Instructors: Please do not post raw PowerPoint files on public

28 Slides277.74 KB

Instructors: Please do not post raw PowerPoint files on public Chapter 12 website. Thank you! From Enterprise Value to Equity Value 1

Session Overview When you have completed the valuation of core operations, you are ready to estimate three values: enterprise value, equity value, and value per share. 1. To determine enterprise value, add to the value of core operations the value of nonoperating assets, such as excess cash and nonconsolidated subsidiaries. 2. To convert enterprise value to equity value, subtract short-term and long-term debt, debt equivalents (such as unfunded pension liabilities), and hybrid securities (such as employee stock options). 3. To estimate value per share, divide the resulting equity value by the most recent number of undiluted shares outstanding. Estimating the value per share completes the technical aspect of the valuation, yet the entire job is not complete. It is time to revisit the valuation with a comprehensive look at its implications. We examine this process in the next session. 2

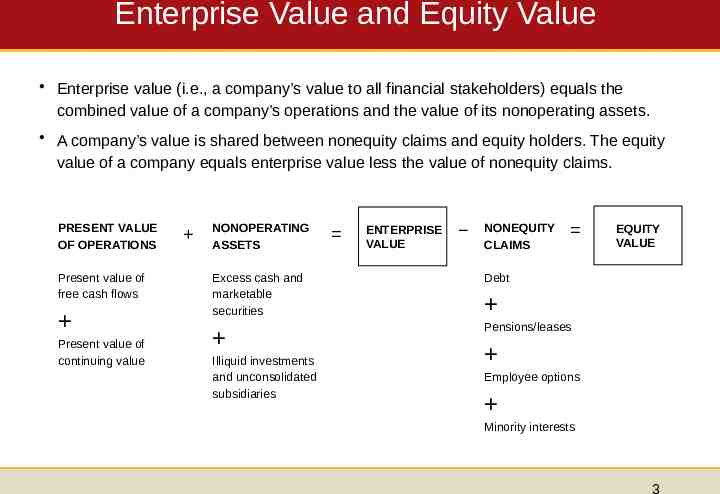

Enterprise Value and Equity Value Enterprise value (i.e., a company’s value to all financial stakeholders) equals the combined value of a company’s operations and the value of its nonoperating assets. A company’s value is shared between nonequity claims and equity holders. The equity value of a company equals enterprise value less the value of nonequity claims. PRESENT VALUE OF OPERATIONS Present value of free cash flows Present value of continuing value NONOPERATING ASSETS ENTERPRISE VALUE NONEQUITY CLAIMS Excess cash and marketable securities Debt Pensions/leases Illiquid investments and unconsolidated subsidiaries EQUITY VALUE Employee options Minority interests 3

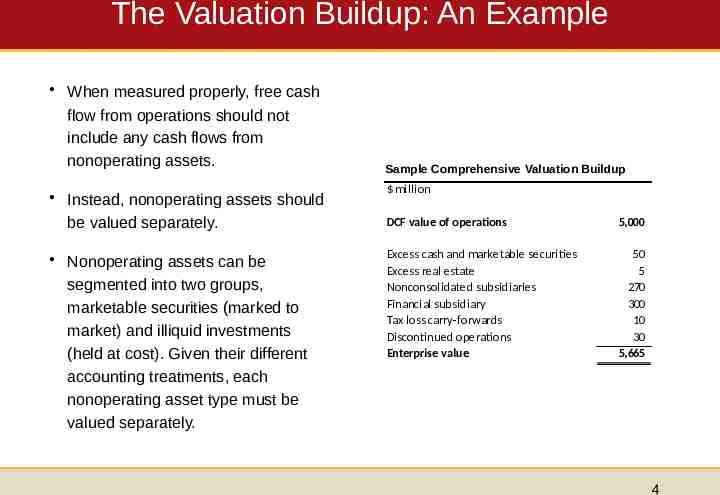

The Valuation Buildup: An Example When measured properly, free cash flow from operations should not include any cash flows from nonoperating assets. Instead, nonoperating assets should be valued separately. Nonoperating assets can be segmented into two groups, marketable securities (marked to market) and illiquid investments (held at cost). Given their different accounting treatments, each nonoperating asset type must be valued separately. Sample Comprehensive Valuation Buildup million DCF value of operations 5,000 Excess cash and marketable securities Excess real estate Nonconsolidated subsidiaries Financial subsidiary Tax loss carry-forwards Discontinued operations Enterprise value 50 5 270 300 10 30 5,665 4

