Tri-annual Review (TAR) and The Audit Relationship

34 Slides7.03 MB

Tri-annual Review (TAR) and The Audit Relationship

Agenda Introduction Goals and Objectives Importance Regulatory Alignment FMR specifics Tri-Annual Review and the Audit Relationship Take Away Application and Tips stmichaelsinc.com 2017 2

Introduction stmichaelsinc.com 2017 3

Goals and Objectives At the conclusion of this hour each participant should be able to: Discuss the importance of Tri-Annual Review or Joint Review Program Discuss Tri-Annual Review and other regulatory relationships Discuss conceptually how a Tri-Annual Review is conducted Discuss how it ties to a Independent Auditor’s assessment Have concepts you can take away and implement at home station stmichaelsinc.com 2017 4

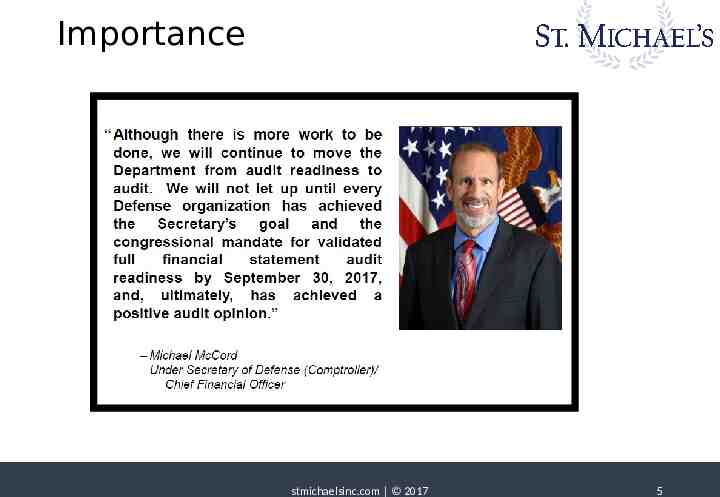

Importance stmichaelsinc.com 2017 5

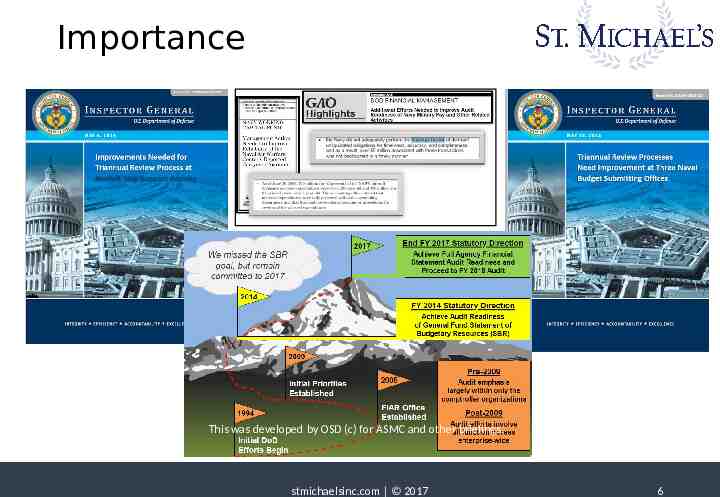

Importance This was developed by OSD (c) for ASMC and other briefings. stmichaelsinc.com 2017 6

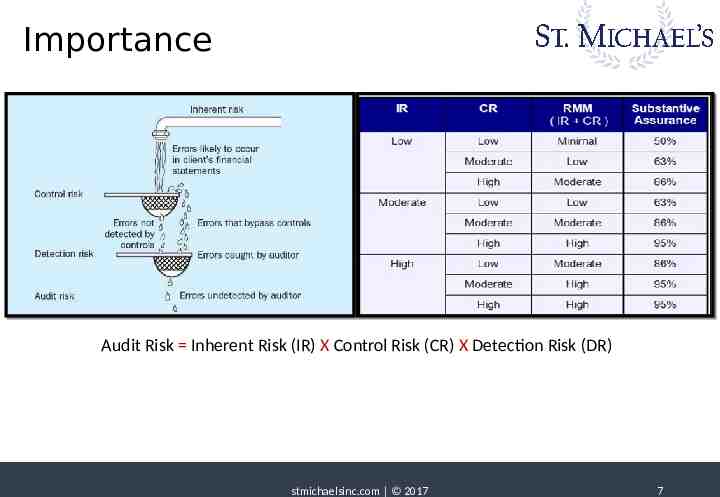

Importance Audit Risk Inherent Risk (IR) X Control Risk (CR) X Detection Risk (DR) stmichaelsinc.com 2017 7

