8 Chapter Accounting for General Long-Term Liabilities

29 Slides353.00 KB

8 Chapter Accounting for General Long-Term Liabilities

What are General Long-term Liabilities? A: Debt and other long-term liabilities that arise from the activities of governmental funds that are not accounted for as fund liabilities of a proprietary or fiduciary fund. If debt reported in a proprietary or fiduciary fund also has general obligation (“full faith and credit”) backing the contingent liability should be disclosed in the notes to the financial statements

Examples of General Long-term Liabilities Tax-supported bonds Long-term warrants Long-term notes Capital lease obligations Long-term portion of judgments and claims

Accounting for General Long-term Liabilities All general long-term liabilities are reported in the governmental activities column of the government-wide Statement of Net Assets. Not reported as liabilities of governmental funds. A debt service fund (a governmental fund), may be established to accounting for the principal and interest payments on general long-term liabilities

Terms Used in Describing Debt Burden Direct debt—obligations that will be repaid by the government whose debt is being evaluated Overlapping (indirect) debt—obligations of other governments that also have the power to tax property located in the jurisdiction of the government whose debt is being evaluated

Example - Overlapping Debt In a given city property owners might be taxed by the city, a county government, and an independent school district, among others. With respect to the city, the portion of the county’s total assessed valuation that lies within the city’s boundaries multiplied by the county’s debt is the amount of overlapping debt of the county borne by city residents See example on page 290

Debt Burden Debt Limit Usually a ceiling on the amount of debt defined as a statutory percentage of assessed valuation or some other valuation of taxable property Debt margin The difference between the debt limit and the amount of debt outstanding subject to the limit Self-supporting debt being repaid from user charges, such as water or sewer charges, typically not subject to the limit. Usually only net debt (debt minus cash available for principal repayment in a debt service fund) is subject to the limit.

Debt Burden Measures Debt per capita (ratio of debt to population) Ratio of debt to estimated true value of taxable property Ratio of debt service expenditures to total general expenditures Multiple year trends in above ratios

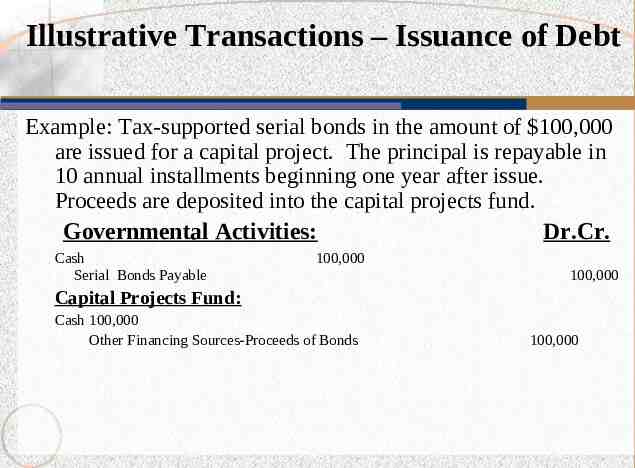

Illustrative Transactions – Issuance of Debt Example: Tax-supported serial bonds in the amount of 100,000 are issued for a capital project. The principal is repayable in 10 annual installments beginning one year after issue. Proceeds are deposited into the capital projects fund. Governmental Activities: Dr.Cr. Cash Serial Bonds Payable 100,000 100,000 Capital Projects Fund: Cash 100,000 Other Financing Sources-Proceeds of Bonds 100,000

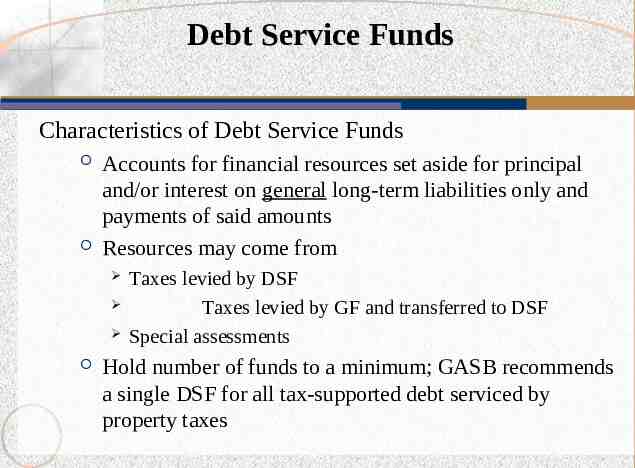

Debt Service Funds Characteristics of Debt Service Funds Accounts for financial resources set aside for principal and/or interest on general long-term liabilities only and payments of said amounts Resources may come from Taxes levied by DSF Taxes levied by GF and transferred to DSF Special assessments Hold number of funds to a minimum; GASB recommends a single DSF for all tax-supported debt serviced by property taxes

