It comes down to this… The success you have enjoyed has created

17 Slides837.00 KB

It comes down to this The success you have enjoyed has created a problem that will someday become very real for those you care about.

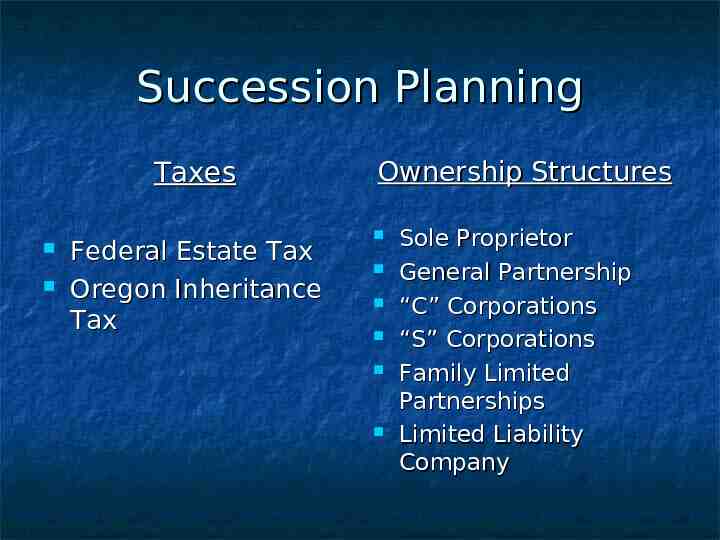

Succession Planning Taxes Federal Estate Tax Oregon Inheritance Tax Ownership Structures Sole Proprietor General Partnership “C” Corporations “S” Corporations Family Limited Partnerships Limited Liability Company

FEDERAL ESTATE TAX This is a tax in flux – it will almost certainly remain, but not in it’s current form.

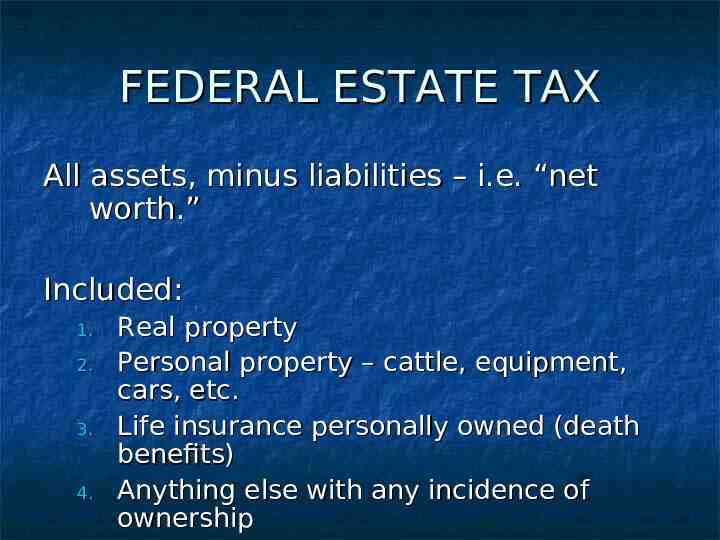

FEDERAL ESTATE TAX All assets, minus liabilities – i.e. “net worth.” Included: 1. 2. 3. 4. Real property Personal property – cattle, equipment, cars, etc. Life insurance personally owned (death benefits) Anything else with any incidence of ownership

