FIVE SECRETS TO A MAGICAL SUB-V 1 2 3 4 5

32 Slides1.57 MB

FIVE SECRETS TO A MAGICAL SUB-V 1 2 3 4 5

WHO WE ARE Kirk Burkley Managing Partner, Bernstein-Burkley, P.C. David Mawhinney Bowditch & Dewey LLP Honorable Catherine Peek McEwen Amy Denton Mayer Shareholder, Stichter, Riedel, Blain & Postler, P.A. USBC, M.D. Fla. (Moderator)

FIVE SECRETS TO A MAGICAL SUB-V 1 Who Goes There? Who shall pass into the magical world of Subchapter V? This “engaging” topic will help you master the eligibility requirements and understand the difference between a “commercial” and “business” activity, and, indeed, what an “activity” is. Which debts make the cut? How are the lesser-known eligibility rules interpreted? 2 The Marvelous, Mysterious Trustee Friend to all, loyal to NONE. Who is this person, the Subchapter V Trustee? What is the extent of their powers? 4 Conjuring Confirmation Master the skills of building consensus, while preparing for a contested confirmation hearing. What sources of proof are sufficient for income projections and feasibility? What constitutes “acceptance” of a plan? What role does the Subchapter V Trustee play in both consensual and contested hearings? 3 Don’t Run Out of Time Debtors beware and do not let 90 days pass without filing your plan, lest the magical world of Subchapter V shall evaporate before your eyes. The secrets to obtaining an extension will be revealed! 5 Remedy for What Ails You. What remedies and default provisions should creditors consider bargaining for in exchange for their yes vote? What “appropriate remedies” should they demand in a non-consensual plan?

OUR MAGICAL MATERIALS 1. Tracking the Up(s) and Down of the SBRA Debt Limit. By Jeffrey Katz (Federal Judicial Intern, Middle District of Florida) 2. How to Effectively Utilize the Subchapter V Trustee to Make Your Subchapter V Case Magical: The Statutory Role of the Subchapter V Trustee, the Subchapter V Trustee as Mediator, and Other Ways to Effectively Utilize the Subchapter V Trustee. By Amy Denton Mayer (Stichter, Riedel, Blain & Postler, P.A) 3. In Their Own Words: Subchapter V Trustees. Compiled by David A. Mawhinney (Bowditch & Dewey LLP) 4. The Enigma of What Circumstances Justify a Subchapter V Plan Filing Deadline Extension. By Nicholas Sellas (Federal Judicial Intern, Middle District of Florida) 5. Role of the Subchapter V Trustee in Demonstrating and Supporting Plan Feasibility. By David A. Mawhinney (Bowditch & Dewey LLP) 6. To Fix or to Float? Projected Disposable Income under Subchapter V. By Michael Harrigan (Federal Judicial Intern, Middle District of Florida) 7. Creditor Remedies Under Subchapter V. By Elizabeth B. (“Lisa”) Vandesteeg (Levenfeld Pearlstein) 8. A Guide to the Small Business Reorganization Act of 2019. By Hon. Paul W. Bonapfel (USBC, N.D. Ga.)

ELIGIBILITY ELIGIBILITY BATTLEGROUNDS Follow the bouncing debt cap. Disqualification by “affiliateness” of public company. Commercial or business activities? Source of the debt? Character of debt?