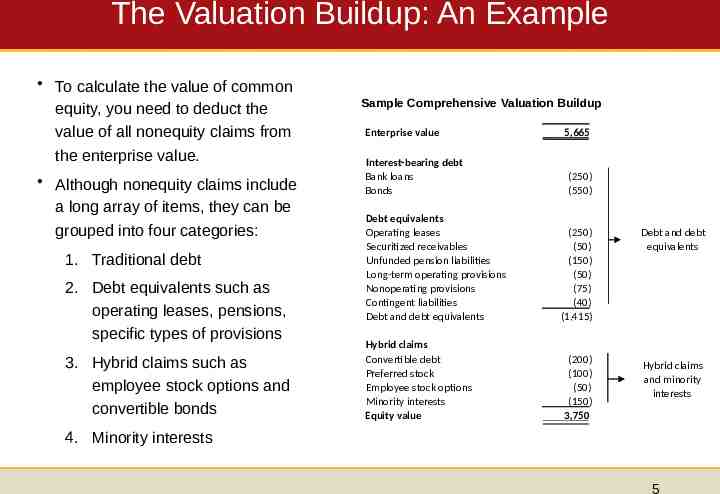

The Valuation Buildup: An Example To calculate the value of common equity, you need to deduct the value of all nonequity claims from the enterprise value. Although nonequity claims include a long array of items, they can be grouped into four categories: 1. Traditional debt 2. Debt equivalents such as operating leases, pensions, specific types of provisions 3. Hybrid claims such as employee stock options and convertible bonds Sample Comprehensive Valuation Buildup Enterprise value Interest-bearing debt Bank loans Bonds Debt equivalents Operating leases Securitized receivables Unfunded pension liabilities Long-term operating provisions Nonoperating provisions Contingent liabilities Debt and debt equivalents Hybrid claims Convertible debt Preferred stock Employee stock options Minority interests Equity value 5,665 (250) (550) (250) (50) (150) (50) (75) (40) (1,415) (200) (100) (50) (150) 3,750 Debt and debt equivalents Hybrid claims and minority interests 4. Minority interests 5

Session Overview When you have completed the valuation of core operations, you are ready to estimate three values: enterprise value, equity value, and value per share. 1. To determine enterprise value, add to the value of core operations the value of nonoperating assets, such as excess cash and nonconsolidated subsidiaries. 2. To convert enterprise value to equity value, subtract short-term and long-term debt, debt equivalents (such as unfunded pension liabilities), and hybrid securities (such as employee stock options). 3. To estimate value per share, divide the resulting equity value by the most recent number of undiluted shares outstanding. Estimating the value per share completes the technical aspect of the valuation, yet the entire job is not complete. It is time to revisit the valuation with a comprehensive look at its implications. We examine this process in the next session. 6

Common Nonoperating Assets Nonoperating assets are assets that do not generate free cash flow (or economic profit) and, therefore, do not impact the value of operations. Excess cash and marketable securities. Under U.S. generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS), companies must report such assets at their fair market value on the balance sheet. Therefore, use the most recent book value as a proxy for the current market value. Nonconsolidated subsidiaries. Nonconsolidated subsidiaries and equity investments are companies in which the parent company holds a noncontrolling equity stake. Because the parent company does not have formal control over these subsidiaries, their financials are not consolidated, so these investments must be valued separately from operations. Customer financing arms. Because financial subsidiaries differ greatly from manufacturing and services businesses, it is critical to separate revenues, expenses, and balance sheet accounts associated with the subsidiary from core operations. 7

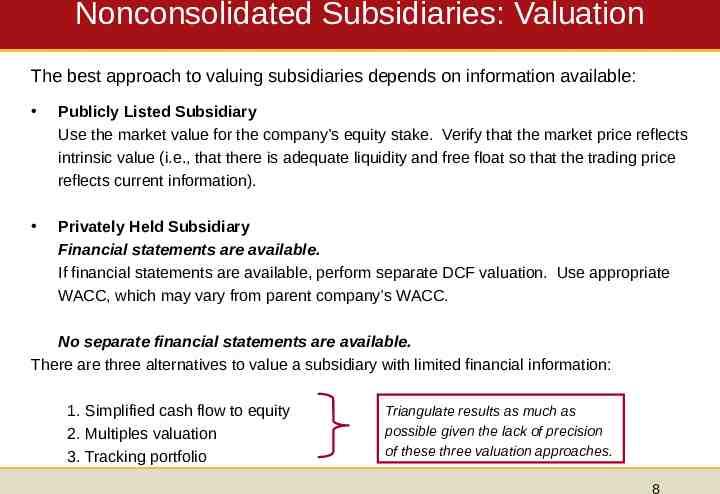

Nonconsolidated Subsidiaries: Valuation The best approach to valuing subsidiaries depends on information available: Publicly Listed Subsidiary Use the market value for the company’s equity stake. Verify that the market price reflects intrinsic value (i.e., that there is adequate liquidity and free float so that the trading price reflects current information). Privately Held Subsidiary Financial statements are available. If financial statements are available, perform separate DCF valuation. Use appropriate WACC, which may vary from parent company’s WACC. No separate financial statements are available. There are three alternatives to value a subsidiary with limited financial information: 1. Simplified cash flow to equity 2. Multiples valuation 3. Tracking portfolio Triangulate results as much as possible given the lack of precision of these three valuation approaches. 8

