Presented by Vincent J. Bono, J.D. and Carolyn Marie Tobin, MA If

24 Slides1.40 MB

Presented by Vincent J. Bono, J.D. and Carolyn Marie Tobin, MA If you have questions about any of your federal benefits, please email them to Carolyn Tobin: [email protected]

Vince Bono’s “Market-Watch” The Two-Minute Rendition

In the Summer of 2003, the Founders of our company were asked to assess the federal retirement system and the various components of the TSP. Much to their surprise, they found that the TSP Funds were not truly managed to maximize gains for the federal employees or minimize their losses. They also found that federal employees were not being shown how to maximize their federal pension or social security incomes, nor were they being taught how to properly plan for their retirement.

We created a proprietary online calculator that will illustrate your Pension, Social Security and TSP/”Other” income at any age & time period you select. It also allows you to project and compare the future performance of your TSP with other approved, tax qualified alternatives. This is a fantastic retirement planning tool that takes under 60 seconds to use, once you are shown how it works. It allows you the ability to reenter different data sets for planning purposes. We do not collect or store any personal information or data there. Please email Carolyn ([email protected]) if you would like your Approved Webinar Host to email you the calculator link. Please include the best day, time and phone number if you would like a free 15 minute telephonic tutorial, which is highly recommended

Our “Approved Webinar Hosts” are well vetted by us, and experts in helping federal employees better plan for their retirement and by agreement with us, do not charge federal employees for any of their retirement consultation services or “Pre-Retirement Strategy Reports”, no matter how extensive their reports or retirement planning advice might be. When your Approved Webinar Host contacts you to answer any questions you might have about your federal benefits and/or federal retirement, we suggest your reach back out to them. Nothing need be done in person, as all of this can be done on the phone and through our internet portals.

Your Life Expectancy When you will be eligible to retire Will you be financially prepared to retire When you can access your TSP money What are your financial options Taxes (State & Federal) Will you make an irreversible mistake

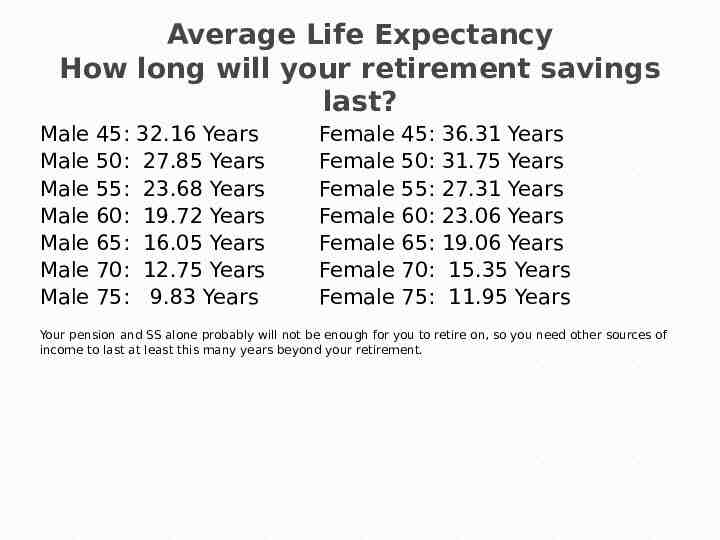

Average Life Expectancy How long will your retirement savings last? Male Male Male Male Male Male Male 45: 50: 55: 60: 65: 70: 75: 32.16 Years 27.85 Years 23.68 Years 19.72 Years 16.05 Years 12.75 Years 9.83 Years Female Female Female Female Female Female Female 45: 50: 55: 60: 65: 70: 75: 36.31 Years 31.75 Years 27.31 Years 23.06 Years 19.06 Years 15.35 Years 11.95 Years Your pension and SS alone probably will not be enough for you to retire on, so you need other sources of income to last at least this many years beyond your retirement.