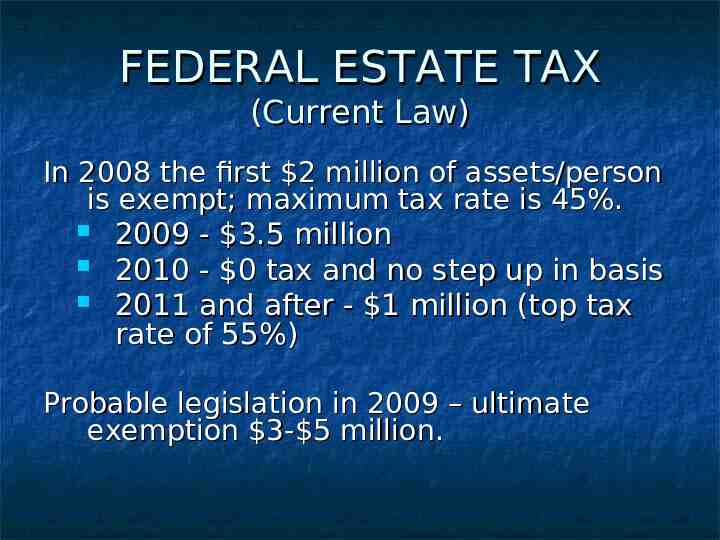

FEDERAL ESTATE TAX (Current Law) In 2008 the first 2 million of assets/person is exempt; maximum tax rate is 45%. 2009 - 3.5 million 2010 - 0 tax and no step up in basis 2011 and after - 1 million (top tax rate of 55%) Probable legislation in 2009 – ultimate exemption 3- 5 million.

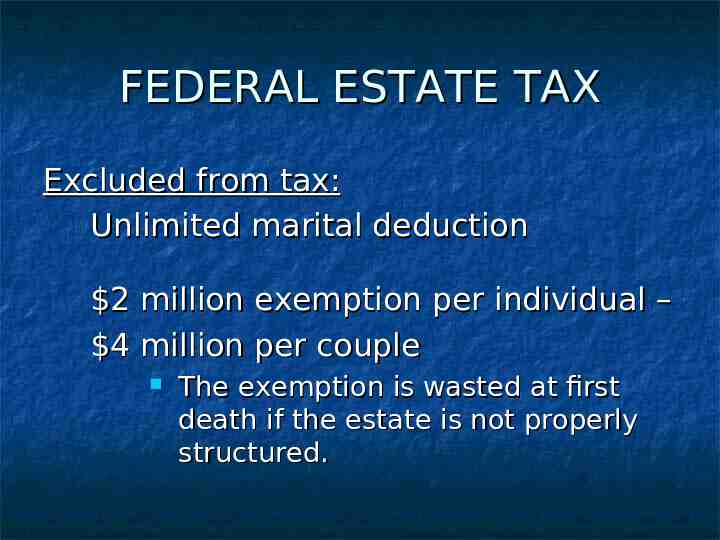

FEDERAL ESTATE TAX Excluded from tax: Unlimited marital deduction 2 million exemption per individual – 4 million per couple The exemption is wasted at first death if the estate is not properly structured.

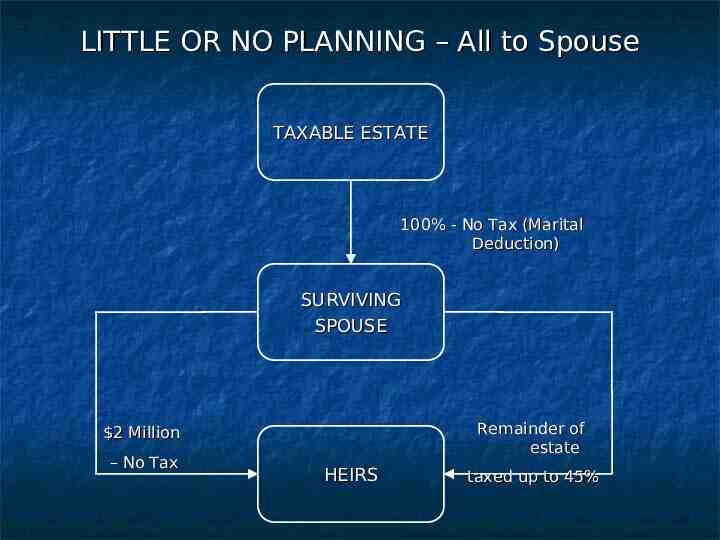

LITTLE OR NO PLANNING – All to Spouse TAXABLE ESTATE 100% - No Tax (Marital Deduction) SURVIVING SPOUSE Remainder of estate 2 Million – No Tax HEIRS taxed up to 45%

