Familiarization Programme for Independent Directors BSE: 539404

16 Slides1.69 MB

Familiarization Programme for Independent Directors BSE: 539404 NSE: SATIN CSE: 30024 Corporate Identity No. L65991DL1990PLC041796

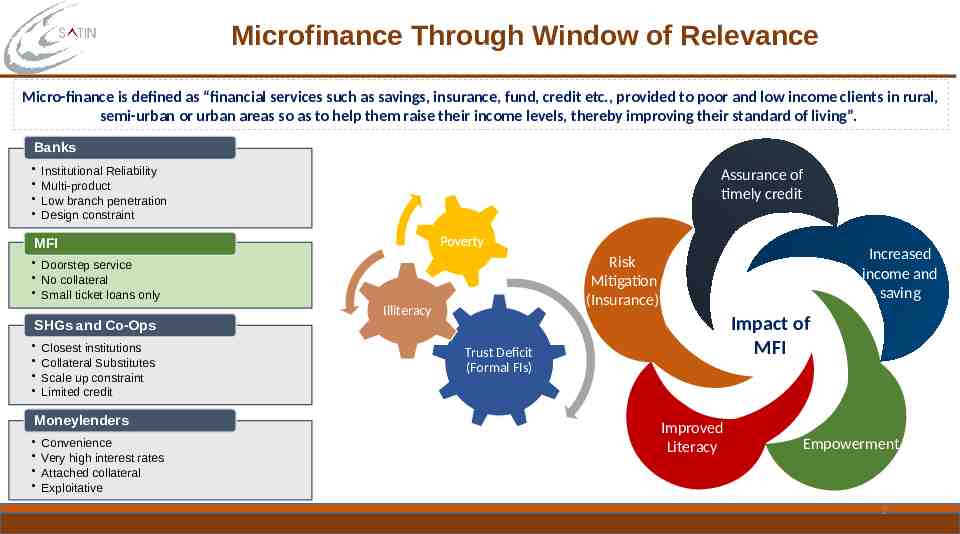

Microfinance Through Window of Relevance Micro-finance is defined as “financial services such as savings, insurance, fund, credit etc., provided to poor and low income clients in rural, semi-urban or urban areas so as to help them raise their income levels, thereby improving their standard of living”. Banks Institutional Reliability Multi-product Low branch penetration Design constraint Assurance of timely credit MFI SHGs and Co-Ops Closest institutions Collateral Substitutes Scale up constraint Limited credit Moneylenders Convenience Very high interest rates Attached collateral Exploitative Increased income and saving Risk Mitigation (Insurance) Doorstep service No collateral Small ticket loans only Illiteracy Impact of MFI Trust Deficit (Formal FIs) Improved Literacy Empowerment 2

