Distribution and Risk Mitigation Silja Calac, ITFA Board Member

14 Slides779.57 KB

Distribution and Risk Mitigation Silja Calac, ITFA Board Member and Senior Underwriter, Swiss Re Corporate Solutions Paolo Carrozza, Chief Commercial Officer Middle East, Euler Hermes GCC Dubai, 13 February 2017 1

AGENDA Brief summary of the Regulatory Environment : Capital Requirements / Basel III Risk Mitigation and Distribution of Trade Assets: Different forms of risk mitigation Insurance: Various risk cover available for transaction banking / trade finance 2

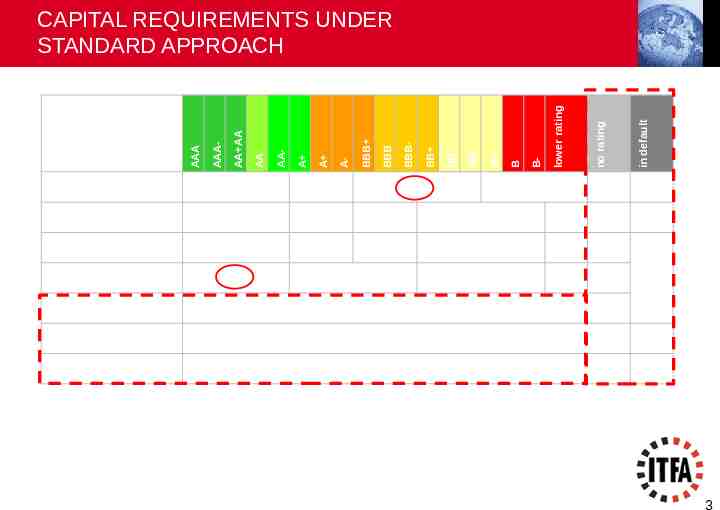

Bank's residence country Banks / Insurance Retail Commercial property Private property 150% 150% 150% 100% 100% 150% 50% 0% 20% 50% 100% 20% 50% 100% 20% 100% 50% lower rating 100% 50% B- 150% 20% B 150% B 100% BB- BB BB BBB- BBB BBB A- A A AA- AA AA AA in default Sovereigns no rating Corporate Customers AAA- AAA CAPITAL REQUIREMENTS UNDER STANDARD APPROACH 150% 75% 50 to 100%, to the discretion of local monetary authority 150% 35% 150% 3

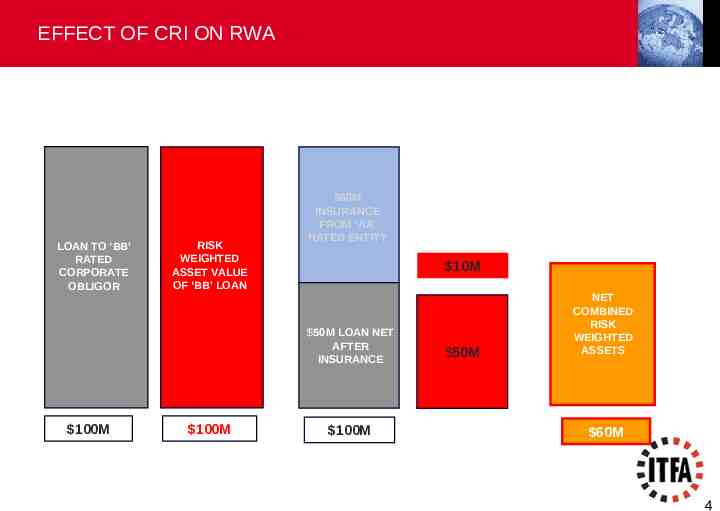

EFFECT OF CRI ON RWA LOAN TO ‘BB’ RATED CORPORATE OBLIGOR RISK WEIGHTED ASSET VALUE OF ‘BB’ LOAN 50M INSURANCE FROM ‘AA’ RATED ENTITY 10M 50M LOAN NET AFTER INSURANCE 100M 100M 100M 50M NET COMBINED RISK WEIGHTED ASSETS 60M 4