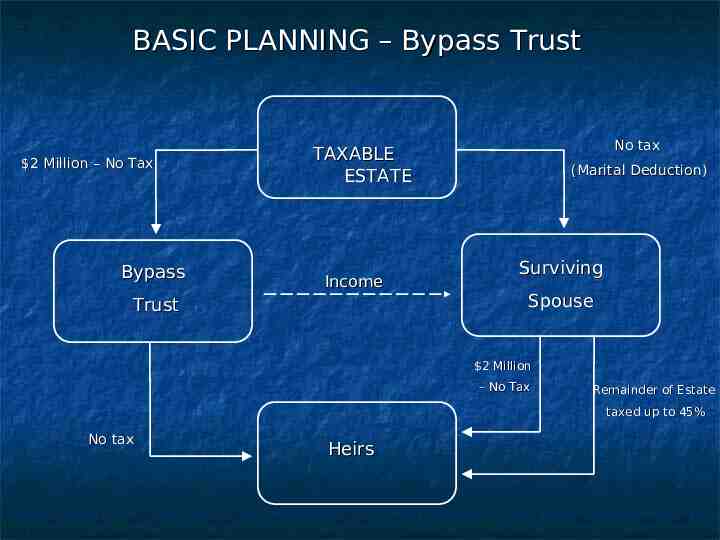

BASIC PLANNING – Bypass Trust 2 Million – No Tax Bypass No tax TAXABLE ESTATE Income Trust (Marital Deduction) Surviving Spouse 2 Million – No Tax Remainder of Estate taxed up to 45% No tax Heirs

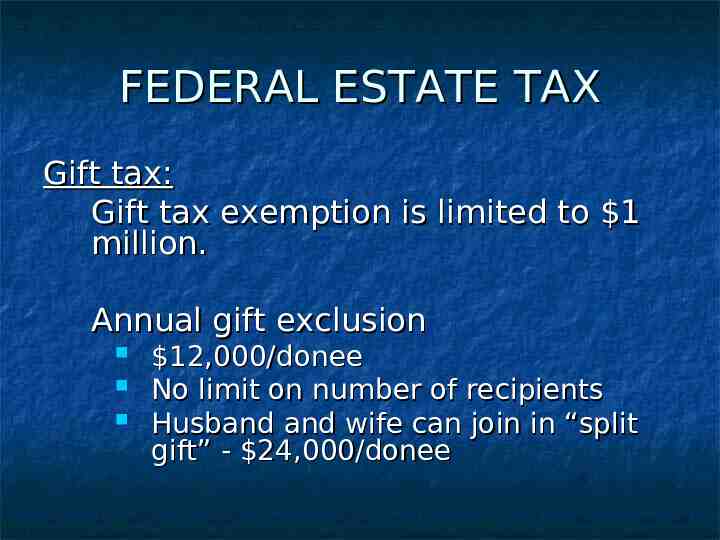

FEDERAL ESTATE TAX Gift tax: Gift tax exemption is limited to 1 million. Annual gift exclusion 12,000/donee No limit on number of recipients Husband and wife can join in “split gift” - 24,000/donee

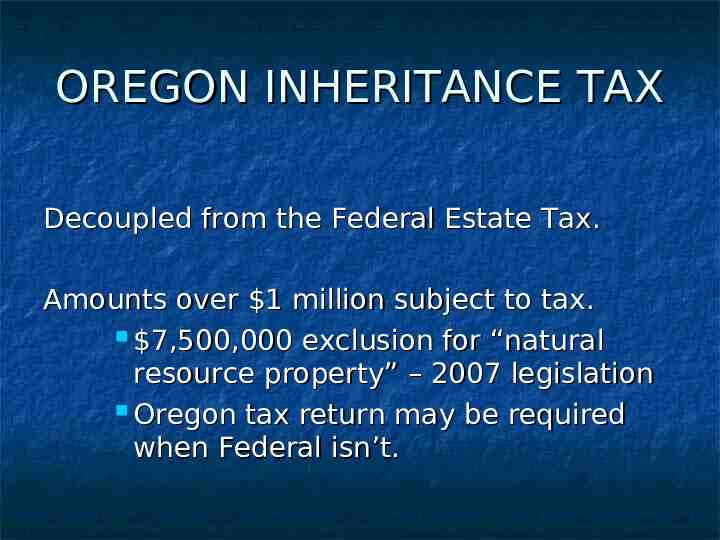

OREGON INHERITANCE TAX Decoupled from the Federal Estate Tax. Amounts over 1 million subject to tax. 7,500,000 exclusion for “natural resource property” – 2007 legislation Oregon tax return may be required when Federal isn’t.

