CORPORATE FINANCE FOR LONG-TERM VALUE Chapter 4: Discount rates

23 Slides775.98 KB

CORPORATE FINANCE FOR LONG-TERM VALUE Chapter 4: Discount rates and scarcity of capital

Part 2: Discount rates and valuation methods Chapter 4: Discount rates and scarcity of capital

The BIG Picture 3 Discounting reflects the time value of money Also other components: premium for market risk, credit risk, liquidity risk Financial discount rates are used for FV and depend on supply and demand of funds in financial markets government policies central banks setting ST interest rates Social discount rates are used for SV and EV Company’s counterparties are societal stakeholders: employees, clients, suppliers, environment ( current future generations) Big question: should current and future generations be treated equal?

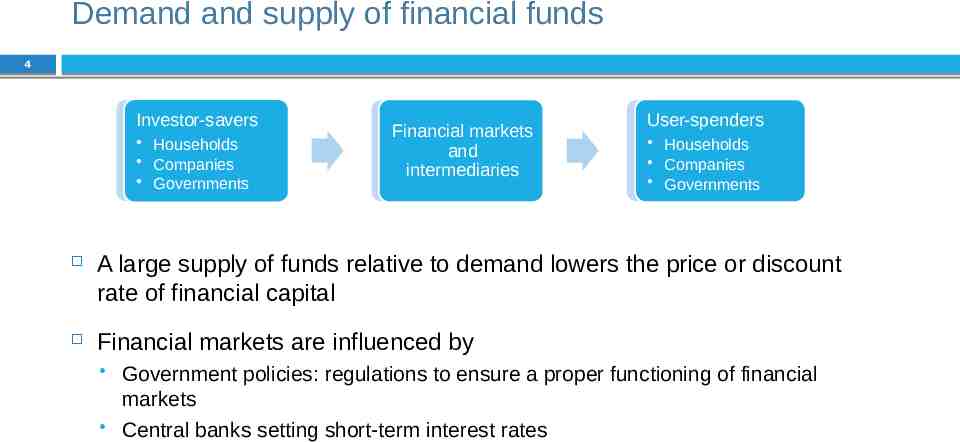

Demand and supply of financial funds 4 Investor-savers Households Companies Governments Financial markets and intermediaries User-spenders Households Companies Governments A large supply of funds relative to demand lowers the price or discount rate of financial capital Financial markets are influenced by Government policies: regulations to ensure a proper functioning of financial markets Central banks setting short-term interest rates

Time value of money 5 People prefer money today over money tomorrow due to inflation and opportunity costs The difference in value between money now and money in the future is called the time value of money The difference is calculated with a discount rate, which is the interest rate r used to determine the present value (PV) of future cash flows The discount factor is the factor by which a future cash flow over n periods must be multiplied to obtain the PV: discount factor

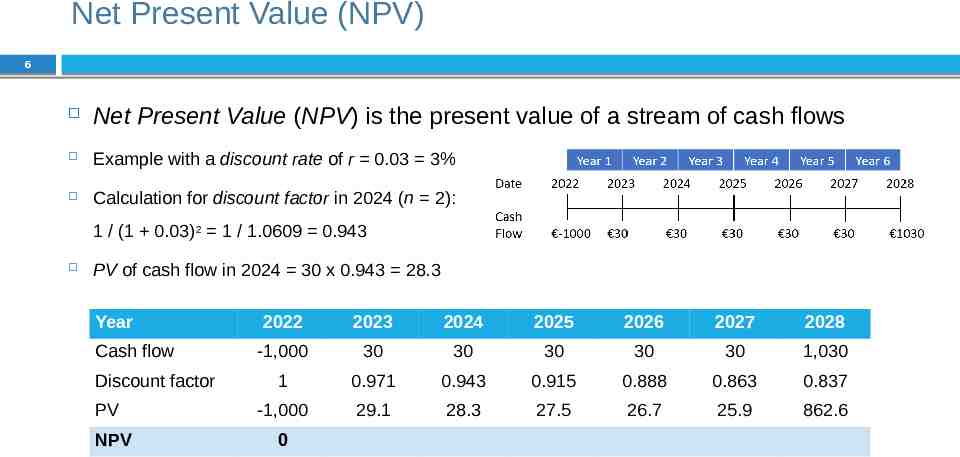

Net Present Value (NPV) 6 Net Present Value (NPV) is the present value of a stream of cash flows Example with a discount rate of r 0.03 3% Calculation for discount factor in 2024 (n 2): 1 / (1 0.03)2 1 / 1.0609 0.943 PV of cash flow in 2024 30 x 0.943 28.3 Year Cash flow Discount factor PV NPV 2022 2023 2024 2025 2026 2027 2028 -1,000 30 30 30 30 30 1,030 1 0.971 0.943 0.915 0.888 0.863 0.837 -1,000 29.1 28.3 27.5 26.7 25.9 862.6 0