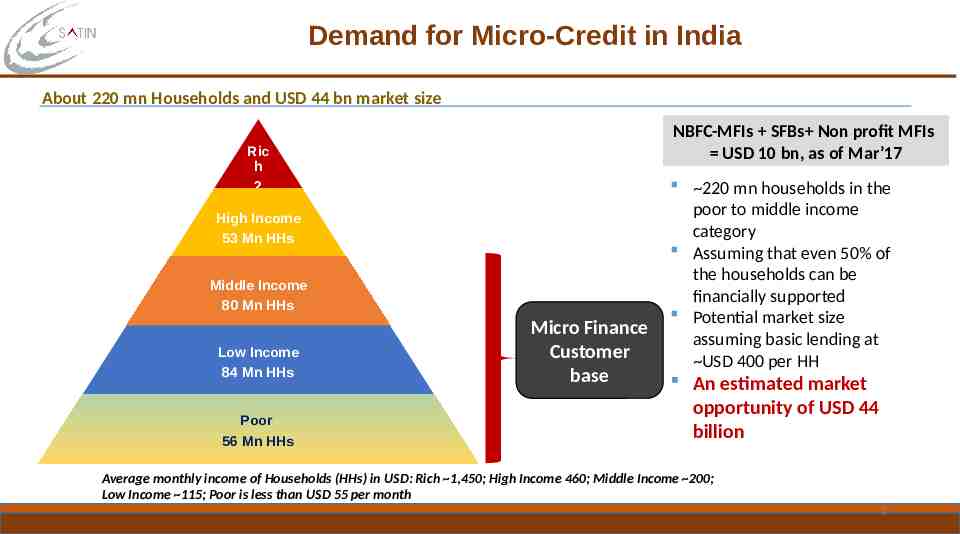

Demand for Micro-Credit in India About 220 mn Households and USD 44 bn market size NBFC-MFIs SFBs Non profit MFIs USD 10 bn, as of Mar’17 Ric h 2 Mn High Income 53 Mn HHs Middle Income 80 Mn HHs Low Income 84 Mn HHs Poor 56 Mn HHs Micro Finance Customer base 220 mn households in the poor to middle income category Assuming that even 50% of the households can be financially supported Potential market size assuming basic lending at USD 400 per HH An estimated market opportunity of USD 44 billion Average monthly income of Households (HHs) in USD: Rich 1,450; High Income 460; Middle Income 200; Low Income 115; Poor is less than USD 55 per month 3

Women-Centric Sustainable Development : Microfinance Women constitute the core fabric of microfinance and are also the critical success factor Women are often among the most vulnerable and poorest members of low-income societies 70% of the world’s poor are women Financially Responsible & More Reliable Improved Sustainability High in Social Collateral Influence children’s nutrition, health, and education Controlled Household Income Microfinance is a powerful instrument of social change, particularly for women Obvious economic and social benefits to involving women in microfinance programs Women are the family nucleus, that is vital for societal improvement and progress Work for Betterment of Entire Family

