National Electricity Regulator Business Plan for 2003/4 Presentation

44 Slides267.50 KB

National Electricity Regulator Business Plan for 2003/4 Presentation to: Parliamentary Portfolio Committee on Minerals and Energy March 2003

Agenda Introduction Background to NER Value added by NER Developments in the electricity industry NER Business Plan and Focus Areas Conclusion

The Supply Chain PRIMARY ENERGY SUPPLY SUPPLY SIDE GENERATION TRANSMISSION & DISTRIBUTION MARKETING, SALES, & CUSTOMER SERVICE DEMAND SIDE COMMERCIAL RESIDENTIAL AGRICULTURAL INDUSTRIAL KEY CUSTOMERS

Role of NER Protect interests of electricity customers Ensure efficient electricity supply industry Ensure lowest cost electricty prices Ensure acceptable quality of service and supply Ensure long term provision and development of electricity services Ensure fair play amongst suppliers – level playing field

How NER fulfills this role Regulates prices of monopoly elements Sets quality of supply and service standards and monitors compliance Mediates and arbitrates within the electricity industry Oversees Integrated Resource Planning Maintains industry information for regulatory purposes and dissemanation Will promote competition in line with government policy

Value Added by NER Supporting government with policy development and drafting of legislation Member of team investigating generation and transmission restructuring to establish competition and a market Member of team investigating the electricity distribution industry restructuring to accelerate rationalisation of distributors Approval of electricity price increases by suppliers (Eskom and municipalities) – Benefit to customers in lower prices Finalisation of electricity pricing policy

Value Added by NER (contd.) Requiring licensees to move towards cost reflective tariffs Setting minimum standards of supply and service – Benefit to customers Dispute resolution (Customers/Suppliers) Data base and information resource Allocation of electrification funds and supporting DME with establishment of INEP Building HR capacity in utility regulation in South Africa – Candidate Regulator’s programme

Developments in the electricity industry Distribution – Establishment (over a transition period) of six regional electricity distributors (REDs) – Merging of Eskom and municipalities – NER responsible for regulation of REDs Generation and Transmisison – Restructuring Eskom into competing generating companies (to establish a competitive generation market) – Privatisation of 30% of generation, and IPPs for new capacity – Creation of a separate transmission company – Setting up of an electricity market to foster competition

Restructuring of ESI and EDI (cont.) Implications for the NER's regulatory responsibilities: – Empowerment of the NER, through appropriate legislation, to manage the needed transition while protecting consumer rights – Accommodation of legitimate interests of (existing and future) private participants – The regulatory and tariff environments are the legislative responsibility of the NER, and it must ensure that appropriate laws and regulations are in place when change takes place

Results of restructuring the ESI Achieves government’s policy goals Competition results in improved efficiency and lower prices than would have been the case Less market power to control prices Significant BEE is achieved Fiscal revenue for debt reduction Considerable inward investment Private sector participation attracts international strategic investors Ease of regulation Benefits to electricity consumers

Business Planning BUSINESS PLAN AND BUDGET Covers the period 1 April 2003 to 31 March 2004 Sets out the priorities for the 2003/04 period Emphasis on undertaking its core regulatory responsibilities effectively and putting in place a regulatory framework for the reformed electrciity indistry STRATEGIC PLAN Covers the period 2003 to 2006 (part of the Business Plan) Provides a medium term planning horison to ensure that its resources are effectively applied to regulate an evolving industry

Business Plan: Focus Areas and Key Activities Support for Government’s ESI restructuring process – High level participation in committees overseeing EDI/ESI restructuring – Participate in EDI/ESI Working Groups through the secondment of professional staff

Business Plan: Focus Areas and Key Activities Generation – Strategy to ensure new generation investment based on the national integrated resource plan (IRP) – Broadening of IPP policy and licensing framework to include renewable IPP’s and demonstration plants – Complete compliance-monitoring framework for generation (including non-grid)

Business Plan: Focus Areas and Key Activities Wholesale Trading and Market Operation – Oversee and ensure the WEPS preparation for implementation – Develop a regulatory framework for transition to wholesale market (including vesting contracts)

Business Plan: Focus Areas and Key Activities Transmission and Systems Operations – Develop and implement the framework for economic regulation of transmission – Develop a compliance-monitoring framework for transmission

Business Plan: Focus Areas and Key Activities Distribution and Retail – Commence with the development of detailed conditions of the REDs licences, consistent with the regulatory framework of REDs as proposed in the Cabinet Blueprint Report – Establish standards and compliance monitoring systems and routines for non-grid operators as well as to develop a compliance-monitoring framework for distribution

Business Plan: Focus Areas and Key Activities Contestable and Special Customers – Develop a licensing framework for contestable customers – Commence with the revision and implementation of the pricing policy for special deal customers consistent with the policy framework for REDs

Business Plan: Focus Areas and Key Activities International, Regional and National Regulatory Issues – Continued support for AFUR activities in line with NEPAD objectives, as well as RERA – Develop a framework for providing regulatory consultancy services on a cost recovery basis