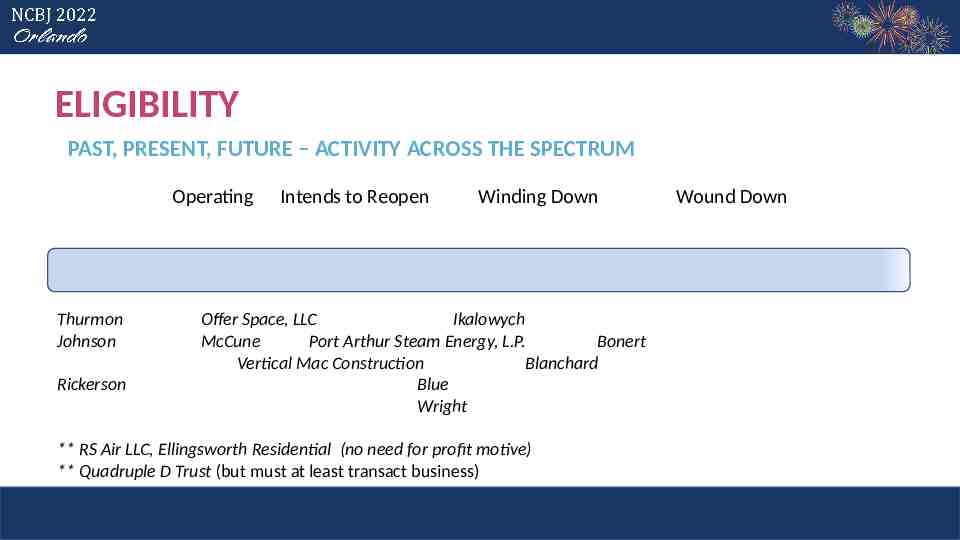

ELIGIBILITY PAST, PRESENT, FUTURE – ACTIVITY ACROSS THE SPECTRUM Operating Thurmon Johnson Rickerson Intends to Reopen Winding Down Offer Space, LLC Ikalowych McCune Port Arthur Steam Energy, L.P. Bonert Vertical Mac Construction Blanchard Blue Wright ** RS Air LLC, Ellingsworth Residential (no need for profit motive) ** Quadruple D Trust (but must at least transact business) Wound Down

ROLE OF THE SUBCHAPTER V TRUSTEE WHO IS THE SUBCHAPTER V TRUSTEE? WHAT IS HIS/HER ROLE? IS THE TRUSTEE FRIEND OR FOE? Fiduciary for the estate. Absent expansion of the Subchapter V Trustee’s powers by the court, the debtor remains in possession and the Subchapter V Trustee’s duties are largely supervisory in nature. Subchapter V Trustee is statutorily obligated to perform the duties enumerated in § 1183(b)(1), (3), (4), (6), and (7). UST Handbook requires the Subchapter V Trustee to perform additional duties. Powers can be expanded by the court with or without removal of the debtor-inpossession; if the DIP is removed, the Subchapter V Trustee would take possession of property of the estate and operate the debtor’s business.

FACILITATION ROLE IS MOST IMPORTANT AND IS UNIQUE Statutory duty to facilitate the development of a consensual plan of reorganization is perhaps the most important role. Facilitation role is unique to Subchapter V; not given to trustees under other chapters of the Bankruptcy Code. Traditionally, trustees tend to be adversarial to the debtor as a result of their duties in protecting the estate and creditors. The Subchapter V Trustee’s role was intentionally designed to be less adversarial; facilitation of a consensual plan requires the Subchapter V Trustee to work with the parties—the creditors and debtor—to agree on a plan. The Subchapter V Trustee acts more like a mediator than an adversary.

ALWAYS DISINTERESTED The Subchapter V Trustee must be disinterested. A “disinterested person” is a person (not necessarily an individual) who is not a creditor, equity security holder, insider, officer, employee or other stakeholder in the debtor, and does not have an interest materially adverse to the estate or any class of creditors or equity security holders. The Subchapter V Trustee must not have any pecuniary interest in the outcome of the case, nor any conflicts of interest that might impair the trustee’s ability to carry out his or her duties. Prior to appointment, the Subchapter V Trustee is required to prepare and submit to the UST a verified statement of disinterestedness. The Subchapter V Trustee begins the appointment as disinterested and is required to notify the UST of any circumstance that develops during the case that impair the trustee’s disinterestedness.

SOMETIMES NEUTRAL A “neutral” is indifferent to the outcome of a dispute, impartial, unbiased. The Subchapter V Trustee is an independent third party who must be fair and impartial to all parties in the case. Subchapter V Trustee is also party in interest in the case, with standing to take positions on myriad issues, such as eligibility for Subchapter V relief, use of cash collateral, payment of prepetition wages, payment of affiliate officer salaries, maintenance of prepetition bank accounts, employment of professionals, exemptions, stay relief, assumption and rejection of leases and contracts, asset sales, plan confirmation, objections to claims, conversion, dismissal, and other contested matters and adversary proceedings. Taking a position on any one of the foregoing issues would not impact the Subchapter V. Trustee’s disinterestedness but would terminate the trustee’s case-inception neutrality.