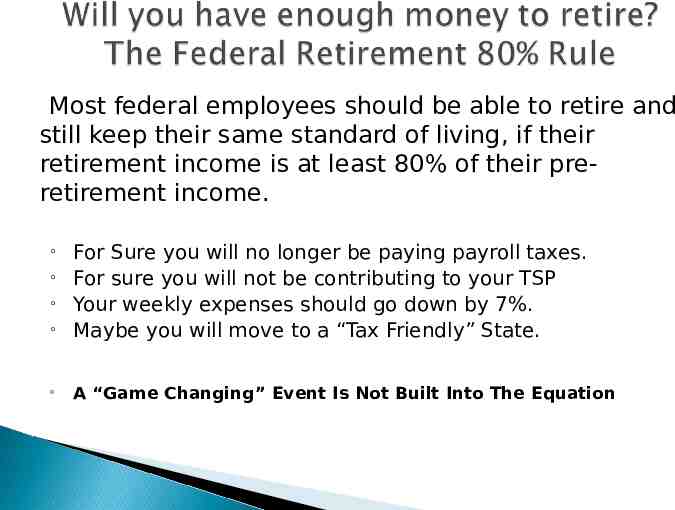

Most federal employees should be able to retire and still keep their same standard of living, if their retirement income is at least 80% of their preretirement income. For Sure you will no longer be paying payroll taxes. For sure you will not be contributing to your TSP Your weekly expenses should go down by 7%. Maybe you will move to a “Tax Friendly” State. A “Game Changing” Event Is Not Built Into The Equation

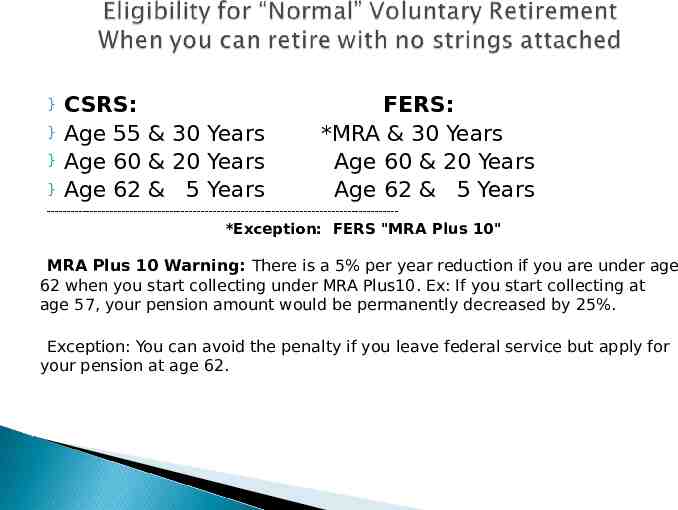

} } } } CSRS: Age 55 & 30 Years Age 60 & 20 Years Age 62 & 5 Years FERS: *MRA & 30 Years Age 60 & 20 Years Age 62 & 5 Years ----------------------------------------------------------------------------------------- *Exception: FERS "MRA Plus 10" MRA Plus 10 Warning: There is a 5% per year reduction if you are under age 62 when you start collecting under MRA Plus10. Ex: If you start collecting at age 57, your pension amount would be permanently decreased by 25%. Exception: You can avoid the penalty if you leave federal service but apply for your pension at age 62.

