WAM-CAT Fall 2021 F66 Overview and Case Study Mary Ann

57 Slides5.49 MB

WAM-CAT Fall 2021 F66 Overview and Case Study Mary Ann Schwalbendorf Local Government Consultant

It’s everyone’s favorite time of the year again Census Season!!

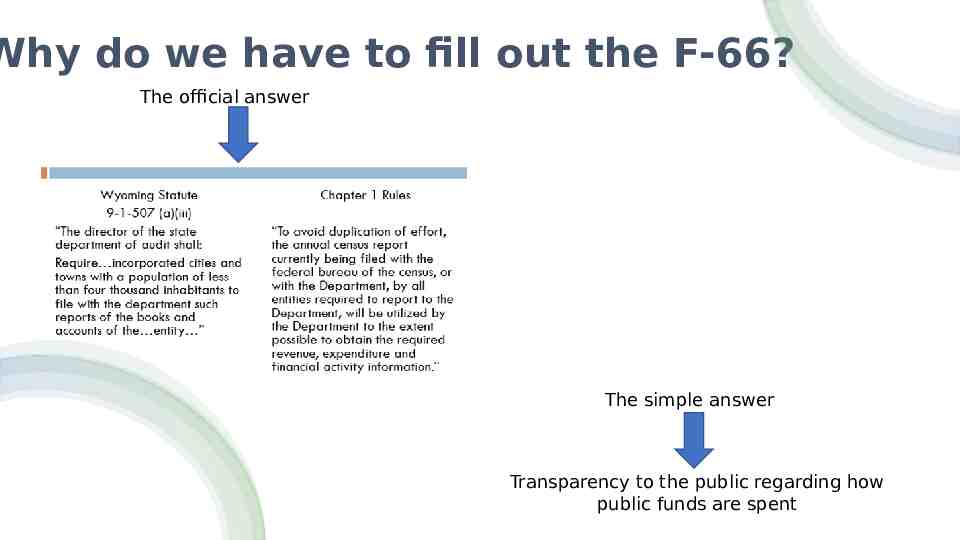

Why do we have to fill out the F-66? The official answer The simple answer Transparency to the public regarding how public funds are spent

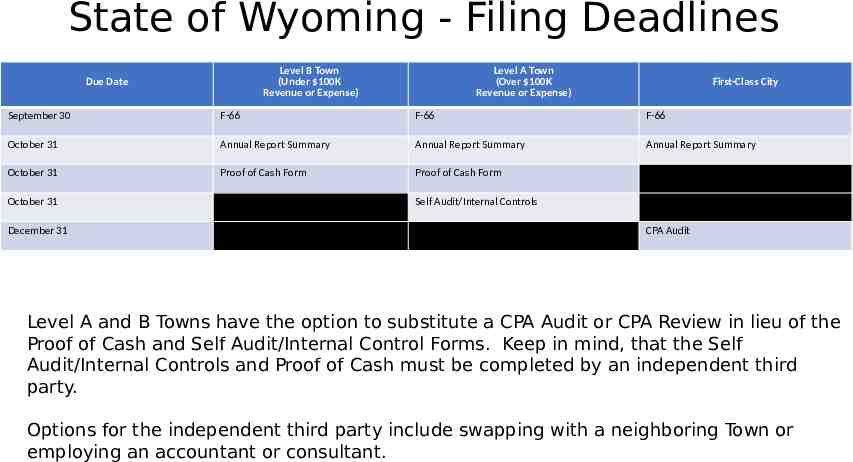

State of Wyoming - Filing Deadlines Level B Town (Under 100K Revenue or Expense) Due Date Level A Town (Over 100K Revenue or Expense) First-Class City September 30 F-66 F-66 F-66 October 31 Annual Report Summary Annual Report Summary Annual Report Summary October 31 Proof of Cash Form Proof of Cash Form October 31 December 31 Self Audit/Internal Controls CPA Audit Level A and B Towns have the option to substitute a CPA Audit or CPA Review in lieu of the Proof of Cash and Self Audit/Internal Control Forms. Keep in mind, that the Self Audit/Internal Controls and Proof of Cash must be completed by an independent third party. Options for the independent third party include swapping with a neighboring Town or employing an accountant or consultant.

Federal Single Audit Single Audit, previously known as the OMB Circular A-133 audit, is a financial statement and federal award audit of a non-federal entity that expends 750,000 or more in federal funds in on year. For entities whose year end is June, the Single Audit is due by March 31. It is intended to ensure adequate internal control and compliance with program requirements. CARES Act Funding requirements have constantly been changing. If you feel that your entity has received enough funds to warrant an audit, please contact a CPA for further clarification and guidance.

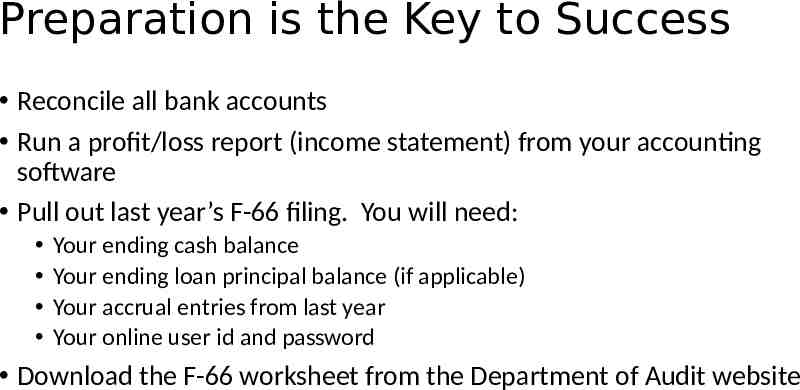

Preparation is the Key to Success Reconcile all bank accounts Run a profit/loss report (income statement) from your accounting software Pull out last year’s F-66 filing. You will need: Your ending cash balance Your ending loan principal balance (if applicable) Your accrual entries from last year Your online user id and password Download the F-66 worksheet from the Department of Audit website

Let’s get this party started!!!!

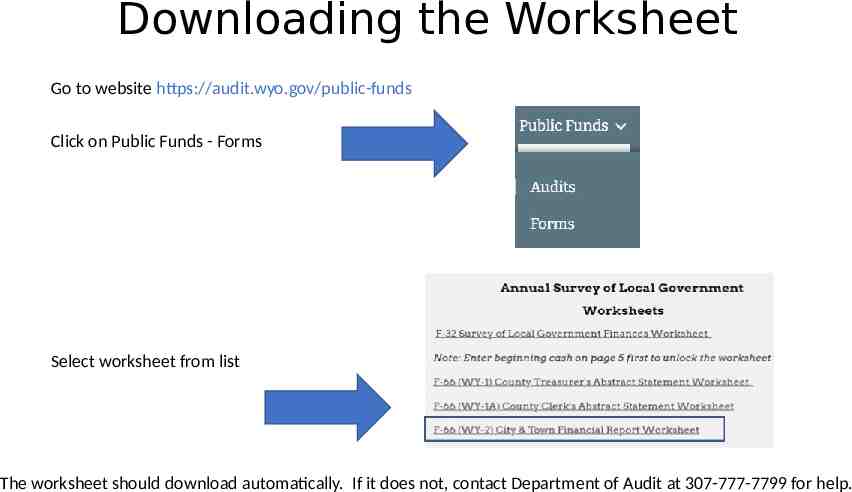

Downloading the Worksheet Go to website https://audit.wyo.gov/public-funds Click on Public Funds - Forms Select worksheet from list The worksheet should download automatically. If it does not, contact Department of Audit at 307-777-7799 for help.