FACILITATOR IS DE FACTO MEDIATOR OR MEDIATOR-LIKE A facilitator is someone that helps a group of people engage in discussions or work together; one who interacts with parties in negotiations, exchanging information and trying to further the process. The term “facilitator” is often used interchangeably with the term mediator. Bankruptcy courts have also described the Subchapter V Trustee as a de facto mediator or mediator-like. The mediator’s role is to suggest alternatives, analyze issues, question perceptions, conduct private caucuses, stimulate negotiations between opposing sides, and keep order. The Subchapter V Trustee’s role as facilitator is identical.

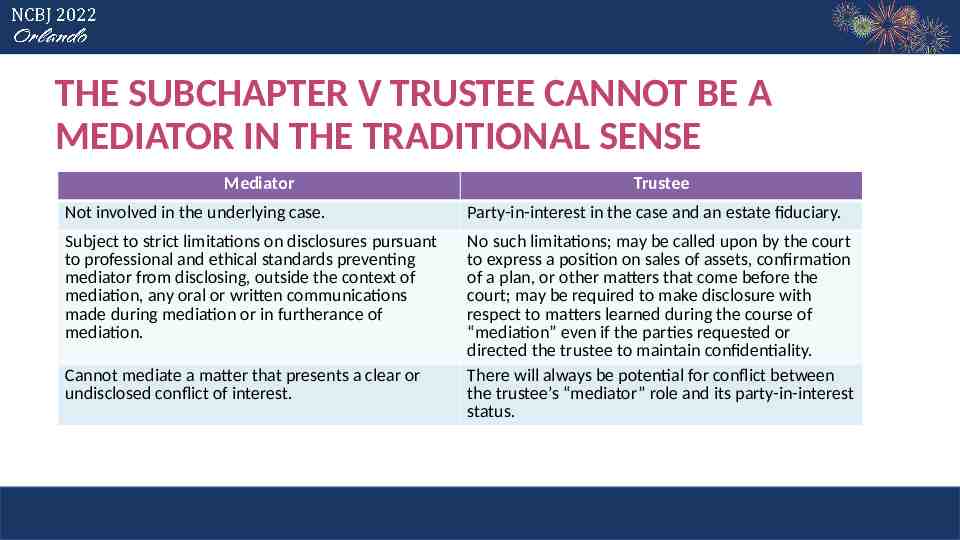

THE SUBCHAPTER V TRUSTEE CANNOT BE A MEDIATOR IN THE TRADITIONAL SENSE Mediator Trustee Not involved in the underlying case. Party-in-interest in the case and an estate fiduciary. Subject to strict limitations on disclosures pursuant to professional and ethical standards preventing mediator from disclosing, outside the context of mediation, any oral or written communications made during mediation or in furtherance of mediation. No such limitations; may be called upon by the court to express a position on sales of assets, confirmation of a plan, or other matters that come before the court; may be required to make disclosure with respect to matters learned during the course of “mediation” even if the parties requested or directed the trustee to maintain confidentiality. There will always be potential for conflict between the trustee’s “mediator” role and its party-in-interest status. Cannot mediate a matter that presents a clear or undisclosed conflict of interest.

ENCOURAGING CANDID COMMUNICATIONS WITH THE TRUSTEE Two concerns expressed by practitioners as to communications with the Subchapter V Trustee: Confidentiality (i.e., protection from disclosure in almost all circumstances), and Admissibility into evidence under Rule 408 of the Federal Rules of Evidence. To remedy the admissibility issue, the parties could agree that all oral and written communications are confidential settlement communications subject to Rule 408 and not discoverable or admissible at trial; this could be memorialized in a written agreement, incorporated into a local rule, or incorporated into the court’s initial Subchapter V procedures order. A real concern regarding confidentiality likely requires a traditional mediator; recognize the limited cases/issues that require a traditional mediator versus the cases/issues that can be addressed efficiently and economically by the Subchapter V Trustee.

