International Capital Taxation Rachel Griffith James Hines Peter

26 Slides270.50 KB

International Capital Taxation Rachel Griffith James Hines Peter Birch Sorensen Comments Julian Alworth 1

Overview 1. 2. 3. 4. Importance of international considerations in tax design The UK Tax system International Tax competition Options for capital income tax reform 2

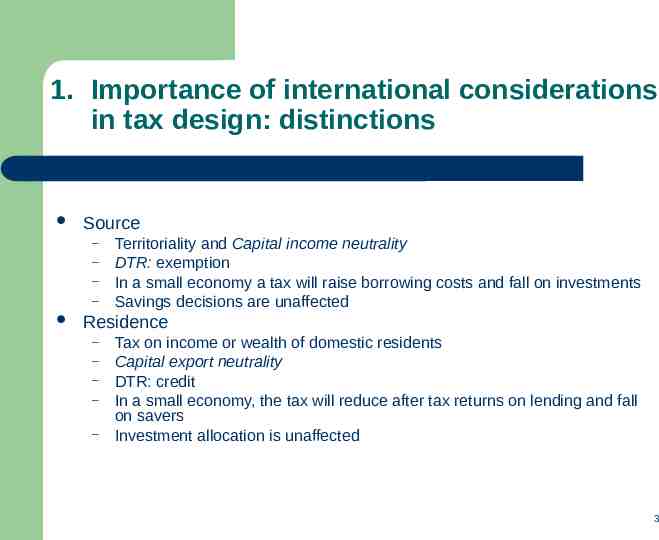

1. Importance of international considerations in tax design: distinctions Source – – – – Territoriality and Capital income neutrality DTR: exemption In a small economy a tax will raise borrowing costs and fall on investments Savings decisions are unaffected Residence – – – – – Tax on income or wealth of domestic residents Capital export neutrality DTR: credit In a small economy, the tax will reduce after tax returns on lending and fall on savers Investment allocation is unaffected 3

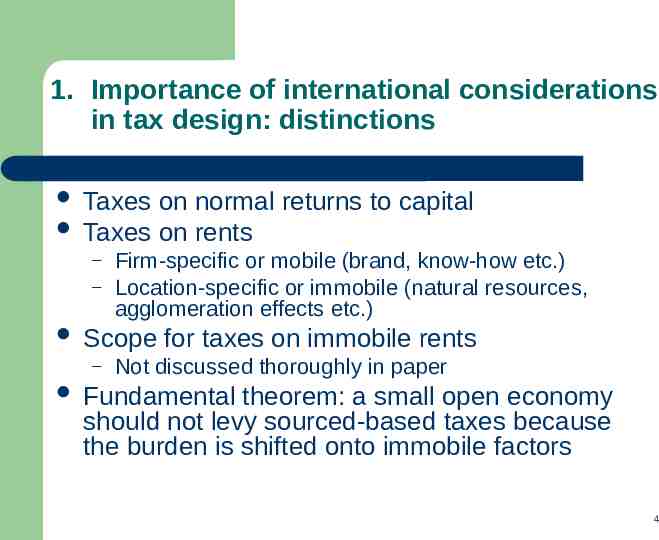

1. Importance of international considerations in tax design: distinctions Taxes on normal returns to capital Taxes on rents – – Scope for taxes on immobile rents – Firm-specific or mobile (brand, know-how etc.) Location-specific or immobile (natural resources, agglomeration effects etc.) Not discussed thoroughly in paper Fundamental theorem: a small open economy should not levy sourced-based taxes because the burden is shifted onto immobile factors 4