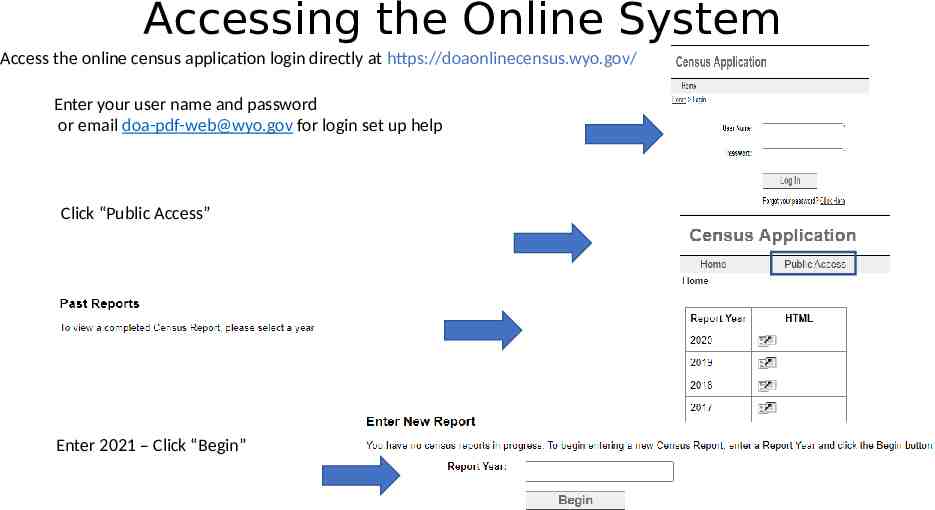

Accessing the Online System Access the online census application login directly at https://doaonlinecensus.wyo.gov/ Enter your user name and password or email [email protected] for login set up help Click “Public Access” Enter 2021 – Click “Begin”

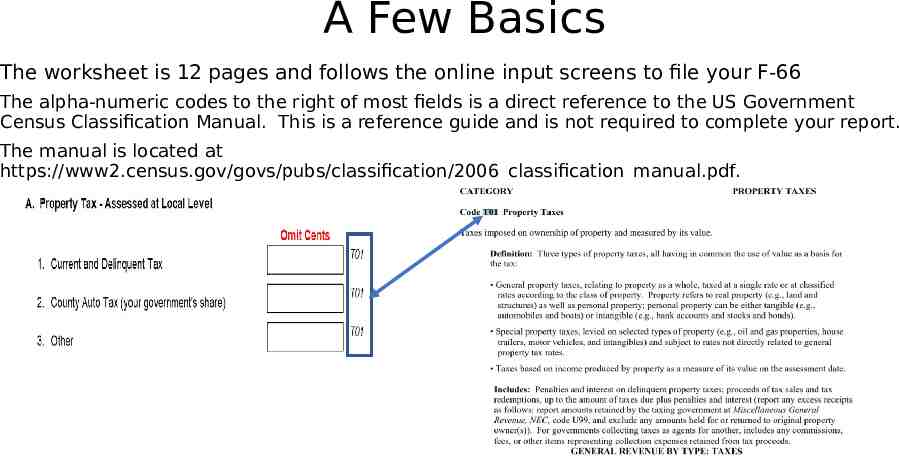

A Few Basics The worksheet is 12 pages and follows the online input screens to file your F-66 The alpha-numeric codes to the right of most fields is a direct reference to the US Government Census Classification Manual. This is a reference guide and is not required to complete your report. The manual is located at https://www2.census.gov/govs/pubs/classification/2006 classification manual.pdf.

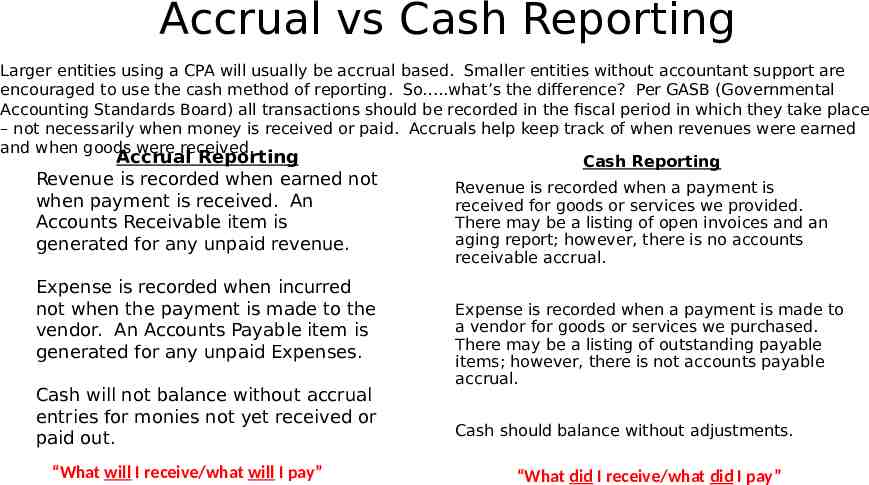

Accrual vs Cash Reporting Larger entities using a CPA will usually be accrual based. Smaller entities without accountant support are encouraged to use the cash method of reporting. So .what’s the difference? Per GASB (Governmental Accounting Standards Board) all transactions should be recorded in the fiscal period in which they take place – not necessarily when money is received or paid. Accruals help keep track of when revenues were earned and when goods were received. Accrual Reporting Cash Reporting Revenue is recorded when earned not when payment is received. An Accounts Receivable item is generated for any unpaid revenue. Expense is recorded when incurred not when the payment is made to the vendor. An Accounts Payable item is generated for any unpaid Expenses. Cash will not balance without accrual entries for monies not yet received or paid out. “What will I receive/what will I pay” Revenue is recorded when a payment is received for goods or services we provided. There may be a listing of open invoices and an aging report; however, there is no accounts receivable accrual. Expense is recorded when a payment is made to a vendor for goods or services we purchased. There may be a listing of outstanding payable items; however, there is not accounts payable accrual. Cash should balance without adjustments. “What did I receive/what did I pay”

One last thought on accruals . When using the accrual method, we record items in our accounting software when the transaction occurs not necessarily when monies are exchanged. The accrual is a representation of the incomplete money side of the transaction. We want to ensure that everything that occurs during the year is recorded in the correct year even though the money due or payable is not fully received.

Items we will report on the F-66 include Revenue Federal State Local Expenses Capital Maintenance Debt Long Term Short Term Cash General Funds Reserve Funds

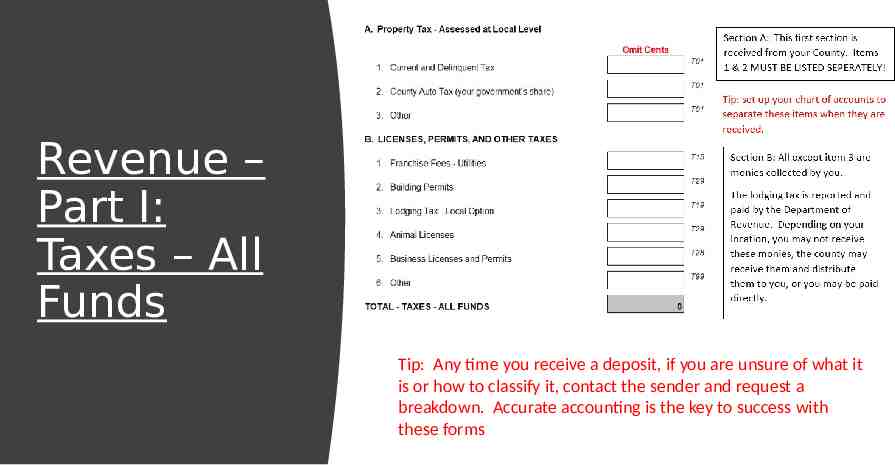

Revenue – Part I: Taxes – All Funds Tip: Any time you receive a deposit, if you are unsure of what it is or how to classify it, contact the sender and request a breakdown. Accurate accounting is the key to success with these forms

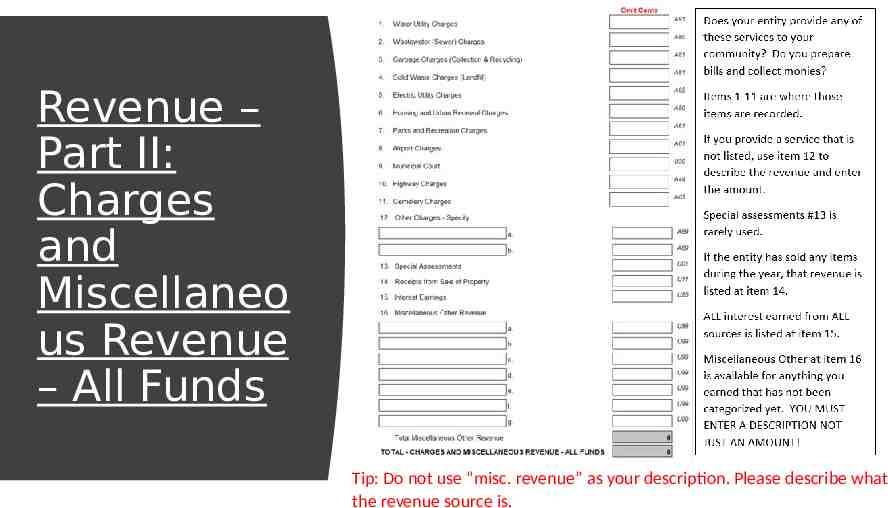

Revenue – Part II: Charges and Miscellaneo us Revenue – All Funds Tip: Do not use “misc. revenue” as your description. Please describe what the revenue source is.