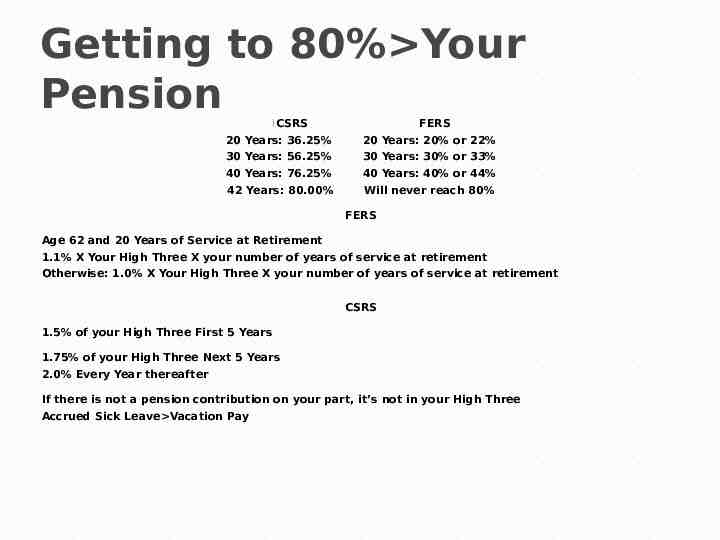

Getting to 80% Your Pension }CSRS FERS 20 Years: 36.25% 20 Years: 20% or 22% 30 Years: 56.25% 30 Years: 30% or 33% 40 Years: 76.25% 40 Years: 40% or 44% 42 Years: 80.00% Will never reach 80% FERS Age 62 and 20 Years of Service at Retirement 1.1% X Your High Three X your number of years of service at retirement Otherwise: 1.0% X Your High Three X your number of years of service at retirement CSRS 1.5% of your High Three First 5 Years 1.75% of your High Three Next 5 Years 2.0% Every Year thereafter If there is not a pension contribution on your part, it’s not in your High Three Accrued Sick Leave Vacation Pay

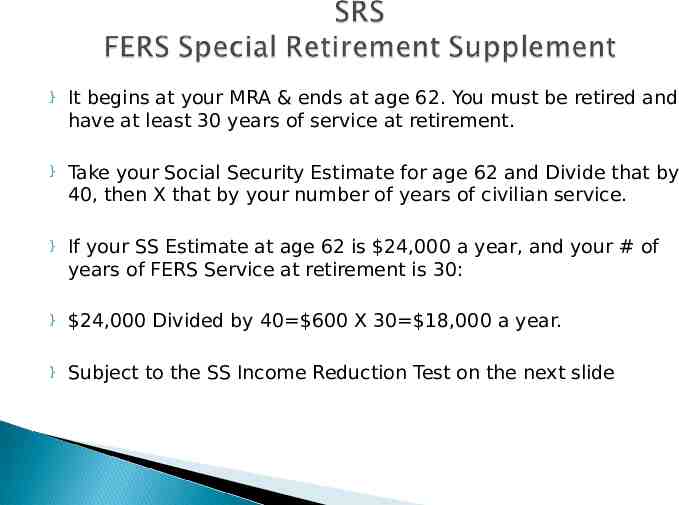

} It begins at your MRA & ends at age 62. You must be retired and have at least 30 years of service at retirement. } Take your Social Security Estimate for age 62 and Divide that by 40, then X that by your number of years of civilian service. } If your SS Estimate at age 62 is 24,000 a year, and your # of years of FERS Service at retirement is 30: } 24,000 Divided by 40 600 X 30 18,000 a year. } Subject to the SS Income Reduction Test on the next slide

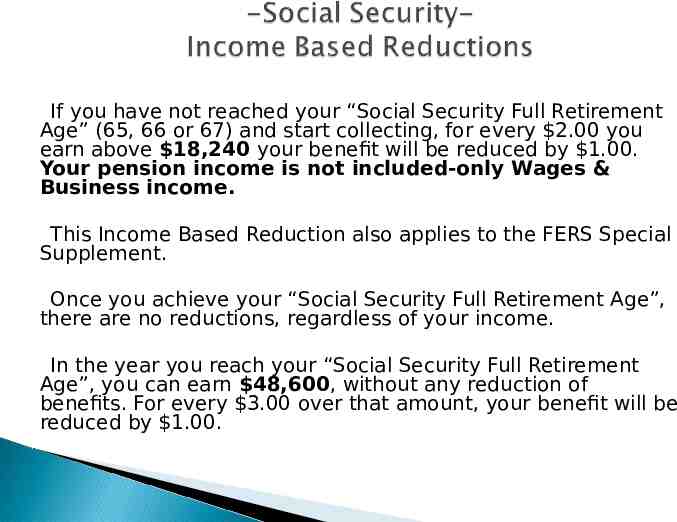

If you have not reached your “Social Security Full Retirement Age” (65, 66 or 67) and start collecting, for every 2.00 you earn above 18,240 your benefit will be reduced by 1.00. Your pension income is not included-only Wages & Business income. This Income Based Reduction also applies to the FERS Special Supplement. Once you achieve your “Social Security Full Retirement Age”, there are no reductions, regardless of your income. In the year you reach your “Social Security Full Retirement Age”, you can earn 48,600, without any reduction of benefits. For every 3.00 over that amount, your benefit will be reduced by 1.00.

