Structuring the Deal: Tax and Accounting Considerations

27 Slides158.50 KB

Structuring the Deal: Tax and Accounting Considerations

One person of integrity can make a difference, a difference of life and death. — Elie Wiesel

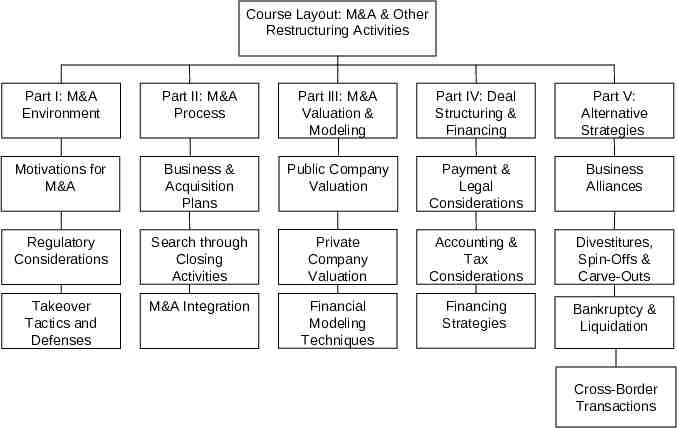

Course Layout: M&A & Other Restructuring Activities Part I: M&A Environment Part II: M&A Process Part III: M&A Valuation & Modeling Part IV: Deal Structuring & Financing Part V: Alternative Strategies Motivations for M&A Business & Acquisition Plans Public Company Valuation Payment & Legal Considerations Business Alliances Regulatory Considerations Search through Closing Activities Private Company Valuation Accounting & Tax Considerations Divestitures, Spin-Offs & Carve-Outs Takeover Tactics and Defenses M&A Integration Financial Modeling Techniques Financing Strategies Bankruptcy & Liquidation Cross-Border Transactions

Learning Objectives Primary Learning Objective: To provide students with knowledge of how accounting treatment and tax considerations impact the deal structuring process. Secondary Learning Objectives: To provide students with knowledge of – Purchase (acquisition method) accounting used for financial reporting purposes; – Goodwill and how it is created; and – Alternative taxable and non-taxable transactions.

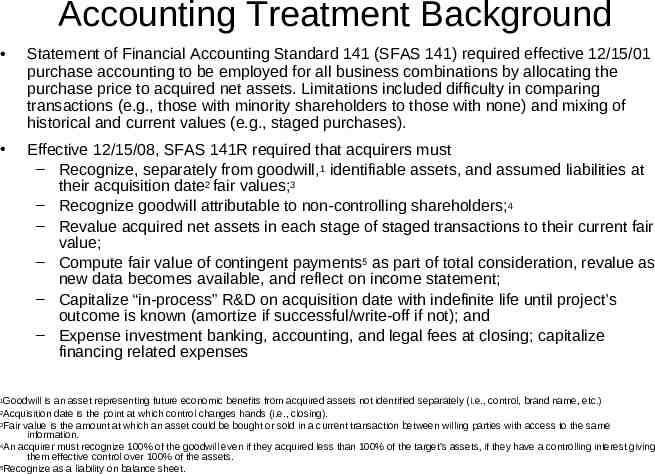

Accounting Treatment Background Statement of Financial Accounting Standard 141 (SFAS 141) required effective 12/15/01 purchase accounting to be employed for all business combinations by allocating the purchase price to acquired net assets. Limitations included difficulty in comparing transactions (e.g., those with minority shareholders to those with none) and mixing of historical and current values (e.g., staged purchases). Effective 12/15/08, SFAS 141R required that acquirers must – Recognize, separately from goodwill,1 identifiable assets, and assumed liabilities at their acquisition date2 fair values;3 – Recognize goodwill attributable to non-controlling shareholders; 4 – Revalue acquired net assets in each stage of staged transactions to their current fair value; – Compute fair value of contingent payments 5 as part of total consideration, revalue as new data becomes available, and reflect on income statement; – Capitalize “in-process” R&D on acquisition date with indefinite life until project’s outcome is known (amortize if successful/write-off if not); and – Expense investment banking, accounting, and legal fees at closing; capitalize financing related expenses Goodwill is an asset representing future economic benefits from acquired assets not identified separately (i.e., control, brand name, etc.) Acquisition date is the point at which control changes hands (i.e., closing). 3Fair value is the amount at which an asset could be bought or sold in a current transaction between willing parties with access to the same information. 4An acquirer must recognize 100% of the goodwill even if they acquired less than 100% of the target’s assets, if they have a controlling interest giving them effective control over 100% of the assets. 5Recognize as a liability on balance sheet. 1 2