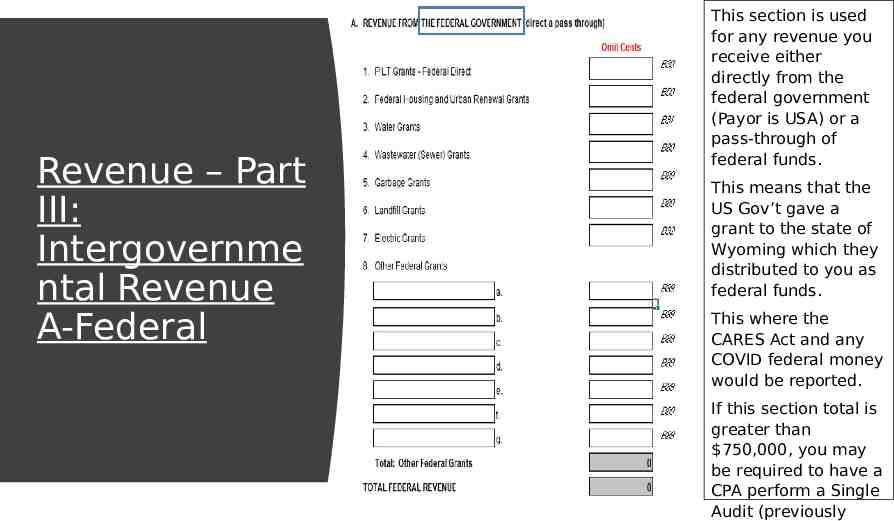

Revenue – Part III: Intergovernme ntal Revenue A-Federal This section is used for any revenue you receive either directly from the federal government (Payor is USA) or a pass-through of federal funds. This means that the US Gov’t gave a grant to the state of Wyoming which they distributed to you as federal funds. This where the CARES Act and any COVID federal money would be reported. If this section total is greater than 750,000, you may be required to have a CPA perform a Single Audit (previously

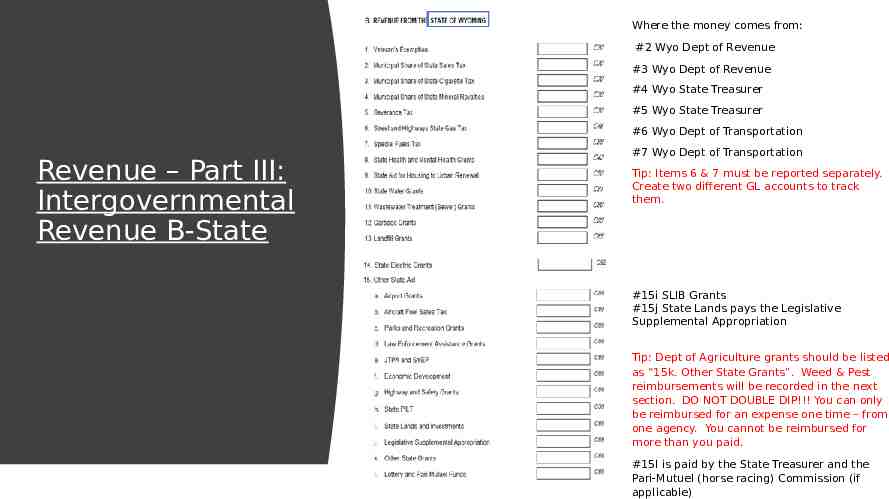

Where the money comes from: #2 Wyo Dept of Revenue #3 Wyo Dept of Revenue #4 Wyo State Treasurer #5 Wyo State Treasurer #6 Wyo Dept of Transportation Revenue – Part III: Intergovernmental Revenue B-State #7 Wyo Dept of Transportation Tip: Items 6 & 7 must be reported separately. Create two different GL accounts to track them. #15i SLIB Grants #15j State Lands pays the Legislative Supplemental Appropriation Tip: Dept of Agriculture grants should be listed as “15k. Other State Grants”. Weed & Pest reimbursements will be recorded in the next section. DO NOT DOUBLE DIP!!! You can only be reimbursed for an expense one time – from one agency. You cannot be reimbursed for more than you paid. #15l is paid by the State Treasurer and the Pari-Mutuel (horse racing) Commission (if applicable)