Arbitrage and law of one price 7 Arbitrage the buying and selling of ‘equivalent’ or ‘similar’ goods in different markets to benefit from price differences (exceeding transaction costs) Arbitrage opportunity situation in which it is possible to make a profit from an investment without taking risk (‘free lunch’) Arbitrage only works if the law of one price does not hold, which says that the same product should sell at the same price Finance predicts that arbitrage profits (NPVs) will often be zero: competition between investors will quickly result in the adjustment of prices of over- or underpriced securities

Law of one price in Finance 8 Finance predicts that arbitrage profits (NPVs) will often be zero: competition between investors will quickly result in the adjustment of prices of over- or under-priced securities Law of one price is underlying many calculations and valuations - two securities that generate the same payoff must cost the same Yields of bonds with same maturity, credit risk and liquidity risk (Ch8) Modigliani-Miller theorem on capital structure (Ch15) Options pricing – put-call parity (Ch19) Etc.

Principal financial markets 9 Money market - for short-term funds up to one year Bond markets - most important segment of the market for debt securities, with a maturity of more than one year Equity markets – companies issue equity to raise funds Derivatives market - financial instruments whose value is derived from the value of the underlying financial instruments Foreign exchange market – determines relative currency value

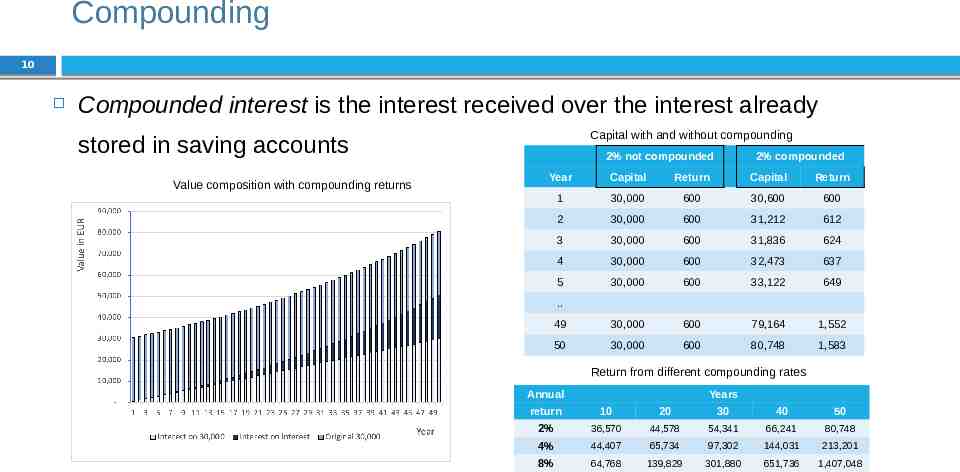

Compounding 10 Compounded interest is the interest received over the interest already Capital with and without compounding stored in saving accounts Value composition with compounding returns 2% not compounded 2% compounded Year Capital Return Capital Return 1 30,000 600 30,600 600 2 30,000 600 31,212 612 3 30,000 600 31,836 624 4 30,000 600 32,473 637 5 30,000 600 33,122 649 49 30,000 600 79,164 1,552 50 30,000 600 80,748 1,583 . Return from different compounding rates Annual Years return 10 20 30 40 50 2% 36,570 44,578 54,341 66,241 80,748 4% 44,407 65,734 97,302 144,031 213,201 8% 64,768 139,829 301,880 651,736 1,407,048

