DEBIT AND CREDIT THEORY

18 Slides1.15 MB

DEBIT AND CREDIT THEORY

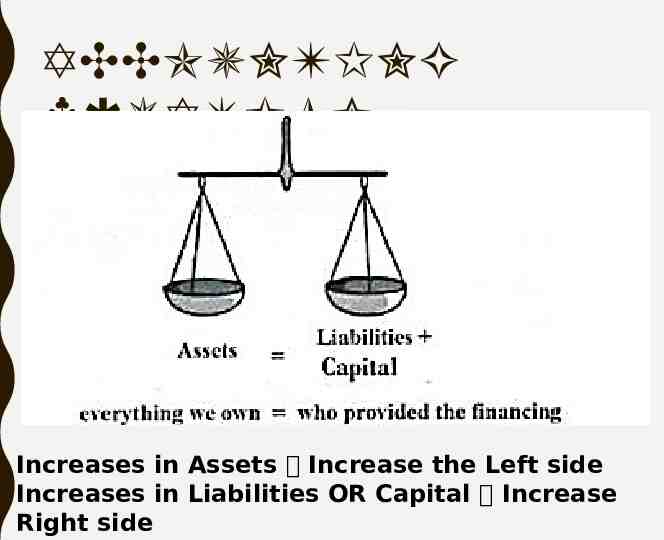

ACCOUNTING EQUATION Increases in Assets Increase the Left side Increases in Liabilities OR Capital Increase Right side

GOODBYE TRANSACTION ANALYSIS SHEET At times it was confusing to describe the many options that are possible as a 2nd account. “ Did assets decrease as well, or did liabilities OR owner’s equity increase?” We can summarize this by saying: anything that increases the left-side (or decreases right-side) is a . “left-side change” anything that increases the right-side (or decreases left-side) is a . “right-side change” Remember:

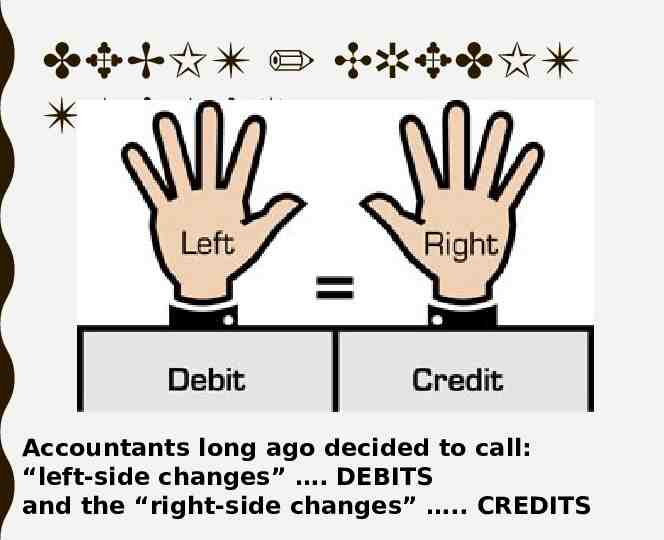

DEBIT / CREDIT THEORY Accountants long ago decided to call: “left-side changes” . DEBITS and the “right-side changes” . CREDITS

