG LEASE with a provision for cesser on redemption: Mortgage of fee simple by grant of long lease (85. Mode of mortgaging freeholds. Law of Property Act 1925). Mortgage of lease by grant of a sub-lease (86 Mode of mortgaging leaseholds. Law of Property Act 1925).

The creation of legal mortgage in GB 2. A CHARGE BY DEED by WAY OF LEGAL MORTGAGE s.87(1) LPA Sample clause in mortgage deed: ‘The Borrower charges the property by way of legal mortgage with payment of all the money payable to the Lender under the mortgage conditions.’ s.87 LPA 25 : The charge gives the Lender ‘the same protection, powers & remedies’ as if the mortgage had been created under s.85(1) or 86(1) LPA 25

The creation of legal mortgage in GB 3. FORMALITIES NEEDED FOR ACTUAL LEGAL STATUS A deed (s.52 LPA 1925) Registration at Land Registry if Borrower’s title to the land is registered Registration at Land Registry if it is a FIRST mortgage of an unregistered title (triggers first registration)

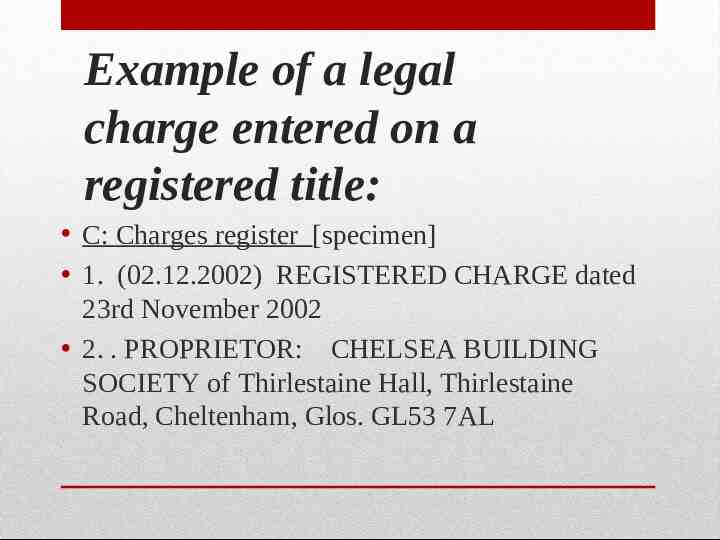

Example of a legal charge entered on a registered title: C: Charges register [specimen] 1. (02.12.2002) REGISTERED CHARGE dated 23rd November 2002 2. . PROPRIETOR: CHELSEA BUILDING SOCIETY of Thirlestaine Hall, Thirlestaine Road, Cheltenham, Glos. GL53 7AL

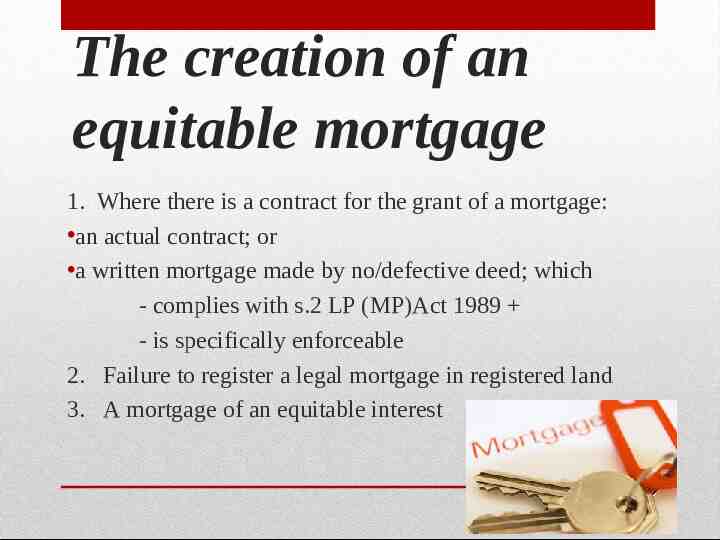

The creation of an equitable mortgage 1. Where there is a contract for the grant of a mortgage: an actual contract; or a written mortgage made by no/defective deed; which - complies with s.2 LP (MP)Act 1989 - is specifically enforceable 2. Failure to register a legal mortgage in registered land 3. A mortgage of an equitable interest

