Public Finance N6 & N6

86 Slides1.07 MB

Public Finance N6 & N6

N5 Module 1 – Fundamental Principles of Public Finance INTRODUCTION Public Financial Management is concerned with the management of public funds or money. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) GOALS AND OBJECTIVES OF GOVERNMENTS All governments are striving towards the realisation of goals. When setting goals, a governement will consider their ideology and the following: The needs of the community; The functions by which they strive to realise their goals; The nature of public services rendered in order to fulfil their functions; The sources of income from which public services could be financed; and The administration and control of such income. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) LAISSEZ-FAIRE Laissez-faire is French and it means “to allow to do”. In this ideology, the government does not intervene in the private economy/social activities of individual citizens or groups – instead it allows a system of free association with what is today called free market principles. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) GOALS OF THE LAISSEZ-FAIRE SYSTEM Maintenance of law and order (protection services); Enforcement of contracts by law courts (legal protection); Protection of private lives; Protection of private property (legal/social protection); and Defence of national community against any enemy (protection services). www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) SOCIAL WELFARE GOALS An ideology of socialism arose in which governments were asked “to create circumstances within which individuals could develop his/her social welfare and physical being”. This led to socialism which was based on the idea that governments were expected to deliver things such as better working conditions, better pay and more protection. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) SOCIALISM (OR COMMUNISM) “Socialism is accepted as a system of statism with centrally concentrated and comprehensive economic/social/physical control of the activities of the individual to the detriment of individual liberty, where the ownership of all the factors of production are vested in the government, and where production, distribution and trade belong to the community and are administered by the government on behalf of the community. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) THE IDEALOGY OF SOCIALISM Socialism advocates the transformation of private property into public property and income provided from such property to be divided in accordance with individual needs. This amounts to the common ownership of all the means of production. www.futuremanagers.com