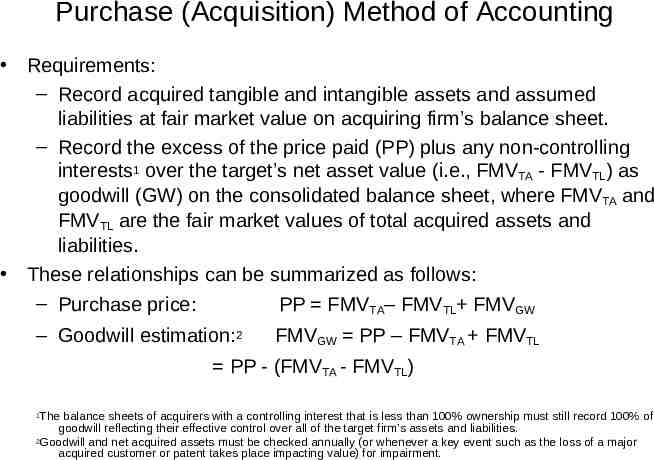

Purchase (Acquisition) Method of Accounting Requirements: – Record acquired tangible and intangible assets and assumed liabilities at fair market value on acquiring firm’s balance sheet. – Record the excess of the price paid (PP) plus any non-controlling interests1 over the target’s net asset value (i.e., FMVTA - FMVTL) as goodwill (GW) on the consolidated balance sheet, where FMVTA and FMVTL are the fair market values of total acquired assets and liabilities. These relationships can be summarized as follows: – Purchase price: PP FMVTA– FMVTL FMVGW – Goodwill estimation:2 FMVGW PP – FMVTA FMVTL PP - (FMVTA - FMVTL) The balance sheets of acquirers with a controlling interest that is less than 100% ownership must still record 100% of goodwill reflecting their effective control over all of the target firm’s assets and liabilities. 2Goodwill and net acquired assets must be checked annually (or whenever a key event such as the loss of a major acquired customer or patent takes place impacting value) for impairment. 1

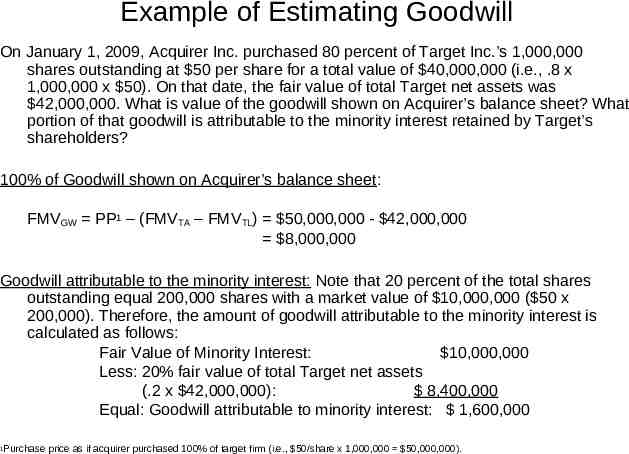

Example of Estimating Goodwill On January 1, 2009, Acquirer Inc. purchased 80 percent of Target Inc.’s 1,000,000 shares outstanding at 50 per share for a total value of 40,000,000 (i.e., .8 x 1,000,000 x 50). On that date, the fair value of total Target net assets was 42,000,000. What is value of the goodwill shown on Acquirer’s balance sheet? What portion of that goodwill is attributable to the minority interest retained by Target’s shareholders? 100% of Goodwill shown on Acquirer’s balance sheet: FMVGW PP1 – (FMVTA – FMVTL) 50,000,000 - 42,000,000 8,000,000 Goodwill attributable to the minority interest: Note that 20 percent of the total shares outstanding equal 200,000 shares with a market value of 10,000,000 ( 50 x 200,000). Therefore, the amount of goodwill attributable to the minority interest is calculated as follows: Fair Value of Minority Interest: 10,000,000 Less: 20% fair value of total Target net assets (.2 x 42,000,000): 8,400,000 Equal: Goodwill attributable to minority interest: 1,600,000 Purchase price as if acquirer purchased 100% of target firm (i.e., 50/share x 1,000,000 50,000,000). 1