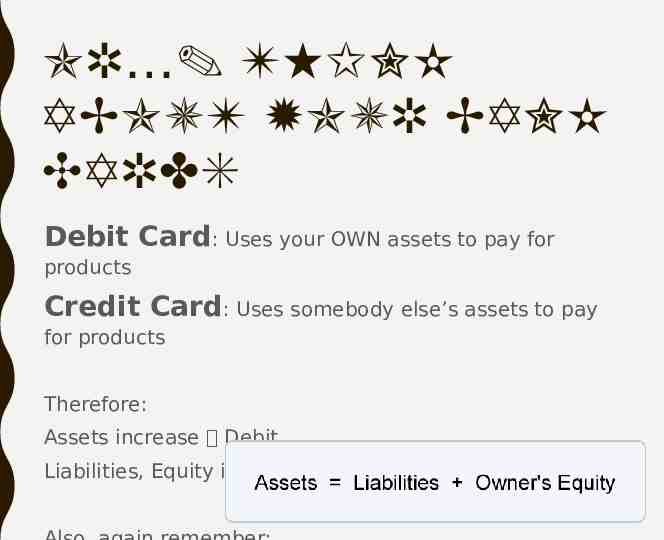

OR . THINK ABOUT YOUR BANK CARDS Debit Card: Uses your OWN assets to pay for products Credit Card: Uses somebody else’s assets to pay for products Therefore: Assets increase Debit Liabilities, Equity increase Credit

OR .

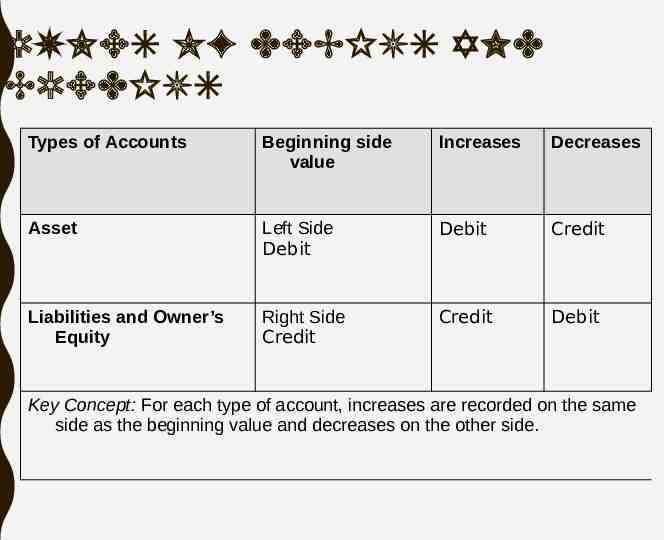

RULES OF DEBITS AND CREDITS Types of Accounts Beginning side value Increases Decreases Asset Left Side Debit Debit Credit Liabilities and Owner’s Equity Right Side Credit Credit Debit Key Concept: For each type of account, increases are recorded on the same side as the beginning value and decreases on the other side.

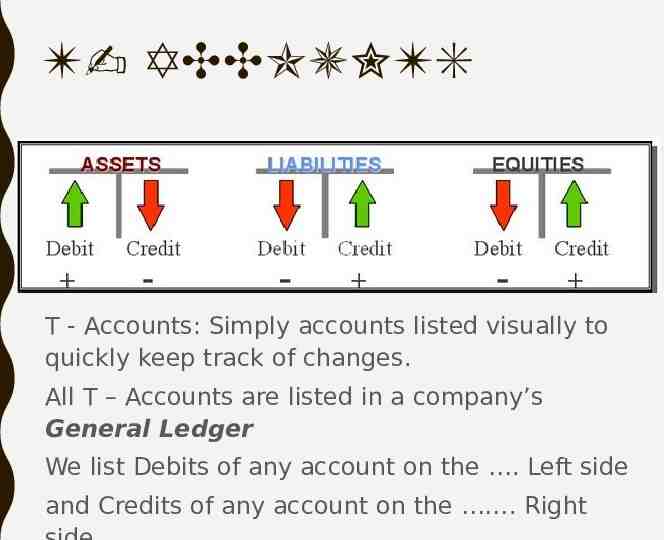

T- ACCOUNTS T - Accounts: Simply accounts listed visually to quickly keep track of changes. All T – Accounts are listed in a company’s General Ledger We list Debits of any account on the . Left side and Credits of any account on the . Right