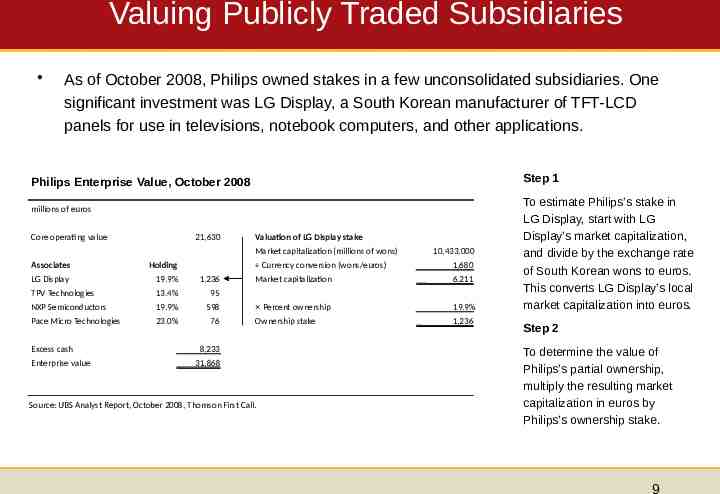

Valuing Publicly Traded Subsidiaries As of October 2008, Philips owned stakes in a few unconsolidated subsidiaries. One significant investment was LG Display, a South Korean manufacturer of TFT-LCD panels for use in televisions, notebook computers, and other applications. Step 1 Philips Enterprise Value, October 2008 millions of euros Core operating value 21,630 Valuation of LG Display stake Market capitalization (millions of wons) Associates LG Display Holding 19.9% 1,236 TPV Technologies 13.4% 95 NXP Semiconductors Pace Micro Technologies 19.9% 23.0% 598 76 Excess cash Enterprise value 10,433,000 Currency conversion (wons/euros) Market capitalization 1,680 6,211 Percent ownership Ownership stake 19.9% 1,236 8,233 31,868 Source: UBS Analyst Report, October 2008, Thomson First Call. To estimate Philips’s stake in LG Display, start with LG Display’s market capitalization, and divide by the exchange rate of South Korean wons to euros. This converts LG Display’s local market capitalization into euros. Step 2 To determine the value of Philips’s partial ownership, multiply the resulting market capitalization in euros by Philips’s ownership stake. 9

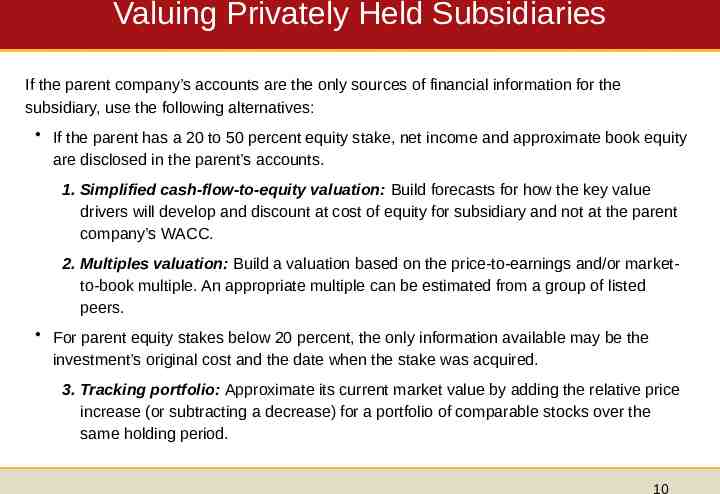

Valuing Privately Held Subsidiaries If the parent company’s accounts are the only sources of financial information for the subsidiary, use the following alternatives: If the parent has a 20 to 50 percent equity stake, net income and approximate book equity are disclosed in the parent’s accounts. 1. Simplified cash-flow-to-equity valuation: Build forecasts for how the key value drivers will develop and discount at cost of equity for subsidiary and not at the parent company’s WACC. 2. Multiples valuation: Build a valuation based on the price-to-earnings and/or marketto-book multiple. An appropriate multiple can be estimated from a group of listed peers. For parent equity stakes below 20 percent, the only information available may be the investment’s original cost and the date when the stake was acquired. 3. Tracking portfolio: Approximate its current market value by adding the relative price increase (or subtracting a decrease) for a portfolio of comparable stocks over the same holding period. 10

Customer Financing Arms To make their products more accessible, some companies operate customer financing businesses. Because financial subsidiaries differ greatly from manufacturing and services businesses, it is critical to separate revenues, expenses, and balance sheet accounts associated with the subsidiary from core operations. Failing to do so will distort return on invested capital, free cash flow, and ultimately your perspective on the company’s valuation. 11

