LRA Tax Practitioner Training Module VII International Taxation

58 Slides597.50 KB

LRA Tax Practitioner Training Module VII International Taxation Liberia Revenue Authority Monrovia

CONTENTS 1. Introduction to International Taxation (Slides 3-7) 2. International Taxation under the Liberia Revenue Code (Slides 8-16) 3. Model Tax Conventions (Slides 17-20) 4.Double Taxation (Slides 21-31 5. Tax Treaties (Slides 32-34) 6. Transfer Pricing (Slides 35-48) 7. Exchange of Information (49-56) 8. Base Erosion and Profit Shifting (57-65) 2

1.1 Introduction to International Taxation: What is international taxation? International taxation is the study of cross-border tax effects and complications that arise when commercial enterprises and individuals perform economic and financial activities in different countries during a particular tax year. IBFD defines: “International Tax is best regarded as the body of legal provisions of different countries that covers the tax aspects of cross – border transactions.” According to Wikipedia “International taxation is the study or determination of tax on a person or business subject to the tax laws of different countries, or the international aspects of an individual country's tax laws as the case may be.” 3

1.2 Introduction to International Taxation: Who are affected by international taxation? Companies and individuals involved in business activities such as sales, purchases, investments, and fund transfers outside their home countries, could be affected by international taxation. Governments and their institutions need to be aware of how international tax principles could affect revenue collection in their countries. 4

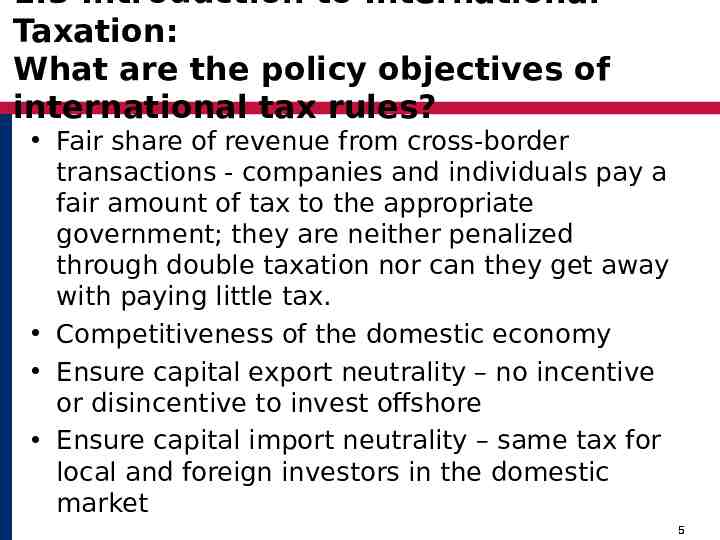

1.3 Introduction to International Taxation: What are the policy objectives of international tax rules? Fair share of revenue from cross-border transactions - companies and individuals pay a fair amount of tax to the appropriate government; they are neither penalized through double taxation nor can they get away with paying little tax. Competitiveness of the domestic economy Ensure capital export neutrality – no incentive or disincentive to invest offshore Ensure capital import neutrality – same tax for local and foreign investors in the domestic market 5

Taxation: What do you need to know to understand international taxation? Domestic tax laws of states that have singed a tax treaties Model tax treaties (OECD, UN, ATAF, US) Model tax treaties developed by contracting states Tax treaties singed by the contracting states Contracts signed or agreements negotiated between a government and the foreign investors, (ex. Bilateral Investment Treaty) Regional economic and tax agreements Transfer pricing regulations, (Advance Pricing Agreements) Global Forum on Transparency and Exchange of Information for Tax Purposes Multilateral Conventions, (MAC, MLI, etc) US Legislation - Foreign Account Tax Compliance Act (FATCA) BEPS Action Plans 6

2.1 International Taxation under the LRC: General provisions Liberia’s domestic tax law is the Liberia Revenue Code (LRC) LRC contains provisions relating to international taxation Particularly Chapter 8 of the LRC is dedicated to international taxation It deals with taxation of non-residents Non-resident pays tax only on Liberian source income while residents pay tax on worldwide income LRC has also made provisions to avoid double taxation on income paid by resident abroad 7

2.2 International Taxation under the LRC: Resident natural person A natural person is resident in Liberia if he: has a normal place of abode in Liberia and is present in Liberia at any time during the tax year is present in Liberia on more than 182 days in a 12-month period, or is an employee or an official of the GOL posted abroad during the tax year 8