MORE WAYS TO UTILIZE SUBCHAPTER V TRUSTEE Communicate shortly after appointment to discuss the case, the players, the goals, the plan, and the potential challenges. Provide copies of historical financials, tax returns, and other financial documents. Provide a draft of the initial two-week cash collateral budget and any subsequent budgets. Provide a draft of the proposed plan, liquidation analysis, and projections. Reach out to request assistance in plan negotiations with creditors, resolution of valuation disputes, and resolution of objections to confirmation. Reach out to request assistance in resolving myriad other contested matters and adversary proceedings. Provide regular, periodic updates, particularly prior to hearings.

SUBCHAPTER V TRUSTEE POLL What are some things debtors or their counsel do that drive you crazy? “Be unresponsive. Our key role is to facilitate a consensual plan, which means that we need to be talking about the issues and how to resolve them. Tough to do when you don’t get return calls or emails.” “Fight with major creditors and then I have to mediate the issue. Hide things from me.” “Treat me as a spy for the Court.” “Push back on my document requests. Don’t take my advice and then later I have to do the “I told you so” dance.”

SUBCHAPTER V TRUSTEE POLL (CONT’D) What kind of business would be most challenging if not impossible to take over as an operating trustee? “Any business that requires the individual to have a license (in particular cash businesses where the principal IS the business – barber, tattoo artist, home improvement).” “Anything requiring particular expertise to operate, like a business in the tech or health industries.” “If the debtor is not willing all business are impossible to run.”

SUBCHAPTER V TRUSTEE POLL (CONT’D) What do all successful debtors have in common? “They face reality.” “Good management and good counsel.” “Preplanning, timely filings, open communications with principle creditor and agreements with creditor on plan treatment.”

SUBCHAPTER V TRUSTEE POLL (CONT’D) What questions do you ask to assess the debtor's ability to perform under the plan? “What changes have been made to the business operations since the Ch 11 was filed? What changes are planned? MORs are the most important documents regarding feasibility.” “How bad the creditors will take it with the proposed distribution and the mood of the creditors.” “How has the pandemic affected the business?”

SUBCHAPTER V TRUSTEE POLL (CONT’D) Other than money, what are some unique motivations you have seen in objecting creditors in your cases? “The largest motivations in most of my subchapter v cases are personal disputes between equity members, between debtors and landlords that have personal relationship.” “Kill the debtor – no cure; in each case the debtor died.” “Family issues - usually involving family partnerships, wherein Debtor a has a partnership interestinvolving inherited property.”

EXTENSION OF TIME JUSTLY ACCOUNTABLE OR NOT – WHAT WORKS? Debtors beware and do not let 90 days pass without filing your plan or obtaining an enlargement (preferably pre-deadline), lest the magical world of Subchapter V shall evaporate before your eyes. Causal links: Yes! Lazy, chronically late, generalized excuses: No!

CONJURING CONFIRMATION ALL CONFIRMABLE PLANS ARE ALIKE, BUT EVERY UNCONFIRMABLE PLAN IS UNCONFIRMABLE IN ITS OWN WAY. The Subchapter V Trustee has an affirmative duty to broker a consensual plan. The Subchapter V Trustee must assess the debtor’s financial health quickly. § 1191(c) sets a heightened feasibility test for nonconsensual plans. Disposable income is all income not reasonably necessary to ensure “the continuation, preservation, or operation of the business of the debtor.” Fixed, floating, actual, projected (abracadabra?) Critical documents include balance sheet, statement of operations (P&L), cash collateral budget and, thereafter, monthly operating reports.