Business Plan: Focus Areas and Key Activities NER Capacity Building – Develop a comprehensive human resource development strategy that will enable the NER to meet its needs in preparation for the developments in the electricity industry

Business Plan: Focus Areas and Key Activities NER Strategic Positioning – Develop criteria to measure its performance so as to meet the expectations of stakeholders – Conduct an intensive positioning exercise in terms of its role and value-addition to its stakeholders – Develop a stakeholder communication and management strategy

Business Plan: Focus Areas and Key Activities Special activity – Commence with the development of a regulatory framework for renewable energy

Business Plan: Process Followed Board provided strategic direction Turned strategic direction into 3-year Strategic Plan Developed 1-year Business Plan based on first year in Strategic Plan Board approved first draft of Strategic and Business Plans Compiled budget Final approval by Board of Strategic and Business Plan with budget

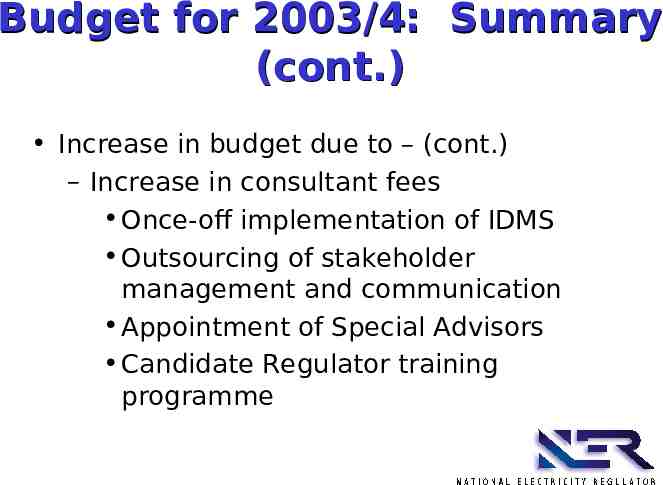

Budget for 2003/4: Summary Budget requested R63,7 million Increase of 24,7% Mainly due to: – New staff appointments (13) – Capital payment of new building – Increased involvement in regional and continental regulatory initiatives – Funding litigation of current court cases – CAPEX requirements Computers and furniture – Travel costs

Budget for 2003/4: Summary (cont.) Increase in budget due to – (cont.) – Increase in consultant fees Once-off implementation of IDMS Outsourcing of stakeholder management and communication Appointment of Special Advisors Candidate Regulator training programme

Levy: Summary Payable by customers – Via generators 0.03320 c/kWh Cost to average domestic households 16c/month May change subject to budget approval

Conclusion NER focusing on priorities for a changing ESI as determined by Government Lot of work done in finalising ‘relevant’ Business Plan NER will focus its efforts on government’s priorities for the sector Insufficient budget to ‘skill up’ totally, but we have nearly achieved our target for a competent regulator NER committed to serve ESI and its stakeholders, especially customers

ADDITIONAL SLIDES

Generation Transmission Distrib Customer Monopoly Model

IPP IPP G&T Distrib Customer Single-Buyer Model

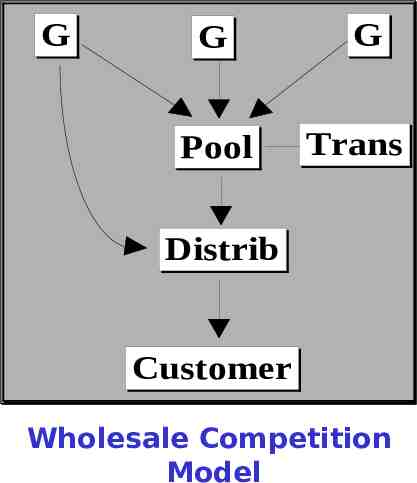

G G Pool G Trans Distrib Customer Wholesale Competition Model

G G Pool S S G T&D S Customers Retail Competition Model

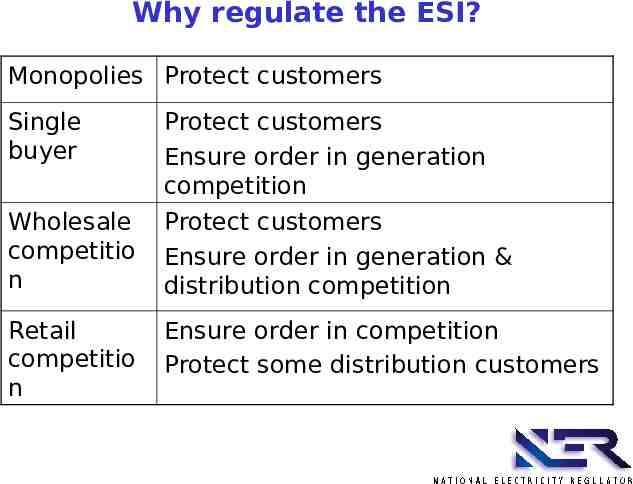

Why regulate the ESI? Monopolies Protect customers Single buyer Protect customers Ensure order in generation competition Wholesale competitio n Protect customers Ensure order in generation & distribution competition Retail competitio n Ensure order in competition Protect some distribution customers