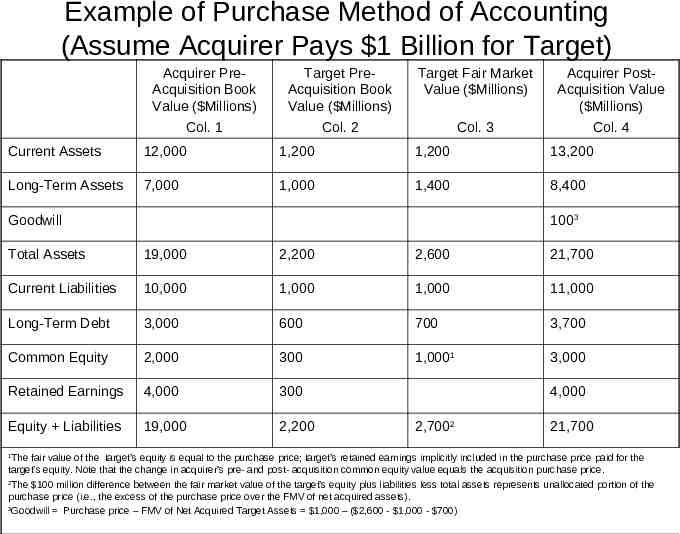

Example of Purchase Method of Accounting (Assume Acquirer Pays 1 Billion for Target) Acquirer PreAcquisition Book Value ( Millions) Col. 1 Target PreAcquisition Book Value ( Millions) Col. 2 Target Fair Market Value ( Millions) Col. 3 Acquirer PostAcquisition Value ( Millions) Col. 4 Current Assets 12,000 1,200 1,200 13,200 Long-Term Assets 7,000 1,000 1,400 8,400 Goodwill 1003 Total Assets 19,000 2,200 2,600 21,700 Current Liabilities 10,000 1,000 1,000 11,000 Long-Term Debt 3,000 600 700 3,700 Common Equity 2,000 300 1,0001 3,000 Retained Earnings 4,000 300 Equity Liabilities 19,000 2,200 4,000 2,7002 21,700 The fair value of the target’s equity is equal to the purchase price; target’s retained earnings implicitly included in the purchase price paid for the target’s equity. Note that the change in acquirer’s pre- and post- acquisition common equity value equals the acquisition purchase price. 2 The 100 million difference between the fair market value of the target’s equity plus liabilities less total assets represents unallocated portion of the purchase price (i.e., the excess of the purchase price over the FMV of net acquired assets). 3 Goodwill Purchase price – FMV of Net Acquired Target Assets 1,000 – ( 2,600 - 1,000 - 700) 1

Discussion Questions 1. 2. 3. Acquirer and Target companies reach an agreement to merge. Describe how the purchase method of accounting would impact the income statement, balance sheet, and cash flows statements of the combined companies. Goodwill is an accounting entry equal to the difference between purchase price and the fair market value of net acquired assets. As a business manager, what do you believe goodwill represents? How could the factors that goodwill represents actually contribute to improving the combined firm’s future cash flows? How might the treatment of contingent payments under SFAS 141R affect the popularity of earnouts from the acquirer’s perspective?

Choosing the Right Deal Structure Consider the Following Factors: – Tax impact (Immediate or Deferred) – Acquirer and Target Shareholder Approvals – Exposure to Target Liabilities – Payment Flexibility – Target Survivability – Limitations on Restructuring Efforts (e.g., tax-free status of spin-offs 2 years before and after tax-free deal could be jeopardized)

Alternative Tax Structures Mergers and acquisitions can be structured as either tax-free, partially taxable, or wholly taxable to target shareholders. Taxable Transactions: – The buyer pays primarily with cash, securities, or other non-equity consideration for the target firm’s stock or assets – Absent a special election, tax basis of target’s assets will not be increased to FMV following a purchase of stock – 338 election: Buyer can elect to have a taxable stock purchase treated as an asset purchase and acquired assets increased to FMV. Taxes must be paid on any gains on acquired assets. – Impact of asset write-up on EPS and potential taxable gains must be weighed against improved cash flow from tax savings Tax-Free Transactions: – Mostly buyer stock used to acquire stock or assets of the target – Buyer must acquire enough of the target’s stock and assets to ensure that the IRS’ continuity of interests and business enterprise principles are satisfied