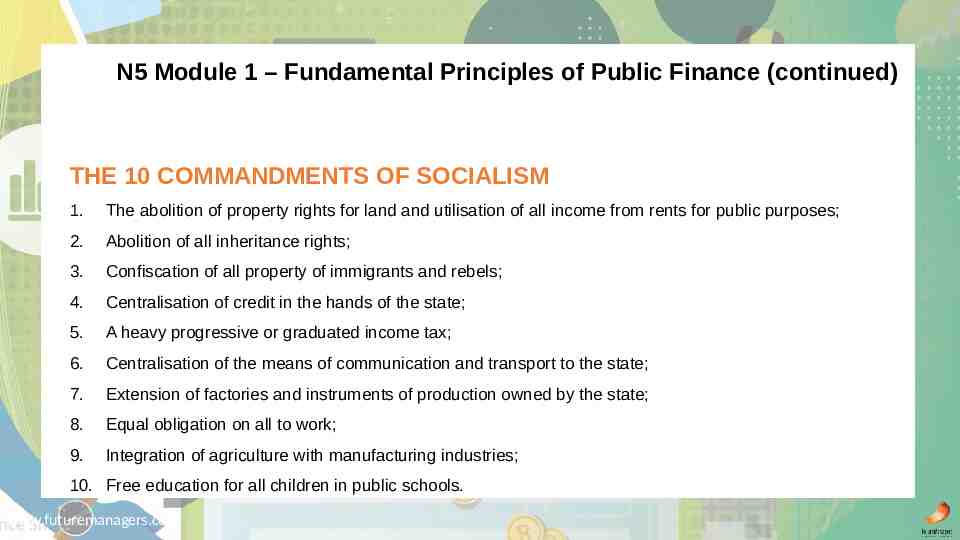

N5 Module 1 – Fundamental Principles of Public Finance (continued) THE 10 COMMANDMENTS OF SOCIALISM 1. The abolition of property rights for land and utilisation of all income from rents for public purposes; 2. Abolition of all inheritance rights; 3. Confiscation of all property of immigrants and rebels; 4. Centralisation of credit in the hands of the state; 5. A heavy progressive or graduated income tax; 6. Centralisation of the means of communication and transport to the state; 7. Extension of factories and instruments of production owned by the state; 8. Equal obligation on all to work; 9. Integration of agriculture with manufacturing industries; 10. Free education for all children in public schools. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) CHARACTERISTICS OF SOCIALISM It does not acknowledge private ownership of production factors; Government decides on how production factors shall be employed; There is a ban on all capitalist or free market systems; Redistribution of income takes place through severe use of taxation; Social security benefits are collectively provided for out of progressive tax sources – to uplift less privileged classes; and Government guarantees a minimum standard of living. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) SOCIAL WELFARE STATE Nations and communities began to seek for some balance between the extremes: the laissez-faire – where the rich got richer and the most entrepreneurial took all, with little or no protection of the less privileged; and socialism – where all remained poor and people had no freedom to decide for themselves. This resulted in the modern social welfare state. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) ECONOMIC WELFARE STATE AS AN IDEOLOGY A modern democracy might lean either towards a laissez-faire or towards a more socialist approach, but in general it attempts to: Recognise the individual as important; Recognise the state as the servant of the individual who needs to be assisted in general and personal self-actualisation; Practise a free-market system with intervention only when necessary; Create a system which protects the rights of all. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) GOVERNMENT FUNCTIONS AND PUBLIC SERVICES In order to realise their goals, governments have to execute a number of functions. Generally these functions are classified as: Line functions – vertical programme subdivisions, and Staff functions – horizontal supporting services. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) LINE FUNCTIONS: VERTICAL Most authorities recognise the following three types of Government Functions: 1. Order and Protection Police and Defence 2. Social or National Welfare Health, education, pensions, etc. 3. Economic Welfare Stimulation of the economy using fiscal (tax) and monetary control (interest rates). www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) STAFF FUNCTIONS OR SERVICES: HORIZONTAL These are supporting functions, contributing to the line functions, in order to realise the goals of the government of the day. Typical services provided by people in various positions in offices throughout the country include: Financial services; Personnel services; Office and secretarial service; and Legal advisory service. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) CLASSIFICATION OF GOVERNMENT SERVICES Generally speaking we look at and classify three different types of services to members of the public: 1. Social/Collective or Public Services; 2. Specific/Particular Services; 3. Quasi-Social or Quasi-Particular Services. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) PRIVATISATION OF GOVERNMENT SERVICES If a government leans more towards a modern, democratic and capitalist society, it will probably seek privatisation of national assets. For example, it might seem logical that many citizens might want to nationalise industries, such as the gold mines. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) REASONS FOR PRIVATISATION The main goal of privatisation is the restructuring and rationalisation of a country’s economy. This could happen for the following reasons: To encourage a policy of private initiative within a market related economy; To reduce excessive government spending; To lower the financial burden of government; and To increase the tax base. www.futuremanagers.com

N5 Module 1 – Fundamental Principles of Public Finance (continued) METHODS OF PRIVATISATION Contracting out – allowing private individuals to supply services; Deregulation – taking away legal/monetary obstacles so that an industry has no protection against competition from others; Depoliticisation – divorcing or separating important services from party politics. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System ORIGIN OF DEMOCRACY Aristotle, a Greek philosopher, came up with the idea of democracy in 384322 BC. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) THE MAGNA CARTA This document depicted the Constitutional relationship between the King, the Common Council and the citizens of England and was signed by King John of England in 1215. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) THE AMERICAN WAR OF INDEPENDENCE The British government expected the people of America to pay them taxes without giving them any representation in the British Parliament. The American colonists were deeply unhappy about this and this led to the American War of Independence. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) THE FRENCH REVOLUTION The French Revolution was the first largescale revolution during which the royal family and the aristocracy of France were executed and a democratically styled government was put in their place. Since then the modern world, and other communities, have sought to fight for a model which closely resembled the one fought for in France. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) 10 DEMOCRATIC PRINCIPLES FOR PUBLIC FINANCIAL MANAGEMENT 1. No tax can be collected from taxpayers without their consent; 2. Utilisation of public financial resources must satisfy the collective needs; 3. Participatory democracy means direct participation by the taxpayers; 4. Public financial decision-making should be; 5. Only elected political representatives has the authority to introduce taxes; 6. Responsibility of the elected political representatives is owed to taxpayers; 7. Political representatives must be sensitive to the needs of the community; 8. The budget programmes should satisfy the needs of the public; 9. Social equity or justice requires integrity; 10. Activities regarding public financial management must take place in public. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) ACCOUNTABILITY Each political representative should give full account of his/her activities. In a democracy officials and representatives are called upon to be accountable for the efficient and effective use of public funds. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) ACCOUNTING Accounting is the mechanism through which representatives can be accountable to the public – at the end of the financial year a report on the financial effects of each department’s activities is compiled. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) FINANCIAL DECISION MAKING IN A PARTICIPATORY DEMOCRACY Most modern governments attempt to implement at least some of the principles of participatory democracy into their ideology; this is done through public meetings, especially on financial matters. www.futuremanagers.com