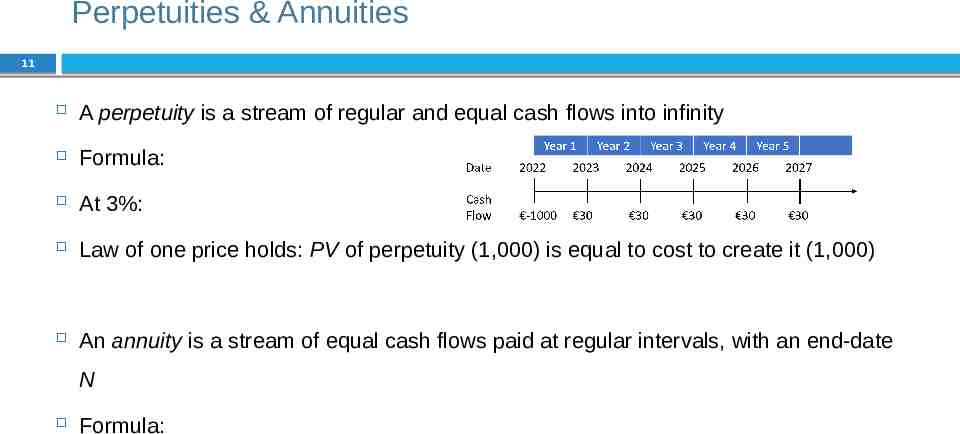

Perpetuities & Annuities 11 A perpetuity is a stream of regular and equal cash flows into infinity Formula: At 3%: Law of one price holds: PV of perpetuity (1,000) is equal to cost to create it (1,000) An annuity is a stream of equal cash flows paid at regular intervals, with an end-date N Formula:

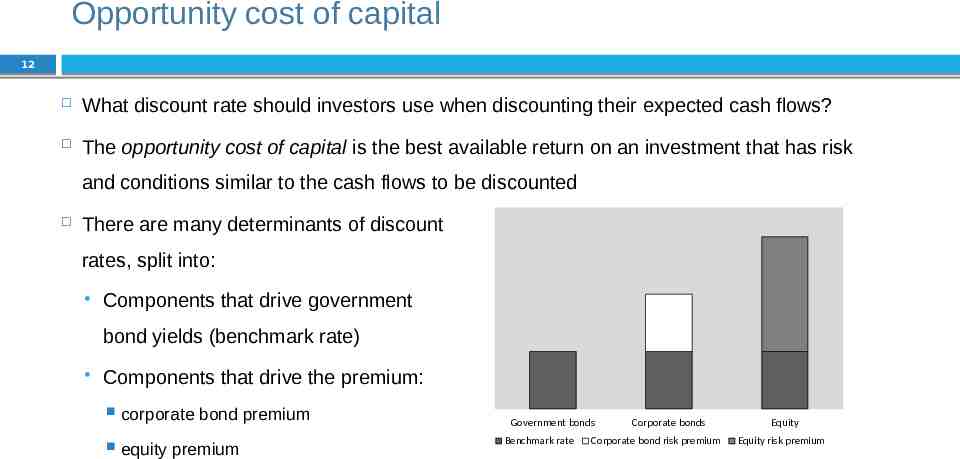

Opportunity cost of capital 12 What discount rate should investors use when discounting their expected cash flows? The opportunity cost of capital is the best available return on an investment that has risk and conditions similar to the cash flows to be discounted There are many determinants of discount rates, split into: Components that drive government bond yields (benchmark rate) Components that drive the premium: corporate bond premium equity premium 7% 6% 5% 4% 3% 2% 1% 0% Government bonds Benchmark rate Corporate bonds Corporate bond risk premium Equity Equity risk premium

Benchmark – government bonds 13 The highest quality government securities are considered ‘risk-free’ Market discount rates are the benchmarks against which discount rates are determined Yields of government bonds are influenced by expected short-term interest rates and the term premium Risk-averse investors demand a term premium (or risk premium) for investments in long-term bonds The term premium leads to a positive term spread, which is the difference between yields for bonds with longer maturity and yields for bonds with shorter maturity

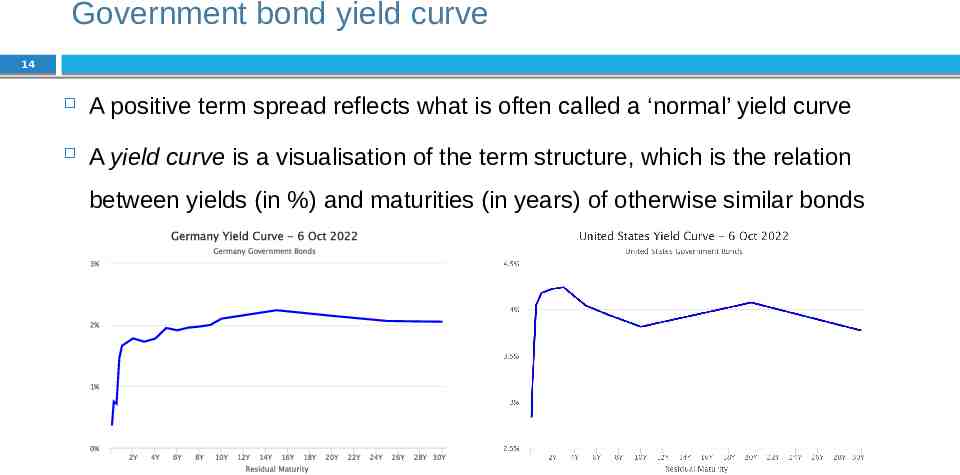

Government bond yield curve 14 A positive term spread reflects what is often called a ‘normal’ yield curve A yield curve is a visualisation of the term structure, which is the relation between yields (in %) and maturities (in years) of otherwise similar bonds