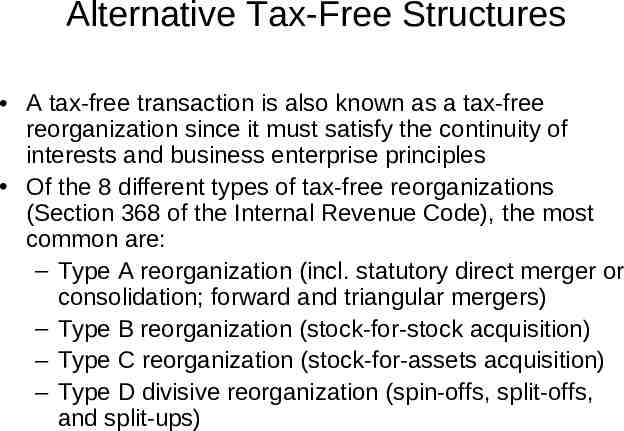

Alternative Tax-Free Structures A tax-free transaction is also known as a tax-free reorganization since it must satisfy the continuity of interests and business enterprise principles Of the 8 different types of tax-free reorganizations (Section 368 of the Internal Revenue Code), the most common are: – Type A reorganization (incl. statutory direct merger or consolidation; forward and triangular mergers) – Type B reorganization (stock-for-stock acquisition) – Type C reorganization (stock-for-assets acquisition) – Type D divisive reorganization (spin-offs, split-offs, and split-ups)

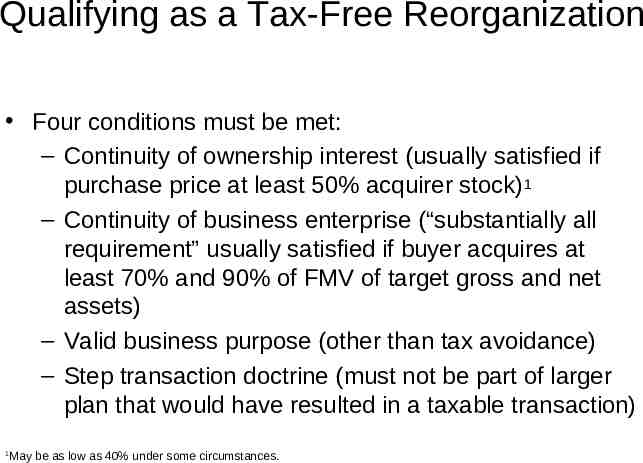

Qualifying as a Tax-Free Reorganization Four conditions must be met: – Continuity of ownership interest (usually satisfied if purchase price at least 50% acquirer stock)1 – Continuity of business enterprise (“substantially all requirement” usually satisfied if buyer acquires at least 70% and 90% of FMV of target gross and net assets) – Valid business purpose (other than tax avoidance) – Step transaction doctrine (must not be part of larger plan that would have resulted in a taxable transaction) May be as low as 40% under some circumstances. 1

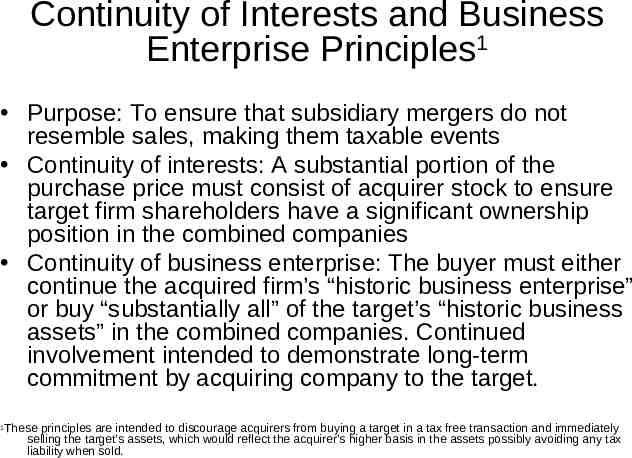

Continuity of Interests and Business Enterprise Principles1 Purpose: To ensure that subsidiary mergers do not resemble sales, making them taxable events Continuity of interests: A substantial portion of the purchase price must consist of acquirer stock to ensure target firm shareholders have a significant ownership position in the combined companies Continuity of business enterprise: The buyer must either continue the acquired firm’s “historic business enterprise” or buy “substantially all” of the target’s “historic business assets” in the combined companies. Continued involvement intended to demonstrate long-term commitment by acquiring company to the target. These principles are intended to discourage acquirers from buying a target in a tax free transaction and immediately selling the target’s assets, which would reflect the acquirer’s higher basis in the assets possibly avoiding any tax liability when sold. 1