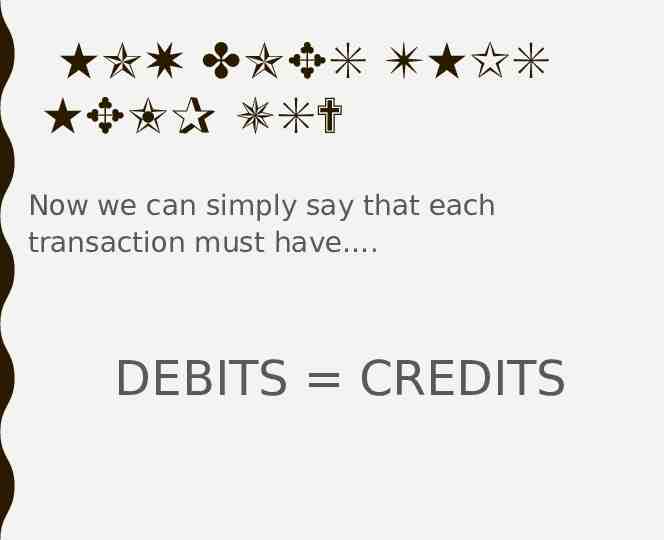

HOW DOES THIS HELP US? Now we can simply say that each transaction must have . DEBITS CREDITS

RECORD TRANSACTIONS USING TACCOUNTS 1. Enter in beginning balances. 2. Record transactions – Write date/transaction # – Record debit/credit amounts for all transactions 3. Total debit/credit sides of t-accounts 4. Calculate new account total NOTE: The collection of all T - Accounts is called the GENERAL LEDGER

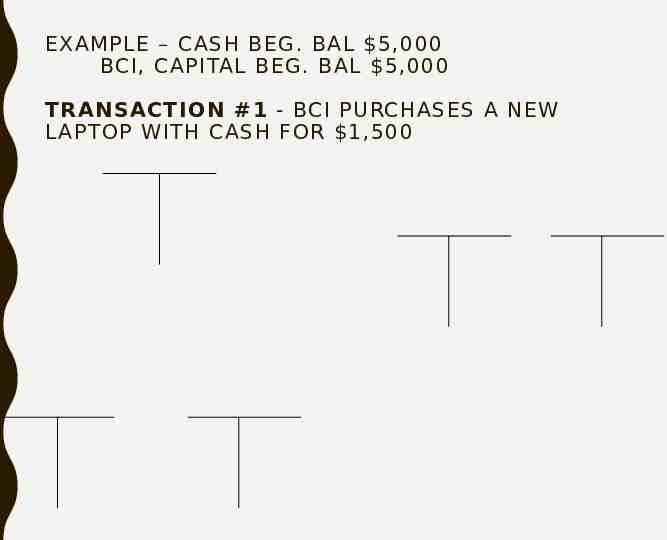

EXAMPLE – CASH BEG. BAL 5,000 BCI, CAPITAL BEG. BAL 5,000 TRANSACTION #1 - BCI PURCHASES A NEW LAPTOP WITH CASH FOR 1,500

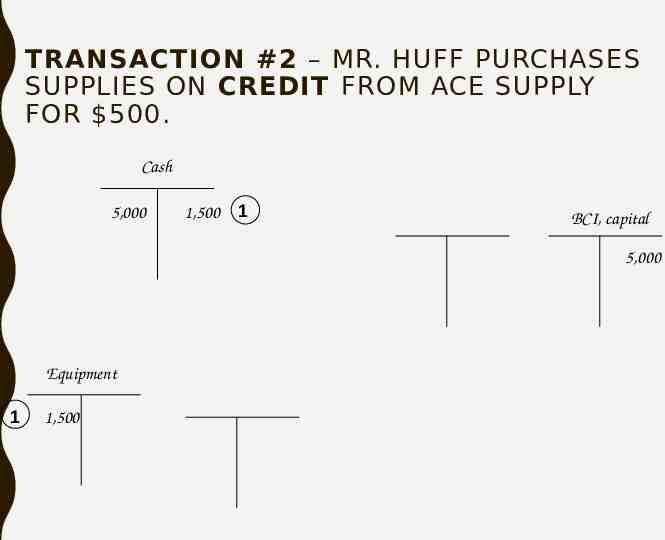

TRANSACTION #2 – MR. HUFF PURCHASES SUPPLIES ON CREDIT FROM ACE SUPPLY FOR 500. Cash 5,000 1,500 1 BCI, capital 5,000 Equipment 1 1,500