2.3 International Taxation under the LRC: Resident legal person A legal person is a resident in Liberia if it is: incorporated or formed under the laws of Liberia and either has its management and control in Liberia; or undertakes the majority of its operations in Liberia a corporation, registered business company, limited liability company, foundation, trust, limited partnership, or similar arrangement that undertakes some business activity in Liberia and has a majority (by vote or value) of direct or indirect shareholders, members, beneficiaries or unit holders resident in Liberia; or a general partnership, joint venture, or trust, and a partner, co-venturer, or trustee is a resident in Liberia. 9

2.4 International Taxation under the LRC: Non-resident A nonresident person is a person who is not a resident of Liberia during the tax year. 10

2.5 International Taxation under the LRC: Permanent establishment The permanent establishment of a nonresident person in Liberia is the establishment through which it carries on business activity in Liberia, in full or in part, for a period of no less than 90 days during the tax year, including activity carried out through an agent. 11

2.6 International Taxation under the LRC: Examples of a PE under the LRC A branch office of a nonresident legal person A construction site, an assembly or batching facility or the exercise of supervisory activities connected with the site or facility A site, drilling equipment, or ship used for prospecting for natural resources or the exercise of supervisory activities connected with the site, equipment, or ship A ship used for fishing in Liberian waters A place used by a nonresident natural person for business activity 12

2.7 International Taxation under the LRC: Liberia-source income of nonresident A nonresident person is subject to tax on Liberia-source income, which includes the following incomes derived from/in: an activity which occurs in Liberia respect of the performance of services or employment exercised in Liberia whether or not the gains or profits from the services or employment are received in Liberia real property located in Liberia disposal of the interest of a shareholder, partner, or beneficiary in a company, partnership, or trust, resident in Liberia rental of personal property used in Liberia derived from the sale or license of industrial or intellectual property used in Liberia Interest, dividend, management fee, or director’s fee, a pension or annuity, a natural resource payment 13

2.8 International Taxation under the LRC: Withholding tax on non-residents Tax on non-resident is collected by withholding on payments at the following rates: Interest, Dividends, Royalties, License Fees, and Similar Payments – 15% Gaming Winnings – 20% Rent -15% Payments for Services – 15% Payments by Mining, Petroleum, and Renewable Resource Projects and Registered Manufacturers: interest 5%, dividends 5% service fees 6% Payments of Acquisition Price -15% 14

2.9 International Taxation under the LRC: Avoidance of double taxation on residents A taxpayer in Liberia may claim a foreign tax credit for amounts of income tax paid to a foreign government on foreign source income. The amount of foreign tax paid or accrued is creditable against Liberian income tax otherwise due. The amount of the credit is limited to the amount of tax that would otherwise be charged on that income at the income tax rates in effect for that tax year, using the taxpayer’s average rate of tax paid. The foreign tax credit is determined on a country-bycountry basis. Credit is available only for a foreign tax that is an income tax or imposed in lieu of an income tax. 15

3.1 Model Tax Conventions: What are model tax conventions? Model Tax Conventions are models that are used to develop International Double Taxation Agreements. There are different models as follows: – The United Nations Model (United Nations Model Income and Capital Tax Convention) – The Organization for Economic Cooperation and Development (OECD) Model Tax Convention on Income and on Capital) – US Model Tax Convention – African Tax Administration Forum (ATAF) Model Tax Convention. UN and OECD Models are commonly used. . 16

3.2 Model Tax Conventions: Why model tax conventions? Model tax conventions are used as starting point for negotiations between two countries. The language used in such models is crucial for both parties. Commentaries and technical explanations assist greatly in the interpretation of a model treaty. The treaty models do not necessarily guarantee that the tax treaties will remain the same for countries adopting it. Some articles could change or be adjusted to particular geopolitical and internal tax policy circumstances agreed by countries during negotiations. 17

3.3 Model Tax Conventions: What is the legal status of bilateral tax treaties? Normally, International Double Taxation Agreements take precedence over national tax legislation But it is recommended that country tax legislation incorporates tax treaty main definitions and considerations for reinforcement and tax policy consistency. 18

3.4 Model Tax Conventions: Why bilateral tax treaties? Bilateral tax treaties’ general aim is to promote international trade and business activities. They do not impose taxation, only provide relief from excessive taxation. More specifically tax treaties have the following objectives: – To eliminate or minimize international juridical double taxation. – To prevent fiscal evasion and avoidance – To eliminate or minimize discriminatory treatment. – To improve the administration of taxes amongst countries. – To obtain a fair division of rents or revenues for stakeholders. 19