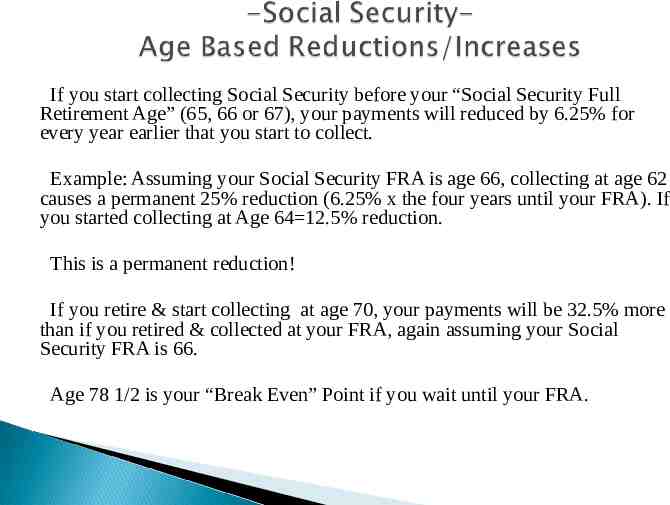

If you start collecting Social Security before your “Social Security Full Retirement Age” (65, 66 or 67), your payments will reduced by 6.25% for every year earlier that you start to collect. Example: Assuming your Social Security FRA is age 66, collecting at age 62 causes a permanent 25% reduction (6.25% x the four years until your FRA). If you started collecting at Age 64 12.5% reduction. This is a permanent reduction! If you retire & start collecting at age 70, your payments will be 32.5% more than if you retired & collected at your FRA, again assuming your Social Security FRA is 66. Age 78 1/2 is your “Break Even” Point if you wait until your FRA.

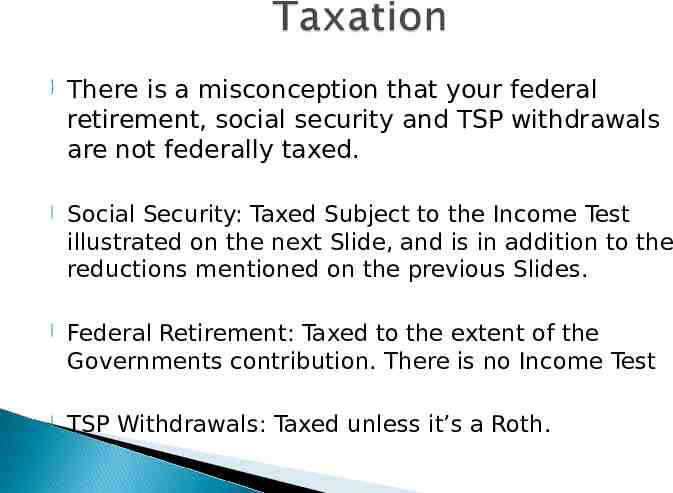

} There is a misconception that your federal retirement, social security and TSP withdrawals are not federally taxed. } Social Security: Taxed Subject to the Income Test illustrated on the next Slide, and is in addition to the reductions mentioned on the previous Slides. } Federal Retirement: Taxed to the extent of the Governments contribution. There is no Income Test } TSP Withdrawals: Taxed unless it’s a Roth.