Importance Senior Leadership Regulatory Audit Good use of Taxpayers Funds stmichaelsinc.com 2017 8

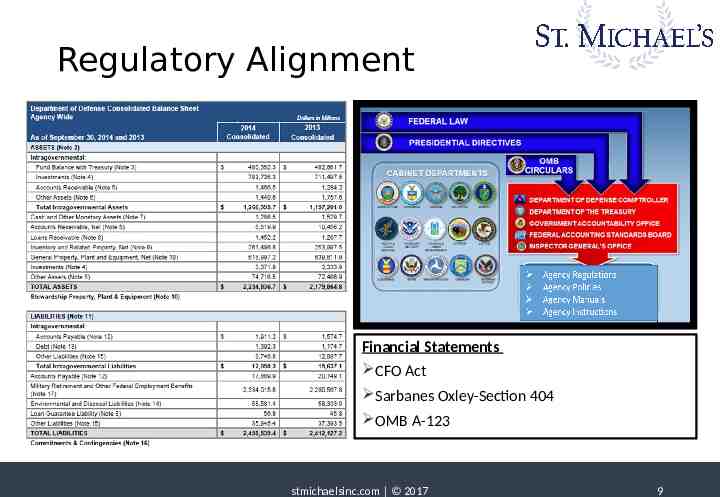

Regulatory Alignment Financial Statements CFO Act Sarbanes Oxley-Section 404 OMB A-123 stmichaelsinc.com 2017 9

FMR Specifics DoD 7000.14-R, Financial Management Regulation, Volume 3, Chapter 8 Standards for Recording and Reviewing Commitments and Obligations Section 0804 Triannual Review of Commitments, Obligations, Accounts Payable and Accounts Receivable Internal Control Process to validate Bona Fide Needs of Appropriations charged Internal Control Process to ensure compliance with United States General Ledger Standard Financial Information Structure Transaction Library Internal Control Process to ensure Commitments, Obligations, Expenditures are valid and accurate stmichaelsinc.com 2017 10

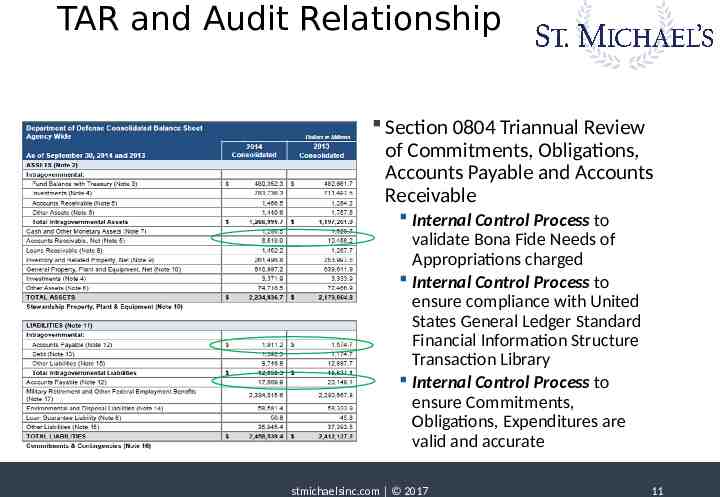

TAR and Audit Relationship Section 0804 Triannual Review of Commitments, Obligations, Accounts Payable and Accounts Receivable Internal Control Process to validate Bona Fide Needs of Appropriations charged Internal Control Process to ensure compliance with United States General Ledger Standard Financial Information Structure Transaction Library Internal Control Process to ensure Commitments, Obligations, Expenditures are valid and accurate stmichaelsinc.com 2017 11