4.1Double Taxation: General introduction Double taxation can take two forms as follows: Economic double taxation: Same income is being taxed twice in the hands of two different taxpayers. Example: state A taxes profits of a subsidiary and also taxes dividends distributed to parent company. Juridical double taxation: It occurs when two or more states apply similar taxes upon the same taxpayer with respect to an identical taxable event and for a matching taxable year. Example: Dividends paid to a non-resident shareholder may be taxed in the source state and residence state. 20

4.2: Double Taxation: Why does nternational double taxation arise? International double taxation may arise because of the selection of different tax bases by different countries. Some countries levy tax on income originated within their boundaries while some counties levy tax on the worldwide income of their residents. Source or origin rule: which tax all revenues produced within a nation without distinction of nationality. Residence or tax domicile of the taxpayer: taxing worldwide income. Nationality: the national of a country is taxed no matter where they are located and therefore taxed on worldwide income. 21

4.3 Double Taxation: Why does international double taxation arise? an example Let us suppose, “Liberia XYZ Company” also carries out business in Ghana through a subsidiary called “ABC Ghana”. Ghana levies tax on the profits generate by “ABC Ghana” in Ghana on the basis of source principle. On the other hand, Liberia levies tax on the total profits of “Liberia XYZ Company”, including its profit generated through “ABC Ghana” in Ghana on the basis of the residence principle. Income generated by “ABC Ghana” is taxed twice, first in Ghana and then in Liberia 22

4.4 Double Taxation: How can international double taxation be avoided? International double taxation can be avoided through: Unilateral relief, or bilateral agreements 23

4.5 Double Taxation: Avoidance of double taxation through unilateral relief International double taxation can be avoided trough unilateral relief. Under this system, a country can grant different types of exemptions, incentives or reliefs to foreign investors through the domestic tax law. A country can also provide reliefs for the tax paid by its residents abroad through the domestic tax law. 24

4.6 Double Taxation: Avoidance of double taxation through a tax treaty International double taxation can also be avoided by completing bilateral tax agreements. Under the bilateral tax agreement either foreign source income is exempt from domestic tax or tax paid in abroad is deducted while determining the domestic tax liability or a credit is provided for tax paid overseas. Bilateral treaties are considered more effective than the unilateral measures in avoiding international double taxation, which is necessary for the promotion of international economic activities. 25

4.7 Double Taxation: What are the methods of avoidance of double taxation? Exemption method Deduction Method Credit Method Tax Sparing 26

4.8 Double Taxation: What is an exemption method? Under the exemption method, foreign source income of a resident is exempt from the domestic tax liability. It is not considered while calculating the tax liability of a resident taxpayer. For example, if a taxpayer has both the domestic source and foreign source income, the latter is not considered while calculating the taxpayer's domestic tax liability. The exemption method looks at income side. 27

4.9 Double Taxation: What is a deduction method? Under the tax deduction system, foreign source income is added to the total taxable incomes of the resident However foreign taxes are deducted in order to arrive at the net income. This is the least effective method to avoid international double taxation. 28

4.10 Double Taxation: What is a tax credit method? Under the tax credit system, tax is levied on the total income of resident, irrespective of its origin and a credit is allowed for the tax paid in the source country. Credit may be granted in two forms: full credit or ordinary credit Under the full credit system, resident taxpayers are allowed to deduct from the domestic tax liability the total amount of tax paid in the other countries. Under the ordinary credit system, the maximum deduction would be the tax to be levied at the rate of the residence country. 29

4.11 Double Taxation: What is tax sparing? State give tax credit or allowances for source State tax that was exempted - To support investment promotion initiatives of the source state. Some investors might not benefit from these credits or allowances if its home government increases the investor’s tax liability compared to the allowances granted by the host government. Tax sparing clauses may be included in tax treaties to ensure that investors take full advantage of certain types of tax allowances or credits. Countries increasingly are reluctant to grant tax sparing 30

5.1 Tax Treaties: How are model tax treaties structured? UN MODEL TAX CONVENTION Article 1 Persons covered Article 2 Taxes covered Article 3 General definitions Article 4 Resident Article 5 Permanent establishment Article 6 Income from immovable property Article 7 Business profits Article 8 International shipping and air transport (alternative A and B) Article 9 Associated enterprises Article 10 Dividends Article 11 Interest Article 12 Royalties Article 12A Fees for technical services Article 13 Capital gains Article 14 Independent personal services Article 15 Dependent personal services 31