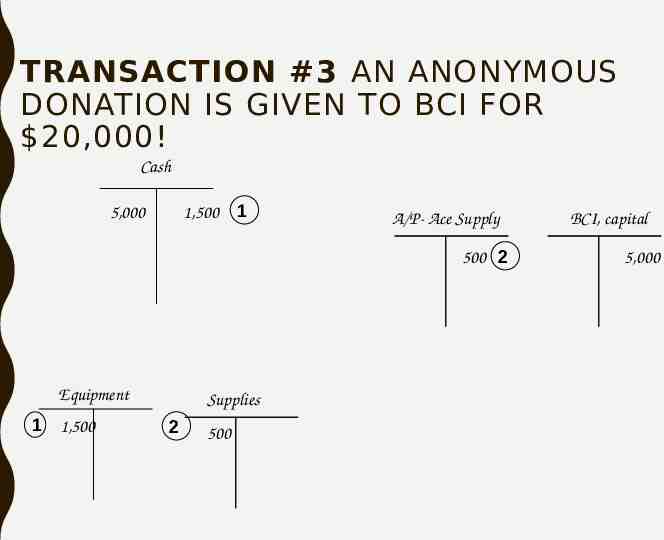

TRANSACTION #3 AN ANONYMOUS DONATION IS GIVEN TO BCI FOR 20,000! Cash 5,000 1,500 1 A/P- Ace Supply 500 2 Equipment 1 1,500 Supplies 2 500 BCI, capital 5,000