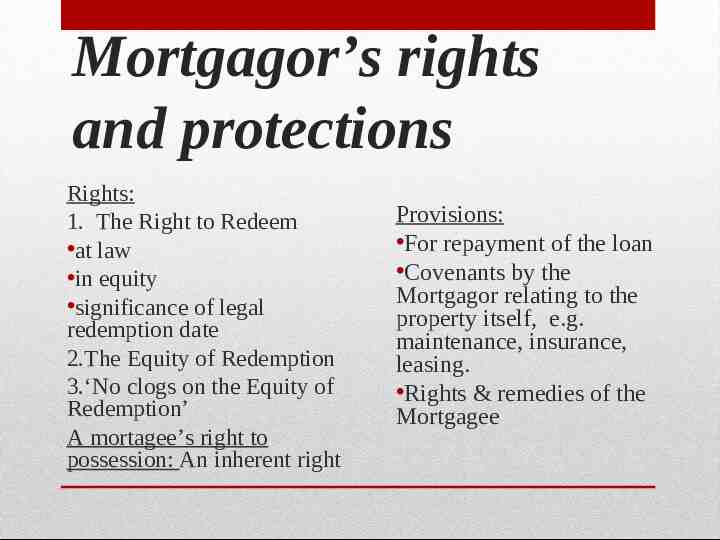

Mortgagor’s rights and protections Rights: 1. The Right to Redeem at law in equity significance of legal redemption date 2.The Equity of Redemption 3.‘No clogs on the Equity of Redemption’ A mortagee’s right to possession: An inherent right Provisions: For repayment of the loan Covenants by the Mortgagor relating to the property itself, e.g. maintenance, insurance, leasing. Rights & remedies of the Mortgagee

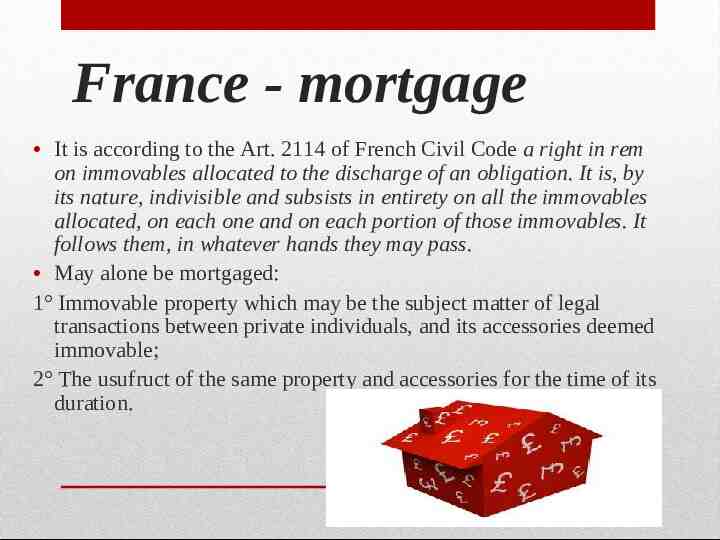

France - mortgage It is according to the Art. 2114 of French Civil Code a right in rem on immovables allocated to the discharge of an obligation. It is, by its nature, indivisible and subsists in entirety on all the immovables allocated, on each one and on each portion of those immovables. It follows them, in whatever hands they may pass. May alone be mortgaged: 1 Immovable property which may be the subject matter of legal transactions between private individuals, and its accessories deemed immovable; 2 The usufruct of the same property and accessories for the time of its duration.

