Audit Information Sharing Rouen Reynolds, CPA, Assistant

14 Slides80.18 KB

Audit Information Sharing Rouen Reynolds, CPA, Assistant Director Sales & Use Tax Division Alabama Department of Revenue

Section 40-2A-10 Confidentiality, disclosure and exchange of tax returns and tax information (e) The commissioner shall promulgate reasonable regulations permitting and governing the exchange of tax returns, information, records, and other documents secured by the department, with tax officers of other agencies of the state, municipal, and county government agencies in the state, federal government agencies, any association of state government tax agencies, any state government tax agencies of other states, and any foreign government tax agencies.

Provisions However, (1) any tax returns, information, records, or other documents remain subject to the confidentiality provisions set forth in subsection (a); (2) the department may charge a reasonable fee for providing information or documents for the benefit of self-administered counties and municipalities; (3) self-administered counties and municipalities may charge a reasonable fee for providing information or documents for the benefit of the department; and

(4) any exchange shall be for one or more of the following purposes: a. Collecting taxes due. b. Ascertaining the amount of taxes due from any person. c. Determining whether a person is liable for, or whether there is probable cause for believing a person might be liable for, the payment of any tax to a federal, state, county, municipal, or foreign government agency.

Exchange of Information Agreement Be sure that the Department has the most up-to-date list To update the list to include authorized personnel, contact Sally Springer in the Commissioner’s Office 334-242-1193

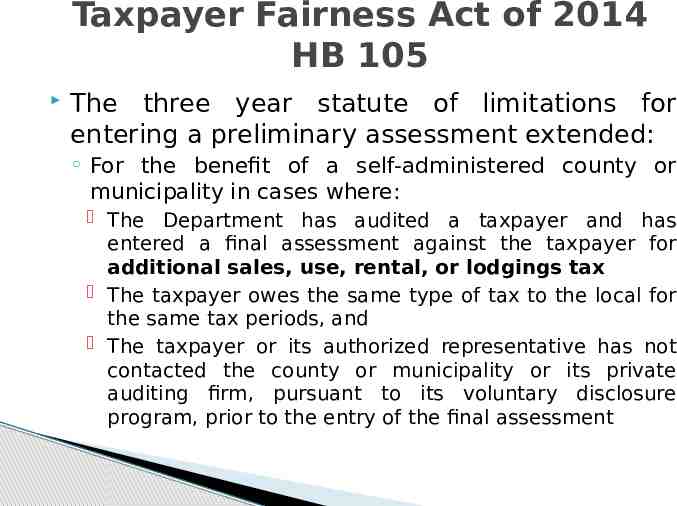

Taxpayer Fairness Act of 2014 HB 105 The three year statute of limitations for entering a preliminary assessment extended: For the benefit of a self-administered county or municipality in cases where: The Department has audited a taxpayer and has entered a final assessment against the taxpayer for additional sales, use, rental, or lodgings tax The taxpayer owes the same type of tax to the local for the same tax periods, and The taxpayer or its authorized representative has not contacted the county or municipality or its private auditing firm, pursuant to its voluntary disclosure program, prior to the entry of the final assessment

Statute of Limitations Extended Shall not expire until the earlier of 6 months from the date of the entry of the final assessment or 60 days following the date of mailing or transmittal by electronic mail by the Department to the self-administered county or municipality or its private auditing firm of a copy of the notice of final assessment and any attachments thereto.

Limitations Any tax assessed by the self-administered county or municipality within the additional time period allowed shall be limited to: Those items changed or adjustments included in the final assessment entered by the Department.

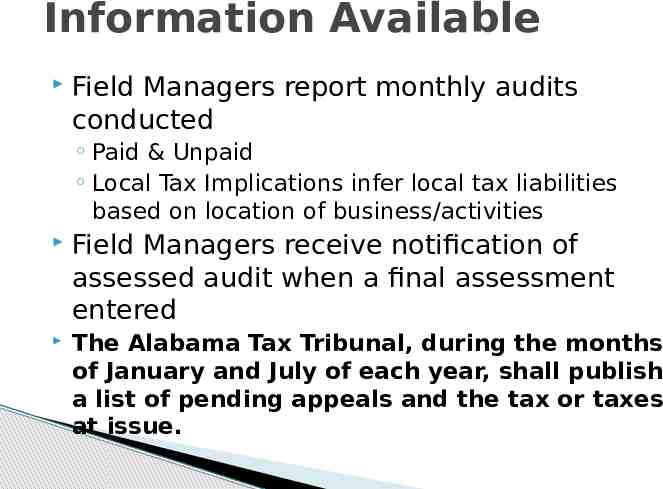

Information Available Field Managers report monthly audits conducted Paid & Unpaid Local Tax Implications infer local tax liabilities based on location of business/activities Field Managers receive notification of assessed audit when a final assessment entered The Alabama Tax Tribunal, during the months of January and July of each year, shall publish a list of pending appeals and the tax or taxes at issue.

How to Request Information Contact the Manager in the District you are located. Define scope of audits being requested Make sure the names on the Exchange Agreement are up-to-date Designate type medium for information preferred Taxmaster file PDF CD Information is encrypted and password protected

Statute Extension Only Applies to Final Assessments Final Assessments not published Subject to confidentiality laws Request District to advise of any contested audits Contact local TPSC to check status of audits subject to being assessed Public record once appealed to Administrative Law Division aka Tax Tribunal

Sample Letter Transmittal Dear Ms. H: Subject: Transmittal of Audits – July thru September 2011 In accordance with the agreement between the State of Alabama Department of Revenue and XXXXX County, enclosed is a disc containing the State tax audits conducted by the Montgomery District Sales and Use Tax Field Office. This information was obtained while a state tax audit was being conducted on the taxpayer. There may be other untaxed items for your locality which were not picked up in this audit. The data is being provided using . Password: LOCAL As you are aware, the information may be used for tax administration purposes only. Upon completion of the use of the enclosed tax information, the recipient agrees to destroy the information and to advise the furnishing party in writing of its destruction. We hope this information will prove helpful in the administration of your tax laws. Yours very truly, Bill Hall, Manager Sales & Use Tax Division Montgomery Taxpayer Service Center

Taxpayer Service Centers www.revenue.alabama.gov/salestax Auburn-Opelika TPSC Wayne Harkins: 334-887-9549 Jefferson-Shelby TPSC Anne Carlton: 205-733-2741 Lynn Nicholson: 205-733-2765 Dothan TPSC Debbie Lee: 334-793-5803 Gadsden TPSC Lisa McKnight: Huntsville TPSC Russell Jones: 256-547-0554 256-837-2319 Mobile TPSC Michele Mayberry: 251-344-4737 Montgomery TPSC Bill Hall: 334-242-2677 Tuscaloosa TPSC Jerry Bobo: 205-759-2571

Foreign Audit Division Leslie Michaud 334-242-1266 Sales & Use Tax Division Ron Rein 334-242-1633 Rouen Reynolds 334-242-1494 or 1575