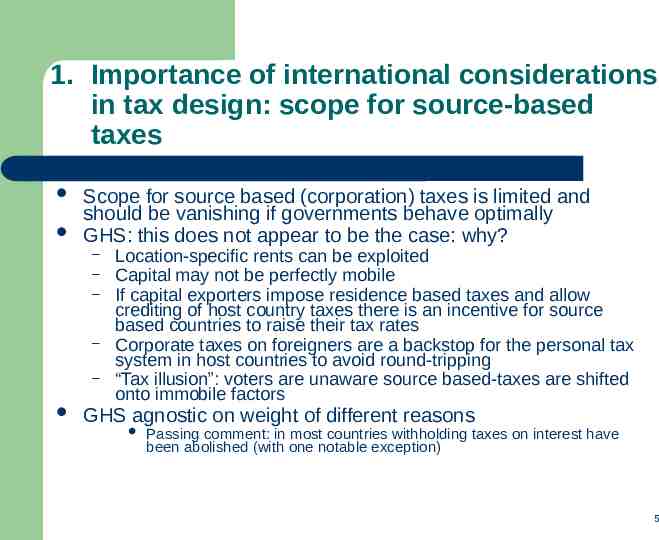

1. Importance of international considerations in tax design: scope for source-based taxes Scope for source based (corporation) taxes is limited and should be vanishing if governments behave optimally GHS: this does not appear to be the case: why? – – – – – Location-specific rents can be exploited Capital may not be perfectly mobile If capital exporters impose residence based taxes and allow crediting of host country taxes there is an incentive for source based countries to raise their tax rates Corporate taxes on foreigners are a backstop for the personal tax system in host countries to avoid round-tripping “Tax illusion”: voters are unaware source based-taxes are shifted onto immobile factors GHS agnostic on weight of different reasons Passing comment: in most countries withholding taxes on interest have been abolished (with one notable exception) 5

1. Importance of international considerations in tax design: empirical evidence Considerable volume of solid empirical evidence that the allocation of investments is highly tax sensitive (though the size of the effects is not measured precisely) Much evidence of tax-avoiding profit shifting Global responsiveness to changes in tax rates of other jurisdictions Tax rates (nominal and effective) have declined in the past 30 years but corporate tax revenues have remained stable or actually increased 6

3. International Tax competition: case against A jurisdiction that unilaterally lowers taxes will attract mobile factors of production thereby reducing national income and tax revenues in other jurisdictions. Spill-over effect (fiscal externality) In a non-cooperative game framework with many jurisdictions this will result in a “race to the bottom” Under-provision of public goods Strong case for tax co-ordination Note: this analysis applies to all taxes on mobile factors of production (little difference between labour and capital mobility) 7

3. International Tax competition: case for competition Gains from tax coordination presume a benevolent government acting in the best interests of citizens “Starving the beast” through tax competition is a way to reduce inefficiencies in government – – – Rent seeking behaviour of bureaucrats and politicians Inefficiencies from redistributive policies Inability to pre-commit to an efficient intertemporal path of taxation Other argument against coordination: common tax policy is not responsive to requirements of individual jurisdictions (national autonomy) 8

3. International Tax competition GHS seem to suggest that tax competition/ coordination is an empirical matter Results are reported of a GE model for OECD countries – Cost of capital differs across countries, leading to wedges in marginal productivities – Coordination leads to a more efficient allocation of capital (raising total income by 0.4%) – However, welfare rises in aggregate by only 0.1% because of induced increase in factor supplies but – There are significant differences in distributional impact amng various countries – Other distortions persist limiting scope of benefits from harmonisation (second-best argument) On balanced GHS are non-committal regarding the benefits from tax harmonisation in the absence of compensation mechanisms 9

3. International Tax competition: Policy Response OECD: Harmful Tax Practices EU Code of Conduct on Preferential Tax Regime EU Savings Directive Authors view: these measures have not necessarily had the intended consequences – – – Tax havens may be beneficial The reduction of preferential tax regimes may lead to more explicit tax rate competition Savings directive leaves large loopholes Common Consolidated Tax Base Role of European Court of Justice 10

3. International Tax competition: Common consolidated tax base Objective: multinational companies could opt to have their business income taxed under a common set of rules valid for all EU countries, base would be apportioned according to formula, each country would apply own tax rate No need to discuss with various tax authorities and sharp reduction in transfer pricing Problems: – – Relation with non EU (formula apportionment with separate accounting) Intangibles in formula (valuation) 11

3. International Tax competition: ECJ Internal Market (1992): “freedom of movement of goods services capital and persons” ECJ is striking down rules that appear to disciminate on grounds of nationality or limit four freedoms Authors: describe the various areas affected but no judgement 12