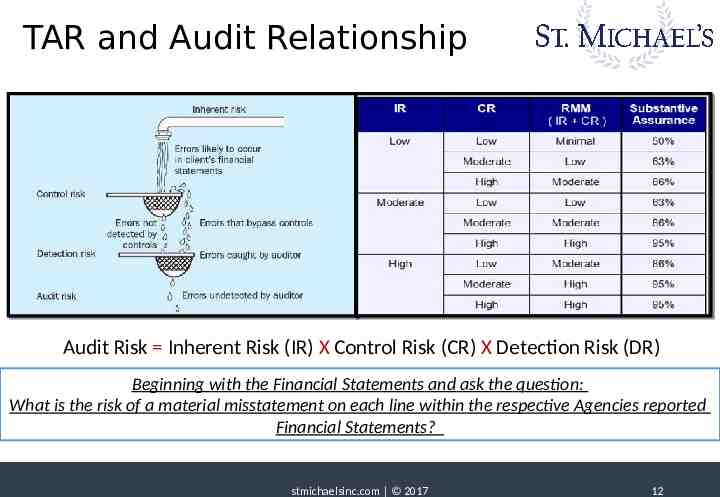

TAR and Audit Relationship Audit Risk Inherent Risk (IR) X Control Risk (CR) X Detection Risk (DR) Beginning with the Financial Statements and ask the question: What is the risk of a material misstatement on each line within the respective Agencies reported Financial Statements? stmichaelsinc.com 2017 12

TAR and Audit Relationship Financial Audit Manual Government Audit Standards stmichaelsinc.com 2017 13