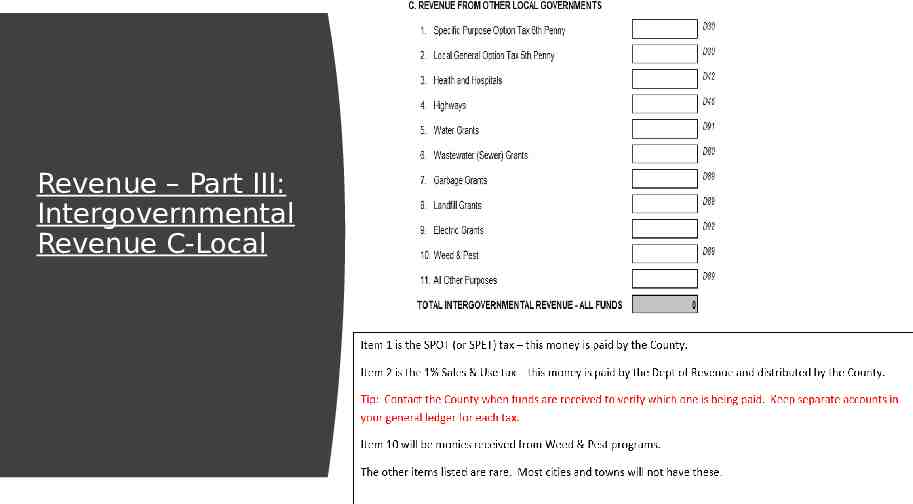

Revenue – Part III: Intergovernmental Revenue C-Local

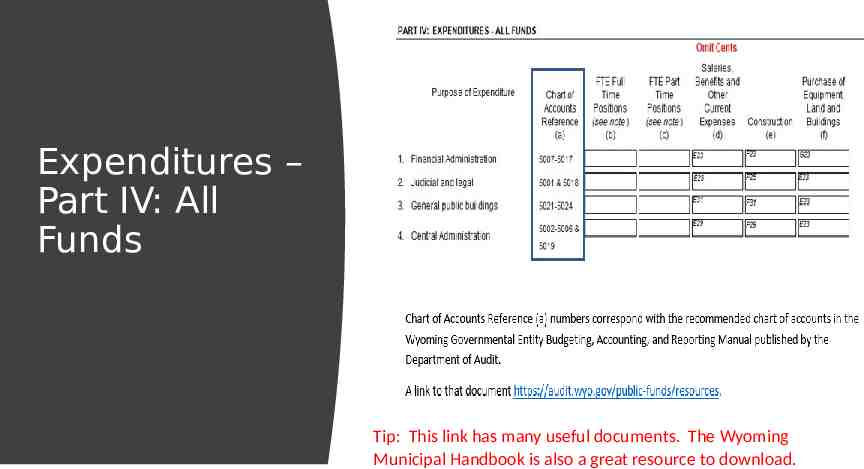

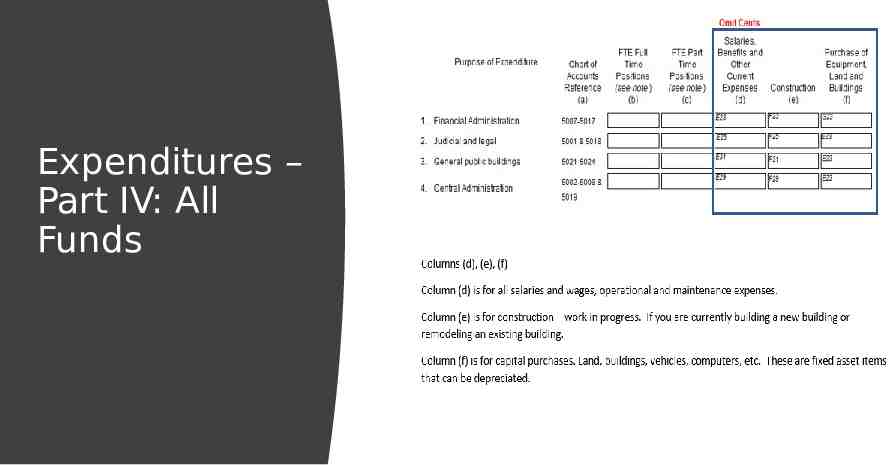

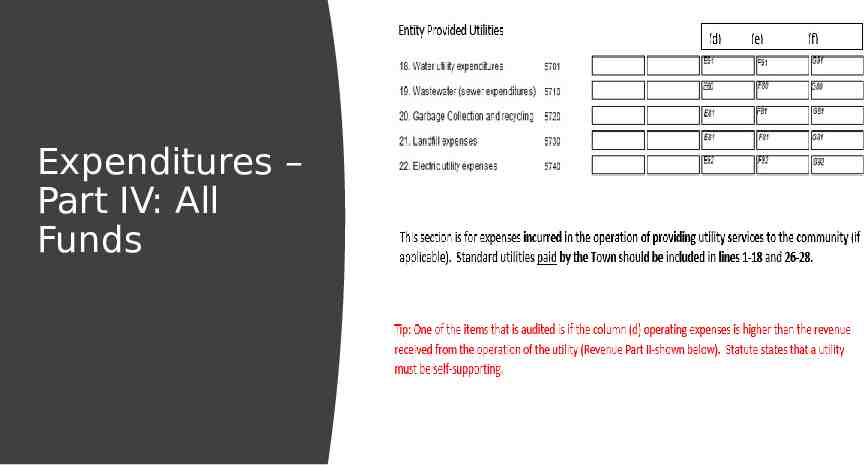

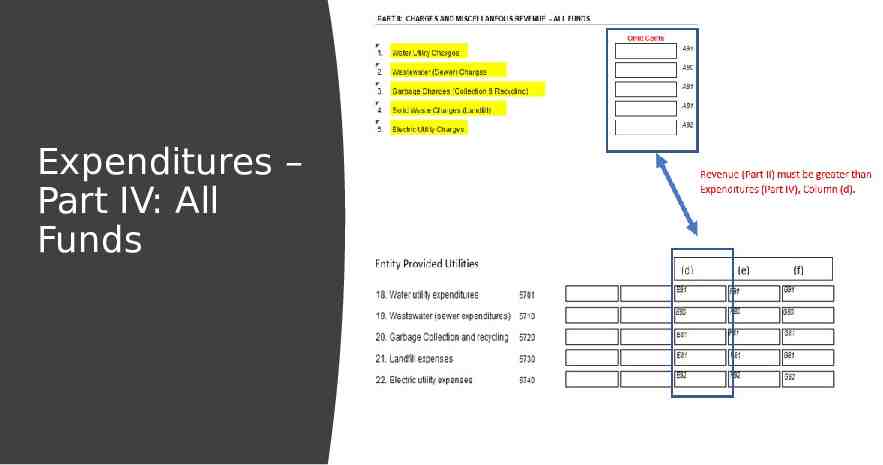

Expenditures – Part IV: All Funds Tip: This link has many useful documents. The Wyoming Municipal Handbook is also a great resource to download.

Expenditures – Part IV: All Funds

Expenditures – Part IV: All Funds

Expenditures – Part IV: All Funds

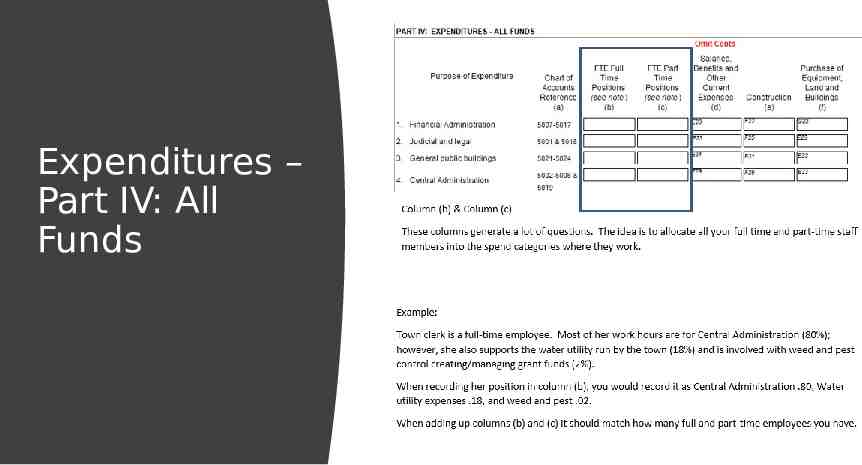

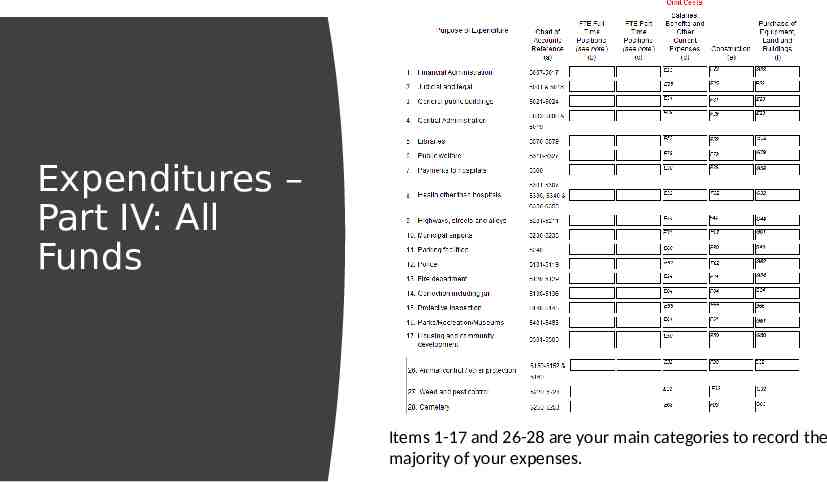

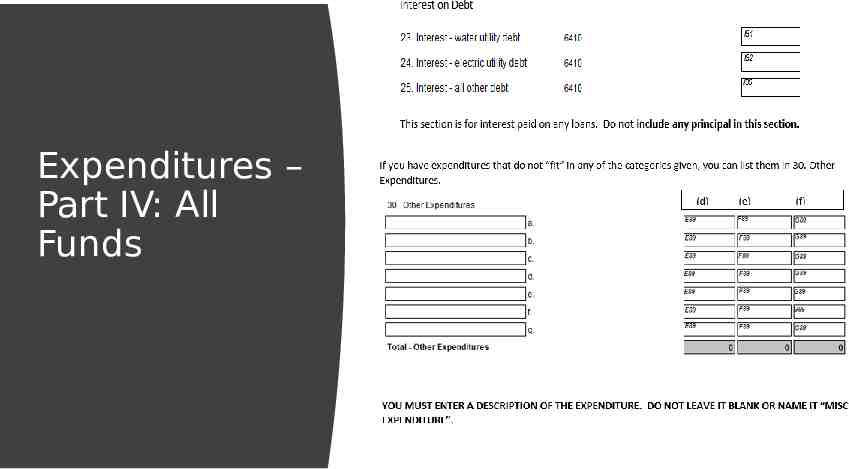

Expenditures – Part IV: All Funds Items 1-17 and 26-28 are your main categories to record the majority of your expenses.

Expenditures – Part IV: All Funds

Expenditures – Part IV: All Funds

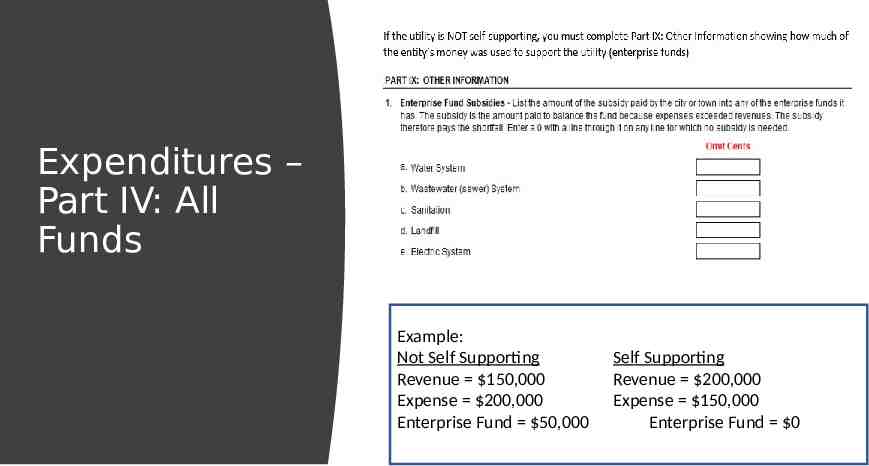

Expenditures – Part IV: All Funds Example: Not Self Supporting Revenue 150,000 Expense 200,000 Enterprise Fund 50,000 Self Supporting Revenue 200,000 Expense 150,000 Enterprise Fund 0