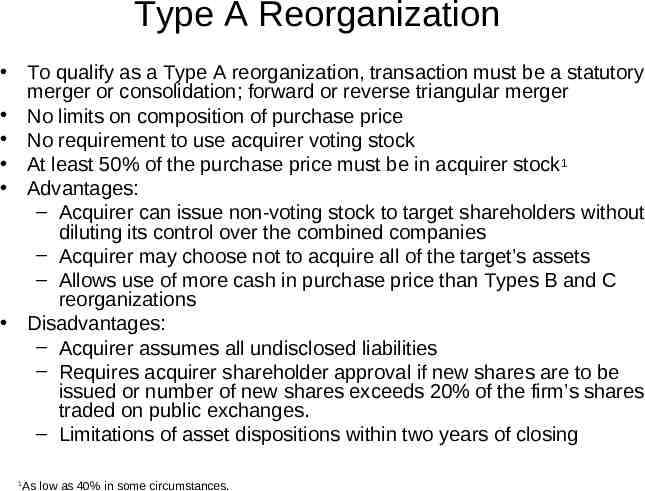

Type A Reorganization To qualify as a Type A reorganization, transaction must be a statutory merger or consolidation; forward or reverse triangular merger No limits on composition of purchase price No requirement to use acquirer voting stock At least 50% of the purchase price must be in acquirer stock1 Advantages: – Acquirer can issue non-voting stock to target shareholders without diluting its control over the combined companies – Acquirer may choose not to acquire all of the target’s assets – Allows use of more cash in purchase price than Types B and C reorganizations Disadvantages: – Acquirer assumes all undisclosed liabilities – Requires acquirer shareholder approval if new shares are to be issued or number of new shares exceeds 20% of the firm’s shares traded on public exchanges. – Limitations of asset dispositions within two years of closing As low as 40% in some circumstances. 1

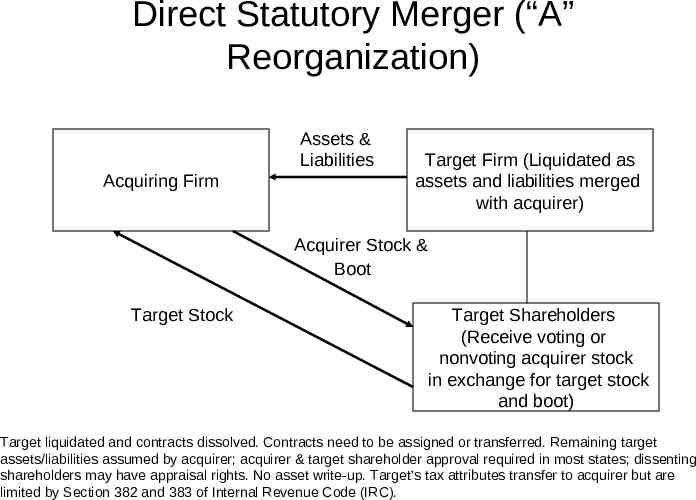

Direct Statutory Merger (“A” Reorganization) Assets & Liabilities Acquiring Firm Target Firm (Liquidated as assets and liabilities merged with acquirer) Acquirer Stock & Boot Target Stock Target Shareholders (Receive voting or nonvoting acquirer stock in exchange for target stock and boot) Target liquidated and contracts dissolved. Contracts need to be assigned or transferred. Remaining target assets/liabilities assumed by acquirer; acquirer & target shareholder approval required in most states; dissenting shareholders may have appraisal rights. No asset write-up. Target’s tax attributes transfer to acquirer but are limited by Section 382 and 383 of Internal Revenue Code (IRC).

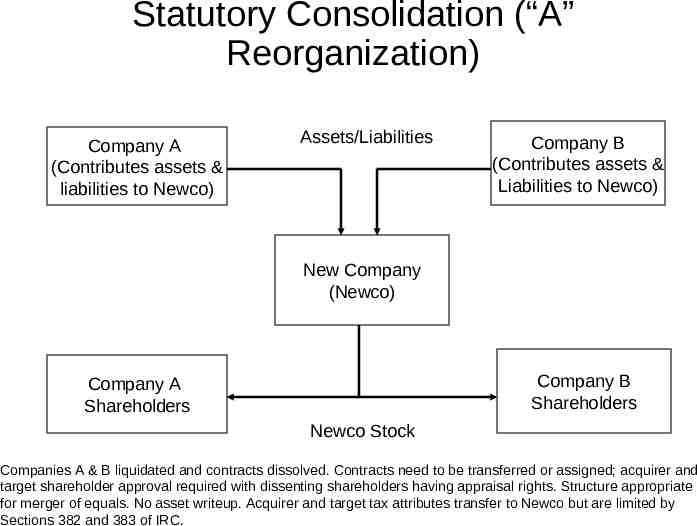

Statutory Consolidation (“A” Reorganization) Company A (Contributes assets & liabilities to Newco) Assets/Liabilities Company B (Contributes assets & Liabilities to Newco) New Company (Newco) Company B Shareholders Company A Shareholders Newco Stock Companies A & B liquidated and contracts dissolved. Contracts need to be transferred or assigned; acquirer and target shareholder approval required with dissenting shareholders having appraisal rights. Structure appropriate for merger of equals. No asset writeup. Acquirer and target tax attributes transfer to Newco but are limited by Sections 382 and 383 of IRC.