Credit risk 15 Apart from interest rate expectations and the term premium, credit risk and liquidity also influence government bond yields Credit risk premium is the spread between the yield of a particular bond and the yield of a bond with similar characteristics but without credit risk Rating agencies (Moody’s, S&P, Fitch) indicate issuers’ credit risk by assigning them a credit rating, (AAA, A , BBB-, etc.) Drivers of country credit rating differences: per capita income, GDP growth, inflation, external debt, economic development and default history

Liquidity 16 Liquidity is the ease with which an investor can sell or buy a bond immediately at a price close to the market price Liquidity premium is the spread between the yield of a bond with high liquidity and a similar bond with less liquidity Example A very liquid 1-yr government bond may trade at a yield of 4.17% And a a less liquid 1-jr gov bond at a yield of 4.30% Liquidity premium is then 13 basis points (4.30% - 4.17% 0.13%)

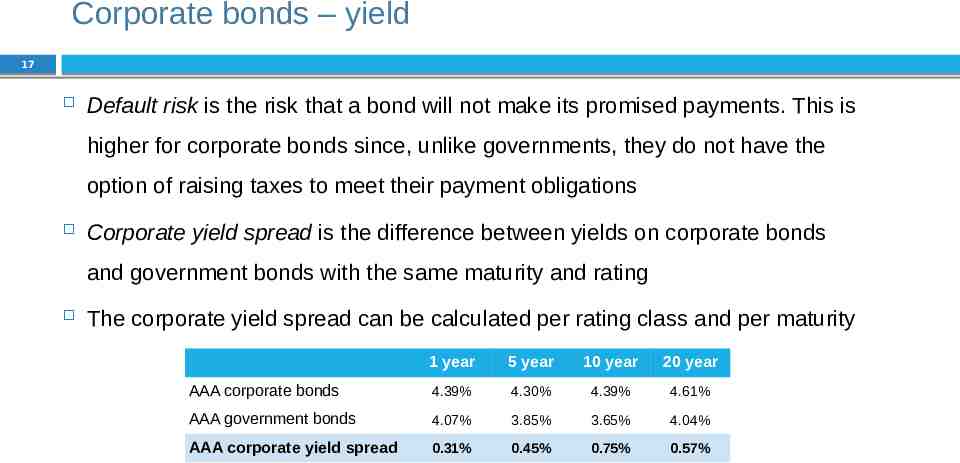

Corporate bonds – yield 17 Default risk is the risk that a bond will not make its promised payments. This is higher for corporate bonds since, unlike governments, they do not have the option of raising taxes to meet their payment obligations Corporate yield spread is the difference between yields on corporate bonds and government bonds with the same maturity and rating The corporate yield spread can be calculated per rating class and per maturity 1 year 5 year 10 year 20 year AAA corporate bonds 4.39% 4.30% 4.39% 4.61% AAA government bonds 4.07% 3.85% 3.65% 4.04% AAA corporate yield spread 0.31% 0.45% 0.75% 0.57%

Equities – market risk premium 18 Shareholders are residual claimants as they are paid only after other stakeholders have been paid As a result, equity typically carries a higher risk than corporate bonds The equity risk premium is the expected excess return of equities over the risk-free rate The equity risk premium tends to be higher for smaller companies, more cyclical companies, and companies with weaker corporate governance

Discounting social and environmental capital 19 The counterparty of companies’ social and environmental capital is the wider society, representing current and future generations. This raises two fundamental and ethical questions: Should current and future generations be treated equally? What is the appropriate discount rate for society (the social discount rate)? Equal treatment of current and future generations implies a zero time preference between current and future generations