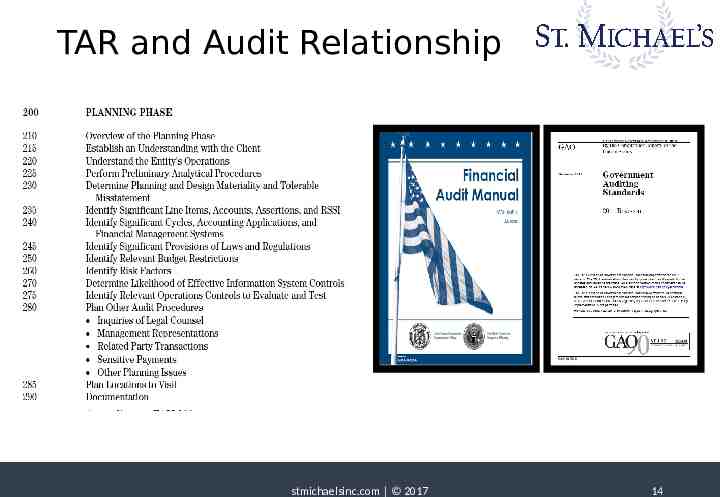

TAR and Audit Relationship stmichaelsinc.com 2017 14

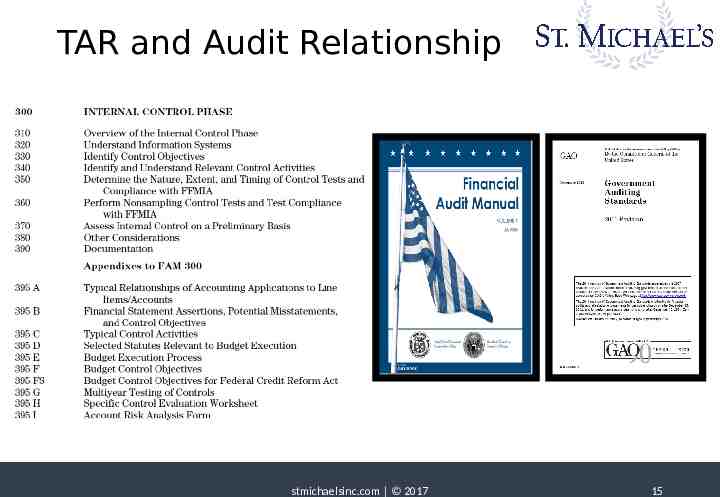

TAR and Audit Relationship stmichaelsinc.com 2017 15

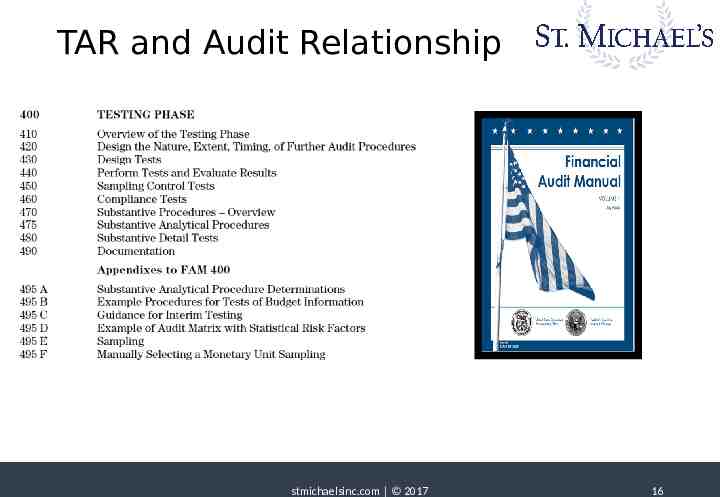

TAR and Audit Relationship stmichaelsinc.com 2017 16

TAR and Audit Relationship This was developed by OSD (c) for ASMC and other briefings. stmichaelsinc.com 2017 17

Importance Senior Leadership Regulatory Audit Good use of Taxpayers Funds Help in current year and with other re-programming needs stmichaelsinc.com 2017 18

St. Michael’s Experience Relationships are Key Commander Funds Holder Contracting Officer (Warranted 1102) Contracting Officer’s Technical Representative Program Manager (Govt) Program Manager (Contractor) Task Order Leadership (Govt) DFAS Most have a policy, but not Agency specific Some have instructions or a SOPs, but very few outside the financial shop have seen it (even fewer know how it works) Every 90 days something is done – but is it the same? Are the same people involved? stmichaelsinc.com 2017 19

St. Michael’s Experience Step 1: Establish a single point of contact to be your Triannual or Joint review person or additional duty Step 2: Draft your awareness campaign (and why it’s important), Agency policy, conduct an end-to-end work flow diagram with swim lanes (relationships), and begin organizational change (ADKAR) Step 3: Circulate your draft amongst key relationships (swim lanes) and seek input (relationships); ADKAR Step 4: Establish Commander/Director Memorandum of Understanding (MOU) with those offices in the flow diagram/swim lanes; continue ADKAR stmichaelsinc.com 2017 20

St. Michael’s Experience Step 5: ADKAR moves to the forefront and training program begins Step 6: Execute policy and instructions through quarterly scheduled reviews. Place TAR onto the Command Calendar for the next 24 months Step 7: Conduct AAR with those in the end-to-end flow diagram, make improvements, adjust policy, instructions, and SOPs. Step 8: Move from K to building A Step 9: Seek out your R and begin to control/solidify your processes (Automation-ADOBE-Dashboards) stmichaelsinc.com 2017 21

Additional Tips That Work Current OSD March 2016 Guidance has some testing requirements Training (Knowledge and Ability) TAR quality assurance review Follow up—Follow up---Follow up Provide examples of acceptable and unacceptable remarks: Remarks must be of a nature that explains specific actions What documentation is obligation waiting on (i.e. receiving report, invoice, etc.) to process payment? Estimated liquidation date (based on input from vendor, DFAS, etc.)? Contact information of the person performing validation, and follow-up if awaiting update/documentation from other organizations stmichaelsinc.com 2017 22

Additional Tips That Work TAR quality assurance review Accountability/Unacceptable remarks: Use those relationships Use the MOUs and Command(U) Some popular vernacular we removed: Simply stating “valid” or “valid per Mr./Ms. Smith” Obligation is still valid / Obligation is to cover XXXX Awaiting final payment OR still researching stmichaelsinc.com 2017 23

Additional Tips That Work Establish an annual plan reviewing ULOs in line with TAR periods Start with oldest FYs and work backwards Review largest dollar amounts Attack amounts less than 1,000 for de-obligation since no MOD is required by contracting Follow-up – Follow-up – Follow-up Adequate documentation Open Lines of Communication Relationships are key collaborate commitments and obligations to determine the validity of the sufficiency funding level to support the bona fide need for the outstanding goods and services stmichaelsinc.com 2017 24