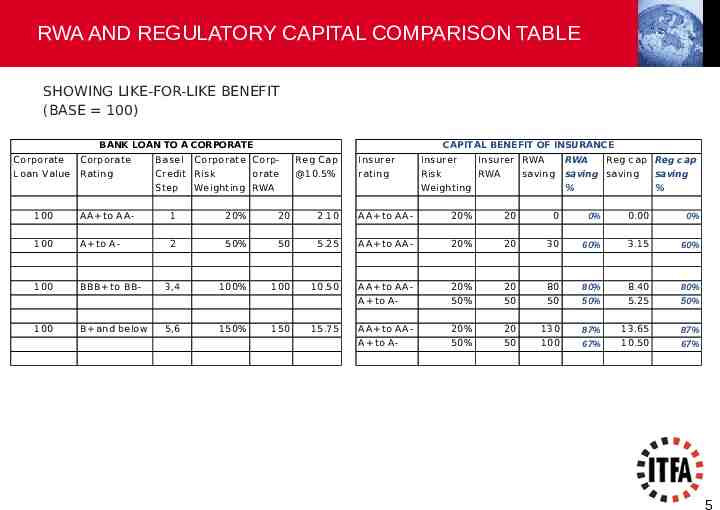

RWA AND REGULATORY CAPITAL COMPARISON TABLE SHOWING LIKE-FOR-LIKE BENEFIT (BASE 100) CAPITAL BENEFIT OF INSURANCE BANK LOAN TO A CORPORATE Corporate Corporate Basel L oan Value Rating Credit Risk Step Corporate Corporate Reg Cap I nsurer Ins urer Ins urer RWA RWA @ 10.5% rating Ris k RWA saving saving saving % % Weighting RWA saving Weighting Reg c ap Reg c ap 100 AA to AA- 1 20% 20 2.10 AA to AA- 20% 20 0 0% 0.00 0% 100 A to A- 2 50% 50 5.25 AA to AA- 20% 20 30 60% 3.15 60% 100 BBB to BB- 100% 100 10.50 AA to AA- 20% 20 80 80% 8.40 80% A to A- 50% 50 50 50% 5.25 50% AA to AA- 20% 20 130 87% 13.65 87% A to A- 50% 50 100 67% 10.50 67% 100 B and below 3,4 5,6 150% 150 15.75 5

DISTRIBUTION CHANNELS OVERVIEW Risk Participations Insurance Forfaiting Agreements Relative simplicity and possibility of being undisclosed to original parties Relies on a “fronting” bank administering the transaction until maturity Also undisclosed and a complementary source of risk capacity Unfunded only, and minimum hold requirements Ongoing framework for individual transactions sold on a forfaiting basis Typically requires recognition of assignment/endorsement/transfer Assignment Frameworks Equitable Assignment Care around perfection of assignment Synthetic Securitisations Possible capital relief from selling first loss on a portfolio Difficult to achieve “risk mitigation” Collateralised Loan Obligations Comprehensive benefits from selling a “vertical slice” of portfolio Expensive to set up, diversity requirements preclude large single tickets Special Purpose Vehicles ECAs / Multilaterals Repackaging transactions for institutional/alternative investors Single transactions may not be profitable enough to cover cost Sovereign / multilateral risk support for transactions Typically in the form of a guarantee only, and specific criteria have to be met 6

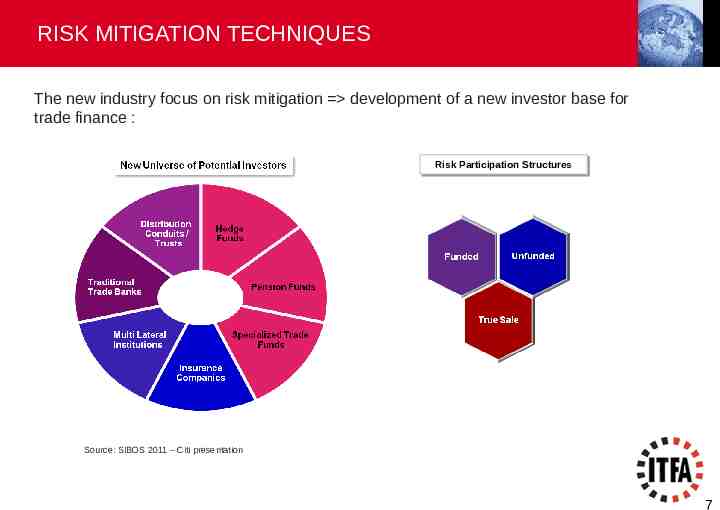

RISK MITIGATION TECHNIQUES The new industry focus on risk mitigation development of a new investor base for trade finance : Risk Risk Participation Participation Structures Structures Source: SIBOS 2011 – Citi presentation 7