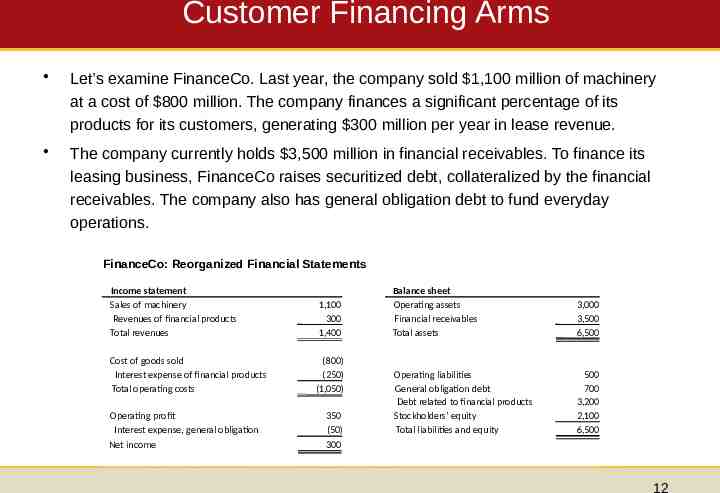

Customer Financing Arms Let’s examine FinanceCo. Last year, the company sold 1,100 million of machinery at a cost of 800 million. The company finances a significant percentage of its products for its customers, generating 300 million per year in lease revenue. The company currently holds 3,500 million in financial receivables. To finance its leasing business, FinanceCo raises securitized debt, collateralized by the financial receivables. The company also has general obligation debt to fund everyday operations. FinanceCo: Reorganized Financial Statements Income statement Sales of machinery Revenues of financial products Total revenues 1,100 300 1,400 Cost of goods sold Interest expense of financial products Total operating costs (800) (250) (1,050) Operating profit Interest expense, general obligation 350 (50) Net income 300 Balance sheet Operating assets Financial receivables Total assets 3,000 3,500 6,500 Operating liabilities General obligation debt Debt related to financial products Stockholders' equity Total liabilities and equity 500 700 3,200 2,100 6,500 12

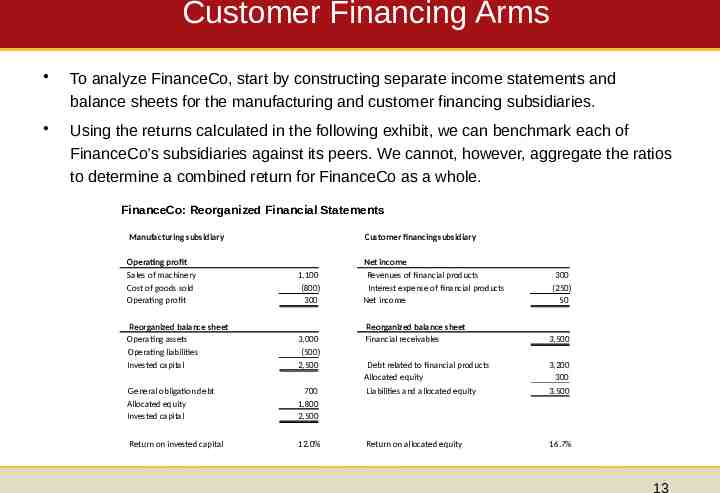

Customer Financing Arms To analyze FinanceCo, start by constructing separate income statements and balance sheets for the manufacturing and customer financing subsidiaries. Using the returns calculated in the following exhibit, we can benchmark each of FinanceCo’s subsidiaries against its peers. We cannot, however, aggregate the ratios to determine a combined return for FinanceCo as a whole. FinanceCo: Reorganized Financial Statements Manufacturing subsidiary Customer financing subsidiary Operating profit Sales of machinery Cost of goods sold Operating profit 1,100 (800) 300 Reorganized balance sheet Operating assets Operating liabilities Invested capital 3,000 (500) 2,500 General obligation debt Allocated equity Invested capital 700 1,800 2,500 Return on invested capital 12.0% Net income Revenues of financial products Interest expense of financial products Net income 300 (250) 50 Reorganized balance sheet Financial receivables 3,500 Debt related to financial products Allocated equity Liabilities and allocated equity 3,200 300 3,500 Return on allocated equity 16.7% 13

Other Nonoperating Assets The preceding items are typically the most significant nonoperating assets. However, companies can have other forms of nonoperating assets as well: Tax loss carry-forwards: Create a separate account for the accumulated tax loss carry-forwards, and forecast the development of this account by adding any future losses and subtracting any future taxable profits on a year-by-year basis. Discount at the cost of debt. Discontinued operations: Most recent book value is a reasonable approximation since assets and liabilities associated with discontinued operations are written down to fair value and disclosed as a net asset on the balance sheet. Excess real estate and other unutilized assets: Identifying these assets is nearly impossible unless they are specifically disclosed in a footnote. For excess real estate, use the most recent appraisal value, an appraisal multiple such as value per square meter, or discounting of future cash flows. 14