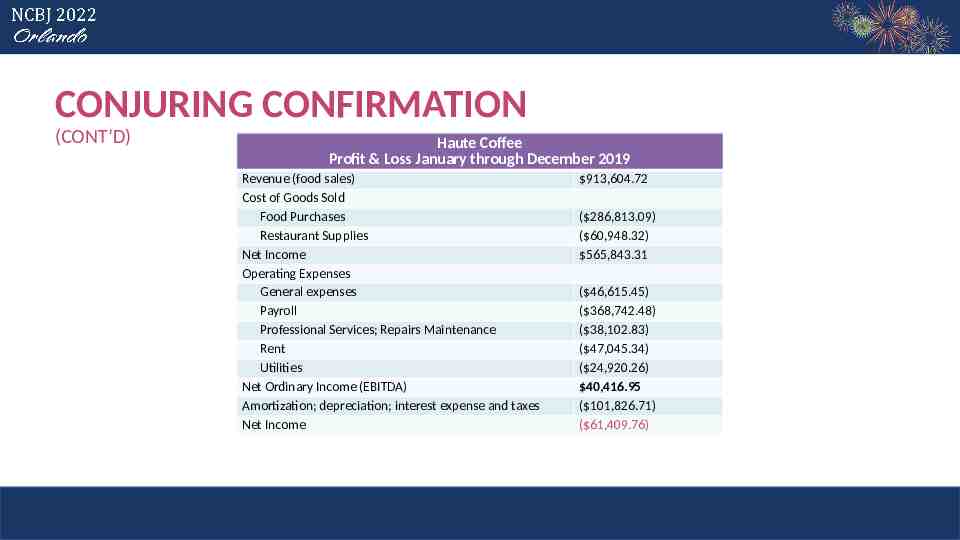

CONJURING CONFIRMATION (CONT’D) Haute Coffee Profit & Loss January through December 2019 Revenue (food sales) Cost of Goods Sold Food Purchases Restaurant Supplies Net Income Operating Expenses General expenses Payroll Professional Services; Repairs Maintenance Rent Utilities Net Ordinary Income (EBITDA) Amortization; depreciation; interest expense and taxes Net Income 913,604.72 ( 286,813.09) ( 60,948.32) 565,843.31 ( 46,615.45) ( 368,742.48) ( 38,102.83) ( 47,045.34) ( 24,920.26) 40,416.95 ( 101,826.71) ( 61,409.76)

CONJURING CONFIRMATION (CONT’D) In re Urgent Care Physicians, Ltd., 2021 WL 6090985 (Bankr. E.D. Wis. Dec. 20, 2021). Court should discount creditor objections under § 1191(c) that challenge the debtor’s business judgment with respect to staffing, investment, etc. Extending the plan term beyond 3 years without a clear equitable basis disproportionality harms small business debtors.

CONJURING CONFIRMATION (CONT’D) BURDENS AND SOURCES OF PROOF Feasibility is debtor’s burden by a preponderance of the evidence. No presumption. The absence of controverting evidence is not sufficient. Lay opinion of owner about projected profits is permitted. Think about how to authenticate contracts, financial statements, and valuations. Creditors can destroy management’s credibility on cross-examination if the projections lack detail, make unfounded assumptions about revenue, and/or fail to address basic spending needs.

REMEDY FOR WHAT AILS YOU What remedies and default provisions should creditors consider bargaining for in exchange for their yes vote? What “appropriate remedies” should they demand in a non-consensual plan?

WHAT DEFAULT PROVISIONS AND REMEDIES SHOULD CREDITORS CONSIDER SEEKING IN EXCHANGE FOR VOTING IN FAVOR OF PLAN CONFIRMATION? In exchange for supporting confirmation of a “consensual plan” under § 1191(a), creditors should negotiate suitable events of default and remedial provisions into the plan. Practicality and creativity are key: Defaults and remedies should fit the creditors’ objectives and the circumstances of each case. Dismissal or conversion to chapter 7 are available remedies for plan defaults -- § 1112(b) applies in Subchapter V cases. Alternatively, if the debtor defaults in performing its plan obligations, remove it as the DIP. o Cause for removal under § 1185(a) includes “failure to perform the obligations of the debtor under a plan confirmed under this subchapter [V].”