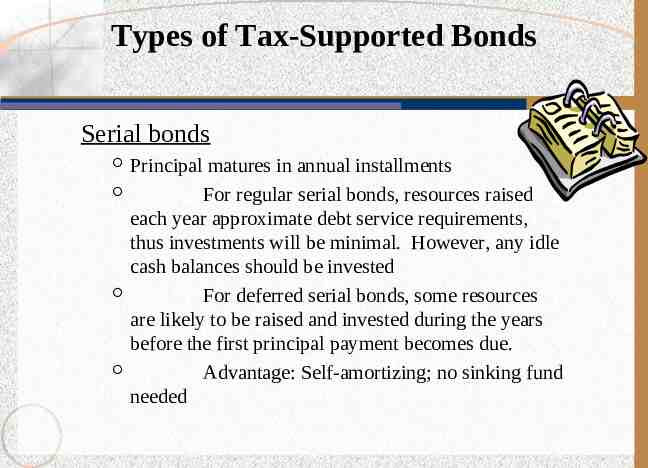

Types of Tax-Supported Bonds Serial bonds Principal matures in annual installments For regular serial bonds, resources raised each year approximate debt service requirements, thus investments will be minimal. However, any idle cash balances should be invested For deferred serial bonds, some resources are likely to be raised and invested during the years before the first principal payment becomes due. Advantage: Self-amortizing; no sinking fund needed

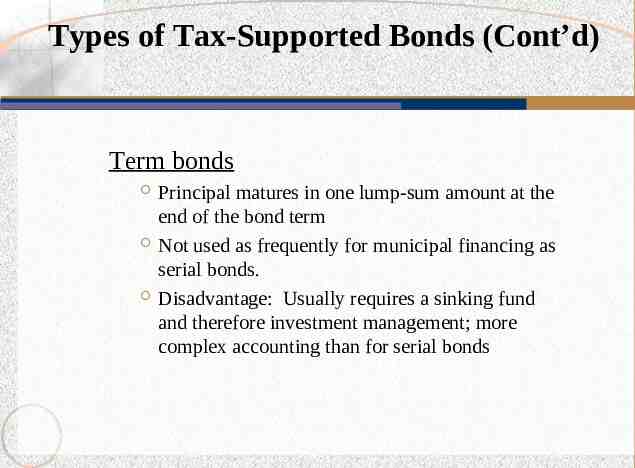

Types of Tax-Supported Bonds (Cont’d) Term bonds Principal matures in one lump-sum amount at the end of the bond term Not used as frequently for municipal financing as serial bonds. Disadvantage: Usually requires a sinking fund and therefore investment management; more complex accounting than for serial bonds

Accounting Principles and Procedures Use modified accrual, with one exception: Expenditures for interest and principal are generally recognized in period in which they are legally due Budgetary accounting typically is used--except there is no need for encumbrance accounting since the debt service fund does not order goods or enter into contracts for services For serial bonds, the amount budgeted for revenues or interfund transfers in is usually just what is needed that fiscal year for matured principal and interest.

Accounting Principles and Procedures (Cont’d) For term bonds (or deferred serial bonds), additional revenues or interfund transfers in are usually budgeted to meet sinking fund requirements, in addition to the amount needed for interest payments during the year Sinking fund investments are reported at fair value at year end. Changes in fair value are reported as a component of investment earnings.

DSF Example Assume bonds are issued on January 1, 2005 and pay interest semiannually on January 1 and July 1 in the amount of 100,000. The fiscal year ends on December 31, 2005. Q: How much expenditures would be recognized in fiscal 2005? A: Only the July 1, 2005 interest payment, or 100,000, would be recognized as an expenditure of 2005.