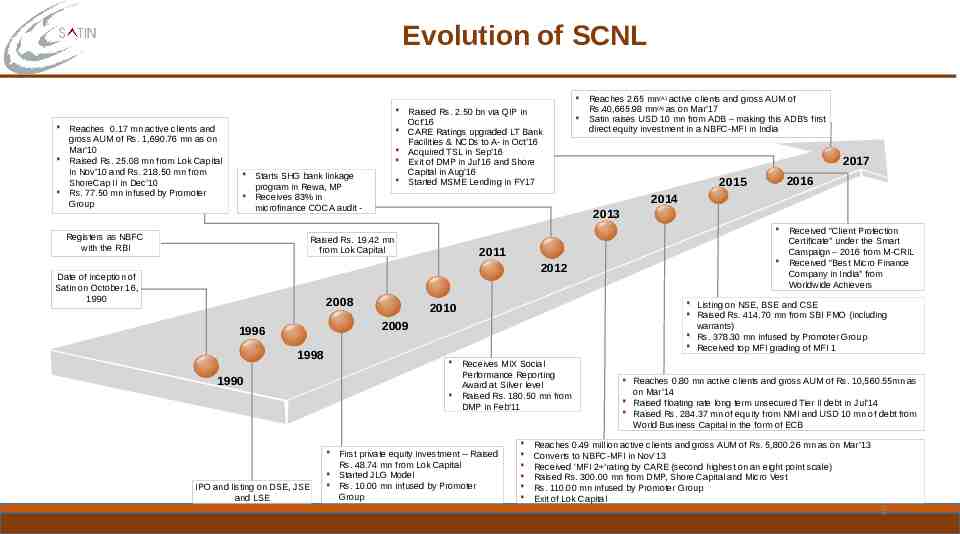

Evolution of SCNL Reaches 0.17 mn active clients and gross AUM of Rs. 1,690.76 mn as on Mar’10 Raised Rs. 25.08 mn from Lok Capital in Nov’10 and Rs. 218.50 mn from ShoreCap II in Dec’10 Rs. 77.50 mn infused by Promoter Group Starts SHG bank linkage program in Rewa, MP Receives 83% in microfinance COCA audit - Raised Rs. 2.50 bn via QIP in Oct’16 CARE Ratings upgraded LT Bank Facilities & NCDs to A- in Oct’16 Acquired TSL in Sep’16 Exit of DMP in Jul'16 and Shore Capital in Aug’16 Started MSME Lending in FY17 Reaches 2.65 mn(A) active clients and gross AUM of Rs.40,665.98 mn(A) as on Mar’17 Satin raises USD 10 mn from ADB – making this ADB’s first direct equity investment in a NBFC-MFI in India 2017 2016 2015 2014 2013 Registers as NBFC with the RBI Raised Rs. 19.42 mn from Lok Capital 2011 2012 Date of inception of Satin on October 16, 1990 2008 Listing on NSE, BSE and CSE Raised Rs. 414.70 mn from SBI FMO (including warrants) Rs. 378.30 mn infused by Promoter Group Received top MFI grading of MFI 1 2010 2009 1996 1998 1990 IPO and listing on DSE, JSE and LSE Received “Client Protection Certificate” under the Smart Campaign – 2016 from M-CRIL Received “Best Micro Finance Company in India” from Worldwide Achievers Receives MIX Social Performance Reporting Award at Silver level Raised Rs. 180.50 mn from DMP in Feb’11 First private equity investment -- Raised Rs. 48.74 mn from Lok Capital Started JLG Model Rs. 10.00 mn infused by Promoter Group Reaches 0.80 mn active clients and gross AUM of Rs. 10,560.55mn as on Mar’14 Raised floating rate long term unsecured Tier II debt in Jul’14 Raised Rs. 284.37 mn of equity from NMI and USD 10 mn of debt from World Business Capital in the form of ECB Reaches 0.49 million active clients and gross AUM of Rs. 5,800.26 mn as on Mar’13 Converts to NBFC-MFI in Nov’13 Received ‘MFI 2 ’rating by CARE (second highest on an eight point scale) Raised Rs. 300.00 mn from DMP, Shore Capital and Micro Vest Rs. 110.00 mn infused by Promoter Group Exit of Lok Capital 5

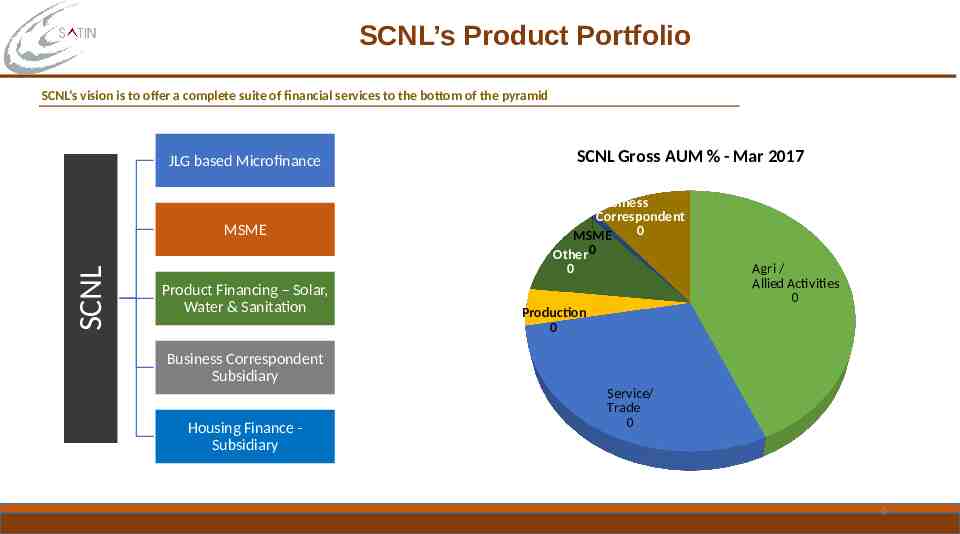

SCNL’s Product Portfolio SCNL’s vision is to offer a complete suite of financial services to the bottom of the pyramid JLG based Microfinance SCNL MSME Product Financing – Solar, Water & Sanitation SCNL Gross AUM % - Mar 2017 Business Correspondent 0 MSME Other 0 0 Agri / Allied Activities 0 Production 0 Business Correspondent Subsidiary Housing Finance Subsidiary Service/ Trade 0 6