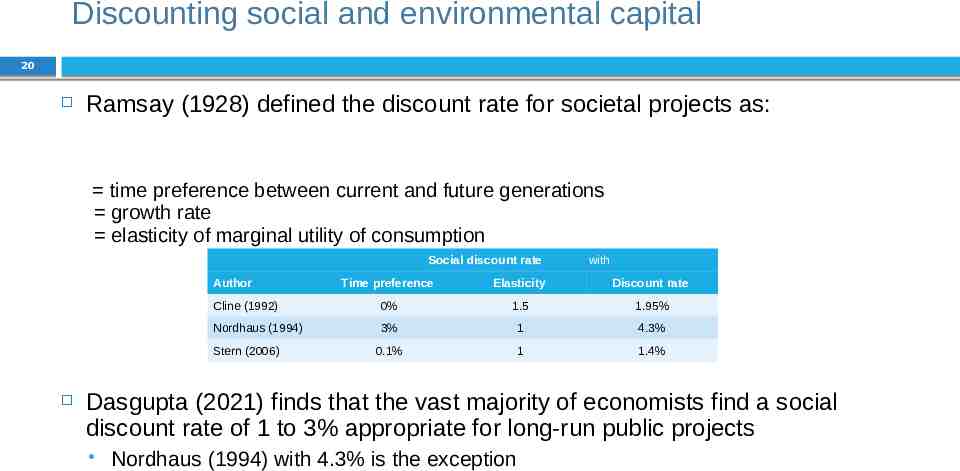

Discounting social and environmental capital 20 Ramsay (1928) defined the discount rate for societal projects as: time preference between current and future generations growth rate elasticity of marginal utility of consumption Social discount rate Author Time preference Elasticity Discount rate Cline (1992) 0% 1.5 1.95% Nordhaus (1994) 3% 1 4.3% 0.1% 1 1.4% Stern (2006) with Dasgupta (2021) finds that the vast majority of economists find a social discount rate of 1 to 3% appropriate for long-run public projects Nordhaus (1994) with 4.3% is the exception

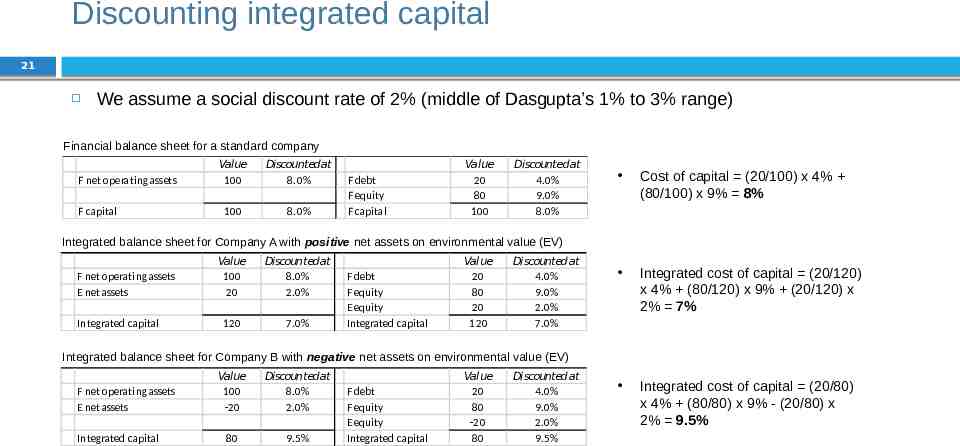

Discounting integrated capital 21 We assume a social discount rate of 2% (middle of Dasgupta’s 1% to 3% range) Financial balance sheet for a standard company F net operating assets F capital Value 100 Discounted at 8.0% 100 8.0% F debt F equity F capital Value 20 80 100 Discounted at 4.0% 9.0% 8.0% Cost of capital (20/100) x 4% (80/100) x 9% 8% Integrated cost of capital (20/120) x 4% (80/120) x 9% (20/120) x 2% 7% Integrated cost of capital (20/80) x 4% (80/80) x 9% - (20/80) x 2% 9.5% Integrated balance sheet for Company A with positive net assets on environmental value (EV) F net operating assets E net assets Integrated capital Value 100 20 Discounted at 8.0% 2.0% 120 7.0% F debt F equity E equity Integrated capital Value 20 80 20 120 Discounted at 4.0% 9.0% 2.0% 7.0% Integrated balance sheet for Company B with negative net assets on environmental value (EV) F net operating assets E net assets Integrated capital Value 100 -20 Discounted at 8.0% 2.0% 80 9.5% F debt F equity E equity Integrated capital Value 20 80 -20 80 Discounted at 4.0% 9.0% 2.0% 9.5%

Internalisation 22 Similar starting financial balance can be different after (the anticipation of) internalisation of social and environmental externalities The empirical prediction is: Companies with large social and environmental liabilities will have a higher cost of integrated capital Companies with social and environmental assets will enjoy a lower cost of integrated capital The risk premium will rise when the risk of internalisation rises

Conclusions 23 Present values and discount rates are needed when considering the future in investment decisions The counterparty of companies’ social and environmental capital is the wider society, representing current and future generations An equal treatment of current and future generations implies a low social discount rate Larger environmental and social liabilities raise the cost of integrated capital, while environmental and social assets lower the cost of integrated capital