Session Overview When you have completed the valuation of core operations, you are ready to estimate three values: enterprise value, equity value, and value per share. 1. To determine enterprise value, add to the value of core operations the value of nonoperating assets, such as excess cash and nonconsolidated subsidiaries. 2. To convert enterprise value to equity value, subtract short-term and long-term debt, debt equivalents (such as unfunded pension liabilities), and hybrid securities (such as employee stock options). 3. To estimate value per share, divide the resulting equity value by the most recent number of undiluted shares outstanding. Estimating the value per share completes the technical aspect of the valuation, yet the entire job is not complete. It is time to revisit the valuation with a comprehensive look at its implications. We examine this process in the next session. 15

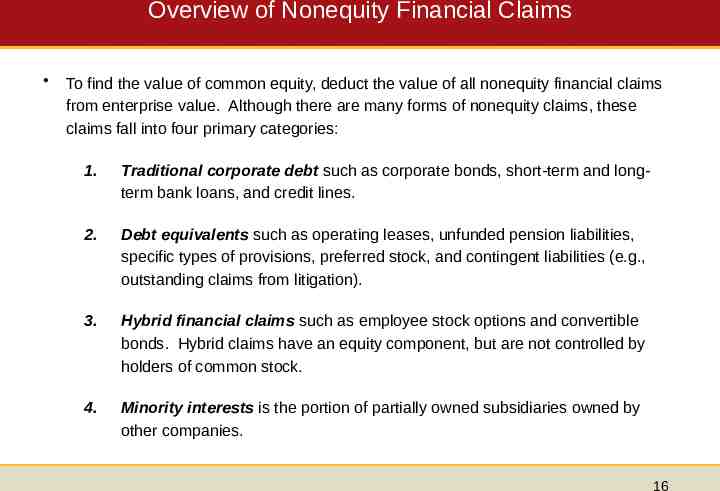

Overview of Nonequity Financial Claims To find the value of common equity, deduct the value of all nonequity financial claims from enterprise value. Although there are many forms of nonequity claims, these claims fall into four primary categories: 1. Traditional corporate debt such as corporate bonds, short-term and longterm bank loans, and credit lines. 2. Debt equivalents such as operating leases, unfunded pension liabilities, specific types of provisions, preferred stock, and contingent liabilities (e.g., outstanding claims from litigation). 3. Hybrid financial claims such as employee stock options and convertible bonds. Hybrid claims have an equity component, but are not controlled by holders of common stock. 4. Minority interests is the portion of partially owned subsidiaries owned by other companies. 16

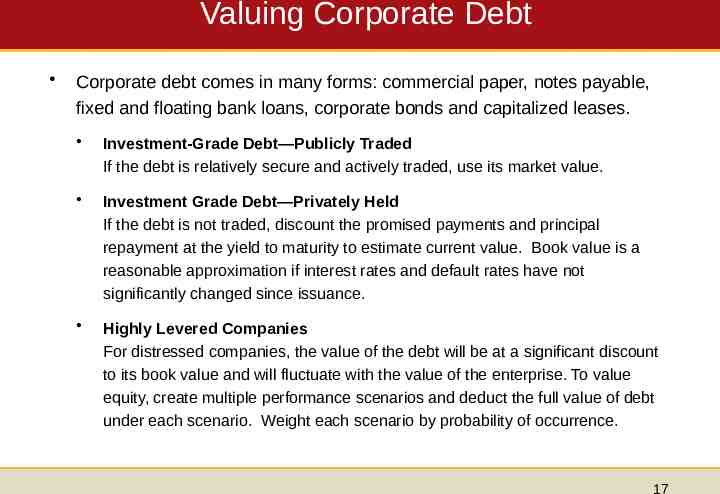

Valuing Corporate Debt Corporate debt comes in many forms: commercial paper, notes payable, fixed and floating bank loans, corporate bonds and capitalized leases. Investment-Grade Debt—Publicly Traded If the debt is relatively secure and actively traded, use its market value. Investment Grade Debt—Privately Held If the debt is not traded, discount the promised payments and principal repayment at the yield to maturity to estimate current value. Book value is a reasonable approximation if interest rates and default rates have not significantly changed since issuance. Highly Levered Companies For distressed companies, the value of the debt will be at a significant discount to its book value and will fluctuate with the value of the enterprise. To value equity, create multiple performance scenarios and deduct the full value of debt under each scenario. Weight each scenario by probability of occurrence. 17

