VA Home Loans Refinance Program Updates

33 Slides2.15 MB

VA Home Loans Refinance Program Updates

Agenda Overview of VA Refinance Products Review changes to VA Cash-Out Refinances Review changes to VA IRRRLs

VA Refinance Products Overview & Discussion

VA Refinance Products Chapter 6, of the VA Lender Handbook provides guidance for two types of Refinance products: Cash-Out Refinancing Loans Interest Rate Reduction Refinancing Loans (IRRRL)

VA Refinance Products In May 2018, The Economic Growth, Regulatory Relief, and Consumer Protection Act was signed into federal law. This law includes The Protecting Veterans From Predatory Lending Act of 2018, designed to protect Veterans from “loan churning” or “serial refinancing”.

VA Cash-Out Refinances Policy Changes Announced In: VA Circular 26-18-30

Overview VA Circular 26-18-30 Implements requirements of The Economic Growth, Regulatory Relief, and Consumer Protection Act for VA Cash-Out Refinance Loans. The changes are effective to all loan applications taken on or after February 15, 2019.

Overview New Cash-Out Refinance Categories Changes to LTV Calculations Net Tangible Benefit and Disclosure Seasoning Requirements Recoupment Period Requirements

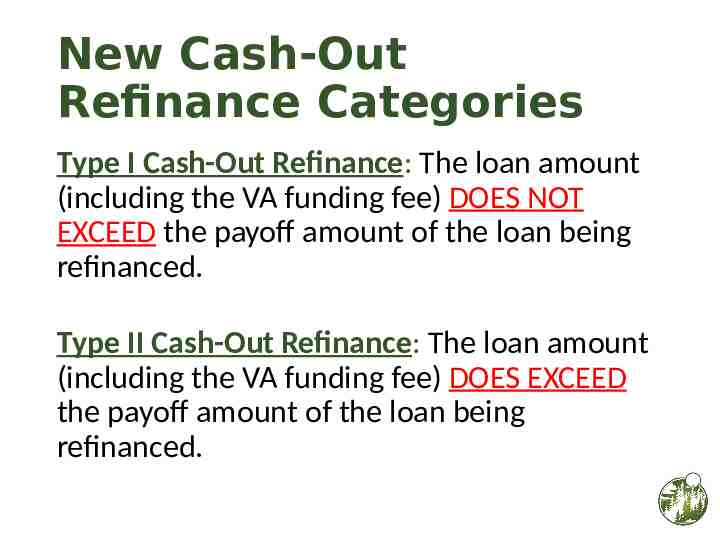

New Cash-Out Refinance Categories Type I Cash-Out Refinance: The loan amount (including the VA funding fee) DOES NOT EXCEED the payoff amount of the loan being refinanced. Type II Cash-Out Refinance: The loan amount (including the VA funding fee) DOES EXCEED the payoff amount of the loan being refinanced.

Loan-To-Value (LTV) Calculations The maximum LTV for Cash-Out Refinances may not exceed 100% INCLUDING the VA Funding Fee. Calculation: Divide the total loan amount (including VA funding fee) by the reasonable value on the NOV.

Net Tangible Benefit (NTB) All Cash-Out loans must pass the Net Tangible Benefit (NTB) Test. In addition, the lender must provide a NTB disclosure at time of initial disclosure and again at time of closing. NOTE: The VA is not creating a new disclosure form. Lenders must create their own disclosure that meets VA Requirements.

Net Tangible Benefit (NTB) The Lender must disclose: The actual Net Tangible Benefit A comparison of the existing loan and the new loan An estimate of the home equity being removed and an explanation of how this may impact the Veteran

Net Tangible Benefit (NTB) The loan must satisfy at least one of the following eight benefits: [1] The new loan eliminates monthly mortgage insurance, whether public or private, or monthly guaranty insurance; [2] The term of the new loan is shorter than the term of the loan being refinanced;