Accounting Principles and Procedures (Cont’d) If taxes are levied by the debt service fund, record “Estimated Revenues” in the budget entry and use the same property tax accounting as for the General Fund If taxes are levied by the General Fund and transferred to the debt service fund, record “Estimated Other Financing Sources” in the budget entry and “Interfund Transfers In (an Other Financing Sources account) for the transfer

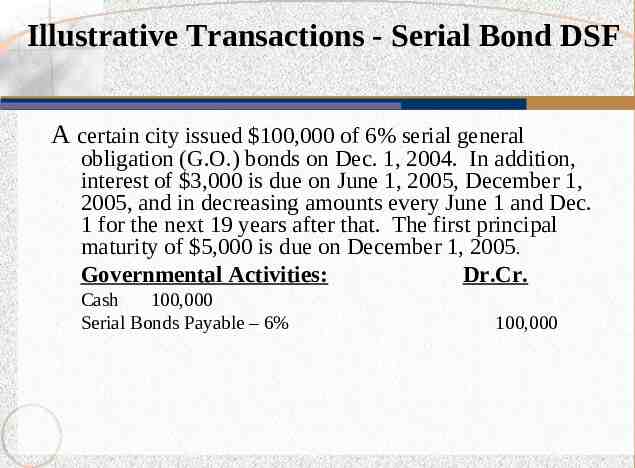

Illustrative Transactions - Serial Bond DSF A certain city issued 100,000 of 6% serial general obligation (G.O.) bonds on Dec. 1, 2004. In addition, interest of 3,000 is due on June 1, 2005, December 1, 2005, and in decreasing amounts every June 1 and Dec. 1 for the next 19 years after that. The first principal maturity of 5,000 is due on December 1, 2005. Governmental Activities: Dr.Cr. Cash 100,000 Serial Bonds Payable – 6% 100,000

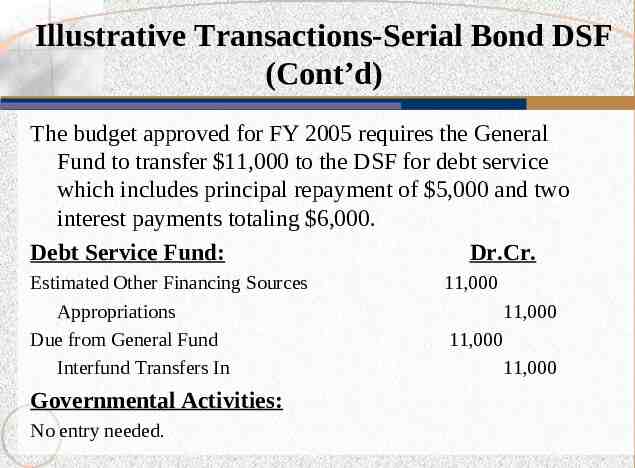

Illustrative Transactions-Serial Bond DSF (Cont’d) The budget approved for FY 2005 requires the General Fund to transfer 11,000 to the DSF for debt service which includes principal repayment of 5,000 and two interest payments totaling 6,000. Debt Service Fund: Dr.Cr. Estimated Other Financing Sources Appropriations Due from General Fund Interfund Transfers In Governmental Activities: No entry needed. 11,000 11,000 11,000 11,000

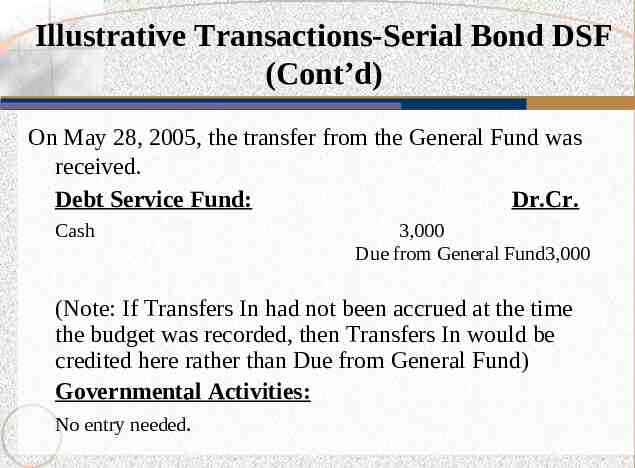

Illustrative Transactions-Serial Bond DSF (Cont’d) On May 28, 2005, the transfer from the General Fund was received. Debt Service Fund: Dr.Cr. Cash 3,000 Due from General Fund3,000 (Note: If Transfers In had not been accrued at the time the budget was recorded, then Transfers In would be credited here rather than Due from General Fund) Governmental Activities: No entry needed.