5.2 Tax Treaties: How are model tax treaties structured? UN MODEL TAX CONVENTION Article 16 Directors’ fees and remuneration of top-level managerial officials Article 17 Artistes and sportspersons Article 18 Pensions and social security payments (alternative A and B) Article 19 Government service Article 20 Students Article 21 Other income Article 22 Capital Article 23A Exemption method Article 23 B Credit method Article 24: Non-discrimination Article 25: Mutual agreement procedure (alternative A and B) Article 26: Exchange of information Article 27: Assistance in the collection of taxes Article 28: Members of diplomatic missions and consular posts Article 29: Entitlement to benefits Article 30: Entry into Force Article 31: Termination 32

5.3 Tax Treaties: Tax treaties in practice Different countries around the world have completed bi-lateral tax treaties Currently, there are over 3500 bilateral tax treaties around the globe Liberia has completed its first bilateral tax treaty with Germany in 1970. Liberia also has singed a treaty exempting shipping and aircraft earnings from double taxation with the United States of America in 1982. Liberia has bilateral investment treaties with France, Belgium, Switzerland and Luxembourg A treaty to avoid double taxation on shipping and aircraft income is in force with New Zealand. Liberia has singed bilateral tax treaties with the United Arab Emirates and the Kingdom of Morocco, which are yet to be ratified by the National Legislature. Liberia also has initiated a process of negotiating bilateral tax treaty with Qatar 33

6.1 Transfer Pricing: Definition of transfer pricing Transfer pricing refers to practice of setting a price for transactions between two or more units under a common ownership. For example, let us suppose XYZ Auto Company has two Units: Battery Unit and Auto Unit. Battery Unit produces batteries while Auto Unit produces cars. Battery Unit can sell batteries to the Auto Unit within the same entity as well as it can sell externally to the independent customers in the market. Similarly, Auto Unit can buy batteries as its intermediate product internally from the Battery Unit as well as externally in the market. Price charged by the Battery Unit to the Auto Unit or price paid by the Auto Unit to the Battery Unit is transfer pricing. 34

6.2 Transfer Pricing: Definition of transfer pricing Different units under a common ownership could be different divisions of an entity. They may also be head quarter and its branch or a parent and its subsidiary. Different units may also be different subsidiaries under a common ownership. These units are called related parties, or associated enterprises. Different units under a common ownership may be located in one tax jurisdiction or different tax jurisdictions. Transfer pricing involving cross border transactions within a multinational enterprise (MNEs) has attracted much attention in the recent times. 35

6.3 Transfer Pricing: MNEs and transfer pricing Transfer pricing is considered the most relevant issue that MNEs and foreign controlled corporations face within international taxation. Tax administrations should be technically prepared to deal with MNEs’ transfer pricing transactions, so the tax official’s approach is effective and professional when assessing tax treatments as per national and bilateral tax treaties. Transfer pricing issues are complex and require thorough analysis so it is important that international corporations and tax administrations design policies in a way they are fair to all stakeholders. 36

6.4 Transfer Pricing: Transfer pricing problems Basic transfer pricing problem: Loss of tax through shifting income (or tax base) between two related (non-arms length) parties with different tax rates by: – transferring income or revenue to low tax rate party; and/or – transferring deductions or costs to high tax rate party Internationally agreed solution to transfer pricing problems – The Arm’s Length Principle 37

6.5 Transfer Pricing: Transfer pricing challenges Transfer of tangibles or trade in goods at non-armslength price is a concern from taxation point of view Transfer of intangibles poses even bigger problem Excessive royalties for right to use industrial, technical or artistic rights (patents, trademarks, designs, etc.) Intra-group services such as management/technical fees, marketing, consultancy advice, accounting, etc. at non-arms length prices Intra-group debt 38

6.6 Transfer Pricing: Addressing the problem of transfer pricing The standard to be applied to determine the true taxable income of a controlled taxpayer is that of a taxpayer dealing at arm’s length with an uncontrolled taxpayer 39

6.11 Transfer Pricing: Transfer pricing under Liberia’s tax laws Liberia has developed and gazetted its Transfer Pricing Regulation in 2016 The Regulation has its legal basis in Section 211 of the Liberia Revenue Code as Amended. The Regulation is largely patterned/guided by the OECD Multilateral Convention on Income and Capital and the United Nations Multilateral Convention on Income and Capital for Developing Countries as revised for time to time. 40