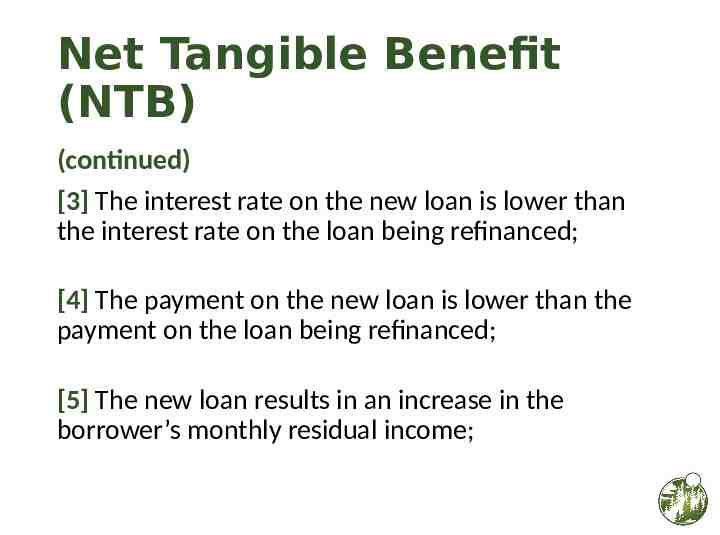

Net Tangible Benefit (NTB) (continued) [3] The interest rate on the new loan is lower than the interest rate on the loan being refinanced; [4] The payment on the new loan is lower than the payment on the loan being refinanced; [5] The new loan results in an increase in the borrower’s monthly residual income;

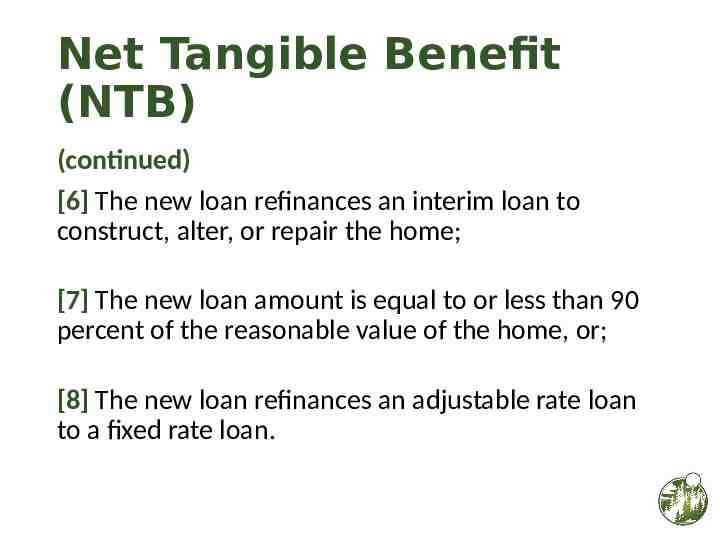

Net Tangible Benefit (NTB) (continued) [6] The new loan refinances an interim loan to construct, alter, or repair the home; [7] The new loan amount is equal to or less than 90 percent of the reasonable value of the home, or; [8] The new loan refinances an adjustable rate loan to a fixed rate loan.

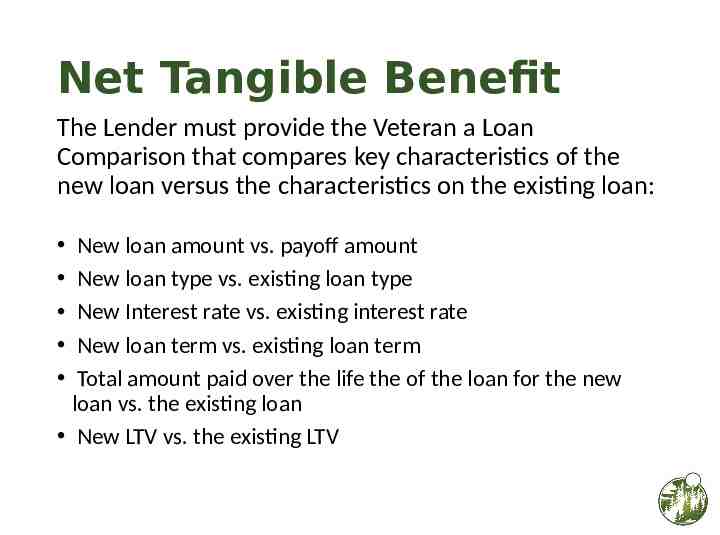

Net Tangible Benefit The Lender must provide the Veteran a Loan Comparison that compares key characteristics of the new loan versus the characteristics on the existing loan: New loan amount vs. payoff amount New loan type vs. existing loan type New Interest rate vs. existing interest rate New loan term vs. existing loan term Total amount paid over the life the of the loan for the new loan vs. the existing loan New LTV vs. the existing LTV

Net Tangible Benefit The Lender must provide the Veteran an estimate of the home equity being removed. The Lender must also include a statement that explains how the removal of this home equity may impact the veteran.