N5 Module 2 – Guidelines for a Democratic Financial System (continued) REPRESENTATIVES VERSUS VOTERS Representatives are chosen to speak, to make decisions on behalf of their voters – direct participation is difficult and expensive as there are too many voters; the representative therefore participates on behalf of the voter. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions THE LEGISLATURE The legislature is a selected body of people given the power and responsibility to make laws for the nation. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) PARLIAMENT Parliament comprises the elected representatives of the people. The government is accountable to Parliament. In terms of the Constitution, Parliament could pass a vote of no confidence in the cabinet, including the President. Parliament also has to decide how to allocate the taxpayers’ money to provide services for the people. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) CABINET The cabinet consists of the President, as head of the cabinet, the Deputy President and ministers. The President appoints the Deputy President and ministers, from among the members of the National Assembly with no more than two ministers from outside the assembly. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) PARLIAMENT: THE PEOPLE DECIDE A parliamentary democracy means that every citizen of voting age has the opportunity to influence the manner in which the country is governed. This means that, although not every citizen is physically making a decision, the people are electing the candidates that they think will make the best decisions for them. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE POWER AND AUTHORITY RELATIONSHIP Power is the ability of an individual, interest group or the government to exert influence over another. In politics, authority is the power given to representatives and government to act on behalf of their voters. In this way the authority itself is supported by the power given to the government by the voters themselves. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) VOTERS AND THE LEGISLATURE The power which the voter holds is given to a government or representatives in an election during which various parties and individuals present a manifesto to the public. In a democracy the real power is vested in the voter, while the authority over public finance rests with the elected representatives within The Legislature. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) INTEREST GROUPS AND THE LEGISLATURE An interest group is formed when a number of people feel strongly about something and wants to make a change. Voters may combine their strength and put pressure on the government to do something – very often this is called a pressure group. Interest groups are a communication channel or link between individual voters and the government. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE IMPOSITION OF TAX Only The Legislature may impose tax and it also allocates the funds that arise from taxation. The Legislature may delegate taxing authority to: The Legislature at regional level (provincial councils); The Legislature at local government level (town councils). www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE ALLOCATION OF FUNDS The ultimate authority to allocate funds must undoubtedly rest with The Legislature. When funds are allocated, values are taken away from one group and given to another group. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) FUNCTIONS OF THE NATIONAL BUDGET Budgets need to be very carefully planned and presented and the total income the state enjoys should be fairly and carefully distributed. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) REDISTRIBUTION OF WEALTH The aim of the redistribution of wealth is to bridge a gap which might have emerged from an imbalance in wealth of poverty. One way to resolve this is to tax the wealthy and allot monetary value to the poor. This comes with its own set of issues, however and can lead to dissatisfaction. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE AUDITOR GENERAL The Auditor-General is empowered to determine the way in which the executive authority executes the management of public funds. The person who holds this office will audit the financial statements of all Accounting Officers at national, provincial and local levels. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) PUBLIC ACCOUNTS COMMITTEE Once the Auditor-General’s report has been submitted The Legislature needs to interpret its findings and act upon its recommendations. Few members of Parliament have the expertise to do this – instead they refer the report to a standing committee – the Public Accounts Committee. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE PUBLIC PROTECTOR The public protector exists to protect the ordinary citizen. The Public Protector: May summon any person or legal body to give evidence; May enter any premises and demand the handing over of all records and documents for investigation; May initiate an investigation by himself, without a public complaint; Is protected from any insult or slander by any member of the public. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE ROLE OF THE EXECUTIVE AUTHORITY The task of the executive authority is to control and co-ordinate all activities related to state spending. In our country, the executive authority is represented, at central government level by the cabinet and at local government level, by a committee. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) AT PROVINCIAL LEVEL The executive council consists of the Premier as head of the council and no less than five and no more than ten members appointed by the Premier. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) AT LOCAL GOVERNMENTAL LEVEL The finance committee has the same responsibilities and functions on local government level as the cabinet does in the central government. However, the committee may be dismissed by the local legislature and the principle of individual and collective responsibility and accountability applies here as it does at central government level. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) CHAIRMAN OF THE FINANCIAL COMMITTEE The chairperson of the finance committee is called upon to account for the proposals, recommendations and financial activities of the committee. They are expected to adopt and encourage good communication channels between the finance committee itself and all the other committees, and should be in a position to exert influence on the chairperson and to persuade them to adopt the recommendations of the finance committee. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE FUNCTIONS OF THE TREASURY The Treasury has the power to disapprove of any proposed (ex-anti) expenditure by any given department should this not be properly motivated. The Treasury plays a vital role in ensuring that the financial policy is correctly interpreted and effectively and efficiently executed. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) THE ROLE/FUNCTION OF THE ADMINISTRATIVE AUTHORITY When we speak of an administrative body in government we refer to various departments. They are created and run in order to provide the citizens of SA with certain essential and important services, for example: Department of Agriculture, Forestry & Fisheries; Department of Arts & Culture; Department of Basic Education; and the Department of Communications. www.futuremanagers.com