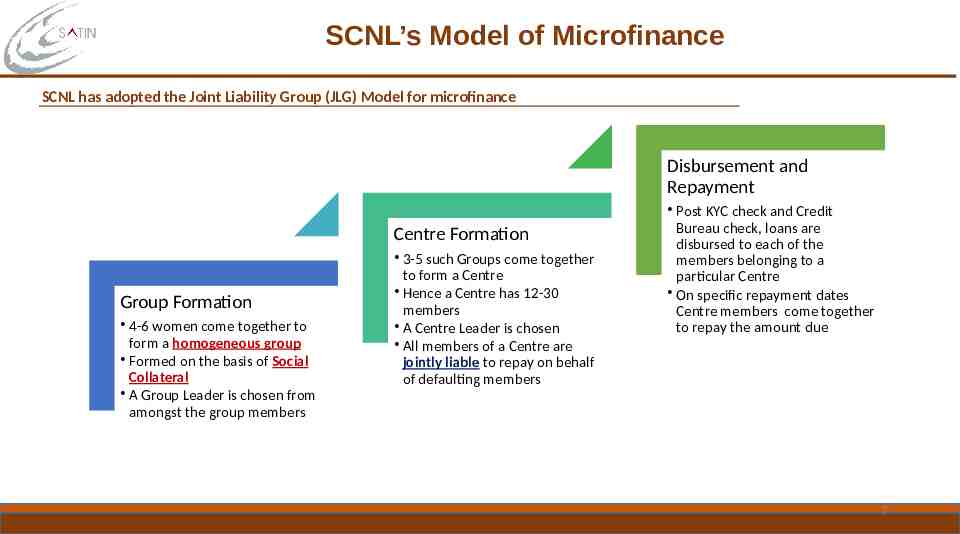

SCNL’s Model of Microfinance SCNL has adopted the Joint Liability Group (JLG) Model for microfinance Disbursement and Repayment Centre Formation Group Formation 4-6 women come together to form a homogeneous group Formed on the basis of Social Collateral A Group Leader is chosen from amongst the group members 3-5 such Groups come together to form a Centre Hence a Centre has 12-30 members A Centre Leader is chosen All members of a Centre are jointly liable to repay on behalf of defaulting members Post KYC check and Credit Bureau check, loans are disbursed to each of the members belonging to a particular Centre On specific repayment dates Centre members come together to repay the amount due 7

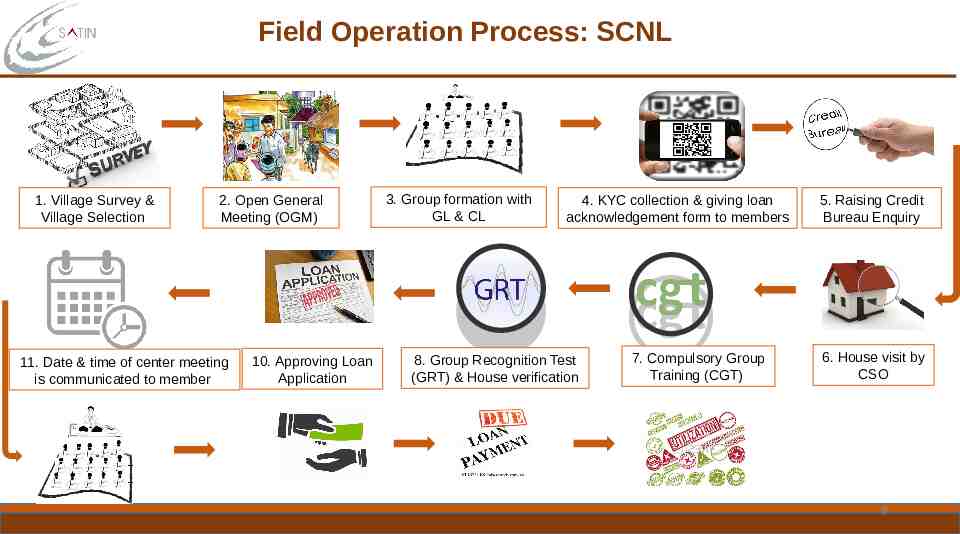

Field Operation Process: SCNL 1. Village Survey & Village Selection 2. Open General Meeting (OGM) 11. Date & time of center meeting is communicated to member 10. Approving Loan Application 3. Group formation with GL & CL 4. KYC collection & giving loan acknowledgement form to members 8. Group Recognition Test (GRT) & House verification 7. Compulsory Group Training (CGT) 5. Raising Credit Bureau Enquiry 6. House visit by CSO 8