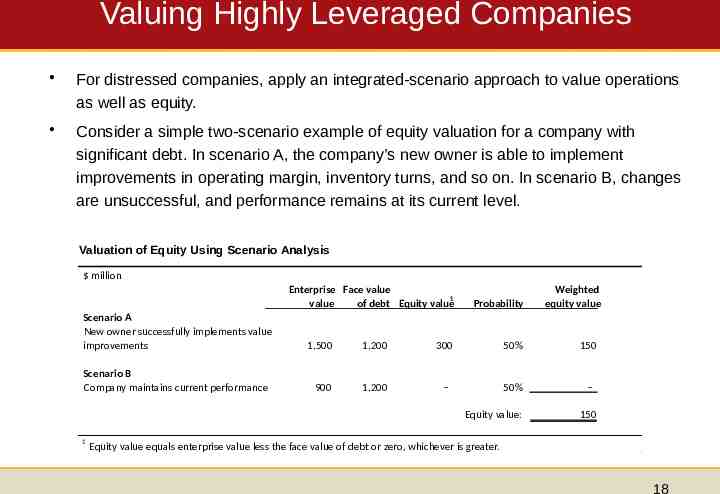

Valuing Highly Leveraged Companies For distressed companies, apply an integrated-scenario approach to value operations as well as equity. Consider a simple two-scenario example of equity valuation for a company with significant debt. In scenario A, the company’s new owner is able to implement improvements in operating margin, inventory turns, and so on. In scenario B, changes are unsuccessful, and performance remains at its current level. Valuation of Equity Using Scenario Analysis million Enterprise Face value 1 value of debt Equity value Scenario A New owner successfully implements value improvements Scenario B Company maintains current performance Probability 1,500 1,200 300 50% 150 900 1,200 50% Equity value: 1 Weighted equity value 150 Equity value equals enterprise value less the face value of debt or zero, whichever is greater. 18

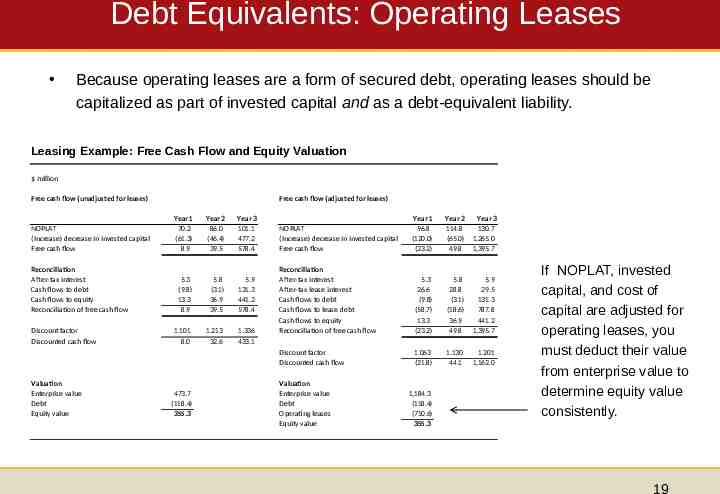

Debt Equivalents: Operating Leases Because operating leases are a form of secured debt, operating leases should be capitalized as part of invested capital and as a debt-equivalent liability. Leasing Example: Free Cash Flow and Equity Valuation million Free cash flow (unadjusted for leases) NOPLAT (Increase) decrease in invested capital Free cash flow Reconciliation After-tax interest Cash flows to debt Cash flows to equity Reconciliation of free cash flow Discount factor Discounted cash flow Valuation Enterprise value Debt Equity value Free cash flow (adjusted for leases) Year 1 70.2 (61.3) 8.9 Year 2 86.0 (46.4) 39.5 Year 3 101.1 477.2 578.4 5.3 (9.8) 13.3 8.9 5.8 (3.1) 36.9 39.5 5.9 131.3 441.2 578.4 1.101 8.0 1.213 32.6 1.336 433.1 473.7 (118.4) 355.3 Year 1 96.8 (120.0) (23.2) Year 2 114.8 (65.0) 49.8 Year 3 130.7 1,265.0 1,395.7 Reconciliation After-tax interest After-tax lease interest Cash flows to debt Cash flows to lease debt Cash flows to equity Reconciliation of free cash flow 5.3 26.6 (9.8) (58.7) 13.3 (23.2) 5.8 28.8 (3.1) (18.6) 36.9 49.8 5.9 29.5 131.3 787.8 441.2 1,395.7 Discount factor Discounted cash flow 1.063 (21.8) 1.130 44.1 1.201 1,162.0 NOPLAT (Increase) decrease in invested capital Free cash flow Valuation Enterprise value Debt Operating leases Equity value 1,184.3 (118.4) (710.6) 355.3 If NOPLAT, invested capital, and cost of capital are adjusted for operating leases, you must deduct their value from enterprise value to determine equity value consistently. 19