Loan Seasoning When paying off an existing VA Guaranteed Home Loan, the existing loan must be seasoned. A loan is considered seasoned by meeting the later of the following dates: 210 days after the 1st monthly payment is made; After 6 monthly payments have been made.

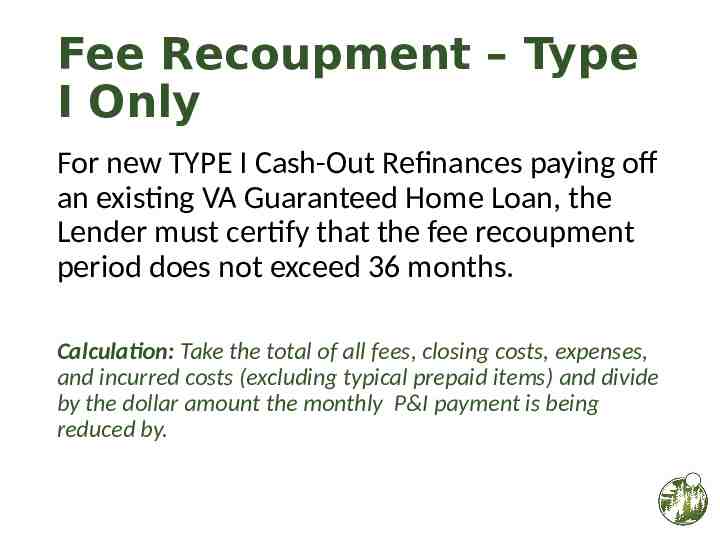

Fee Recoupment – Type I Only For new TYPE I Cash-Out Refinances paying off an existing VA Guaranteed Home Loan, the Lender must certify that the fee recoupment period does not exceed 36 months. Calculation: Take the total of all fees, closing costs, expenses, and incurred costs (excluding typical prepaid items) and divide by the dollar amount the monthly P&I payment is being reduced by.

VA IRRRL Refinances Policy Changes Announced In: VA Circular 26-18-13 VA Circular 26-18-1

Overview VA Circular 26-18-13 Implements requirements of The Economic Growth, Regulatory Relief, and Consumer Protection Act for VA IRRRL Refinances. The changes went into effect for all loan applications taken on or after May 25, 2018.

Overview Net Tangible Benefit Discount Points & LTV Restrictions Appraisal Requirements Seasoning Requirements Fee Recoupment Loan Comparison Disclosure

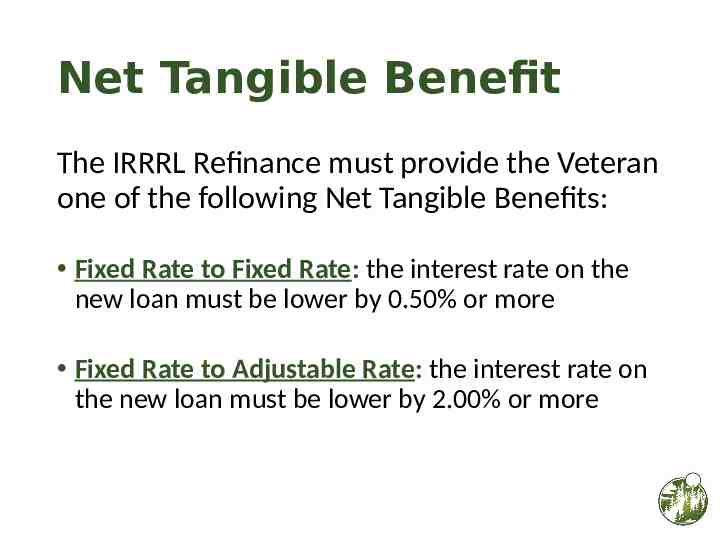

Net Tangible Benefit The IRRRL Refinance must provide the Veteran one of the following Net Tangible Benefits: Fixed Rate to Fixed Rate: the interest rate on the new loan must be lower by 0.50% or more Fixed Rate to Adjustable Rate: the interest rate on the new loan must be lower by 2.00% or more