Summary and Review Today we discussed: Tri-Annual Review Importance Tri-Annual Review and other Regulatory Guidance Tri-Annual Review relationship with Independent Auditor’s Assessment Tri-Annual Review Tips stmichaelsinc.com 2017 25

QUESTION S? stmichaelsinc.com 2017 26

St Michael’s TAR Process Backup Slides 05/18/2023 stmichaelsinc.com 2017 27

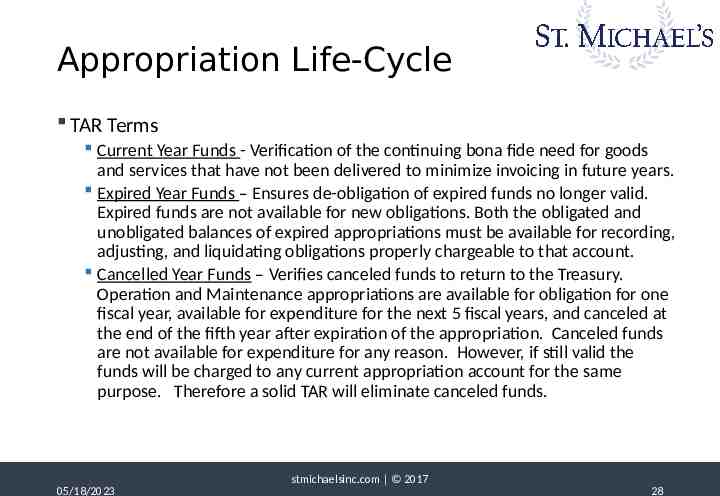

Appropriation Life-Cycle TAR Terms Current Year Funds - Verification of the continuing bona fide need for goods and services that have not been delivered to minimize invoicing in future years. Expired Year Funds – Ensures de-obligation of expired funds no longer valid. Expired funds are not available for new obligations. Both the obligated and unobligated balances of expired appropriations must be available for recording, adjusting, and liquidating obligations properly chargeable to that account. Cancelled Year Funds – Verifies canceled funds to return to the Treasury. Operation and Maintenance appropriations are available for obligation for one fiscal year, available for expenditure for the next 5 fiscal years, and canceled at the end of the fifth year after expiration of the appropriation. Canceled funds are not available for expenditure for any reason. However, if still valid the funds will be charged to any current appropriation account for the same purpose. Therefore a solid TAR will eliminate canceled funds. stmichaelsinc.com 2017 05/18/2023 28

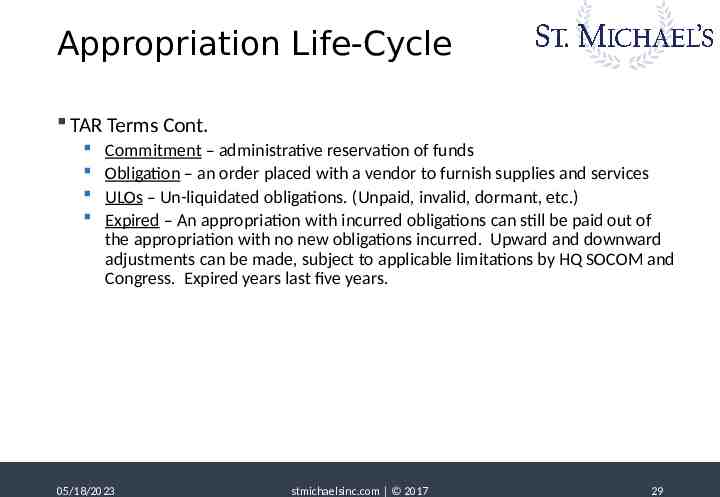

Appropriation Life-Cycle TAR Terms Cont. Commitment – administrative reservation of funds Obligation – an order placed with a vendor to furnish supplies and services ULOs – Un-liquidated obligations. (Unpaid, invalid, dormant, etc.) Expired – An appropriation with incurred obligations can still be paid out of the appropriation with no new obligations incurred. Upward and downward adjustments can be made, subject to applicable limitations by HQ SOCOM and Congress. Expired years last five years. 05/18/2023 stmichaelsinc.com 2017 29