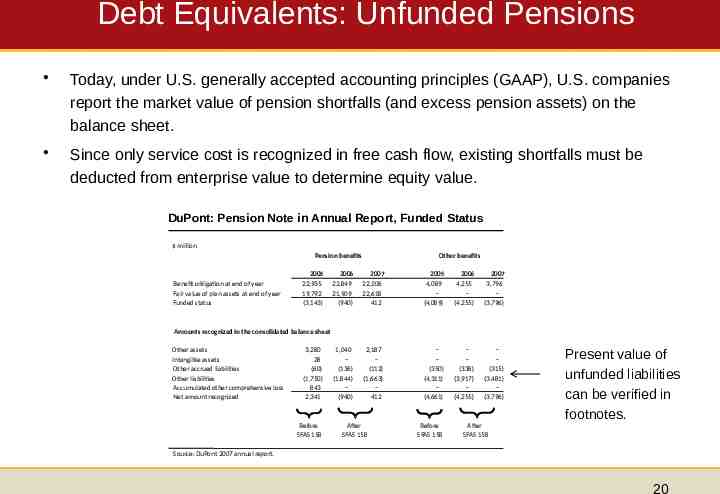

Debt Equivalents: Unfunded Pensions Today, under U.S. generally accepted accounting principles (GAAP), U.S. companies report the market value of pension shortfalls (and excess pension assets) on the balance sheet. Since only service cost is recognized in free cash flow, existing shortfalls must be deducted from enterprise value to determine equity value. DuPont: Pension Note in Annual Report, Funded Status million Pension benefits Benefit obligation at end of year Fair value of plan assets at end of year Funded status 2005 22,935 19,792 (3,143) Other benefits 2006 22,849 21,909 (940) 2007 22,206 22,618 412 2005 4,089 (4,089) 2006 4,255 (4,255) 2007 3,796 (3,796) 1,040 (136) (1,844) (940) 2,187 (112) (1,663) 412 (350) (4,311) (4,661) (338) (3,917) (4,255) (315) (3,481) (3,796) Amounts recognized in the consolidated balance sheet Other assets Intangible assets Other accrued liabilities Other liabilities Accumulated other comprehensive loss Net amount recognized 3,280 28 (60) (1,750) 843 2,341 Before SFAS 158 After SFAS 158 Before SFAS 158 Present value of unfunded liabilities can be verified in footnotes. After SFAS 158 Source: DuPont 2007 annual report. 20

Other Debt Equivalents Other common debt equivalents: For long-term operating provisions and nonoperating provisions, the balance sheet value offers a reasonable approximation. Long-term operating provisions (e.g., plant-decommissioning costs) are typically recorded at a discounted value. Nonoperating provisions (e.g., restructuring charges) are generally recorded at a nondiscounted value, but are near term in nature. Contingent liabilities (e.g., pending litigation) should be valued by estimating the associated expected (not book) after-tax cash flows and discounted at the cost of debt. 21

Hybrid Securities: Convertible Debt Convertible bonds differ from traditional debt in that they give the holder the additional right to convert the bonds into common stock. If the convertible bonds are actively traded, deduct their market value, but only if estimated stock price is near the traded stock price, as the value of convertible bonds depends on your estimate of equity value. If the market price differs from your estimate of share price, 1. Option valuation approach: The value of convertible bonds can be estimated using an adjusted Black-Scholes convertible bond pricing model. 2. Conversion value approach: This common approach assumes that all convertible bonds are immediately exchanged for equity and ignores the time value of the conversion option. The approach works well when the conversion option is deep in the money. 22

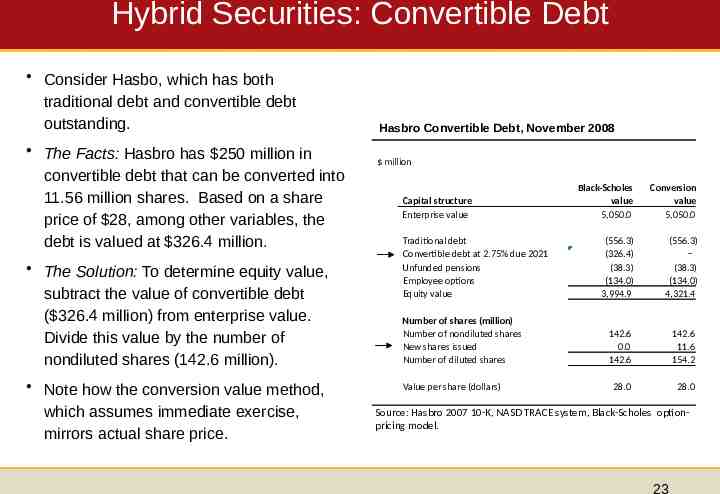

Hybrid Securities: Convertible Debt Consider Hasbo, which has both traditional debt and convertible debt outstanding. The Facts: Hasbro has 250 million in convertible debt that can be converted into 11.56 million shares. Based on a share price of 28, among other variables, the debt is valued at 326.4 million. The Solution: To determine equity value, subtract the value of convertible debt ( 326.4 million) from enterprise value. Divide this value by the number of nondiluted shares (142.6 million). Note how the conversion value method, which assumes immediate exercise, mirrors actual share price. Hasbro Convertible Debt, November 2008 million Capital structure Enterprise value Traditional debt Convertible debt at 2.75% due 2021 Unfunded pensions Employee options Equity value Number of shares (million) Number of nondiluted shares New shares issued Number of diluted shares Value per share (dollars) Black-Scholes value 5,050.0 Conversion value 5,050.0 (556.3) (326.4) (38.3) (134.0) 3,994.9 (556.3) (38.3) (134.0) 4,321.4 142.6 0.0 142.6 142.6 11.6 154.2 28.0 28.0 Source: Hasbro 2007 10-K, NASD TRACE system, Black-Scholes optionpricing model. 23