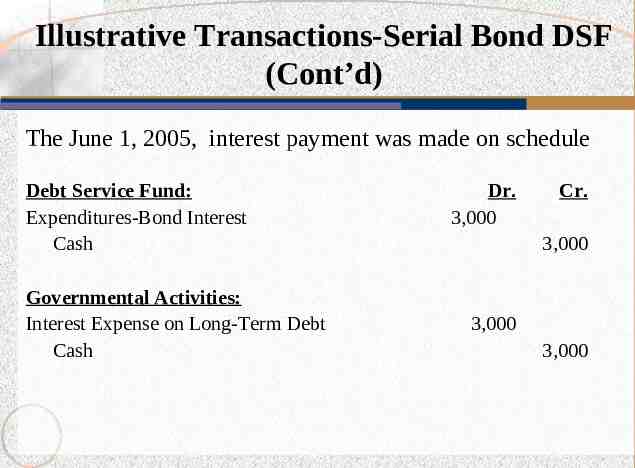

Illustrative Transactions-Serial Bond DSF (Cont’d) The June 1, 2005, interest payment was made on schedule Debt Service Fund: Expenditures-Bond Interest Cash Governmental Activities: Interest Expense on Long-Term Debt Cash Dr. 3,000 Cr. 3,000 3,000 3,000

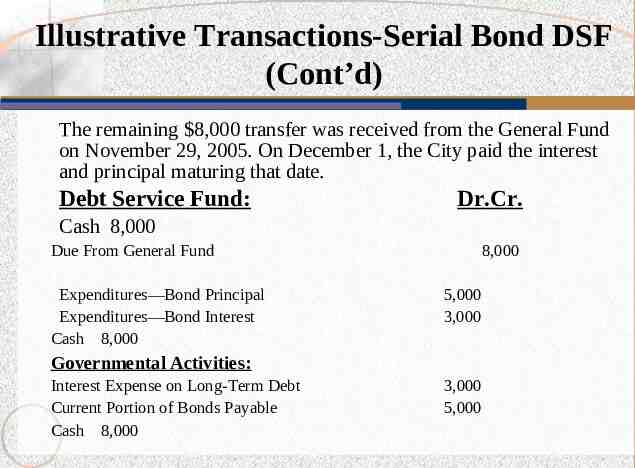

Illustrative Transactions-Serial Bond DSF (Cont’d) The remaining 8,000 transfer was received from the General Fund on November 29, 2005. On December 1, the City paid the interest and principal maturing that date. Debt Service Fund: Dr.Cr. Cash 8,000 Due From General Fund Expenditures—Bond Principal Expenditures—Bond Interest Cash 8,000 8,000 5,000 3,000 Governmental Activities: Interest Expense on Long-Term Debt Current Portion of Bonds Payable Cash 8,000 3,000 5,000

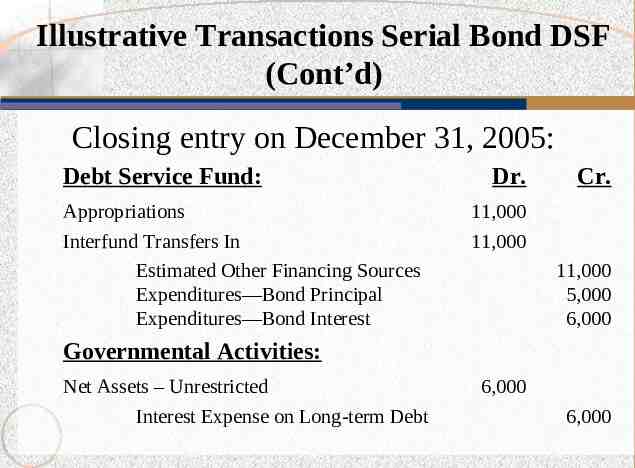

Illustrative Transactions Serial Bond DSF (Cont’d) Closing entry on December 31, 2005: Debt Service Fund: Appropriations Interfund Transfers In Estimated Other Financing Sources Expenditures—Bond Principal Expenditures—Bond Interest Dr. Cr. 11,000 11,000 11,000 5,000 6,000 Governmental Activities: Net Assets – Unrestricted Interest Expense on Long-term Debt 6,000 6,000