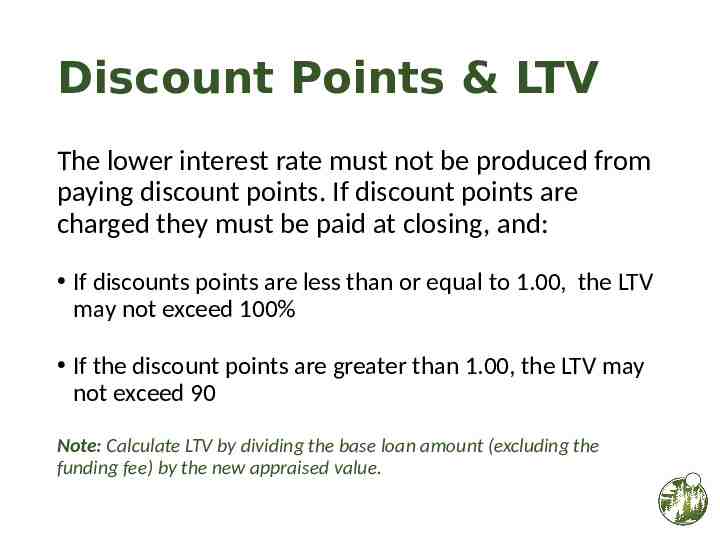

Discount Points & LTV The lower interest rate must not be produced from paying discount points. If discount points are charged they must be paid at closing, and: If discounts points are less than or equal to 1.00, the LTV may not exceed 100% If the discount points are greater than 1.00, the LTV may not exceed 90 Note: Calculate LTV by dividing the base loan amount (excluding the funding fee) by the new appraised value.

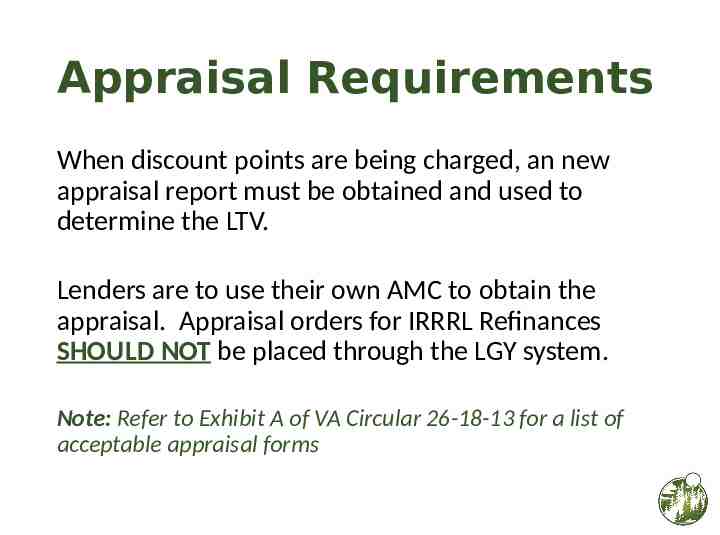

Appraisal Requirements When discount points are being charged, an new appraisal report must be obtained and used to determine the LTV. Lenders are to use their own AMC to obtain the appraisal. Appraisal orders for IRRRL Refinances SHOULD NOT be placed through the LGY system. Note: Refer to Exhibit A of VA Circular 26-18-13 for a list of acceptable appraisal forms

Loan Seasoning The existing VA Guaranteed Home Loan being refinanced must be seasoned. A loan is considered seasoned by meeting the later of the following dates: 210 days after the 1st monthly payment is made; After 6 monthly payments have been made.

Fee Recoupment The Lender must certify that the fee recoupment period does not exceed 36 months. Calculation: Take the total of all fees, closing costs, expenses, and incurred costs (excluding typical prepaid items) and divide by the dollar amount the monthly P&I payment is being reduced by.

Loan Comparison Disclosure The VA has clarified that Lender’s must now provide the Veteran a Refinance Loan Comparison and Lender Certification disclosure at time of initial disclosure and again at time of closing. Note: Refer to Exhibit A of VA Circular 26-18-1, Change 1 for VA FAQs regarding the specifics of the disclosure and timing requirements.

Closing Comments Additional Resources

Additional Reference VA Circular 26-17-12: Instructions for completing the IRRRL Worksheet {VA Form 268923} VA Circular 26-17-11: Instructions regarding how to document fees on the Loan Estimate and Closing Disclosure

Additional References VA Home Loans General https://www.benefits.va.gov/homeloans/index.asp VA Lenders Page https://www.benefits.va.gov/homeloans/lenders.asp