WHAT DEFAULT PROVISIONS AND REMEDIES SHOULD CREDITORS CONSIDER SEEKING IN EXCHANGE FOR VOTING IN FAVOR OF PLAN CONFIRMATION? (CONT’D) If the Subchapter V Trustee’s services have ended, consider “reappointing” the trustee to, e.g., operate or wind-down business. o Plan provision that POE does not “vest” in reorganized/post-confirmation debtor. Creditors’ claims are revived (“Phoenix clause”); no amount is discharged. Potential default and remedial provisions in a plan for secured creditors may include: o Streamlined notice and abbreviated cure periods; o “Ex parte” motions for stay relief; o Expedited procedures to terminate, relieve, modify, or annul the automatic stay; o Entry of orders granting relief from the stay without the necessity of an actual hearing; and/or o Waiver of any “stay” periods under Bankruptcy Rule 4001(a)(3), etc.

WHAT DEFAULT PROVISIONS AND REMEDIES SHOULD CREDITORS CONSIDER SEEKING IN EXCHANGE FOR VOTING IN FAVOR OF PLAN CONFIRMATION? (CONT’D) Other default and remedial provisions for secured creditors may include: o Empowerment to exercise its contractual and state law rights and remedies. o Any discharge injunction does not discharge or affect the secured creditor’s liens, rights, and remedies. Potential default and remedial provisions for equipment lessors or landlords may include: o Remedies similar to those for secured creditors, plus – o Immediate access to the leased premises, permit landlord to change locks, and/or direct the debtor to surrender or vacate the leased premises. Potential default and remedial provisions for unsecured creditors may include: o Conversion to chapter 7 for the chapter 7 trustee to liquidate unencumbered assets.

WHAT “APPROPRIATE REMEDIES” SHOULD CREDITORS DEMAND IN A NON-CONSENSUAL, CRAMDOWN PLAN? To confirm a plan over creditors’ objections, § 1191(b) requires that the plan not discriminate unfairly, and be fair and equitable, with respect to each non-accepting, impaired class of claims or interests, and § 1191(c) defines what “fair and equitable” treatment includes, for purposes of “non-consensual” cramdown. With respect to impaired classes of secured claims, “fair and equitable” treatment includes satisfying one of the cramdown alternatives of § 1129(b)(2)(A). o If a class of secured claims is “under-secured,” consider § 1111(b)(2) election to have its claim(s) treated as being “fully secured” for purposes of § 1129(b)(2). o The election may create feasibility problems for the debtor that may give the class greater negotiating leverage.

WHAT “APPROPRIATE REMEDIES” SHOULD CREDITORS DEMAND IN A NON-CONSENSUAL, CRAMDOWN PLAN? (CONT’D) With respect to impaired classes of unsecured claims, “fair and equitable” treatment includes committing the debtor’s “projected disposable income” (or property of equivalent value) for 3 to 5 years to fund distributions. o This may create leverage to obtain more favorable plan treatment and better default remedies.

WHAT “APPROPRIATE REMEDIES” SHOULD CREDITORS DEMAND IN A NON-CONSENSUAL, CRAMDOWN PLAN? (CONT’D) For a non-consensual plan to be “fair and equitable,” § 1191(c)(3)(b) requires that it also must provide “appropriate remedies . . . to protect the holders of claims or interests in the event that the payments are not made.” For secured creditors or lessors, “appropriate remedies” might include: o Abbreviated notice and cure provisions, entry of expedited orders authorizing them to foreclose upon or take possession of their collateral or leased property; and o Plan or confirmation order provisions that the automatic stay and the discharge injunction (whichever is applicable post-confirmation) will not impede their deployment of contractual and state law remedies against their collateral or leased property.

WHAT “APPROPRIATE REMEDIES” SHOULD CREDITORS DEMAND IN A NON-CONSENSUAL, CRAMDOWN PLAN? (CONT’D) For unsecured creditors, “appropriate remedies” might include: o A lien on unencumbered or less-than-fully encumbered property to secure repayment of their claims; o Expedited liquidation of nonexempt assets (in cases of individual debtors); o Empowering a (reappointed) Subchapter V Trustee to dispose of other unencumbered assets; o A truncated process for declaring defaults and allowing the claim collection process to begin; or o Immediate conversion to chapter 7 for the chapter 7 trustee to liquidate unencumbered assets.