4. Options for capital income tax reform Alternative concepts of tax neutrality (can we think of territoriality and residence in other terms) – – GHS recognize a trend towards exemption Justification Most international investments occur through acquisition If all companies are to be treated on a par in a bidding the valuation of assets should be unaffected by tax (ownership neutrality) Holding company regimes (participation exemption) Spanish shopping spree Countries are trying to place their multinationals at a competitive advantage in a bidding environment 13

4. Options for capital income tax reform Should UK move to territoriality? – – – – What do we think of the current system? If one believes that deferral entails that the current credit system operates like an exemption system then the behavioural response to moving towards an exemption system should be small GHS argue that such a move would probably result in a small net loss of revenue GHS however suggest design of new system would be critical (without going into details) The UK does not have an active/passive distinction UK does not have complex interest and expense allocation rules 14

4. Options for capital income tax reform Common Consolidated Tax Base (CCCTB) vs. Home state taxation (HST) – – CCCTB – EU: 27 national corporate tax regimes High compliance and costs for multinationals and significant costs of administration Option would be to define a common base Home state taxation (Gammie & Lodin) – – – – – MNCs calculate EU wide tax on a consolidated basis according to the rules of the country of residence of parent company Tax base would be allocated according to formula apportionment and revenues would be allocated on the basis of tax rates in individual countries Pros: flexibility no need for a common base and optional for companies Cons: competition for headquarters may narrow tax base (though mutual recognition of tax bases would limit problem) and potentially lower revenues if companies opt for system with lower revenues. GHS do not appear to favour HST 15

4. Options for capital income tax reform ACE CBIT Dual Income Tax 16

Conclusions Source based taxation is under pressure but there is continued for taxation in foreseeable future The benefits for tax co-ordination are small Current reform proposals appear to solve certain issues but have some flaws 17

Comments General Aspects Specific theoretical and policy questions 18

General Aspects Insufficient description of UK tax system and comparison with US, Canada and main EU countries – – – – How much revenue does the UK raise from foreign source income? CFC regime, working of DTR in UK versus other countries, active/passive income, transfer pricing What are perceived to be the main areas needing adjustment? Major changes in recent years 19

Elements not considered in this version Editorial: International aspects of the taxation of labour, wealth and consumption (including transaction taxes) Several current issues treated only in a cursory fashion (example: active/passive distinction, corporate personal tax integration in an open economy, transfer pricing) Prime focus on certain aspects of corporate tax (individual income tax discussed only in passing) 20

General Aspects Macro-background – – Political framework – – – Trends in the economy (de-materialisation, services, finance etc. Do these trends pose permanent or passing issues for tax policy? Internal market Constraints on sovereignty Which audience for the policy recommendations ? Domestic or European? Evaluation – Will the EU go ahead? What solution is desirable at the EU level? If coordinated solutions are not found what is a reasonable standalone policy? 21

Specific issues The attractions and limits of exemption Rents and source based taxes Financing complications Collective investment vehicles 22

Attractions and limits of exemption Attractions: Simplicity and EU compatibility as applied on the continent – – Participation exemption (parent-subsidiary directive – non black-listed countries) Black listed countries (CFC) Back-stop – provisions Active-passive Losses, triangulations 23

Rents and sourced based taxes Do rents represent a solid basis for believing in a source based tax system? Are foreigners being truly taxed? Who incorporates agglomeration and other location specific rents? Timing issues are important If assets tradeable, capitalisation effects are important and rents are taxed upfront Capital gains tax crucial 24

Financing complications Debt-equity distinction is a major issue at the international level Financing arrangements are important in the way exemption and residence operate Example: authors suggest that exemption is equivalent to ownership neutrality Yes only if financing is loaded unto acquired company 25

Collective investment vehicles Collective investment vehicles have proliferated in recent year – – Corporate form desirable but not corporate tax – – create greater liquidity from previously untradeable assets Diversification Pass-through treatment desirable for investors: If you previously owned a building directly you still wish to be taxed in the same fashion Limited liability and transferability Reliance on Residence of final investors Source-based taxes have not worked 26