Recent Developments In The Theory And Practice Of Islamic Banking

34 Slides133.50 KB

Recent Developments In The Theory And Practice Of Islamic Banking And Finance Humayon Dar Loughborough University

References El-Gamal, M. A. 2000 A Basic Guide to Contemporary Islamic Banking and Finance. ONLINE RESOURCE http://www.ruf.rice.edu/ elgamal/files/primer.pdf Al-Jarhi, M. A. and Iqbal, M. 2001 Islamic Banking: Answers to Some Frequently Asked Questions. Jeddah: IRTI.

Lecture Plan Introduction Models of Islamic banking and finance Earlier models Later models Practice Pre-1980 1980-1990 1990 onwards

Lecture Plan Recent developments Change in thinking/emphasis Future Conclusions

Introduction Banking and finance in commensurate with the Shariah – Islamic law Shariah-compliant banking? Halal banking?

Introduction Banking and finance as an integral part of an Islamic economic system Banking and finance to achieve policy objectives of an Islamic system? Social Banking?

Introduction Spread all over the world Over 50-75 countries About 250 Islamic financial institutions 200- 800 billion in size Average annual growth of 15%

How Did It All Start? It is a modern banking style: post-1950 phenomenon Egypt (1963), Malaysia (1963) and Pakistan (1965) early experimentation Malaysia stands out Pakistan and Egypt left behind The Middle East as a hub of Islamic Finance

What Was The Initial Thinking? Ills of interest highlighted interest-based financial system: a cause of under-development Need for an Islamic alternative socio-economic development, equity and justice etc emphasised Idea of social or community banking Mit Ghamr was a social bank

What Was The Initial Thinking? Development motive was at the heart of Islamic banking thinking Islamic Development Bank (1974)

Modelling Islamic Banking And Finance Modelling of Islamic banking shifted the emphasis from social banking to profit loss sharing and profit-motive Two-Tier Mudaraba Model profit motive emphasised Conventional banking style was adopted as a way forward private banks or special Islamic banks (1974 - )

Practice Murabaha or fixed-return modes dominated PLS marginalised Idea of social/ community/ development banking faded away Era of Islamic commercial banking earning profit as opposed to charging interest

Practice Anglo-Saxon model of banking Profitability as a yardstick of success

Current Issues Transition from interest-free paradigm to asset-based paradigm Pricing of Islamic financial products Screening principles for investing in equity and stocks

Current Issues Financial innovation Regulation of Islamic financial services Towards a theory of Islamic financial firm

Interest-Free Versus Asset-Based Interest-free banking was a hallmark of Islamic finance pre-1990 emphasis Institutionalisation of Murabaha post-1990 phenomenon Return on asset-backed financial assets is acceptable

An Example! 1. 2. I need 100,000 for a business venture for a period of one year. I have got two options Borrowing at a rate of interest of 7% Going Islamic way First is not acceptable to my Shariah Advisor What about the second?

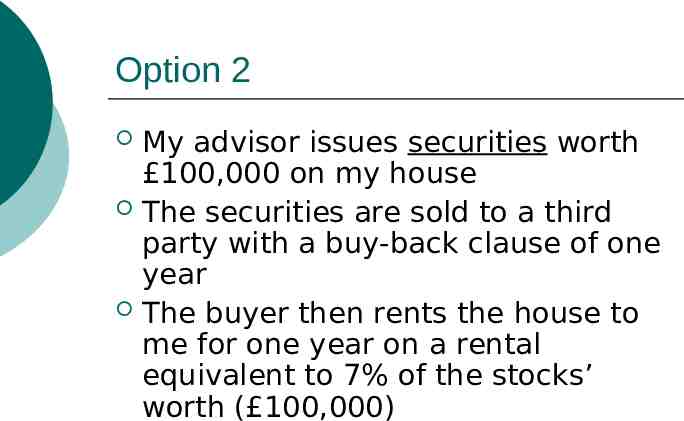

Option 2 My advisor issues securities worth 100,000 on my house The securities are sold to a third party with a buy-back clause of one year The buyer then rents the house to me for one year on a rental equivalent to 7% of the stocks’ worth ( 100,000)

Option 2 Is it acceptable? YES This is what we do in securitisation!!!

What’s The Difference? Option 1 involves Riba while Option 2 involves trade Probably right But Are they really different? Yes Probably not

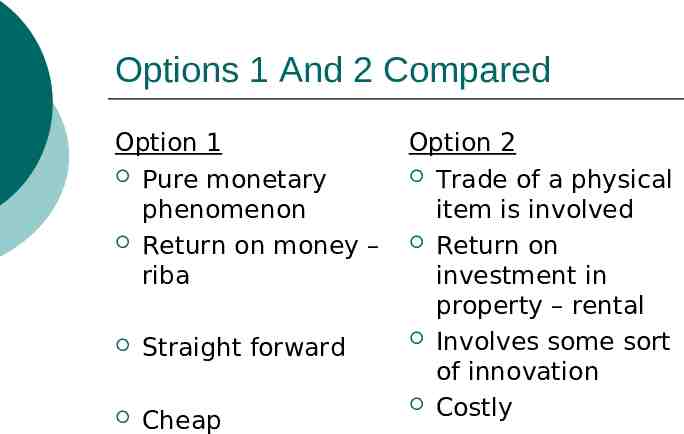

Options 1 And 2 Compared Option 1 Pure monetary phenomenon Return on money – riba Straight forward Cheap Option 2 Trade of a physical item is involved Return on investment in property – rental Involves some sort of innovation Costly