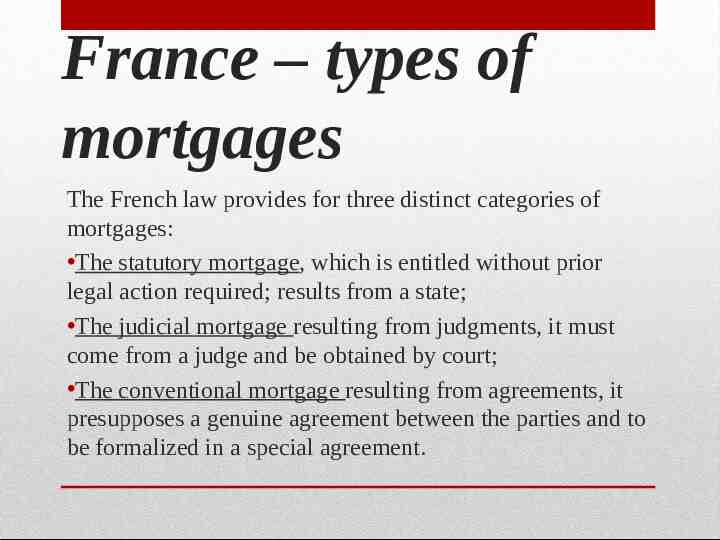

France – types of mortgages The French law provides for three distinct categories of mortgages: The statutory mortgage, which is entitled without prior legal action required; results from a state; The judicial mortgage resulting from judgments, it must come from a judge and be obtained by court; The conventional mortgage resulting from agreements, it presupposes a genuine agreement between the parties and to be formalized in a special agreement.

Statutory mortgage - described in French civil code Section I - Of Statutory Mortgages Art. 2121 -2122. Independently of statutory mortgages resulting from other Codes or from particular statutes, the rights and claims to which a statutory mortgage is granted are: 1 Those of one spouse, on the property of the other; 2 Those of minors or adults in guardianship, on the property of a guardian or statutory administrator; 3 Those of the State, of departments, of communes and of public institutions, on the property of collectors and accounting administrators; 4 Those of a legatee, on the property of the succession, under Article 1017 5 Those stated in Article 2101, 2 , 3 , 5 , 6 , 7 and 8

Judical mortgage - described in Section II – of judicial mortgages in article 2123 of French civil code. The judicial mortgage is the result of a court decision, it is necessary to a debtor insolvent if claims by any other means. The creditor with a judicial mortgage can: Register its interest in all properties currently owned by the debtor; Take additional inscriptions on buildings came later in his debtor's assets.

Conventional mortgage It is stablished in section III Of Conventional Mortgages and according to the Art. 2124 Conventional mortgages may be granted only by those who have the capacity of conveying the immovables which they burden with them. The mortgage extends automatically to interest and other accessories and is transmitted automatically to the secured claim.

The legal effects of mortgages Between creditors, a mortgage, either statutory, or judicial, or conventional, ranks only from the day of the registration made by the creditor at the land registry, in the form and manner prescribed by law. Where several registrations are required on the same day as to the same immovable, that which is required by virtue of the instrument of title bearing the remotest date shall be deemed of prior rank, whatever the order resulting from the register provided for in Article 2200 may be.

Germany In Germany the most important informations connected with mortgages are included in BGB German Civil Code Division 7 called Mortgage, land charge, annuity land charge sections 1113- 1190. According to article 1113: 1)A plot of land may be encumbered in such a way that the person in whose favour the encumbrance is created is to be paid out of the land a specific sum of money to satisfy a claim to which he is entitled (mortgage). 2)The mortgage may also be created for a future or a conditional claim.

Types of mortgages In Germany, the general term is Grundpfandrecht („real security on real property“). It encompasses the Grundschuld (§§ 1191 ss. BGB) and the Hypothek (§§ 1113 ss. BGB). The Hypothek is an accessory security whereas the Grundschuld is a nonaccessory security. In the Civil Code, the default model is the Hypothek whereas the Grundschuld is regulated largely by references to the rules on the Hypothek. In practice, however, the Grundschuld prevails, as it is more flexible and may also be used to secure later debts with the same creditor. - Further subtypes of the Hypothek are the Sicherungshypothek (§§ 1184 ss. BGB), a strictly accessory mortgage - and the Höchstbetragshypothek (§ 1190 BGB).

Legal nature Mortgage and land charge are both a ius in rem. They entitle the creditor to enforce paymentof a claim of money from the real estate (§ 1147 BGB). Satisfaction by execution The satisfaction of the creditor from the plot of land and from the objects to which the mortgage extends is effected by execution. However, the creditor still needs a title for encorcement: If the owner has not declared submission to enforcement the creditor first has to go to court to get an enforceable title before he may start a forced sale.

Thank you