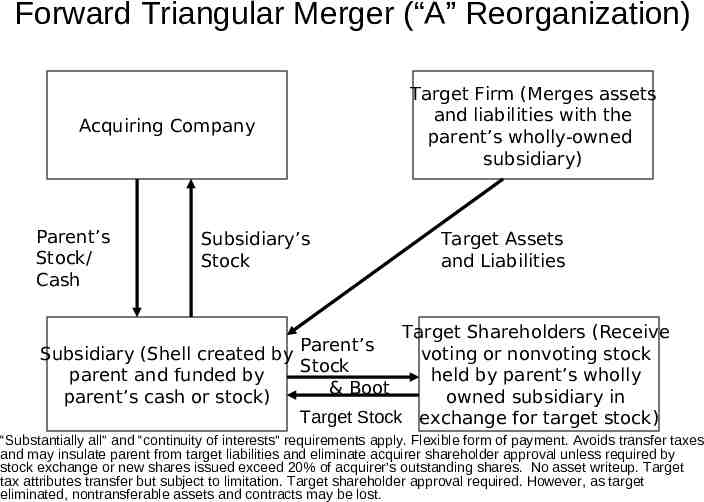

Forward Triangular Merger (“A” Reorganization) Acquiring Company Parent’s Stock/ Cash Subsidiary’s Stock Target Firm (Merges assets and liabilities with the parent’s wholly-owned subsidiary) Target Assets and Liabilities Target Shareholders (Receive Parent’s Subsidiary (Shell created by voting or nonvoting stock Stock parent and funded by held by parent’s wholly & Boot parent’s cash or stock) owned subsidiary in Target Stock exchange for target stock) “Substantially all” and “continuity of interests” requirements apply. Flexible form of payment. Avoids transfer taxes and may insulate parent from target liabilities and eliminate acquirer shareholder approval unless required by stock exchange or new shares issued exceed 20% of acquirer’s outstanding shares. No asset writeup. Target tax attributes transfer but subject to limitation. Target shareholder approval required. However, as target eliminated, nontransferable assets and contracts may be lost.

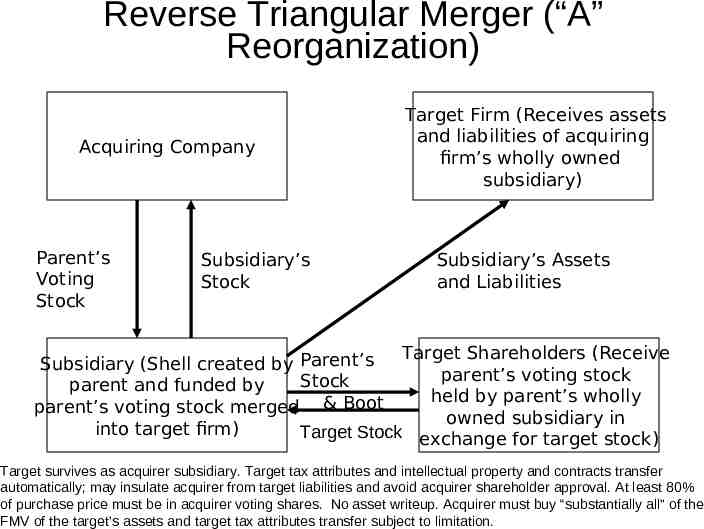

Reverse Triangular Merger (“A” Reorganization) Acquiring Company Parent’s Voting Stock Subsidiary’s Stock Target Firm (Receives assets and liabilities of acquiring firm’s wholly owned subsidiary) Subsidiary’s Assets and Liabilities Target Shareholders (Receive Subsidiary (Shell created by Parent’s parent’s voting stock Stock parent and funded by held by parent’s wholly parent’s voting stock merged & Boot owned subsidiary in into target firm) Target Stock exchange for target stock) Target survives as acquirer subsidiary. Target tax attributes and intellectual property and contracts transfer automatically; may insulate acquirer from target liabilities and avoid acquirer shareholder approval. At least 80% of purchase price must be in acquirer voting shares. No asset writeup. Acquirer must buy “substantially all” of the FMV of the target’s assets and target tax attributes transfer subject to limitation.