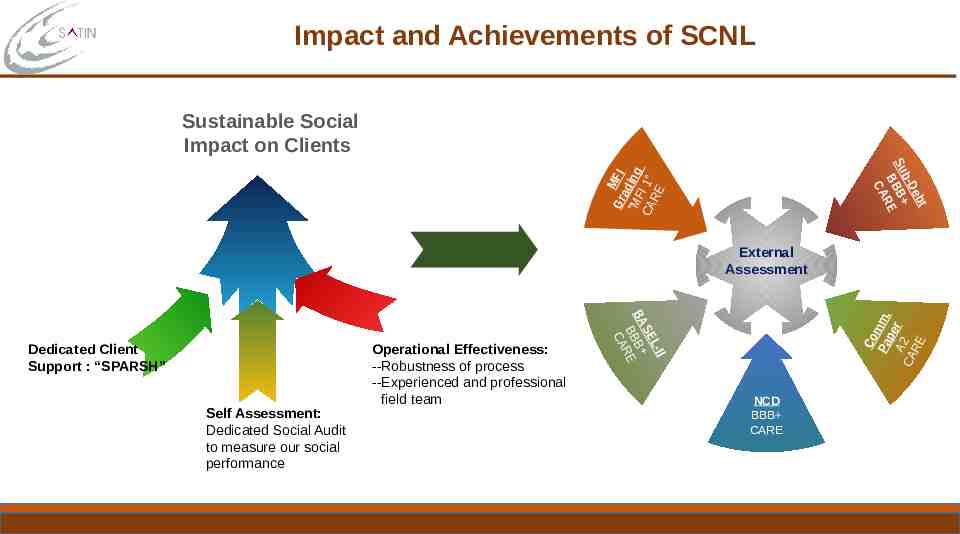

Impact and Achievements of SCNL Sustainable Social Impact on Clients Gr MFI a "M ding F CA I 1" RE t eb b-D S u B BB RE CA External Assessment Self Assessment: Dedicated Social Audit to measure our social performance Co m Pa m. pe A2 r CA RE Operational Effectiveness: --Robustness of process --Experienced and professional field team I L-I SE BA B BB RE CA Dedicated Client Support : “SPARSH” NCD BBB CARE

Awards for SCNL Winner Winner of of “Best “Best NBFC-MFI NBFC-MFI Award” Award” & & Runner-up Runner-up for for “CSR Initiatives & Business Responsibility Award” “CSR Initiatives & Business Responsibility Award” in in NBFC-MFI NBFC-MFI category category –– CIMSME CIMSME Banking Banking and and NBFC NBFC Awards Awards 2016 2016 Received Received certificate certificate for for being being the the ‘Best ‘Best Micro Micro Finance Finance Company Company in in India’ India’ from from Worldwide Worldwide Achievers Achievers at at the the Business Business Leaders’ Leaders’ Summit Summit and and Awards, Awards, 2016 2016 Received Received “Client “Client Protection Protection Certificate” Certificate” under under the the Smart Smart Campaign Campaign –– 2016 2016 from from M-CRIL M-CRIL Received Received “India “India Iconic Iconic Name Name in in Microfinance” Microfinance” AwardAward2015 2015 from from IIBA IIBA First First MFI MFI to to receive receive funding funding from from Mudra Mudra Bank Bank 10