Expenditures – Part IV: All Funds

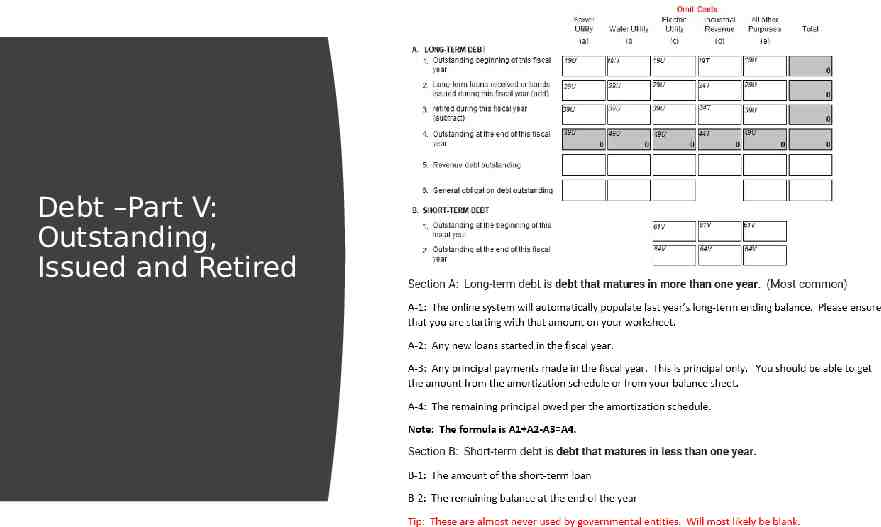

Debt –Part V: Outstanding, Issued and Retired

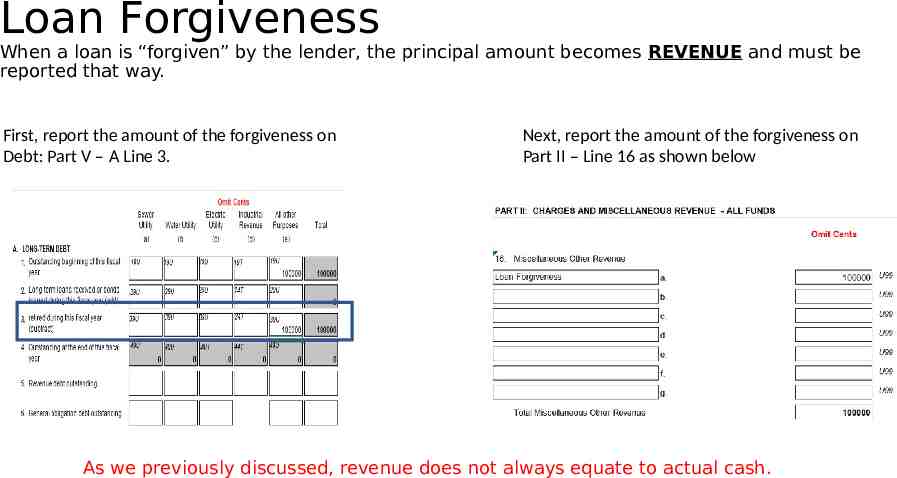

LOAN FORGIVENESS Debt –Part V: Outstanding, Issued and Retired When a loan is “forgiven” by the lender, the principal amount becomes REVENUE and must be reported that way. As we previously discussed, revenue does not always equate to actual cash. LOAN ADJUSTMENTS If a loan ending or beginning balance is incorrect and requires an adjustment, there is a process to correct the balance. We will address these reporting processes later in the training.

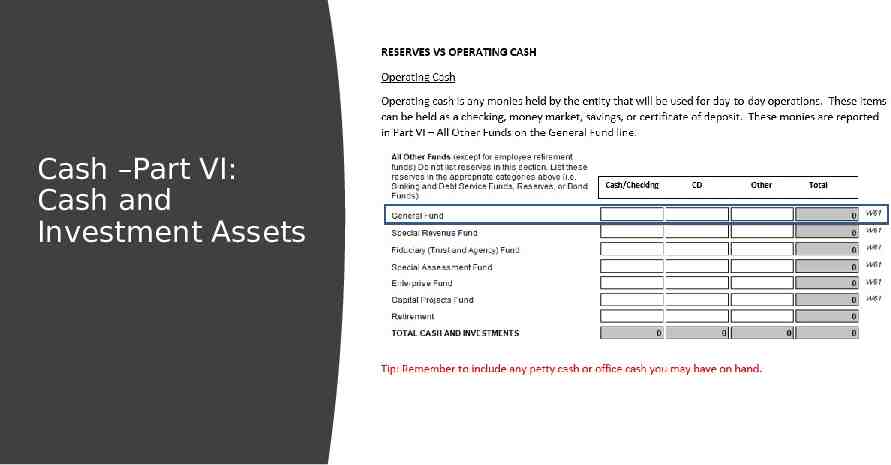

Cash –Part VI: Cash and Investment Assets

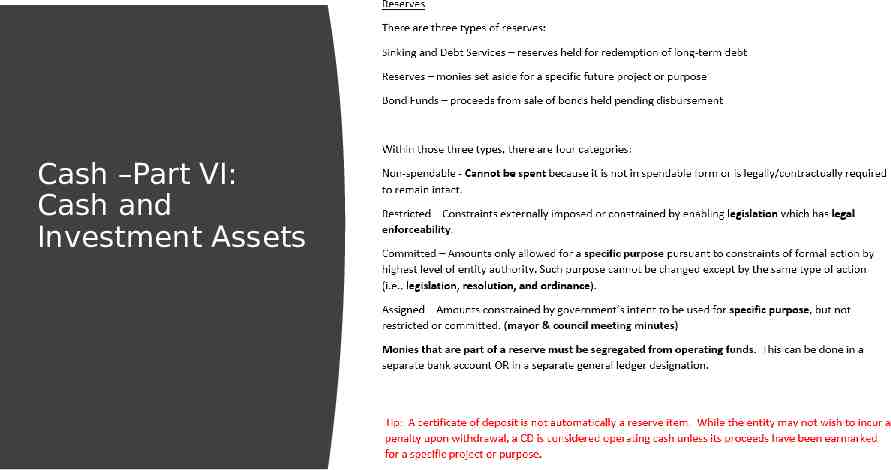

Cash –Part VI: Cash and Investment Assets

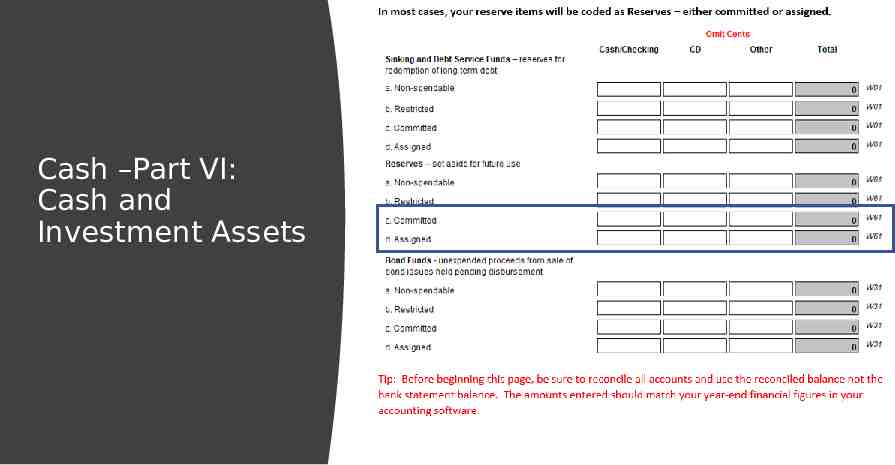

Cash –Part VI: Cash and Investment Assets

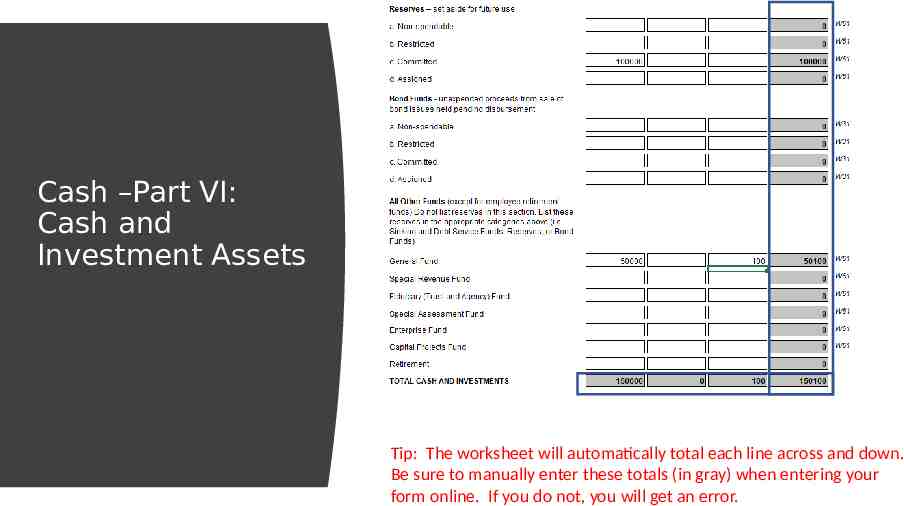

Cash –Part VI: Cash and Investment Assets Tip: The worksheet will automatically total each line across and down. Be sure to manually enter these totals (in gray) when entering your form online. If you do not, you will get an error.