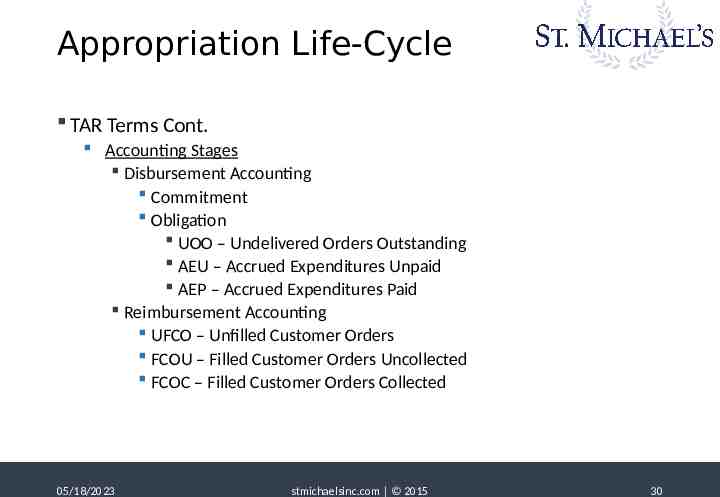

Appropriation Life-Cycle TAR Terms Cont. Accounting Stages Disbursement Accounting Commitment Obligation UOO – Undelivered Orders Outstanding AEU – Accrued Expenditures Unpaid AEP – Accrued Expenditures Paid Reimbursement Accounting UFCO – Unfilled Customer Orders FCOU – Filled Customer Orders Uncollected FCOC – Filled Customer Orders Collected 05/18/2023 stmichaelsinc.com 2015 30

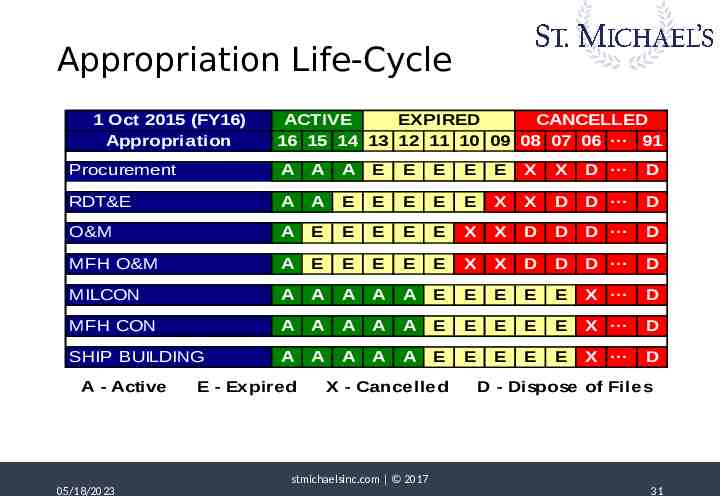

Appropriation Life-Cycle 1 Oct 2015 (FY16) Appropriation ACTIVE EXPIRED CANCELLED 16 15 14 13 12 11 10 09 08 07 06 ··· 91 Procurement A A A E E E E E X X D ··· D RDT&E A A E E E E E X X D D ··· D O&M A E E E E E X X D D D ··· D MFH O&M A E E E E E X X D D D ··· D MILCON A A A A A E E E E E X ··· D MFH CON A A A A A E E E E E X ··· D SHIP BUILDING A A A A A E E E E E X ··· D A - Active E - Expired X - Cancelled D - Dispose of Files stmichaelsinc.com 2017 05/18/2023 31