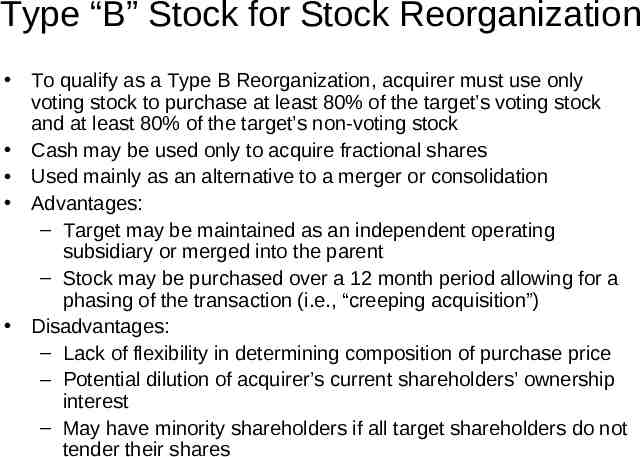

Type “B” Stock for Stock Reorganization To qualify as a Type B Reorganization, acquirer must use only voting stock to purchase at least 80% of the target’s voting stock and at least 80% of the target’s non-voting stock Cash may be used only to acquire fractional shares Used mainly as an alternative to a merger or consolidation Advantages: – Target may be maintained as an independent operating subsidiary or merged into the parent – Stock may be purchased over a 12 month period allowing for a phasing of the transaction (i.e., “creeping acquisition”) Disadvantages: – Lack of flexibility in determining composition of purchase price – Potential dilution of acquirer’s current shareholders’ ownership interest – May have minority shareholders if all target shareholders do not tender their shares

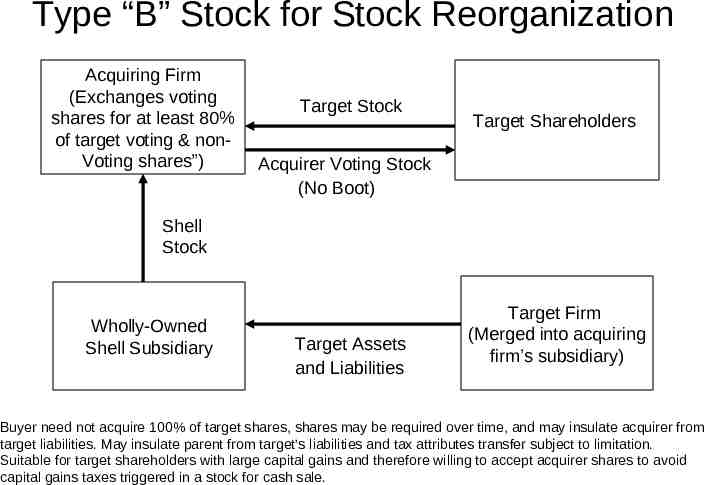

Type “B” Stock for Stock Reorganization Acquiring Firm (Exchanges voting shares for at least 80% of target voting & nonVoting shares”) Target Stock Target Shareholders Acquirer Voting Stock (No Boot) Shell Stock Wholly-Owned Shell Subsidiary Target Assets and Liabilities Target Firm (Merged into acquiring firm’s subsidiary) Buyer need not acquire 100% of target shares, shares may be required over time, and may insulate acquirer from target liabilities. May insulate parent from target’s liabilities and tax attributes transfer subject to limitation. Suitable for target shareholders with large capital gains and therefore willing to accept acquirer shares to avoid capital gains taxes triggered in a stock for cash sale.