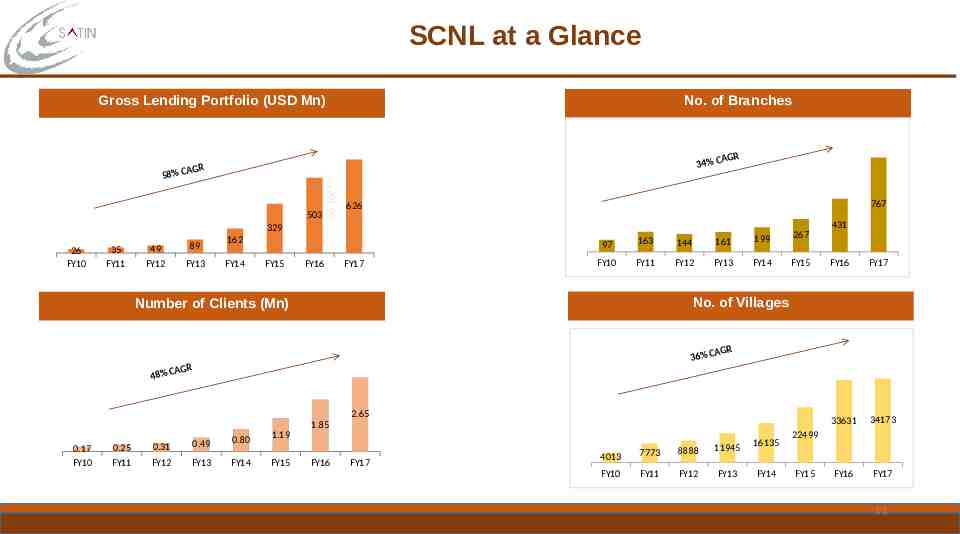

SCNL at a Glance Gross Lending Portfolio (USD Mn) No. of Branches 503 36,168** AGR 34% C AGR 58% C 767 626 431 329 26 FY10 35 FY11 49 89 FY12 FY13 162 FY14 FY15 FY16 FY17 97 163 144 161 199 267 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 33631 34173 FY16 FY17 No. of Villages Number of Clients (Mn) AGR 36% C AGR 48% C 2.65 0.17 FY10 0.25 0.31 0.49 0.80 FY11 FY12 FY13 FY14 1.19 FY15 1.85 FY16 FY17 4013 7773 8888 11945 FY10 FY11 FY12 FY13 16135 FY14 22499 FY15 11

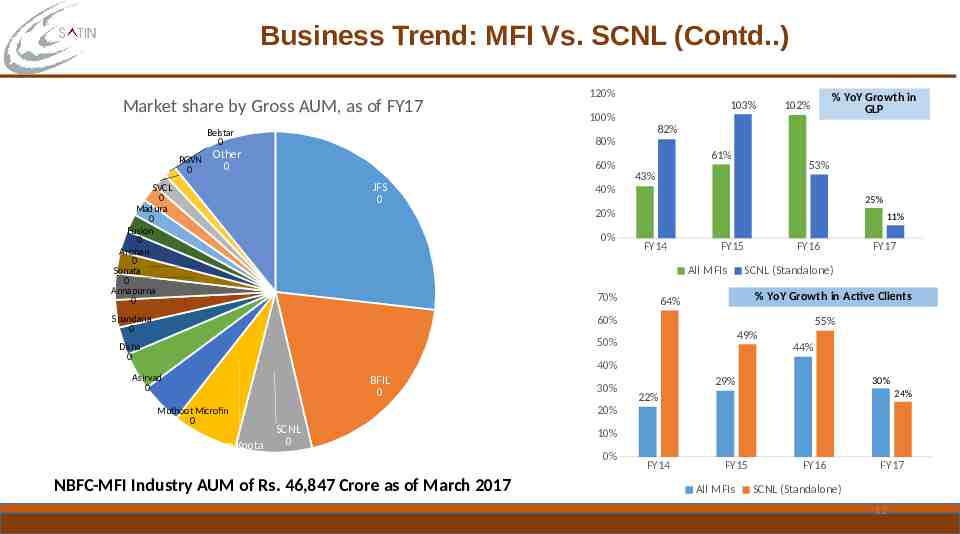

Business Trend: MFI Vs. SCNL (Contd.) Market share by Gross AUM, as of FY17 Belstar 0 RGVN 0 120% 103% 100% 82% 80% Other 0 60% JFS 0 SVCL 0 Madura 0 Fusion 0 Arohan 0 Sonata 0 Annapurna 0 % YoY Growth in GLP 102% 61% 53% 43% 40% 25% 20% 0% 11% FY14 FY15 All MFIs 70% Spandana 0 FY16 SCNL (Standalone) % YoY Growth in Active Clients 64% 60% 55% 49% 50% Disha 0 FY17 44% 40% Asirvad 0 BFIL 0 Muthoot Microfin 0 Grameen Koota 0 30% 30% 29% 24% 22% 20% SCNL 0 NBFC-MFI Industry AUM of Rs. 46,847 Crore as of March 2017 10% 0% FY14 FY15 All MFIs FY16 FY17 SCNL (Standalone) 12