N5 Module 3 – Role of the Central Government in the Financing of Public Institutions (continued) FINANCIAL CONTROL WITHIN THE ADMINISTRATIVE AUTHORITY There are different members of authority who have control or influence on the finances, namely: The Minister; The Auditor-General; The Accounting Officers; and The Departmental Financial Officers. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State ALLOCATION AND EXPENDITURE OF INCOME – INCOME OF CENTRAL GOVERNMENT Every government must have a particular ideology which will determine not only how it will govern its people, but also how it will allocate taxing authority at various levels – those levels being central, provincial and local. The various levels of government should logically supplement each other in a reasonable way – this means that the money they collect through taxes and the services they provide should not overlap. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) ACCOUNTABILITY When a vertical relationship exists and the central government allocates funds to the provincial authority, or when the province allocates funds to a local authority, the body that donates the funds remains accountable to the taxpayers. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) SUFFICIENT REVENUE Each government level should have sufficient revenue to provide the essential services required, and also those services which the voters might have demanded during the general or regional election. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) EQUAL DISTRIBUTION Equal distribution should take place on a vertical level – down from the central government to the regional and local, and also on a horizontal level – between regions or local authorities on the same level. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) ACQUISITION OF INCOME The central government receives its income from the citizens of the country, from trading itself and also from investment. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) TAX Tax can come from: Income tax from taxpayers (personal income tax); Interest on dividends received by investors; Customs and excise duties; Value-added tax (VAT); Tax on foreign shareholders; tax on profits; Fringe benefits tax; Tax on international trade transactions; Ad Valorem; and Airport tax. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) DETERMINATION OF FINANCIAL NEEDS There exist a number of criteria used to determine the financial needs that a community might have: Ideal criterion: the desirable minimum levels of service is determined as well as the cost to supply such a service minimum; Average criterion: according to which the financial need is measured in terms of rendering an average standard of service. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) DETERMINATION OF FINANCIAL CAPACITY Several criteria can determine the financial capacity of a community: Per capita income of a community; The revenue potential of an ideal tax system; Representative revenue system – financial capacity of the government is regarded as the potential revenue which may be collected within a certain demarcated area or region. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) DIVISION OF SOURCES OF INCOME The logical allocation of functions goes hand in hand with the rational or logical allocation of revenue sources. This means that there is an attempt to allow the authority who is most capable of providing services to also be responsible for generating income. www.futuremanagers.com