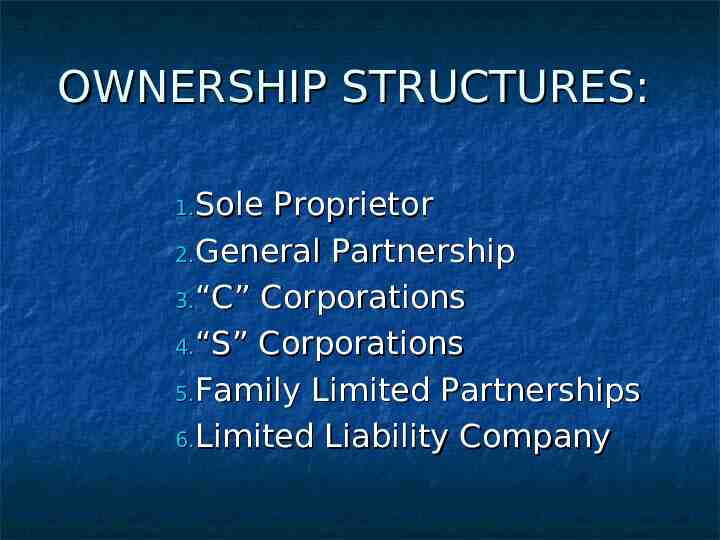

OWNERSHIP STRUCTURES: 1.Sole Proprietor 2.General Partnership 3.“C” Corporations 4.“S” Corporations 5.Family Limited Partnerships 6.Limited Liability Company

SOLE PROPRIETOR Single owner in a business venture. Advantages: 1. 2. Owner has complete control. Simple to establish and operate. Disadvantages: 1. 2. 3. Unlimited personal liability. No continuity. Not easily transferable.

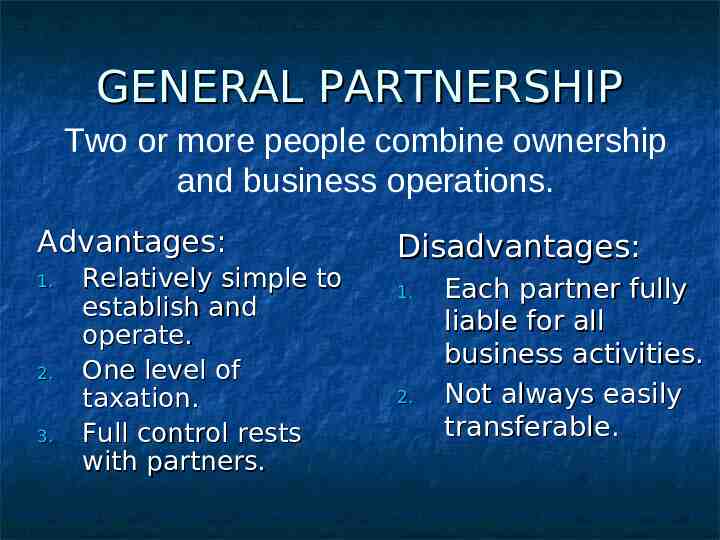

GENERAL PARTNERSHIP Two or more people combine ownership and business operations. Advantages: 1. 2. 3. Relatively simple to establish and operate. One level of taxation. Full control rests with partners. Disadvantages: 1. 2. Each partner fully liable for all business activities. Not always easily transferable.