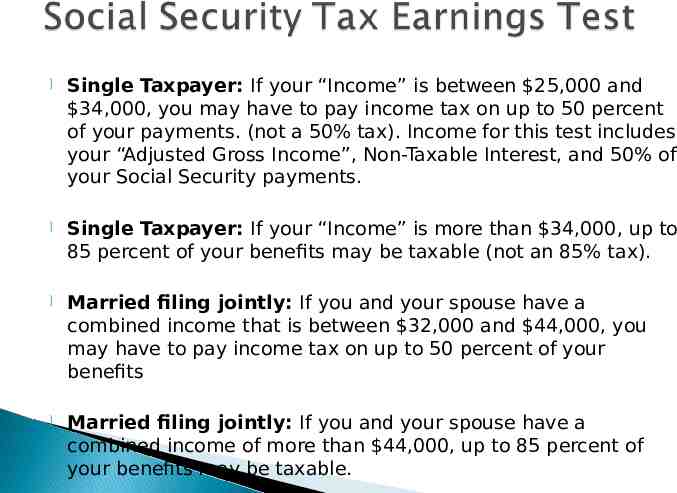

} Single Taxpayer: If your “Income” is between 25,000 and 34,000, you may have to pay income tax on up to 50 percent of your payments. (not a 50% tax). Income for this test includes your “Adjusted Gross Income”, Non-Taxable Interest, and 50% of your Social Security payments. } Single Taxpayer: If your “Income” is more than 34,000, up to 85 percent of your benefits may be taxable (not an 85% tax). } Married filing jointly: If you and your spouse have a combined income that is between 32,000 and 44,000, you may have to pay income tax on up to 50 percent of your benefits } Married filing jointly: If you and your spouse have a combined income of more than 44,000, up to 85 percent of your benefits may be taxable.

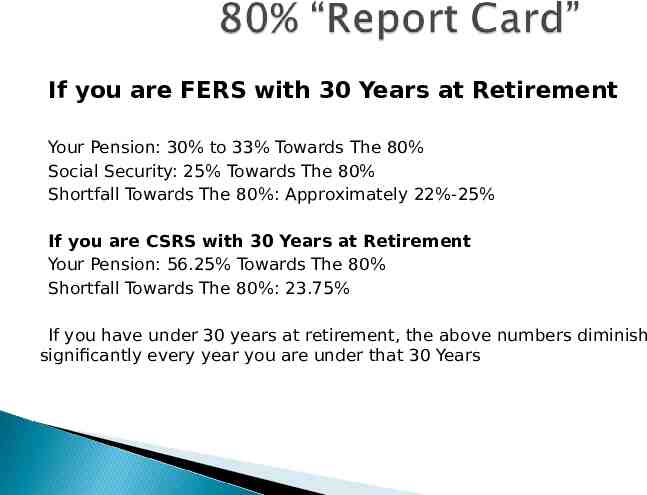

If you are FERS with 30 Years at Retirement Your Pension: 30% to 33% Towards The 80% Social Security: 25% Towards The 80% Shortfall Towards The 80%: Approximately 22%-25% If you are CSRS with 30 Years at Retirement Your Pension: 56.25% Towards The 80% Shortfall Towards The 80%: 23.75% If you have under 30 years at retirement, the above numbers diminish significantly every year you are under that 30 Years

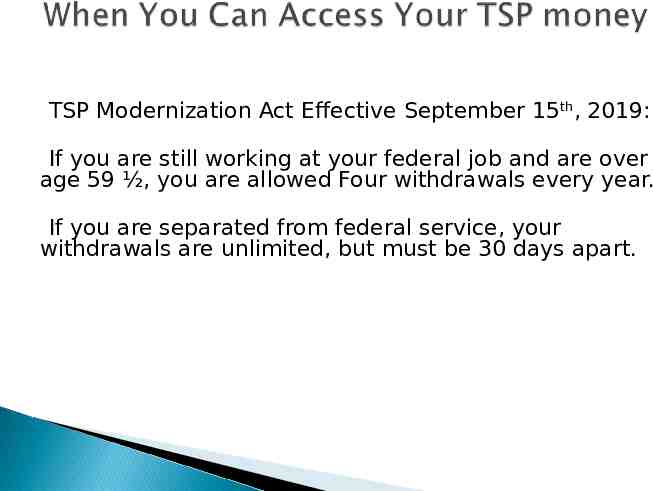

TSP Modernization Act Effective September 15th, 2019: If you are still working at your federal job and are over age 59 ½, you are allowed Four withdrawals every year. If you are separated from federal service, your withdrawals are unlimited, but must be 30 days apart.