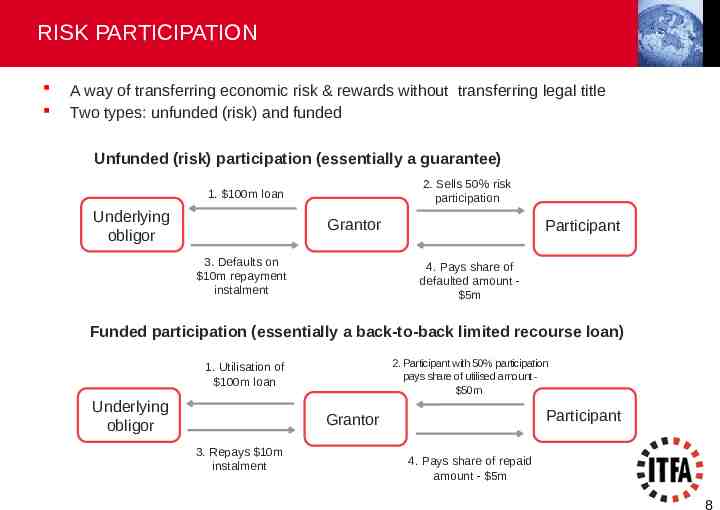

RISK PARTICIPATION A way of transferring economic risk & rewards without transferring legal title Two types: unfunded (risk) and funded Unfunded (risk) participation (essentially a guarantee) 2. Sells 50% risk participation 1. 100m loan Underlying obligor Grantor 3. Defaults on 10m repayment instalment Participant 4. Pays share of defaulted amount 5m Funded participation (essentially a back-to-back limited recourse loan) 2. Participant with 50% participation pays share of utilised amount 50m 1. Utilisation of 100m loan Underlying obligor Participant Grantor 3. Repays 10m instalment 4. Pays share of repaid amount - 5m 8

BAFT MRPA http://www.baft.org/policy/document-library 9

INTRODUCTION: WHY INSURANCE? The insurance market grew materially over the last 20 years as a consequence of growth in Emerging Market investments as well as political risk events (Argentina, Asian Debt crises, .) and an increase in banks’ acceptance of the benefits of using insurance. Overall market size is estimated at over 2.0-2.5bn annual premium and growing. Main placement hubs are London, Zurich, New York, Singapore. Whereas the cover is unfunded the key value proposition of the insurance market is that it typically does not compete directly with the banks and is confidential. Key benefits of using insurance are: Alternative distribution channel – Opportunity to sell down on a private/confidential basis, complementary with or as an alternative to traditional loan syndication. – Provides a straight forward mechanism for sell down of club or bi-lateral transactions. Additional capacity – On risks where you have reached internal credit limits (counterparty/country). – To write a larger share of transactions (obtaining better pricing or league table status) in the knowledge that you can sell down to insurer. Capital management – If cover is “unconditional” typically capital relief under Basel II/III on transactions, potentially enhancing return on capital committed to a transaction (specifically if “advanced” approach is used). – Manage concentrations against counterparties, sub-sectors, geographies etc. 10