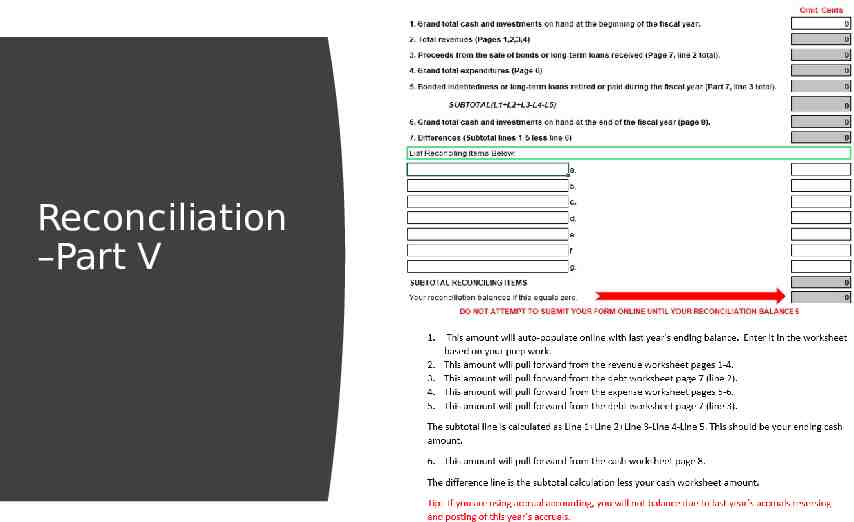

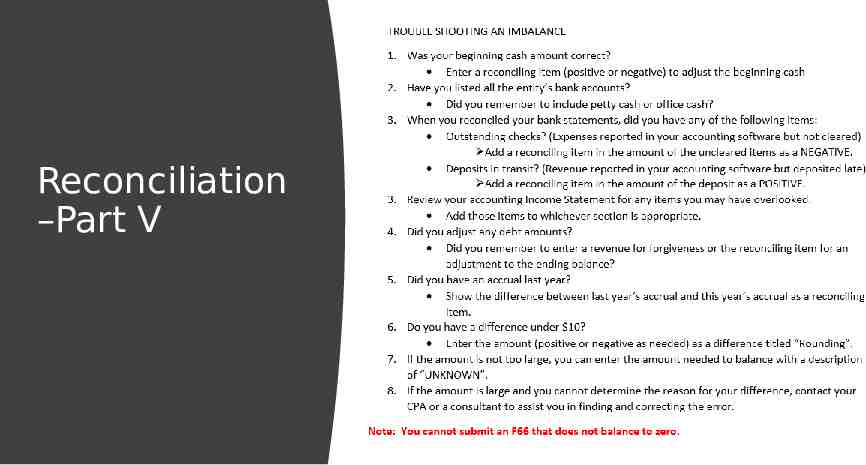

Reconciliation –Part V

Reconciliation –Part V

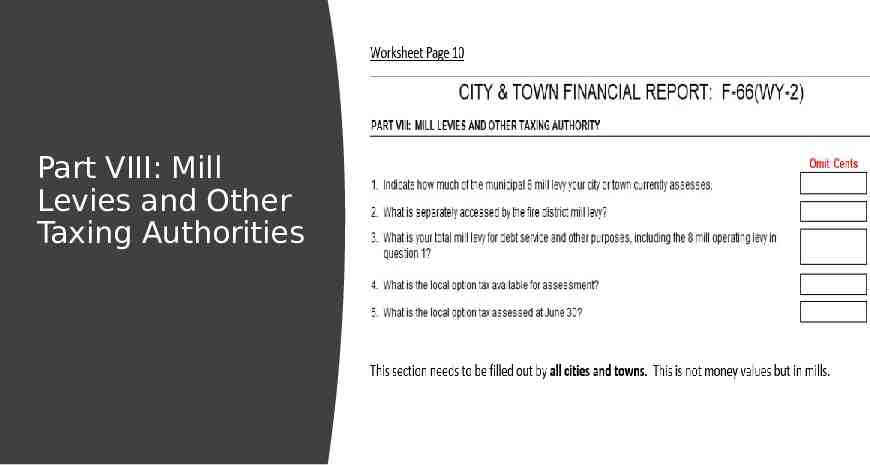

Part VIII: Mill Levies and Other Taxing Authorities

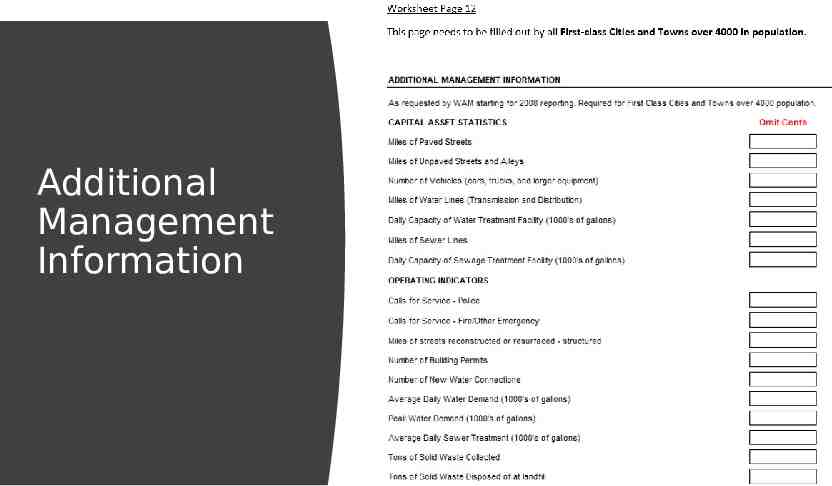

Additional Management Information

Special Procedures

Loan Forgiveness When a loan is “forgiven” by the lender, the principal amount becomes REVENUE and must be reported that way. First, report the amount of the forgiveness on Debt: Part V – A Line 3. Next, report the amount of the forgiveness on Part II – Line 16 as shown below As we previously discussed, revenue does not always equate to actual cash.

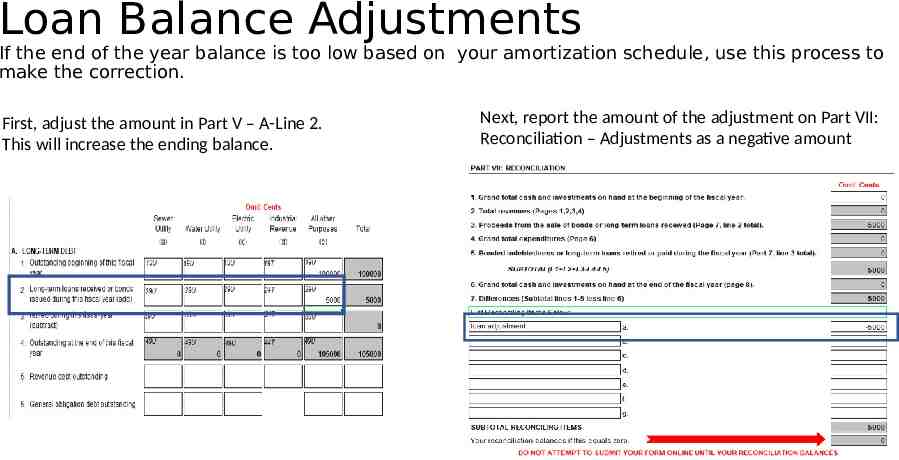

Loan Balance Adjustments If the end of the year balance is too low based on your amortization schedule, use this process to make the correction. First, adjust the amount in Part V – A-Line 2. This will increase the ending balance. Next, report the amount of the adjustment on Part VII: Reconciliation – Adjustments as a negative amount