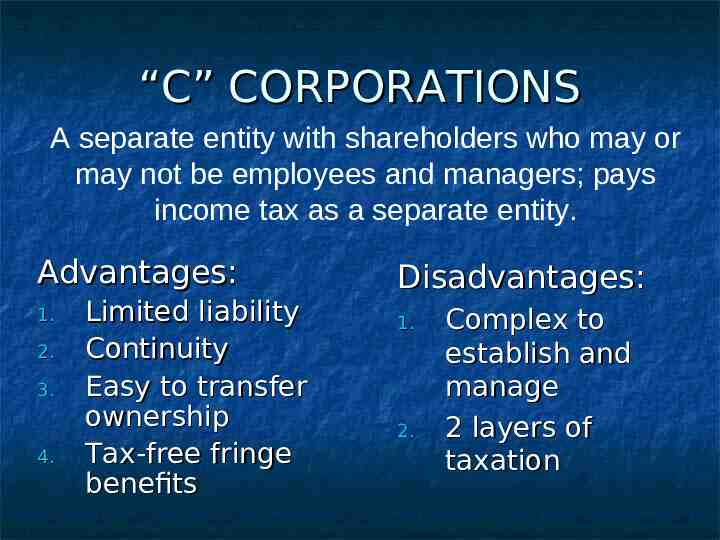

“C” CORPORATIONS A separate entity with shareholders who may or may not be employees and managers; pays income tax as a separate entity. Advantages: 1. 2. 3. 4. Limited liability Continuity Easy to transfer ownership Tax-free fringe benefits Disadvantages: 1. 2. Complex to establish and manage 2 layers of taxation

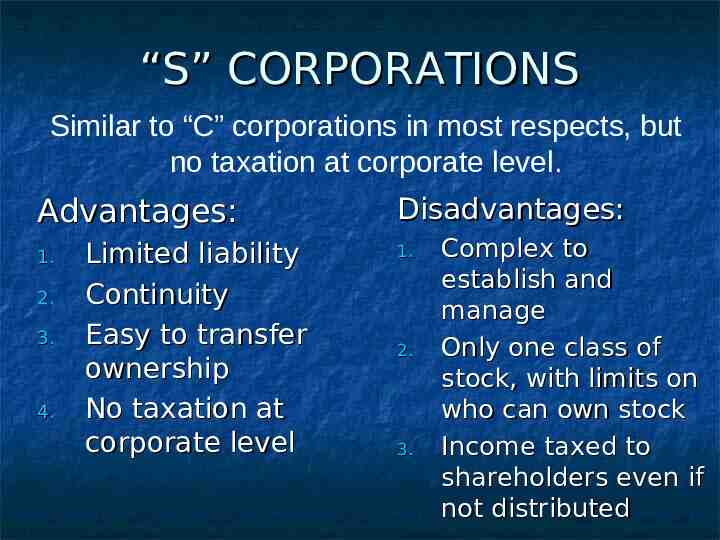

“S” CORPORATIONS Similar to “C” corporations in most respects, but no taxation at corporate level. Advantages: 1. 2. 3. 4. Limited liability Continuity Easy to transfer ownership No taxation at corporate level Disadvantages: 1. 2. 3. Complex to establish and manage Only one class of stock, with limits on who can own stock Income taxed to shareholders even if not distributed

FAMILY LIMITED PARTNERSHIP A form of partnership with a General Partner and one or more Limited Partners. Advantages: 1. 2. 3. Limited liability for limited partners Can transfer ownership without transferring control Significant valuation discounts Disadvantages: 1. Relatively complex to set up and manage

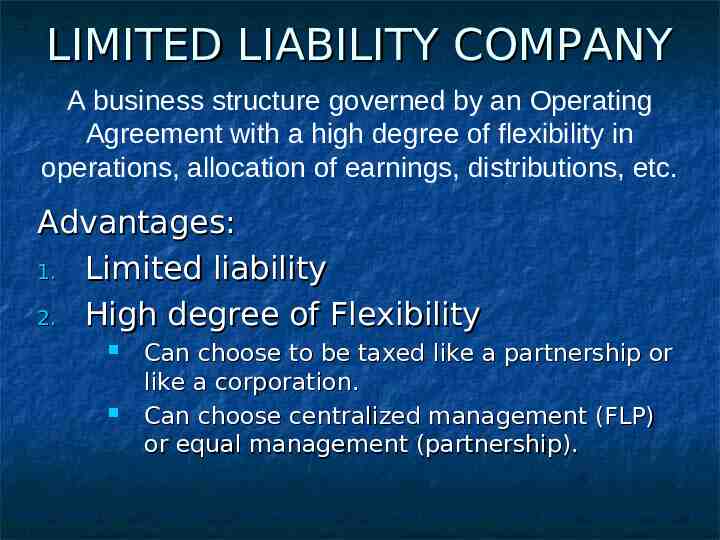

LIMITED LIABILITY COMPANY A business structure governed by an Operating Agreement with a high degree of flexibility in operations, allocation of earnings, distributions, etc. Advantages: 1. Limited liability 2. High degree of Flexibility Can choose to be taxed like a partnership or like a corporation. Can choose centralized management (FLP) or equal management (partnership).