7.1 Exchange of Information for Tax Purposes: A Necessity Exchange of information for tax purposes is necessary to: detect and address domestic and international tax evasion and avoidance; facilitate detection and deterrence of illegal financial flows; obtain domestic synergies i.e. third party reporting for tax purposes may be leveraged to support anticorruption initiatives improve reputation and confidence in and integrity of a Government’s regulatory systems, particularly with regard to commitment to transparency and to addressing socio-economic equity and fairness; 41

7.2 Exchange of Information for Tax Purposes: Required information As an example, for purposes of enforcing income tax legislation of a jurisdictions, the following information may be required to ensure full compliance: Statements of income and expenses Ownership structures to identify beneficial ownership Information on economic activity of resident persons undertaken in a foreign jurisdiction Identities of beneficiaries of income in foreign transparent entities 42

7.3 Exchange of Information: Automatic Exchange of Information Automatic Exchange of Information (AEOI) is the exchange of information between jurisdictions without having to request it. It involves systematic and periodic transmission of bulk taxpayer information between jurisdictions Automatic exchanges normally occur on an annual basis based on the fiscal year of the source country There is global momentum towards AEOI AEOI standard has the potential for improving global tax enforcement Much more challenging standard for countries to meet than the current standard of “exchange of information on request” followed in most Double Tax Agreements. 43

7.4 Exchange of Information: Global forum on transparency and exchange of information for tax purposes The OECD Global Forum on Transparency and Exchange of Information for Tax Purposes is the leading international body working on the implementation of global transparency and exchange of information standards around the world. Major contributions of the Global Forum include: - Develop guidance for common reporting such as automatic exchange of financial account information and exchange of information on request. - Promotion of the automatic exchange of information standard as the global benchmark Its area of focus is on tax havens, offshore financial centers, tax information exchange agreements, money laundering and tax evasion. 162 tax jurisdictions have become members of Global Forum by February 2021. 44

7.5 Exchange of Information: Global forum peer review assessment criteria for exchange of information upon request Competent authority availability and access to ownership and identity information in their jurisdiction; Reliability of accounting records maintained in their jurisdictions; Access to banking information; Competent authorities should have the power to obtain and provide information that is the subject of a request; The taxpayer rights and safeguards should be provided for e.g. notification, appeal rights etc.; Exchange of information mechanisms should provide for effective exchange of information. The jurisdictions’ network of information exchange mechanisms should cover all relevant partners. 45

7.6 Exchange of Information: Convention on mutual administrative assistance in tax matters Government of Liberia has ratified the Convention on Mutual Administrative Assistance in Tax Matters. Its objective is, among other things, is to enable jurisdiction exchange tax information automatically. This is a coordinated effort between Liberia and other States to foster all forms of administrative assistance in matters concerning taxes, whilst at the same time ensuring adequate protection of the rights of taxpayers. 46

7.7: Exchange of Information: US Legislation - Foreign Account Tax Compliance Act (FATCA) FATCA was enacted in 2010 by the US Congress to target non-compliance by U.S. taxpayers using foreign accounts. FATCA requires foreign financial institutions to report to the US Internal Revenue Service information about financial accounts held by U.S. taxpayers, or by foreign entities in which U.S. taxpayers hold a substantial ownership interest. U.S. financial institutions and other U.S withholding agents must both withhold 30% on certain payments to foreign entities that do not comply with FATCA obligations. Foreign financial institutions are encouraged to either directly register with the IRS to comply with the FATCA regulations or comply with the FATCA Intergovernmental Agreements as applicable to their jurisdictions. 47

7.8 Exchange of Information: Inter-governm agreements Inter-Governmental Agreements with partner jurisdictions facilitate the effective and efficient implementation of FATCA. They overcome domestic legal impediments to compliance; and They reduce burdens on foreign financial institutions in partner jurisdictions. Two model Inter-Governmental Agreements developed to implement FATCA: Model 1- Foreign financial institution reports to foreign government and the foreign government reports to US Internal Revenue Service Model 2 - Foreign financial institution reports directly to US Internal Revenue Service 48

8.1 Base Erosion and Profit Shifting : Background (I) Multi-national enterprises operate in various countries with different level of taxation. They move their profits from high to no or low tax jurisdiction through intra-group transactions in order to avoid corporate income tax. It reduces government revenue and country’s ability to pay for hospitals, schools, road, and other public services. This led to an unprecedented public attention on the corporate income tax around the world in the recent past. 49