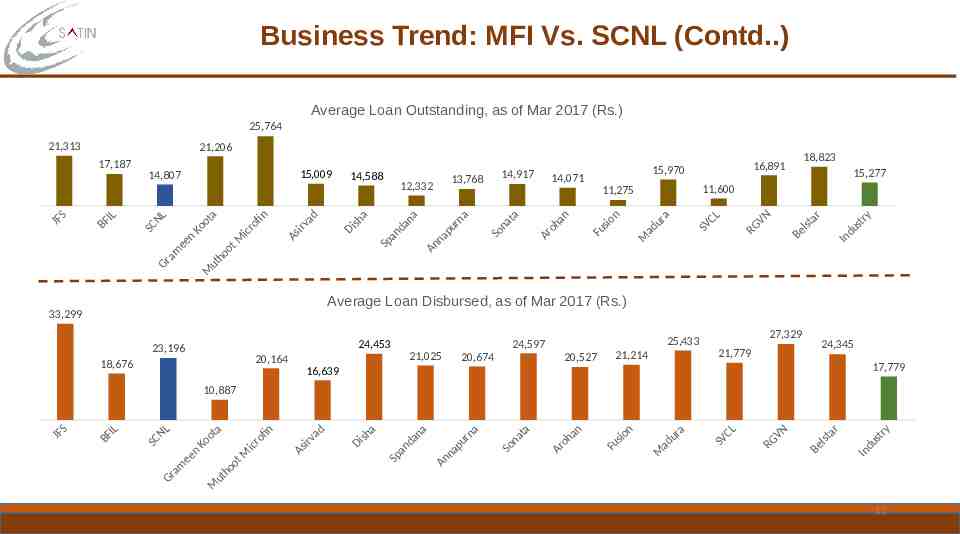

Business Trend: MFI Vs. SCNL (Contd.) Average Loan Outstanding, as of Mar 2017 (Rs.) 25,764 21,313 21,206 17,187 S JF IL BF 15,009 14,807 NL SC Gr am ee n a ot o K M M ot o h ut n ofi r ic 14,588 a sh i D ad is rv A 13,768 12,332 a an d an Sp a rn u p na n A 14,917 14,071 n ha o Ar n sio u F 15,277 11,600 11,275 a at n So 18,823 16,891 15,970 M a ur d a CL SV VN G R r sta l Be y str u d In Average Loan Disbursed, as of Mar 2017 (Rs.) 33,299 24,453 23,196 20,164 18,676 21,025 20,674 27,329 25,433 24,597 20,527 24,345 21,779 21,214 17,779 16,639 10,887 S JF IL BF NL C S a Gr m n ee a ot o K M M ot o h ut n ofi r ic ad v r i As a sh i D na a d an p S a rn u ap n An a at n So an h o Ar n io s Fu M a ur d a C SV L VN RG B r sta l e try s du In 13