ESI market reform: International Experience Monopolies Single Buyer? Wholesale Competition Retail Competition A transition process from single buyer to wholesale competition, to retail competition, monitored by a regulator

Drivers for change Maximise financial and economic returns to the state – Fiscal revenue, debt reduction The need to demonstrate economic efficiency – Allocative efficiency, next investment in generation capacity – Driving operational costs down Widened resource availability and technological change – Competitive imports from SAPP – Natural gas from Namibia and Mozambique and CCGTs – Information and computer technologies Opportunity for BEE International environmental concerns Need for improved customer service and choice

But protect Electrification programme Cross-subsidies for poor (but more transparent) Internationally competitive electricity prices Management, technical and R&D competencies in electrcuiity industry Security of supply Potential for demand-side management and energy efficiency investments National regulatory oversight and control Globally competitive business for the African Renaissance

1998 White Paper on Energy Policy Introduce competition to the industry, especially the generation sector Give customers the right to choose their electricity supplier Permit open, non-discriminatory access to the transmission system Encourage private sector participation in the industry Eskom will have to be restructured into separate generation and transmission companies Government intends to separate power stations into a number of companies

RED RED 66 Customers Customers (000’s)1008 (000’s)1008 Load Load (TWh)28 (TWh)28 Electrified Electrified (%)60 (%)60 RED RED 44 Customers Customers (000’s)720 (000’s)720 Load Load (TWh)31 (TWh)31 Electrified Electrified (%)70 (%)70 Pretori a Pietersbu rg East Rand Pretori a Rustenburg Vryburg Nelspr uit East Rand Witbank Lichtenberg Kroonstad Johannes burg Lydenburg Johannes burg Newcastl e Ulundi Harrismith Kimberley Upington RED RED 22 Customers Customers (000’s)1006 (000’s)1006 Load Load (TWh)29 (TWh)29 Prieska Electrified Electrified (%)73 (%)73 Calvinia Bergville Bloemfontein Pietermaritzburg Customers Customers (000’s)857 (000’s)857 Load Load (TWh)14 (TWh)14 Electrified Electrified (%)81 (%)81 De Aar Umtata Graaf Reinet RED RED 33 Customers Customers (000’s)1400 (000’s)1400 Load Load (TWh)29 (TWh)29 Electrified Electrified (%)56 (%)56 East London Cape Town Richards Bay Durban Victoria West RED RED 11 RED RED 55 Customers Customers (000’s)683 (000’s)683 Load Load (TWh)37 (TWh)37 Electrified Electrified (%)60 (%)60 Port Elizabeth

Phase I: Eskom Corporatisation Immediate - 2003 – Formation of Eskom Holdings Limited with subsidiaries Generation, Transmission, Distribution and Enterprises – Ringfence clusters of generators into divisions of generation for internal competition – Transmission ringfences operations into wires and system operations – Transform EPP into SAPEX to allow progress to power exchange – All sales through SAPEX (mandatory) but CFD in place between Generation and Distribution to guarantee minimum revenue – Ringfencing of Eskom Distribution into proposed REDs continues, and municipalities continue to ringfence their electricity businesses away from other municipal activities

Eskom Holdings Eskom Generation Clusters Eskom Enterprises Eskom Transmission SAPEX Wires SO Trader Eskom Distribution Municipal Distributors Customers

Phase II: Corporatisation of generation and independent power exchange 2002/3 – Eskom Generation creates separate generation companies (GenCos) following portfolios – Separate Independent Power Exchange established Under State ownership Mandatory competitive pool – All sales through IPE but CFDs in place between Gencos and REDs/contestable customers, with progressively reducing minimum revenue guarantees – REDs established at distribution level

Eskom Holdings GenCo1 GenCo2 GenCon Eskom Enterprises Independent Power Exchange State Transmission Co Trader Wires SO RED1 RED2 Customers RED6 Contestable Customers

Phase III: Private sector and competition 2003/4 – Transmission company separated from Eskom Holdings and put into state-owned company – IPE continues, but now operated as MMM and minimum revenue guarantees phased out – Opportunities for BEE to buy mothballed power stations (about 10% of Eskom’s capacity) – Additional sale of one or more generation clusters (portfolios) of up to 20% of Eskom’s capacity – Private sector encouraged to invest in new capacity – Eskom to be left in the end with a 70% share of the market

Eskom Holdings Genco A EskomG enCo Trader Eskom GenCo Eskom Enterprises Power Exchange State Transmission Co Wires SO RED1 RED2 Customers RED6 Special Customers

Regional Regulatory Issues All SADC countries see benefit from establishment of regional regulatory association (RERA) Not constrained by the different stages of regulatory development at national level Only deal with regional issues – Will not interfere with national mandates Designed to fill existing regulatory gaps Learn from other SADC initiatives – TRASA