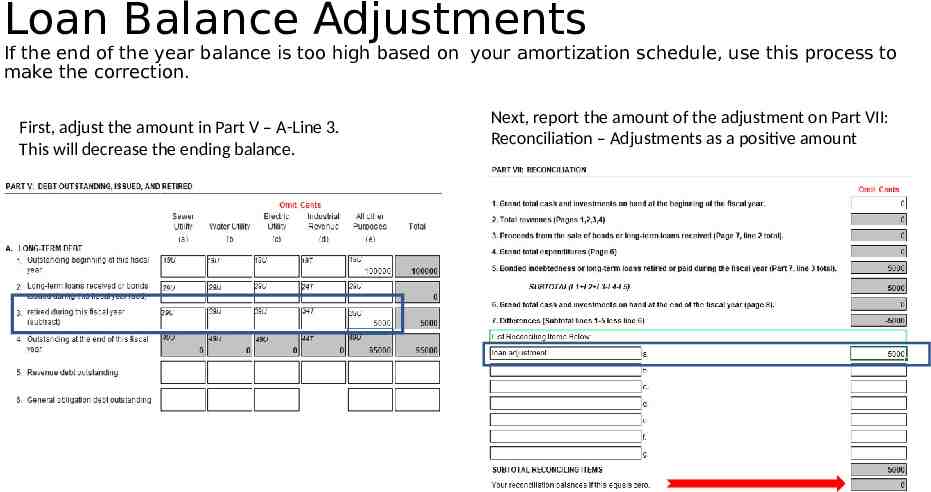

Loan Balance Adjustments If the end of the year balance is too high based on your amortization schedule, use this process to make the correction. First, adjust the amount in Part V – A-Line 3. This will decrease the ending balance. Next, report the amount of the adjustment on Part VII: Reconciliation – Adjustments as a positive amount

Practice Scenarios

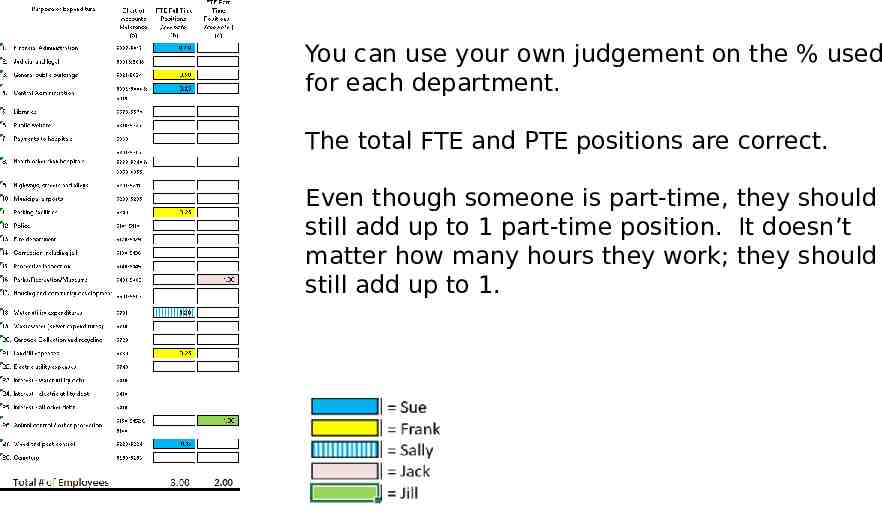

Practice Scenario #1 The Town has 3 full-time and 2 part-time employees. Based on the data below, record their FTE & PTE positions. Full-Time Employees Sue, the Town clerk mostly works on day-to-day town items, but does occasionally help with water billings and prepares and manages the weed & pest grant process. Frank, the Town maintenance man works janitorial on all buildings, collects parking fees, and assists at the landfill. Sally works as the water dept clerk only. Part-Time Employees Jack works for animal control Jill works for parks & recreation

You can use your own judgement on the % used for each department. The total FTE and PTE positions are correct. Even though someone is part-time, they should still add up to 1 part-time position. It doesn’t matter how many hours they work; they should still add up to 1.

Practice Scenario #2 Per the Profit/Loss Schedule, the following expenses were incurred this year: Town Hall Utilities - 5,000 Town Clerk/Treasurer salary - 30,000 Fire Department wages - 10,000 Purchase New Police Cruiser - 40,000 Parks & Recreation Reimbursable Expense - 2,000 Water Utility Loan Payment - 4,500 principal & 500 interest Unfinished work to build new crematorium - 15,000 Based on this data, fill out the expenses portion of the F66.

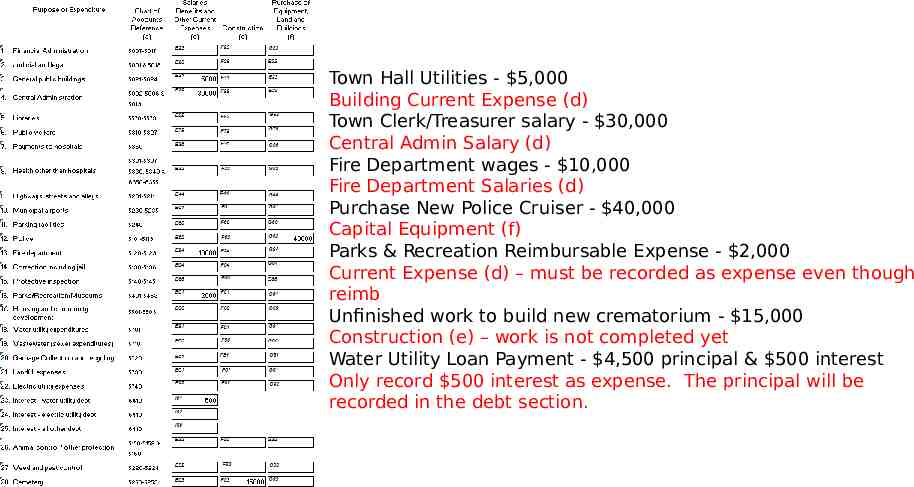

Town Hall Utilities - 5,000 Building Current Expense (d) Town Clerk/Treasurer salary - 30,000 Central Admin Salary (d) Fire Department wages - 10,000 Fire Department Salaries (d) Purchase New Police Cruiser - 40,000 Capital Equipment (f) Parks & Recreation Reimbursable Expense - 2,000 Current Expense (d) – must be recorded as expense even though reimb Unfinished work to build new crematorium - 15,000 Construction (e) – work is not completed yet Water Utility Loan Payment - 4,500 principal & 500 interest Only record 500 interest as expense. The principal will be recorded in the debt section.

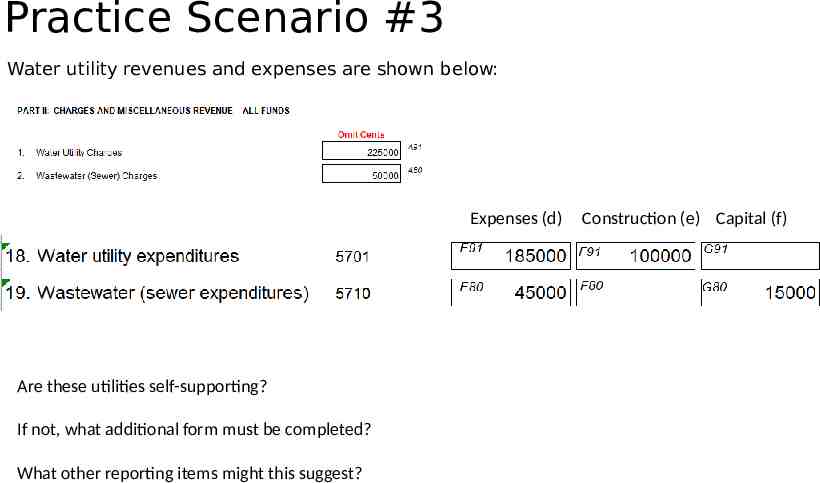

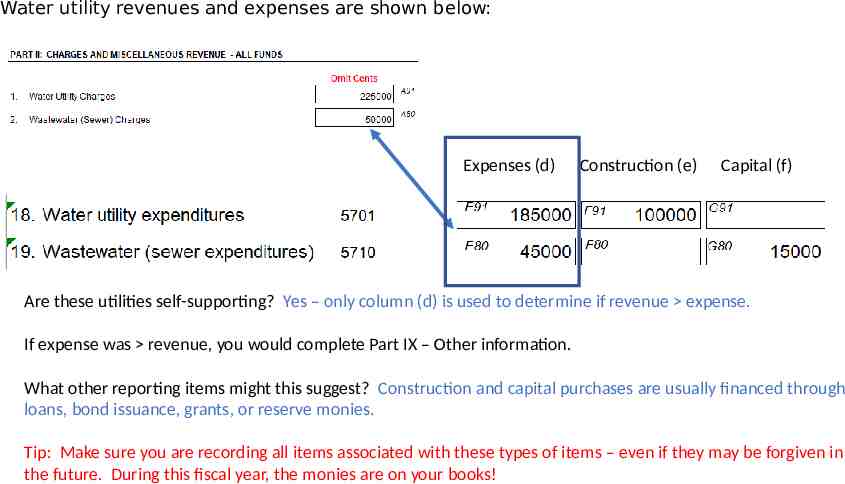

Practice Scenario #3 Water utility revenues and expenses are shown below: Expenses (d) Are these utilities self-supporting? If not, what additional form must be completed? What other reporting items might this suggest? Construction (e) Capital (f)

Water utility revenues and expenses are shown below: Expenses (d) Construction (e) Capital (f) Are these utilities self-supporting? Yes – only column (d) is used to determine if revenue expense. If expense was revenue, you would complete Part IX – Other information. What other reporting items might this suggest? Construction and capital purchases are usually financed through loans, bond issuance, grants, or reserve monies. Tip: Make sure you are recording all items associated with these types of items – even if they may be forgiven in the future. During this fiscal year, the monies are on your books!

