Personal Finance Fundamentals Disclaimer: The views expressed are

32 Slides452.64 KB

Personal Finance Fundamentals Disclaimer: The views expressed are those of the presenters and do not necessarily reflect those of the Federal Reserve Bank of Dallas or the Federal Reserve System.

TEKS (18) Personal financial literacy. The student understands the role of individuals in financial markets. The student is expected to: (E) identify the types of loans available to consumers; (F) explain the responsibilities and obligations of borrowing money; and (G) develop strategies to become a low-risk borrower by improving one's personal credit score. (19) Personal financial literacy. The student applies critical-thinking skills to analyze the costs and benefits of personal financial decisions. The student is expected to: (A) examine ways to avoid and eliminate credit card debt; (B) evaluate the costs and benefits of declaring personal bankruptcy; (20) Personal financial literacy. The student understands how to provide for basic needs while living within a budget. The student is expected to: (A) evaluate the costs and benefits of renting a home; (B) evaluate the costs and benefits of buying a home; and (C) assess the financial aspects of making the transition from renting to home ownership.

3 M’s Moving On and Moving Out – Mindset – Money – Management

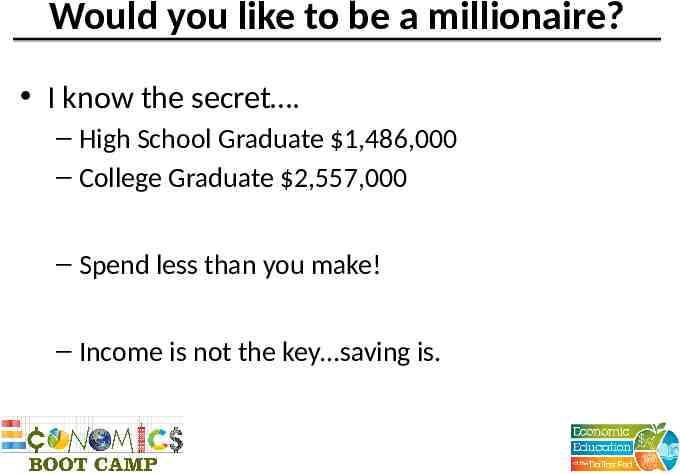

Would you like to be a millionaire? I know the secret . – High School Graduate 1,486,000 – College Graduate 2,557,000 – Spend less than you make! – Income is not the key saving is.

Wealth Most of us define wealth as the dollar value of the assets that we own. To determine our wealth we add up all that we own and subtract all that we owe – that equals our net worth. Simply put: – Own – Owe Wealth

Budgeting Budgeting (controlling your spending) will allow you to increase your wealth. 3 M’s of budgeting

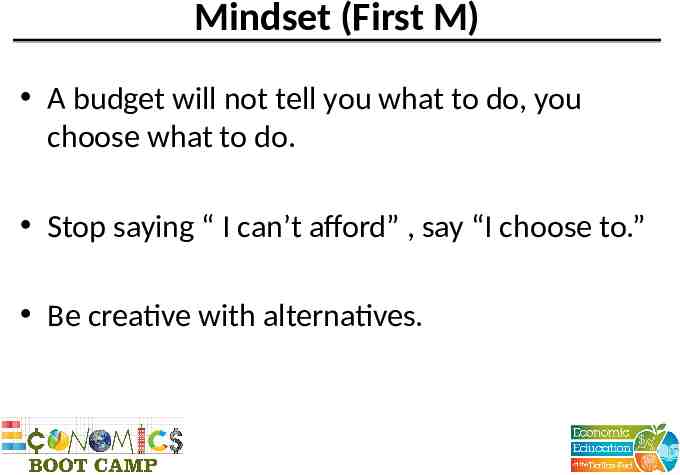

Mindset (First M) A budget will not tell you what to do, you choose what to do. Stop saying “ I can’t afford” , say “I choose to.” Be creative with alternatives.

What type of spender are you ? Everyone stand. Sit down when I call out something you can’t give up: – Candy – Cookie – Soda – Bottled water

Sit down when you can’t give it up Starbucks Going out with your friends once a week Buying lunch vs. bringing lunch Seeing the latest movies Getting your nails done Getting your hair done once a week

Sit down when you can’t give it up. Cable television Latest video games Cell phone

What type of spender are you? A’s - impulsive, leave the cash and debit card at home B’s -you have more discipline but may have to find alternatives for some of the things you like to do C’s – you are probably all ready on your way to good savings habits.