Employee Stock Options Employee stock options give the holder the right, but not the obligation, to buy company stock at a specified price, known as the exercise price. If not specifically expensed as part of NOPLAT, outstanding options must be treated as a nonequity claim: Option valuation models: The value of options can be estimated using optionvaluation models such as Black-Scholes or advanced binomial (lattice) models. Under U.S. GAAP and IFRS, the notes to the balance sheet report the value of all employee stock options outstanding as estimated by option-pricing models. This value is a good approximation only if your estimate of share price is close to the one underlying the option values in the footnotes. Exercise value approach: This common method provides only a lower bound for the value of employee options. It assumes that all options are exercised immediately and thereby ignores the time value of options. 24

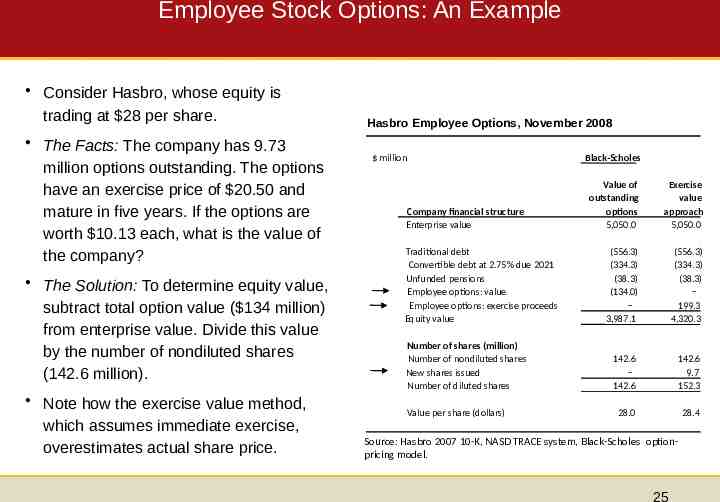

Employee Stock Options: An Example Consider Hasbro, whose equity is trading at 28 per share. The Facts: The company has 9.73 million options outstanding. The options have an exercise price of 20.50 and mature in five years. If the options are worth 10.13 each, what is the value of the company? The Solution: To determine equity value, subtract total option value ( 134 million) from enterprise value. Divide this value by the number of nondiluted shares (142.6 million). Note how the exercise value method, which assumes immediate exercise, overestimates actual share price. Hasbro Employee Options, November 2008 million Black-Scholes Company financial structure Enterprise value Traditional debt Convertible debt at 2.75% due 2021 Unfunded pensions Employee options: value Employee options: exercise proceeds Equity value Number of shares (million) Number of nondiluted shares New shares issued Number of diluted shares Value per share (dollars) Value of outstanding options 5,050.0 Exercise value approach 5,050.0 (556.3) (334.3) (38.3) (134.0) 3,987.1 (556.3) (334.3) (38.3) 199.3 4,320.3 142.6 142.6 142.6 9.7 152.3 28.0 28.4 Source: Hasbro 2007 10-K, NASD TRACE system, Black-Scholes optionpricing model. 25

Minority Interest What is a minority interest? When a company controls a subsidiary without full ownership, the subsidiary’s financial position must be fully consolidated in the group accounts. The portion of third-party ownership is classified as minority interest, and this must be deducted as a nonequity claim. A minority interest is a claim only on a particular nonconsolidated subsidiary; its valuation is related to the subsidiary, not the company as a whole. If the subsidiary is publicly listed, deduct the proportional market value owned by outsiders from enterprise value to determine equity value. If the subsidiary is privately held, you can perform a separate valuation of the minority interest using a DCF approach, multiples, or a tracking portfolio, depending on the information available. 26

Session Overview When you have completed the valuation of core operations, you are ready to estimate three values: enterprise value, equity value, and value per share. 1. To determine enterprise value, add to the value of core operations the value of nonoperating assets, such as excess cash and nonconsolidated subsidiaries. 2. To convert enterprise value to equity value, subtract short-term and long-term debt, debt equivalents (such as unfunded pension liabilities), and hybrid securities (such as employee stock options). 3. To estimate value per share, divide the resulting equity value by the most recent number of undiluted shares outstanding. Estimating the value per share completes the technical aspect of the valuation, yet the entire job is not complete. It is time to revisit the valuation with a comprehensive look at its implications. We examine this process in the next session. 27

Calculating Value per Share How you determine the value per share depends on how options and convertible debt are valued. The two methods are: Option-Based Valuation Divide the total equity value by the number of undiluted shares outstanding. Use undiluted shares outstanding because the value of convertible debt and stock options has already been deducted from the enterprise value. The number of shares outstanding is the gross number of shares issued, less the number of shares in treasury. Conversion and Exercise Value Method Divide the total equity value by the diluted number of shares. Under this method, convertible debt and stock options are not incorporated as nonequity claims, but rather through the number of shares outstanding. This method generates a different equity value than the option-based valuation. 28