Practice Scenario #4 At the end of last year 2020, you had accounts receivable accrual of 1,000. This year, you had income of 5,000, and your accounts receivable accrual was 500 at the end of the year, 2021. How much revenue did we earn this year? How much cash did we receive? What was the change in the accrual?

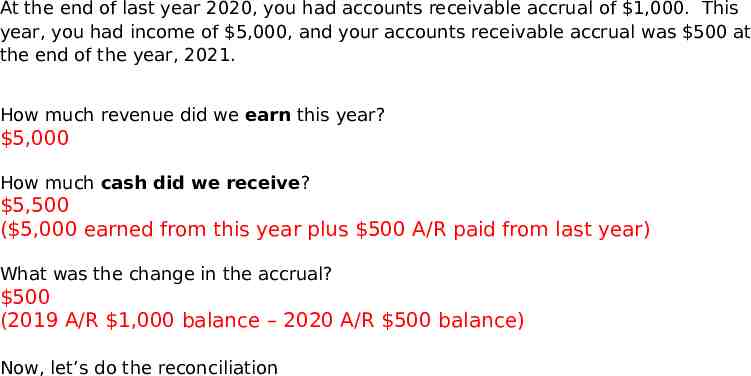

At the end of last year 2020, you had accounts receivable accrual of 1,000. This year, you had income of 5,000, and your accounts receivable accrual was 500 at the end of the year, 2021. How much revenue did we earn this year? 5,000 How much cash did we receive? 5,500 ( 5,000 earned from this year plus 500 A/R paid from last year) What was the change in the accrual? 500 (2019 A/R 1,000 balance – 2020 A/R 500 balance) Now, let’s do the reconciliation

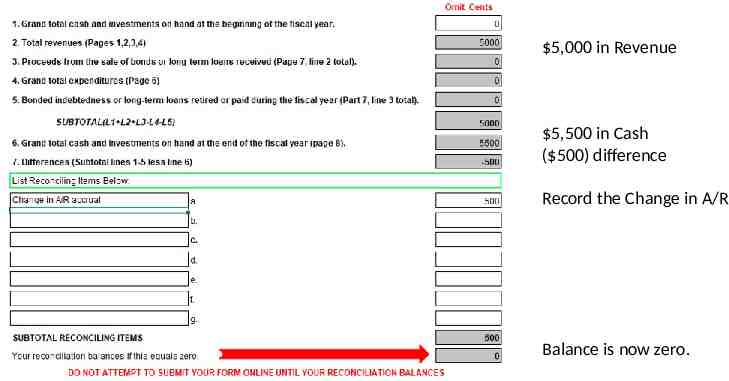

5,000 in Revenue 5,500 in Cash ( 500) difference Record the Change in A/R Balance is now zero.

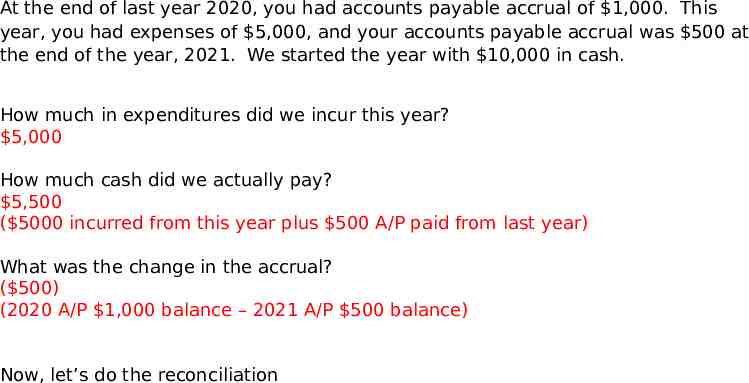

Practice Scenario #5 At the end of last year 2020, you had accounts payable accrual of 1,000. This year, you had expenses of 5,000, and your accounts payable accrual was 500 at the end of the year, 2021. We started the year with 10,000 in cash. How much in expenditures did we incur this year? How much cash did we actually pay? What was the change in the accrual?

At the end of last year 2020, you had accounts payable accrual of 1,000. This year, you had expenses of 5,000, and your accounts payable accrual was 500 at the end of the year, 2021. We started the year with 10,000 in cash. How much in expenditures did we incur this year? 5,000 How much cash did we actually pay? 5,500 ( 5000 incurred from this year plus 500 A/P paid from last year) What was the change in the accrual? ( 500) (2020 A/P 1,000 balance – 2021 A/P 500 balance) Now, let’s do the reconciliation

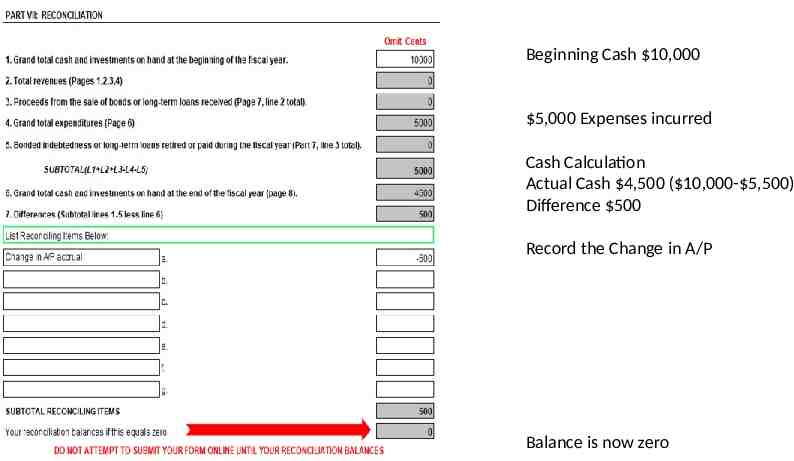

Beginning Cash 10,000 5,000 Expenses incurred Cash Calculation Actual Cash 4,500 ( 10,000- 5,500) Difference 500 Record the Change in A/P Balance is now zero

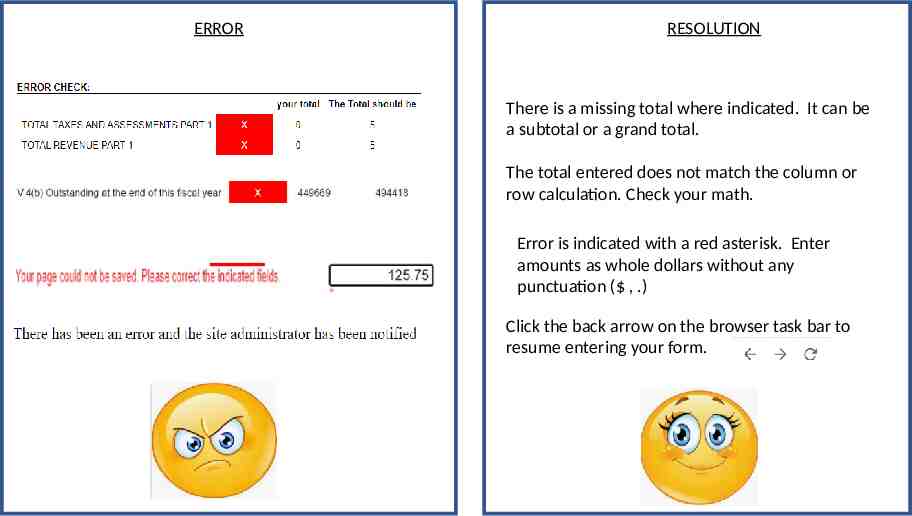

Common Online Errors

ERROR RESOLUTION There is a missing total where indicated. It can be a subtotal or a grand total. The total entered does not match the column or row calculation. Check your math. Error is indicated with a red asterisk. Enter amounts as whole dollars without any punctuation ( , .) Click the back arrow on the browser task bar to resume entering your form.

Thank you for your participation in today’s seminar!!