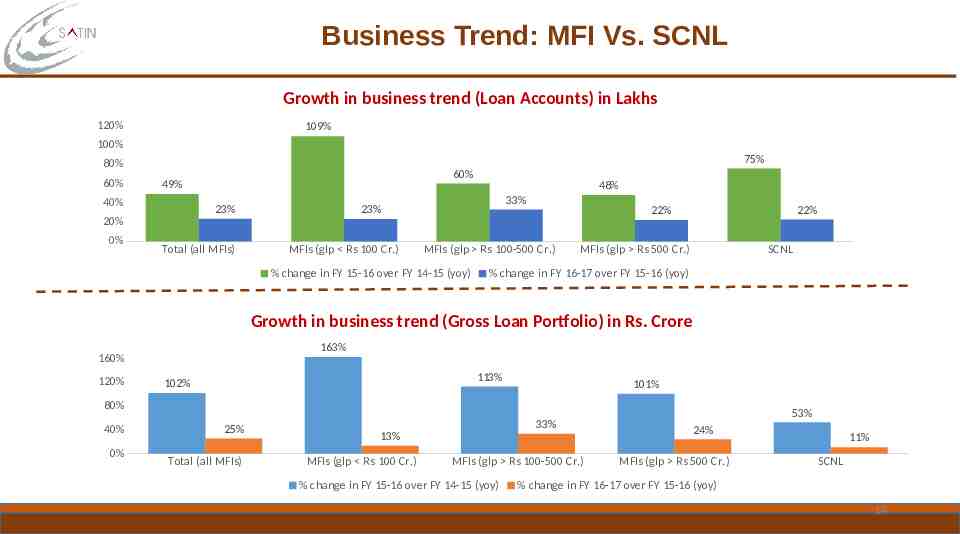

Business Trend: MFI Vs. SCNL Growth in business trend (Loan Accounts) in Lakhs 120% 109% 100% 75% 80% 60% 60% 49% 40% 23% Total (all MFIs) 33% 23% 20% 0% 48% MFIs (glp Rs 100 Cr.) MFIs (glp Rs 100-500 Cr.) % change in FY 15-16 over FY 14-15 (yoy) 22% 22% MFIs (glp Rs 500 Cr.) SCNL % change in FY 16-17 over FY 15-16 (yoy) Growth in business trend (Gross Loan Portfolio) in Rs. Crore 163% 160% 120% 113% 102% 101% 80% 40% 0% 25% Total (all MFIs) 33% 13% MFIs (glp Rs 100 Cr.) MFIs (glp Rs 100-500 Cr.) % change in FY 15-16 over FY 14-15 (yoy) 53% 24% MFIs (glp Rs 500 Cr.) 11% SCNL % change in FY 16-17 over FY 15-16 (yoy) 14

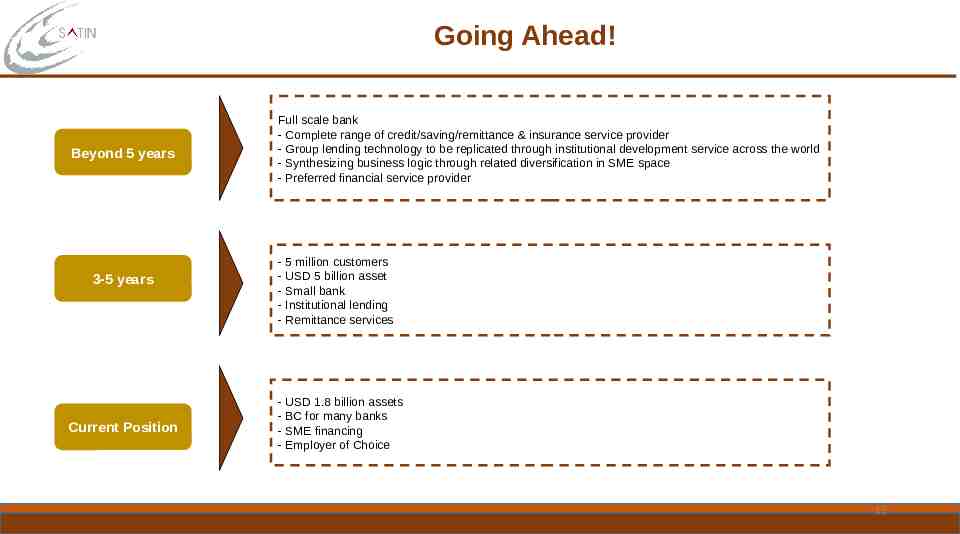

Going Ahead! Beyond 5 years 3-5 years Current Position Full scale bank - Complete range of credit/saving/remittance & insurance service provider - Group lending technology to be replicated through institutional development service across the world - Synthesizing business logic through related diversification in SME space - Preferred financial service provider - 5 million customers - USD 5 billion asset - Small bank - Institutional lending - Remittance services - USD 1.8 billion assets - BC for many banks - SME financing - Employer of Choice 15

Thank You!! 16