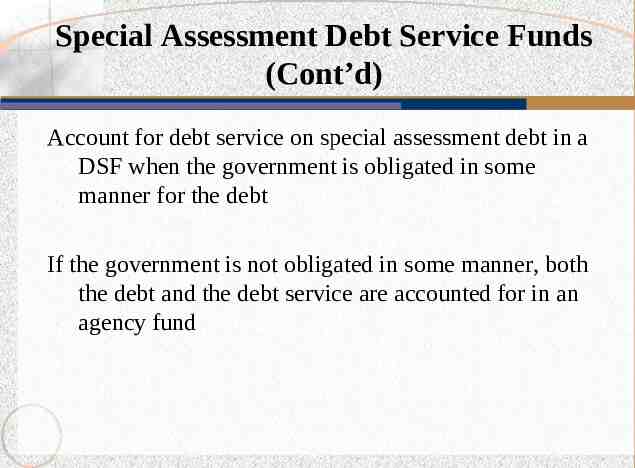

Special Assessment Debt Service Funds (Cont’d) Account for debt service on special assessment debt in a DSF when the government is obligated in some manner for the debt If the government is not obligated in some manner, both the debt and the debt service are accounted for in an agency fund

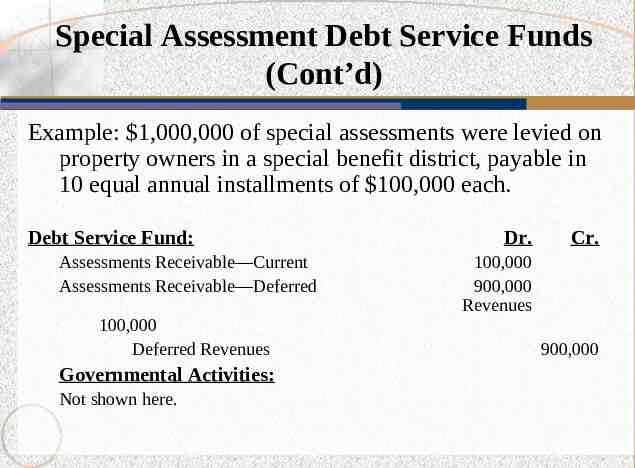

Special Assessment Debt Service Funds (Cont’d) Example: 1,000,000 of special assessments were levied on property owners in a special benefit district, payable in 10 equal annual installments of 100,000 each. Debt Service Fund: Assessments Receivable—Current Assessments Receivable—Deferred 100,000 Deferred Revenues Governmental Activities: Not shown here. Dr. Cr. 100,000 900,000 Revenues 900,000

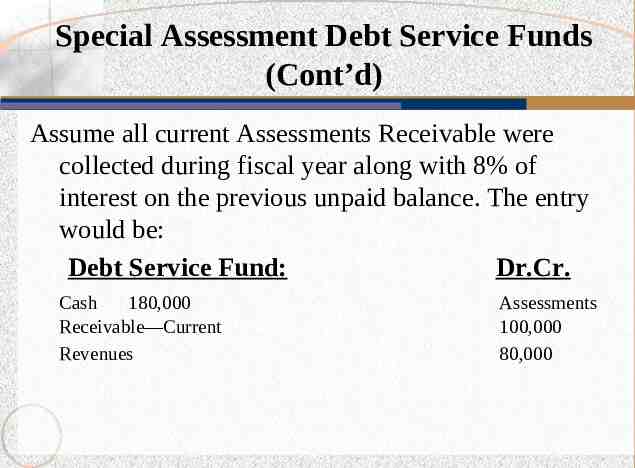

Special Assessment Debt Service Funds (Cont’d) Assume all current Assessments Receivable were collected during fiscal year along with 8% of interest on the previous unpaid balance. The entry would be: Debt Service Fund: Dr.Cr. Cash 180,000 Receivable—Current Revenues Assessments 100,000 80,000