Why is it hard to discipline our spending? Just do it! (Mentality) Advertising Keeping up appearances It isn’t fun!

Money Do the math: How much is coming in and how much is going out. Don’t forget those monthly or annual expenses – holidays, special events, prom. Include money for savings. Remember – Life happens!

Management (2nd M) Set aside time each week to go over your plan. Make adjustments. You won’t be perfect, don’t give up. Find a partner to work with you. Without a plan, you just plan to fail.

Budgeting tips Pay yourself first. Be honest with yourself. Don’t give up. Other people don’t budget and they are fine. Really?

Savings Difficult to do. Allows us to set money aside for emergencies. Allows you to have the freedom to make choices.

Bank accounts Do Your Research Banks accounts are insured for up to 250,000. Bank account features vary from bank to bank.

Types of accounts Checking Savings Money Market CD

Risk & return Generally, the greater the risk the greater the rate of return. What does that mean? – If investors are less certain that they will get their investment back they will ask for a higher interest rate to compensate them for the uncertainty (risk) that they are taking.

Be Comfortable with Your Investments. Each of us has a different risk tolerance All purchases of stocks and bonds carry risk.

TYPES of RISK Risk of Default Risk of capital loss Risk of inflation Risk of liquidity

How much risk can you afford? Financial goals Time horizon Financial risk tolerance

Stocks, bonds, mutual funds Each of these items is a way to invest the money that you have earned. Stocks you become one of the owners of a corporation. You can receive dividends, vote for the board of directors, and sell your stock. Bonds you make a loan to a company or government entity. They agree to pay you back over time at a set rate of interest. Mutual Funds a bundle of these assets used to diversify risk

Money Credit Cards Credit cards represent a loan. The card (or the number) is simply a way to access a line of credit. On the other hand, a debit card is a way to spend checkable deposits, just like a paper check.

Credit Cards Advantages Pre-approved loan Widely accepted Some consumer protection Can establish credit history Disadvantages Requires discipline from borrower Can have high fees and interest Identity theft

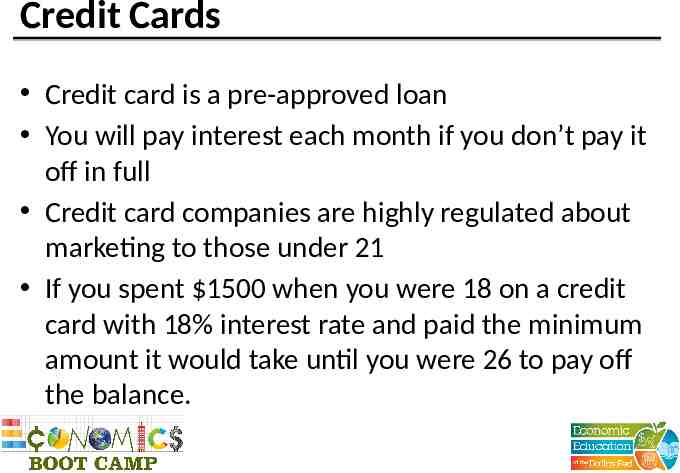

Credit Cards Credit card is a pre-approved loan You will pay interest each month if you don’t pay it off in full Credit card companies are highly regulated about marketing to those under 21 If you spent 1500 when you were 18 on a credit card with 18% interest rate and paid the minimum amount it would take until you were 26 to pay off the balance.

Debit Cards Advantages Widely accepted Some consumer protection Ease of use Disadvantages Requires recordkeeping Can have fees and penalties Identity theft May lead to higher spending

Debit cards A debit card gives you electronic access to your account. If you are overdrawn you will be charged a fee. Consumers who shop with debit cards tend to spend about 30% more than those shopping with cash.

Using credit wisely Credit can allow an individual to have the use of a product or service now rather than waiting for the future. When might this be a good decision? – Education – Housing – Transportation – Necessities

Identity theft Don’t give out information unless you contacted them. Protect your information at school Don’t text your information to others –you don’t know where there phone may be Never carry your social security card Order a credit report each year and check it annualcreditreport.com

Your financial future Think about your goals and dreams Determine wants vs. needs Make a plan Implement your plan Evaluate – weekly, monthly, yearly Make adjustments Stay informed about your options A great financial future awaits you !

Questions ?