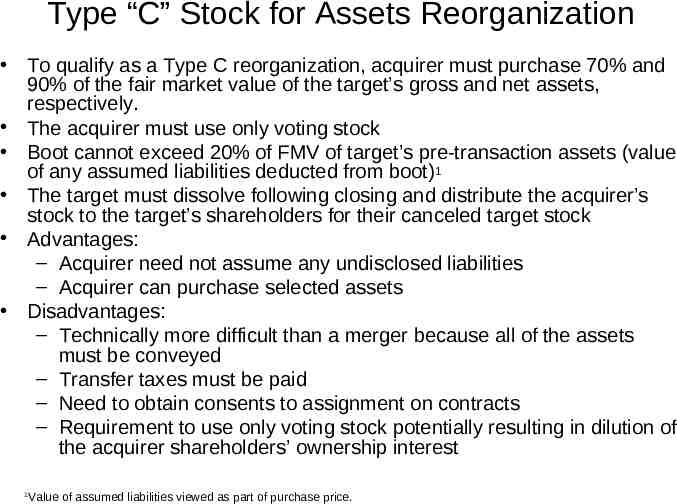

Type “C” Stock for Assets Reorganization To qualify as a Type C reorganization, acquirer must purchase 70% and 90% of the fair market value of the target’s gross and net assets, respectively. The acquirer must use only voting stock Boot cannot exceed 20% of FMV of target’s pre-transaction assets (value of any assumed liabilities deducted from boot)1 The target must dissolve following closing and distribute the acquirer’s stock to the target’s shareholders for their canceled target stock Advantages: – Acquirer need not assume any undisclosed liabilities – Acquirer can purchase selected assets Disadvantages: – Technically more difficult than a merger because all of the assets must be conveyed – Transfer taxes must be paid – Need to obtain consents to assignment on contracts – Requirement to use only voting stock potentially resulting in dilution of the acquirer shareholders’ ownership interest Value of assumed liabilities viewed as part of purchase price. 1

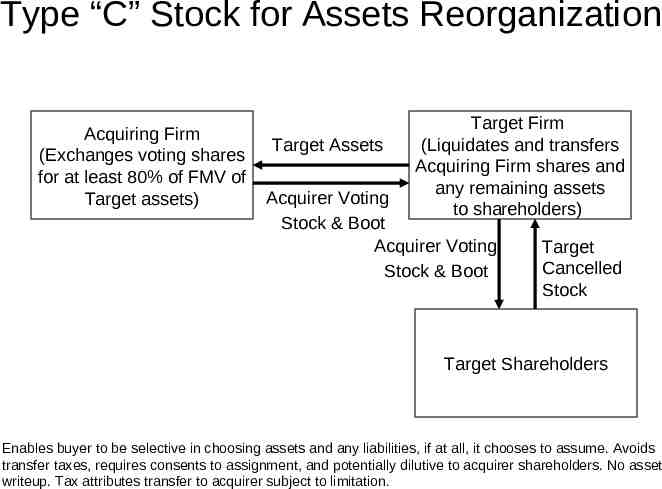

Type “C” Stock for Assets Reorganization Acquiring Firm (Exchanges voting shares for at least 80% of FMV of Target assets) Target Assets Target Firm (Liquidates and transfers Acquiring Firm shares and any remaining assets to shareholders) Acquirer Voting Stock & Boot Acquirer Voting Stock & Boot Target Cancelled Stock Target Shareholders Enables buyer to be selective in choosing assets and any liabilities, if at all, it chooses to assume. Avoids transfer taxes, requires consents to assignment, and potentially dilutive to acquirer shareholders. No asset writeup. Tax attributes transfer to acquirer subject to limitation.

Type D Divisive Reorganizations Type D Divisive Reorganizations apply to spin-offs, split-ups, and split-offs Spin-Off: Stock in a new company is distributed to the original company’s shareholders according to some pre-determined formula. Both the parent and the entity to be spun-off must have been in business for at least five years prior to the spin-off. Split-off: A portion of the original company is separated from the parent, and shareholders in the original company may exchange their shares for shares in the new entity. No new firm created. Split-up: The original company ceases to exist, and one or more new companies are formed from the original business as original shareholders exchange their shares for shares in the new companies. For these reorganizations to qualify as tax-free, the distribution of shares must not be for the purpose of tax avoidance.

Implications of Tax Considerations for Deal Structuring In taxable transactions, target generally demands a higher purchase price Higher purchase price often impacts form of payment as buyer tries to maintain PV of transaction by deferring some of purchase price Buyer may avoid EPS dilution by buying target stock or assets using a non-equity form of payment in a taxable transaction If buyer wants to preserve cash and obtain target’s tax credits, buyer may use its stock to purchase target stock in a non-taxable transaction

Discussion Questions 1. Explain how tax considerations affect the deal structuring process? From seller’s perspective? From buyer’s perspective? 2. What is a Type A reorganization? When does it make sense for a buyer to use a Type A reorganization? 3. What is a reverse triangular merger? Under what circumstances would a buyer wish to use this type of reorganization? 4. How might the buyer structure the transaction in order to avoid EPS dilution? (Hint: Consider the factors that make a transaction taxable or non-taxable.)

Things to Remember For financial reporting purposes, all M&As must be accounted for using purchase accounting. Taxable transactions: – Direct cash merger – Cash purchase of assets – Cash purchase of stock Tax-free transactions: – Type A reorganization (Incl. direct statutory merger or consolidation; forward and reverse triangular merger) – Type B stock-for-stock reorganization – Type C stock-for-assets reorganization