Chapter 3 The Audit Process

13 Slides143.00 KB

Chapter 3 The Audit Process

Overview of Audit Process Developing an Understanding with the Client Financial statement engagements Audits Compilations Reviews

Accepting a Potential Client Need to assess: Reasons for a change in auditors Management’s integrity and reputation Any legal proceedings Overall financial position Related party transactions Major risks affecting the client and the future of the client’s operations

The Engagement Letter Mutual understanding of the nature of the audit services Timing of services Expected fees Responsibilities for fraud detection Client’s responsibilities Need for other services

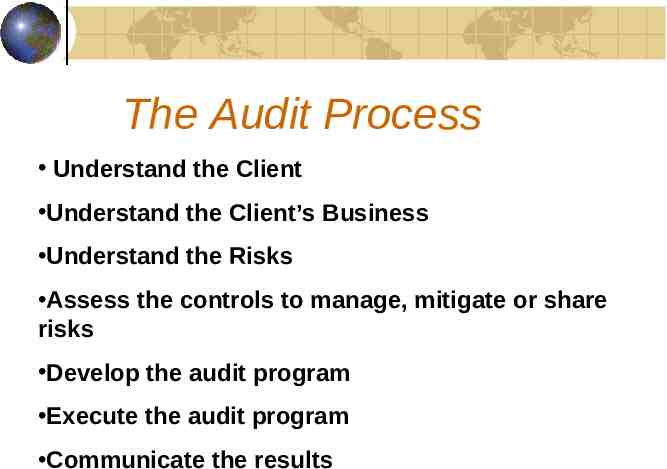

The Audit Process Understand the Client Understand the Client’s Business Understand the Risks Assess the controls to manage, mitigate or share risks Develop the audit program Execute the audit program Communicate the results

Materiality and Audit Risk What is Materiality? The magnitude of an omission or misstatement of accounting information that, in light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the omission or misstatement.

Materiality and Audit Risk Overall materiality versus individual account materiality Materiality Approaches Risk of Material Misstatement Risk-based approach to auditing Risk Concepts Engagement risk Audit risk

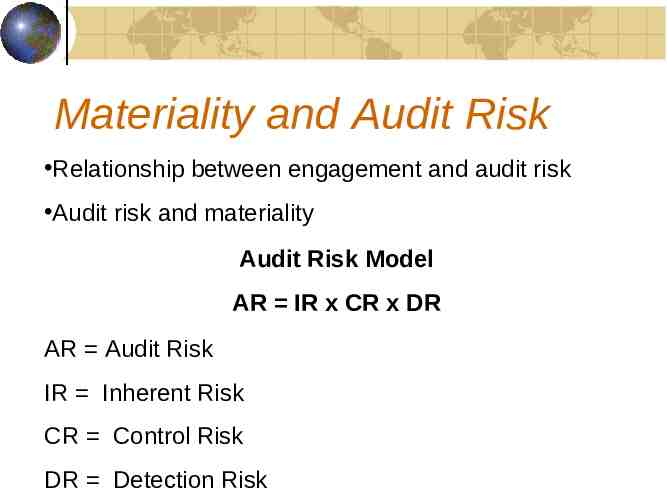

Materiality and Audit Risk Relationship between engagement and audit risk Audit risk and materiality Audit Risk Model AR IR x CR x DR AR Audit Risk IR Inherent Risk CR Control Risk DR Detection Risk

Audit Risk Model Inherent Risk - the susceptibility of transactions to be recorded in error or to be influenced by management’s fraudulent activities. Control Risk - the risk that a material misstatement that could occur in a transaction or adjusting entries will not be prevented or quickly detected by the entity’s internal controls. Environment Risk - A combination of inherent and control risk. Detection Risk - The risk that the auditor will not detect a material misstatement that exists in an account balance.

Limitations of the Audit Risk Model Inherent risk is difficult to formally assess. Audit risk is subjectively determined. The model treats each risk component as separate and independent. Audit technology is not so precisely developed that each component of the model can be accurately assessed. Adjusting Audit Risk

Management Assertions Assertions are positive statements about the “state of being.” Financial Statement Assertions Existence or occurrence Completeness Rights and obligations Valuation or allocation Presentation and disclosure

Assertions for Other Assurance Services Specific to each engagement All assurance services are driven by specific assertions. The auditor’s task is to identify evidence that is persuasive about the assertions being tested.

Audit Evidence and Procedures Broad Concepts of Audit Evidence Relevance Persuasiveness Sufficiency Relationship Among Audit Procedures and Assertions AUDIT PROGRAMS