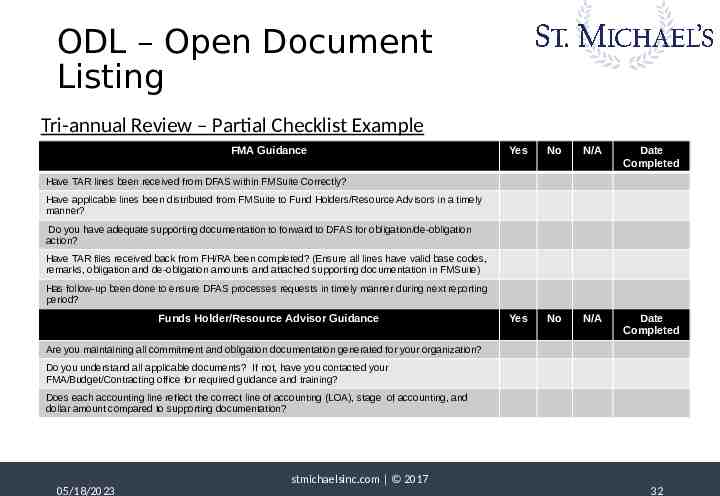

ODL – Open Document Listing Tri-annual Review – Partial Checklist Example FMA Guidance Yes No N/A Date Completed Yes No N/A Date Completed Have TAR lines been received from DFAS within FMSuite Correctly? Have applicable lines been distributed from FMSuite to Fund Holders/Resource Advisors in a timely manner? Do you have adequate supporting documentation to forward to DFAS for obligation/de-obligation action? Have TAR files received back from FH/RA been completed? (Ensure all lines have valid base codes, remarks, obligation and de-obligation amounts and attached supporting documentation in FMSuite) Has follow-up been done to ensure DFAS processes requests in timely manner during next reporting period? Funds Holder/Resource Advisor Guidance Are you maintaining all commitment and obligation documentation generated for your organization? Do you understand all applicable documents? If not, have you contacted your FMA/Budget/Contracting office for required guidance and training? Does each accounting line reflect the correct line of accounting (LOA), stage of accounting, and dollar amount compared to supporting documentation? stmichaelsinc.com 2017 05/18/2023 32

TAR Guidance FMR – DoD Financial Management Regulation 7000.14-R, Vol 3, Chap 8 and DFAS-DE 7220.4-G DoD’s Goal – Increase DoD’s ability to use available appropriations before they expire and ensure remaining open obligations are valid and liquidated before the cancellation of the appropriation. Tri-Annual Review (TAR) Requirements – All commitments and obligations shall be reviewed, whether current or dormant, at least annually in order to substantiate the year-end certification requirements. TAR Reporting Periods Oct-Jan - all canceling funds Feb-May - all expired funds Jun-Sep - all current funds 05/18/2023 stmichaelsinc.com 2017 33

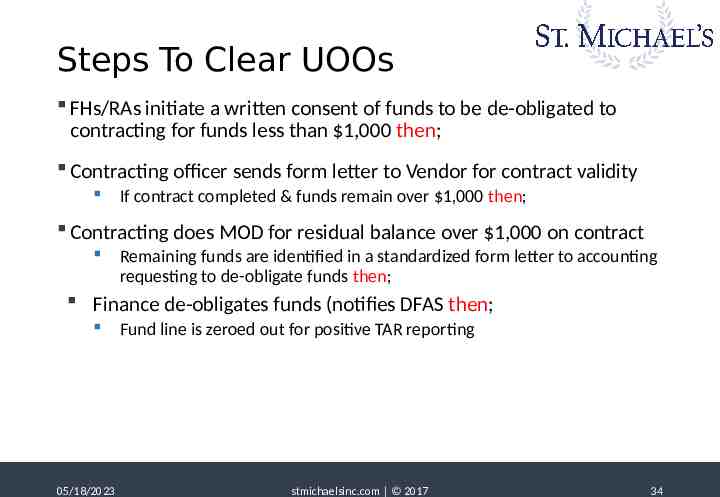

Steps To Clear UOOs FHs/RAs initiate a written consent of funds to be de-obligated to contracting for funds less than 1,000 then; Contracting officer sends form letter to Vendor for contract validity If contract completed & funds remain over 1,000 then; Contracting does MOD for residual balance over 1,000 on contract Remaining funds are identified in a standardized form letter to accounting requesting to de-obligate funds then; Finance de-obligates funds (notifies DFAS then; 05/18/2023 Fund line is zeroed out for positive TAR reporting stmichaelsinc.com 2017 34