N5 Module 4 – The Generation of Income and the Expenditure within a State (continued) REVENUE SHARING Revenue sharing means that a specific government body has the authority to tax a community and collect revenue; then to distribute this revenue, according to a formula, amongst various levels of government either horizontally or vertically. www.futuremanagers.com

N6 Module 1 – Government Revenue INTRODUCTION Whatever the government earns, it’s money out of your pocket. However, this does not mean that they derive their income solely from taxation – there are times when grants, donations and loans make up their income needs – in other words they are forced to ask for aid, or to borrow money to balance their budget. www.futuremanagers.com

N6 Module 1 – Government Revenue (continued) SOURCES OF INCOME Taxation is the main source of income for most governments; and there is only one aim in acquiring this source of income: to gather enough funds to pay for services expected by the taxpayers of a country or a region. www.futuremanagers.com

N6 Module 1 – Government Revenue (continued) ECONOMIC REGULATORY FUNCTION A government may use taxation in order to “cool” down the economy; by taking away more from people, citizens have less to spend and this has the effect of regulating the economy, generally by lowering inflation – when spending declines, inflation nearly always drops also. www.futuremanagers.com

N6 Module 1 – Government Revenue (continued) REDISTRIBUTION OF WEALTH Whenever a system of taxation is employed, redistribution of wealth can automatically take place. This means that a low-income earner will enjoy the same protection from the defence force or benefit from medical services, having paid a smaller percentage of his/her income than a wealthier person. www.futuremanagers.com

N6 Module 1 – Government Revenue (continued) GENERAL CHARACTERISTICS OF TAX Taxation is Compulsory; and There is an absence of Quid Pro Quo – a taxpayer cannot expect to receive measurable value for each unit of currency paid over in the form of taxation. www.futuremanagers.com

N6 Module 1 – Government Revenue (continued) TYPES OF TAXATION Taxes may be: Direct such as: Income tax; and Wealth; or Indirect such as: VAT; and Excise duty. www.futuremanagers.com

N6 Module 2 – Characteristics and Functions of the Government Budget TENSIONS Tension exists in the sense that the political aspirations of a group of people might conflict radically with acceptable economic norms. For example, although a minister of finance might want to build seven new dams to supply his voters/citizens with water, economic common sense might dictate that the country can only afford two. www.futuremanagers.com

N6 Module 2 – Characteristics and Functions of the Government Budget (continued) PROTECTION OF CITIZENS The budget is a guideline, and enforceable so it protects the citizen because appointed officials are then expected to act according to the wishes of the legislative authorities. www.futuremanagers.com

N6 Module 2 – Characteristics and Functions of the Government Budget (continued) POLICY DIRECTION The most important characteristics of a budget policy are: It is enforceable; It reflects the political aspirations of the government of the day; It attempts to obey and take sound economic considerations; It attempts to satisfy tensions; It reflects the fiscal policy of the government; and It clearly outline a hierarchy of authority. www.futuremanagers.com