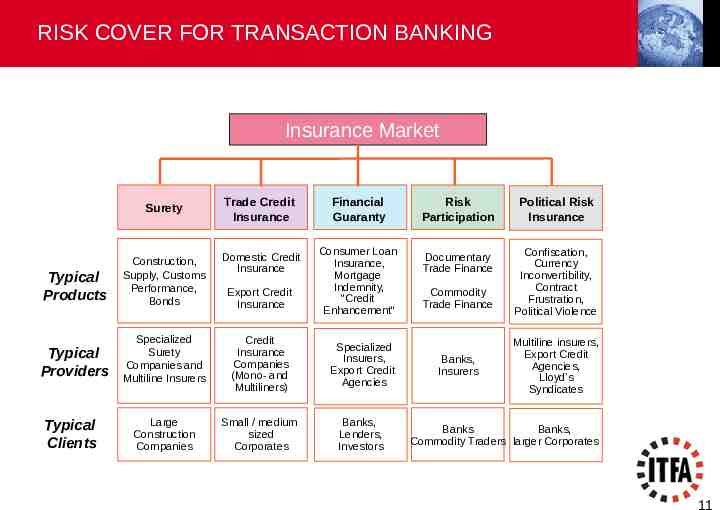

RISK COVER FOR TRANSACTION BANKING Insurance Market Solutions Surety Trade Credit Insurance Typical Products Construction, Supply, Customs Performance, Bonds Domestic Credit Insurance Typical Providers Specialized Surety Companies and Multiline Insurers Credit Insurance Companies (Mono- and Multiliners) Specialized Insurers, Export Credit Agencies Large Construction Companies Small / medium sized Corporates Banks, Lenders, Investors Typical Clients Export Credit Insurance Financial Guaranty Consumer Loan Insurance, Mortgage Indemnity, "Credit Enhancement" Risk Participation Political Risk Insurance Documentary Trade Finance Confiscation, Currency Inconvertibility, Contract Frustration, Political Violence Commodity Trade Finance Banks, Insurers Multiline insurers, Export Credit Agencies, Lloyd’s Syndicates Banks Banks, Commodity Traders larger Corporates Page 11 11

CREDIT RISK INSURANCE Cover: Non-payment of a debt or a financial obligation Credit Risk Insurance “CRI” – covering a wide range of financial obligations – loans, guarantees, documentary credits Short Term Trade Credit Insurance “TCI” – covering accounts receivable Non-payment caused by “3 Perils” : Confiscation/Expropriation, War/Political Violence and Inconvertibility Political Risk Insurance “PRI” – covering loans, guarantees, projects – parent company lending 12

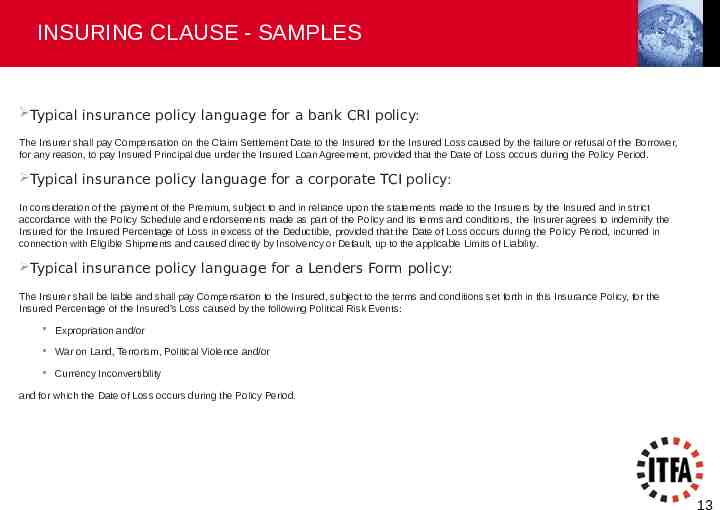

INSURING CLAUSE - SAMPLES Typical insurance policy language for a bank CRI policy: The Insurer shall pay Compensation on the Claim Settlement Date to the Insured for the Insured Loss caused by the failure or refusal of the Borrower, for any reason, to pay Insured Principal due under the Insured Loan Agreement, provided that the Date of Loss occurs during the Policy Period. Typical insurance policy language for a corporate TCI policy: In consideration of the payment of the Premium, subject to and in reliance upon the statements made to the Insurers by the Insured and in strict accordance with the Policy Schedule and endorsements made as part of the Policy and its terms and conditions, the Insurer agrees to indemnify the Insured for the Insured Percentage of Loss in excess of the Deductible, provided that the Date of Loss occurs during the Policy Period, incurred in connection with Eligible Shipments and caused directly by Insolvency or Default, up to the applicable Limits of Liability. Typical insurance policy language for a Lenders Form policy: The Insurer shall be liable and shall pay Compensation to the Insured, subject to the terms and conditions set forth in this Insurance Policy, for the Insured Percentage of the Insured’s Loss caused by the following Political Risk Events: Expropriation and/or War on Land, Terrorism, Political Violence and/or Currency Inconvertibility and for which the Date of Loss occurs during the Policy Period. 13

OUR WEBSITE: WWW.ITFA.ORG 14