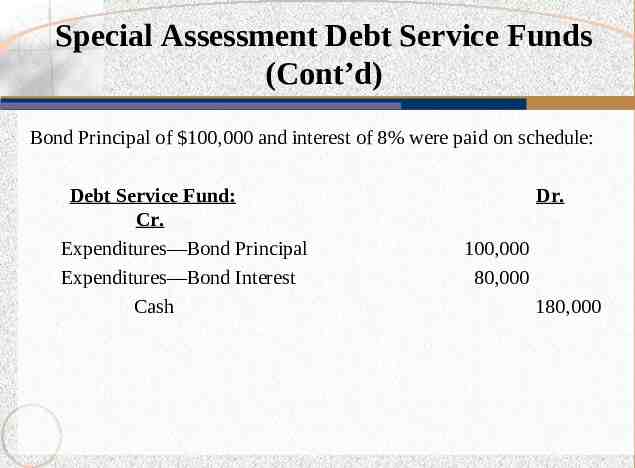

Special Assessment Debt Service Funds (Cont’d) Bond Principal of 100,000 and interest of 8% were paid on schedule: Debt Service Fund: Cr. Expenditures—Bond Principal Expenditures—Bond Interest Cash Dr. 100,000 80,000 180,000

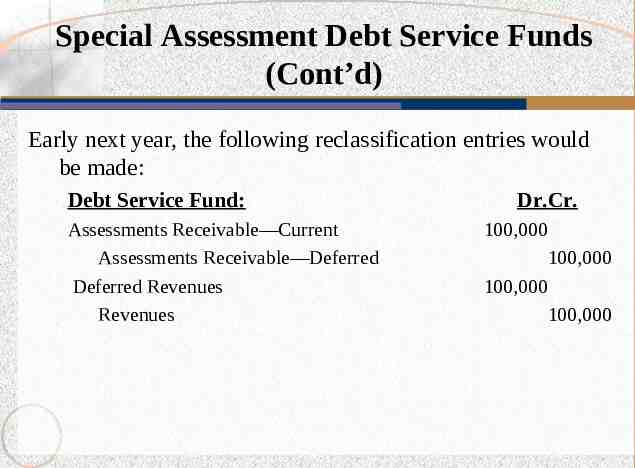

Special Assessment Debt Service Funds (Cont’d) Early next year, the following reclassification entries would be made: Debt Service Fund: Assessments Receivable—Current Assessments Receivable—Deferred Deferred Revenues Revenues Dr.Cr. 100,000 100,000 100,000 100,000

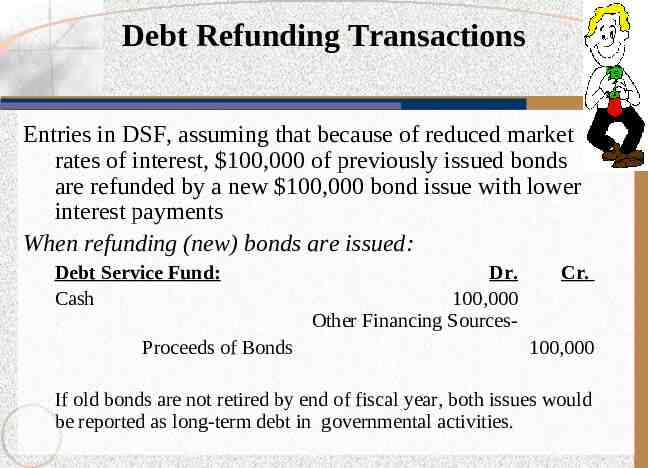

Debt Refunding Transactions Entries in DSF, assuming that because of reduced market rates of interest, 100,000 of previously issued bonds are refunded by a new 100,000 bond issue with lower interest payments When refunding (new) bonds are issued: Debt Service Fund: Cash Proceeds of Bonds Dr. 100,000 Other Financing Sources- Cr. 100,000 If old bonds are not retired by end of fiscal year, both issues would be reported as long-term debt in governmental activities.

Debt Refunding Transactions (Cont’d) Assuming old bonds are retired shortly after issue of refunding bonds Debt Service Fund: Cr. Other Financing Uses— Refunded Bonds Cash 100,000 Dr. 100,000 (Note: Report only the new issue as debt in governmental activities)