N6 Module 2 – Characteristics and Functions of the Government Budget (continued) FUNCTIONS OF THE ANNUAL BUDGET Reflect policy; Co-ordinate and integrate activities; Be a source of information; Control expenditure; Promote redistribution of wealth; Promote accountability. Regulate the economy; Detail an operating programme; www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget INTRODUCTION A budget can be described as a financial statement which contains the estimates of revenue and expenditure over a certain period of time. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) BUDGET CONCEPTS Revenue: the source of funds; Expenditure: the spending of funds; Capital expenditure: spending on infrastructure or services which last longer than a current year; Operational/current expenditure: the funds needed to run a department; Policy directives: the reflection of the overall policy of the government of the day. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) BUDGET FOR CENTRAL GOVERNMENT – THE ANNUAL BUDGET The budget programme is directed towards satisfying the needs and demands of the public – they might be educational, safety or protection needs. The cycle itself may be divided into the following phases: the preparation phase; approval, execution and control. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) TYPES OF BUDGETS There are two different budgets, namely: The Revenue Budget, showing expected income or revenue; and The Expenditure Budget showing proposals for expenditure by the executive authority. These two budgets are drafted independently. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) THE REVENUE BUDGET The State Revenue Fund is the fund into which all income is paid. There are two receivers of revenue – the Commissioner of Inland Revenue (SARS) and the Commissioner of Customs and Excise. They draft their own separate revenue budgets which are then combined into the Budget of Revenue. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) THE EXPENDITURE BUDGET This forms the main part of the budget which is read and tabled in Parliament every year in March. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) PROVINCIAL GOVERNMENT FINANCE The principles which apply to the central government should apply to the provincial authorities as well. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) PROVINCIAL REVENUE At a provincial level, the following are the main sources of income at present: National Government Grants; Taxation; and Levies and General Activities. www.futuremanagers.com

N6 Module 3 – Compilation of a Government Budget (continued) LOCAL GOVERNMENT FINANCE Compared to the budget at a national level, the following applies for local authorities: Capital budgets and operational budgets are drafted separately; The expenditure and revenue budgets are drafted together; There is only one main budget; A budget vote listing programmes is drawn up for each service; and No distinction between collective, particular and quasi-collective services. www.futuremanagers.com

N6 Module 4 – Capital Budgeting SEPARATE CAPITAL BUDGETS While the capital budget might be drafted separately, the two work hand in hand to provide a financial plan for realising an objective in the provision of public services. Drafting a separate budget might be advantageous for the following reasons: It allows equitable Financing It has a stabilising Effect and; It provides Greater Control. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) THE PROCESS OF CAPITAL BUDGETING Capital Development Programme: A list of essential capital projects for a period of time is drawn up. Certain criteria are used to prioritise projects: High priority for original construction or for essential extensions. Desirable completion. Useful completion. Dispensable completion. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) THE FINANCIAL ANALYSIS When doing a financial analysis is important to consider the following: There should be enough money for extensions; New loans cannot be taken out if the tax base only just covers the repayments for existing loans. The possible growth in the tax base is also taken in account. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) OPERATING BUDGET If a project is financed by using a loan the following three items will have to appear on the operating budget: Loan repayments; Operating costs; and Maintenance. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) IMPACT ON TAX AND USER CHARGES Whether the project is financed from revenue within one year, or whether loans are made over a number of years, taxpayers will be directly affected. Not only will the tax base have to cope with the repayments, but it will also have to provide operating expenses and maintenance. Added to this will be the user charges or tariffs. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) BUDGET ISSUES AND PROBLEMS Issues might arise in the following fields or owing to the following reasons: Political consideration; Purchasing of capital assets; Factors related to community needs, technological changes, cost escalations and other projects; and Volatile domestic economies. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) INTERNAL CAPITAL SOURCES Both capital expenditure and operating expenditure are financed from the State Revenue Fund into which all taxes and other sources of revenue are paid. Finance for capital projects may be financed from external loans or from internal revenue such as taxes. www.futuremanagers.com

N6 Module 4 – Capital Budgeting (continued) FORMAT FOR CAPITAL BUDGETS If a capital budget be drafted separately the following should be included: A budget vote for each service; The details of the costs of the project appears under each sub-vote for each capital project of a budget vote; Financial sources. www.futuremanagers.com