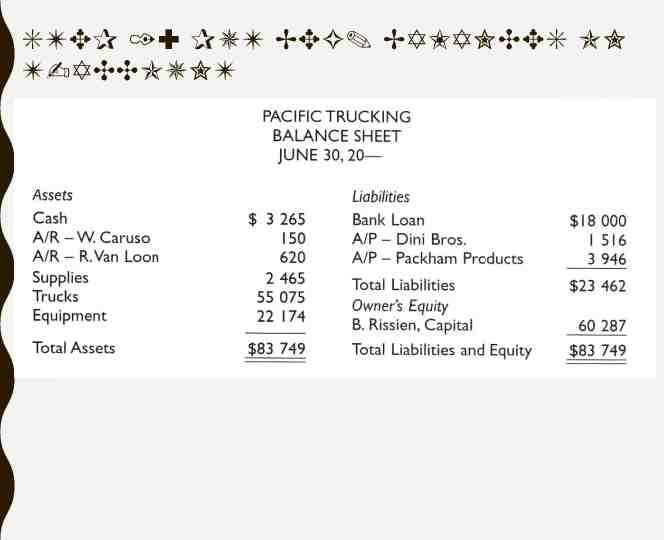

STEP 1: PUT BEG. BALANCES ON T-ACCOUNT

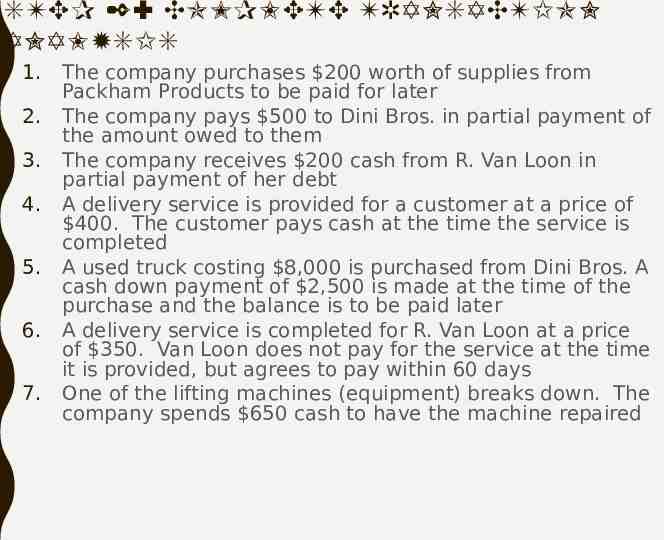

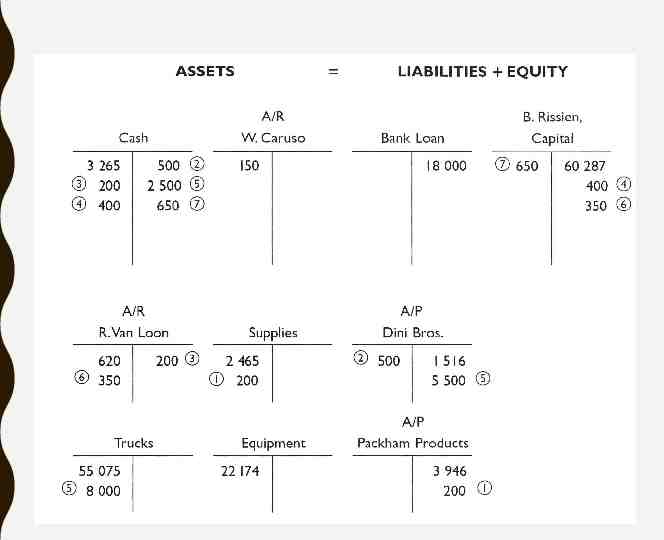

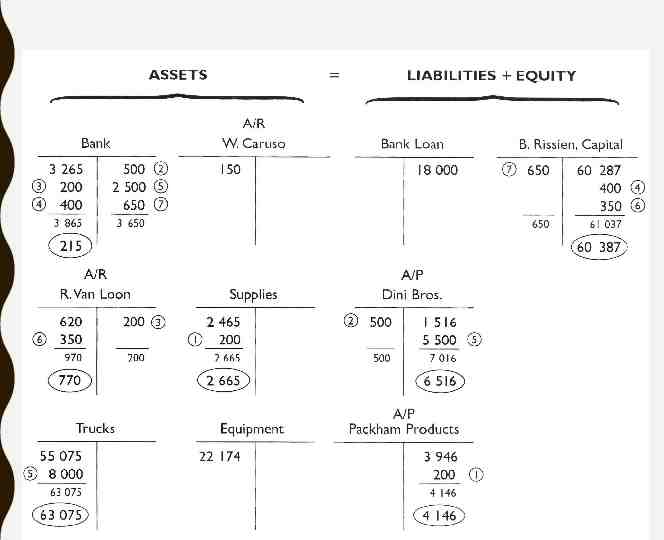

STEP 2: COMPLETE TRANSACTION ANALYSIS 1. 2. 3. 4. 5. 6. 7. The company purchases 200 worth of supplies from Packham Products to be paid for later The company pays 500 to Dini Bros. in partial payment of the amount owed to them The company receives 200 cash from R. Van Loon in partial payment of her debt A delivery service is provided for a customer at a price of 400. The customer pays cash at the time the service is completed A used truck costing 8,000 is purchased from Dini Bros. A cash down payment of 2,500 is made at the time of the purchase and the balance is to be paid later A delivery service is completed for R. Van Loon at a price of 350. Van Loon does not pay for the service at the time it is provided, but agrees to pay within 60 days One of the lifting machines (equipment) breaks down. The company spends 650 cash to have the machine repaired

HOMEWORK Page 62 # 12ab, 13ab, 14ab