Ask Carolyn For The Entire Article [email protected] What is your “Federal Retirement Destiny” By Vincent J. Bono, J.D. If you have ever attended one of our complimentary federal employee pre-retirement strategy webinars, one of the topics we cover is alternatives to your TSP Funds. The reason we added this section to our webinars is because, with the market at all-time highs, now might be a good time to lock-in your TSP gains on a tax free basis and put that money in a place where it can participate in the upside of the stock market, but without any downside risk due to “market conditions”. Basically, you have three TSP options when you leave federal service, but the decisions you make now (or fail to make as the case may be) can significantly impact your “Retirement Destiny”. Let me preface the rest of this article by assuring you that I do not sell anything to federal employees so if you are expecting a “sales pitch”, it won’t be from me. Our job at Federal Employee Advocates is to help you better plan for your retirement and we do not charge federal employees for any of our services. Now back to your three TSP options:

Leave your money in the TSP and take withdrawals. This is risky because unless it is all in the G Fund you can lose money. Historically the G Fund Averages about 2.5% Swap out your TSP money for a guaranteed income. This is a MetLife “Single Premium Immediate Annuity” This is risky because if you need money for an emergency, you have no access to it. MetLife now owns your money! Transfer your money to the company of your choice.

What Smart Federal Employees Do To Better Plan For Their Retirement Rule Number 1 They never risk any of their retirement money. Rule Number 2 They never, ever forget Rule Number 1 Now is the perfect time to build a “Bullet-Proof” Federal Retirement With the stock market experiencing extreme volatility, federal employees should consider putting their money in a place that still participates in the upside of the stock market but with zero downside stock market risk and no possibility of having prior games Clawed-Back. If you are within 12 years of retirement, Claw-Backs are the most dangerous components of the TSP C, S, I, F & L Funds.

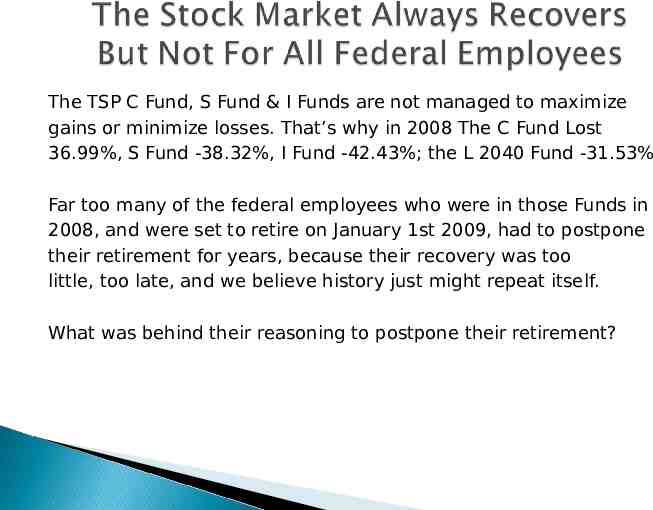

The TSP C Fund, S Fund & I Funds are not managed to maximize gains or minimize losses. That’s why in 2008 The C Fund Lost 36.99%, S Fund -38.32%, I Fund -42.43%; the L 2040 Fund -31.53% Far too many of the federal employees who were in those Funds in 2008, and were set to retire on January 1st 2009, had to postpone their retirement for years, because their recovery was too little, too late, and we believe history just might repeat itself. What was behind their reasoning to postpone their retirement?