But Are They Really Different? Option 1 Return on money Option 2 Return on securities

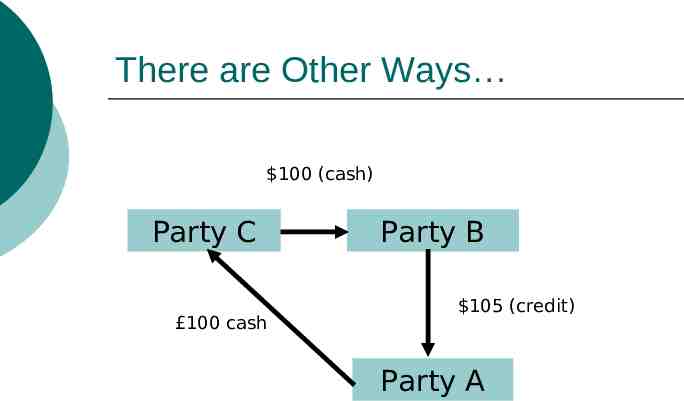

There are Other Ways 100 (cash) Party C 100 cash Party B 105 (credit) Party A

Result Asset-based financing has become a hallmark of Islamic banking and finance in the 21st century

Pricing Of Islamic Financial Products Interest remains relevant Benchmarking with LIBOR, KLIBOR Positive correlation between interest and prices of Islamic financial products Normally a “mark-up” over the benchmarked interest

Consequently Demand for Islamic finance remains sluggish at a grassroots level Islamic finance’s focus remains on the so-called “captive market” Islamic finance as an elitist phenomenon Is it supply-driven?

Principles Of Islamic Investing Investing in stocks in a Halal/ Islamic way Dow Jones and FT Islamic Indices Full details available on the respective websites http://www.djindexes.com http://www.ftse.com/indices market data/ground rules/global-islamic-gro und-rules.pdf Islamic investment/ mutual fund industry

Financial Innovation Strong need for financial innovation for further growth in Islamic finance Securitisation Sukuk structures

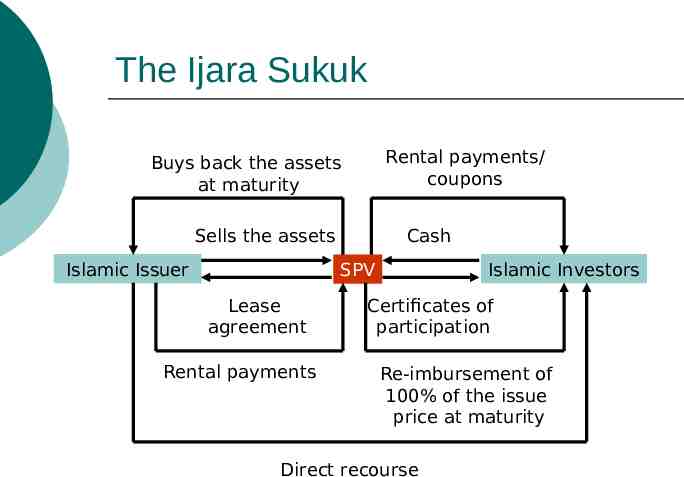

The Ijara Sukuk Rental payments/ coupons Buys back the assets at maturity Sells the assets Islamic Issuer Cash Islamic Investors SPV Lease agreement Rental payments Certificates of participation Re-imbursement of 100% of the issue price at maturity Direct recourse

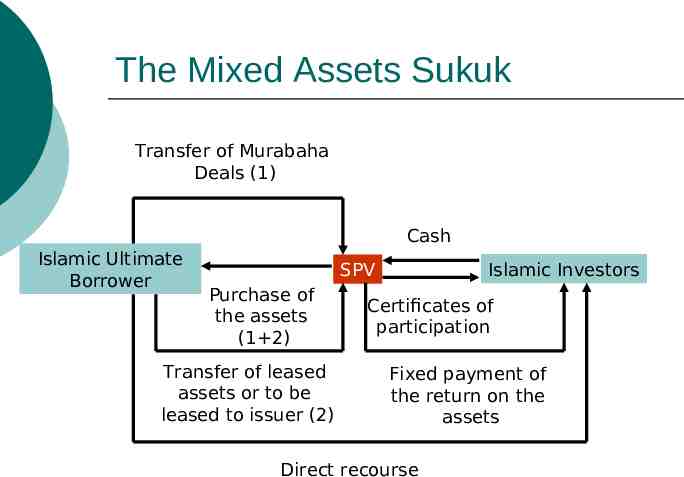

The Mixed Assets Sukuk Transfer of Murabaha Deals (1) Cash Islamic Ultimate Borrower Islamic Investors SPV Purchase of the assets (1 2) Transfer of leased assets or to be leased to issuer (2) Certificates of participation Fixed payment of the return on the assets Direct recourse

Regulation of Islamic Financial Services Separate regulatory framework for Islamic finance is considered a necessity AAIOFI IFSB

Towards A Theory Of The Islamic Financial Firm Definition(s) Objectives Analysis

Future Of Islamic Finance Not much different from conventional finance Need for re-direction Need for genuine innovation Future lies in Islamic homelands and not in the Western financial centres

Conclusion Thank you