8.2 Base Erosion and Profit Shifting: Background (II) In 2012, G20 Finance Ministers asked OECD for a diagnosis on BEPS. In 2013, OECD and G20 countries took joint action and developed an action plan to tackle BEPS. BEPS Action Plans with 15 separate work streams were published in 2015 15 BEPS Action Plans are presented in the following slides. 50

8.3 Base Erosion and Profit Shifting: Fifteen Action Plans (1) Action 1:Address the tax challenges of the digital economy Action 2: Neutralize the effects of hybrid mismatch arrangements Action 3: Strengthen CFC rules Acton 4: Limit base erosion via interest deductions and other financial payments Action 5: Counter harmful tax practices more effectively, taking into account transparency and substance Action 6: Prevent treaty abuse Action 7: Prevent the artificial avoidance of PE status Action 8: Assure that transfer pricing outcomes are in line with value creation – Intangibles 51

8.4 Base Erosion and Profit Shifting: Fifteen Action Plans (I1) Action 9: Assure that transfer pricing outcomes are in line with value creation – Risks and capital Action 10: Assure that transfer pricing outcomes are in line with value creation – Other high-risk transactions Action 11: Establish methodologies to collect and analyses data on BEPS and the actions to address it Action12: Require taxpayers to disclose their aggressive tax planning arrangements Action13: Re-examine transfer pricing documentation Action14: Make dispute resolution mechanisms more effective Action15: Develop a multilateral instrument 52

8.5 Base Erosion and Profit Shifting: Introduction to multilateral instrument BEPS Action Plan 15 is related to the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting. It is popularly knowns as "Multilateral Instrument" or "MLI“. As it is time consuming to amend bilateral tax treaties, MLI is used to quickly implement a series of tax treaty measures to update international tax rules and lessen the opportunity for tax avoidance by multinational enterprises. MLI entered into force on 1 July 2018. As of February 18, 1921, 95 tax jurisdictions all over the world have signed MLI and others are considering to adopt it. Liberia is yet to sign MLI. The structure of MLI is given in the following slides. 53

8.6 Base Erosion and Profit Shifting: Structure of multilateral instrument (1) Article 1 – Scope of the Convention Article 2 – Interpretation of Terms Article 3 –Transparent Entities Article 4 – Dual Resident Entities Article 5 – Application of Methods for Elimination of Double Taxation Article 6 – Purpose of a Covered Tax Agreement Article 7 – Prevention of Treaty Abuse Article 8 – Dividend Transfer Transactions Article 9 – Capital Gains from Alienation of Shares or Interests of Entities Deriving their Value Principally from Immovable Property Article 10 – Anti-abuse Rule for Permanent Establishments Situated in Third Jurisdictions 54

8.7 Base Erosion and Profit Shifting: Structure of multilateral instrument (II) Article 11 – Application of Tax Agreements to Restrict a Party’s Right to Tax its Own Residents Article 12 – Artificial Avoidance of Permanent Establishment Status through Commissionaire Arrangements and Similar Strategies Article 13 – Artificial Avoidance of Permanent Establishment Status through the Specific Activity Exemptions Article 14 – Splitting-up of Contracts Article 15 – Definition of a Person Closely Related to an Enterprise Article 16 – Mutual Agreement Procedure Article 17 – Corresponding Adjustments Article 18 – Choice to Apply Part VI 55

8.8 Base Erosion and Profit Shifting: Structure of multilateral instrument (III) Article 19 – Mandatory Binding Arbitration Article 20 – Appointment of Arbitrators Article 21 – Confidentiality of Arbitration Proceedings Article 22 – Resolution of a Case Prior to the Conclusion of the Arbitration Article 23 – Type of Arbitration Process Article 24 – Agreement on a Different Resolution Article 25 – Costs of Arbitration Proceedings Article 26 – Compatibility Article 27 – Signature and Ratification, Acceptance or Approval Article 28 – Reservations 56

8.9 Base Erosion and Profit Shifting : Structure of multilateral instrument (IV) Article 29 – Notifications Article 30 – Subsequent Modifications of Covered Tax Agreements Article 31 – Conference of the Parties Article 32 – Interpretation and Implementation Article 33 – Amendment Article 34 – Entry into Force Article 35 – Entry into Effect Article 36 – Entry into Effect of Part VI Article 37 - Withdrawal Article 38 – Relation with Protocols Article 39 – Depositary 57

END OF MODULE 07 ON INTERNATIONAL TAXATION THANK YOU! 58