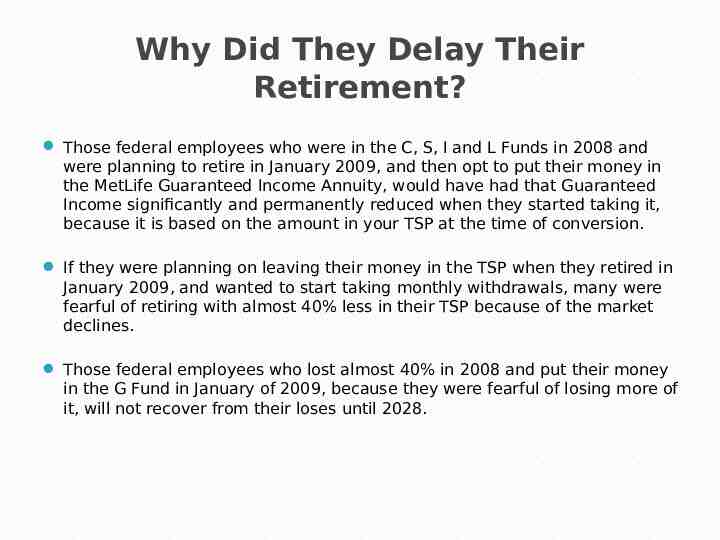

Why Did They Delay Their Retirement? Those federal employees who were in the C, S, I and L Funds in 2008 and were planning to retire in January 2009, and then opt to put their money in the MetLife Guaranteed Income Annuity, would have had that Guaranteed Income significantly and permanently reduced when they started taking it, because it is based on the amount in your TSP at the time of conversion. If they were planning on leaving their money in the TSP when they retired in January 2009, and wanted to start taking monthly withdrawals, many were fearful of retiring with almost 40% less in their TSP because of the market declines. Those federal employees who lost almost 40% in 2008 and put their money in the G Fund in January of 2009, because they were fearful of losing more of it, will not recover from their loses until 2028.

Enhanced Fixed Indexed Annuities They are Safe & Secure Like your TSP C, S, I & L Funds, they participate in the upside of the Stock Market. Unlike those TSP Funds, they can not lose money due to “Market Conditions”. Unlike those TSP Funds, they can not have prior gains “Clawed Back” due to “Market Conditions”. Unlike the MetLife Annuity Income Option YOU OWN THE MONEY!

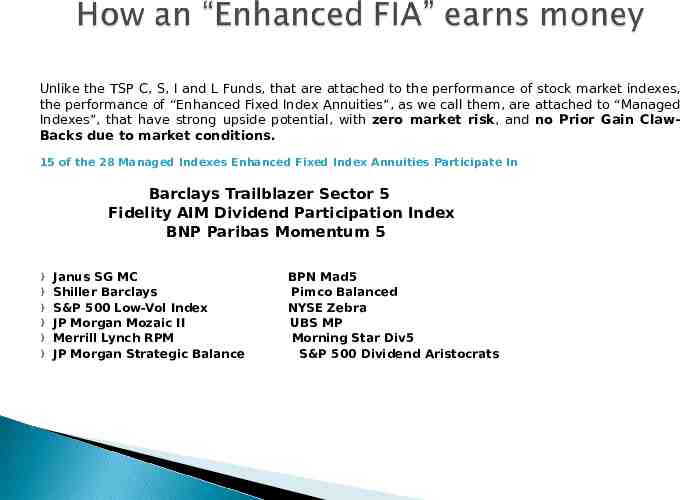

Unlike the TSP C, S, I and L Funds, that are attached to the performance of stock market indexes, the performance of “Enhanced Fixed Index Annuities”, as we call them, are attached to “Managed Indexes”, that have strong upside potential, with zero market risk, and no Prior Gain ClawBacks due to market conditions. 15 of the 28 Managed Indexes Enhanced Fixed Index Annuities Participate In Barclays Trailblazer Sector 5 Fidelity AIM Dividend Participation Index BNP Paribas Momentum 5 } } } } } } Janus SG MC Shiller Barclays S&P 500 Low-Vol Index JP Morgan Mozaic II Merrill Lynch RPM JP Morgan Strategic Balance BPN Mad5 Pimco Balanced NYSE Zebra UBS MP Morning Star Div5 S&P 500 Dividend Aristocrats