SBA 504 Lending Zions Bank Peter J. Morgan, Executive Vice President 1

15 Slides237.00 KB

SBA 504 Lending Zions Bank Peter J. Morgan, Executive Vice President 1

Zions Bank Statistics - 2006 New SBA 504 fundings 600 million Average loan Size 750K 1st mortgage loan size 100K to 8M Average loan-to-value (LTV) 54% Nationwide market 50 states Industries 100 2

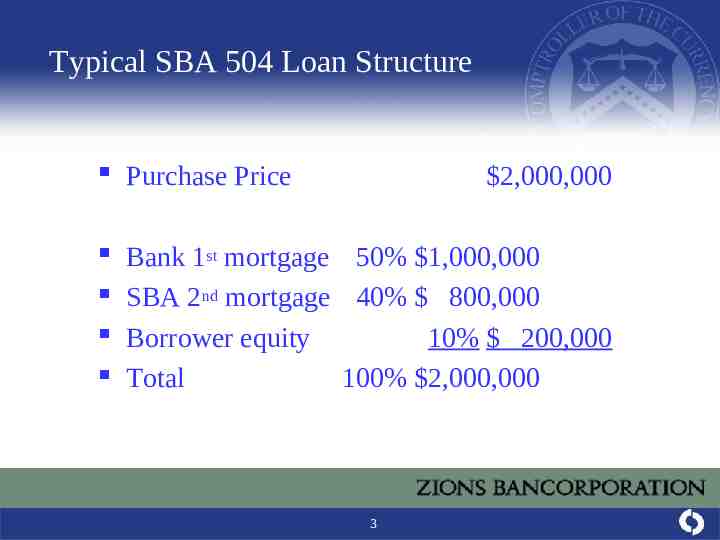

Typical SBA 504 Loan Structure Purchase Price Bank 1st mortgage 50% 1,000,000 SBA 2nd mortgage 40% 800,000 Borrower equity 10% 200,000 Total 100% 2,000,000 2,000,000 3

Loan Terms & Structure Bank 1st Mortgage: SBA 504 Debenture: Generally 50% or more of project costs; cannot be less than SBA 504 loan No limit on amount of loan Term must be at least half that of the SBA 504 loan 20 and 25 year maturity common, some 30 years Amount and rates can be modified w/ SBA consent 4 Generally 40% of eligible project costs; 35% if special use or start-up, 30% if both. Term & maturity, 10 or 20 yrs No balloon payments or calls Loan cannot be added to or modified after closing Can subordinate to new 1st mortgage

Variety of Property Types Generally multi-purpose Office, warehouse, office/warehouse mix, light industrial, retail, manufacturing, freezer/cold storage, medical or dental office & clinics More special-use Auto/motorcycle/boat dealer, pre-school, hotels/motel, restaurant, banquet/reception center, veterinary clinic, day-care, funeral home, auto repair, bowling center, health club/gym, gas station/c-store, car wash, golf course, assisted living center, grocery store, theater, marina, amusement park, etc. 5

Zions Bank 504 Portfolio by Property Type 14% 2% 32% 7% 6% 13% 4% 19% 3% 6 Off/Whse Hotels GS/C-store Medical Office Restaurant Retail Manufacturing Other

Best SBA 504 Prospects Small companies experiencing rapid growth Small business that is out of space and wants to graduate from a lease to building ownership Leasing with option to purchase building Expanding to or opening second location Things to expect if Rapid growth, business may only show ability to service proposed debt in last 12-18 months Start-up, prior industry experience is crucial 10% down payment, higher leverage and debt/worth, consider overall financial strength of total package 7

Zions SBA 504 Marketing Branch network with managers & loan officers trained and familiar with SBA loan programs Small business Business Development Office calling network focusing on SBA loan opportunities Excellent relationship with every Certified Development Corporation (CDC) in our multi-state market footprint Equal bonus and incentive structure for loan officers Individual goals for minimum SBA volume 8

Bank Benefits of SBA 504 Program Participation Loan-to-value ratio 50%, with lower probability of loss if default May tolerate higher default risk Can finance larger projects Ability to finance multiple projects Diversify project financing risk Secondary market liquidity Premium and/or fee income Community Reinvestment Act (CRA) Credit 9

Loan Pricing & Fees Bank 1st Mortgage: SBA 504 Debenture: Variable repricing monthly, quarterly, or annually indexed to Prime, Commercial Paper or LIBOR Fixed rates for 5 -10 yrs (or full loan term) indexed to LIBOR, Fed Home Loan Bank, US Treasury, etc. Typical 1% origination fee, with possible interim loan fee 10 20 yr fixed rate indexed to 10 yr US Treasury yield Origination fees 2.75%, grossed up and included in loan amount One-time lender fee due SBA equal to .5% of 1st Mtg

Interim Loan Closing Mirror approval figures with CDC/SBA Close in accordance with SBA Authorization Include construction or interim financing for SBA debenture One note w/ pay down or two separate notes 11 Allow adequate time for interim loan (3-12 months) Notify CDC when project is complete and loan fully disbursed Follow-up to verify borrower closes its loan with the CDC

Zions Bank First Mortgage Loan History Slightly higher probability of default, however, lower losses in the event of default Delinquency rate of approx 1% Classified special mention, or substandard, 2-3% Principal loss rate of 10 bps (.10%) If default and trustee sale, SBA usually protects its 2nd lien and buys out the bank lender on newer multi-purpose properties w/equity, however, will rarely bid if special use or the equity is deemed insufficient. 12

Secondary Market Benefits Referring lender keeps applicable loans fees plus premium Expand geographic markets Manage commercial real estate or industry concentrations Multiple loans to same borrower Finance expansions, start-ups, and higher risk industries High fee income with no credit risk Liquidity management 13

SBA 504 1st Mortgage Secondary Market Example Purchase Price 2.0 million (40,000 sf office/whs bldg) Bank First Mortgage Interest Rate 1.0 million (50% LTC/LTV) 7.98% (FHLB 2.75) (fixed for 5 yrs, reprices every 5 yrs) Maturity & Amortization Prepayment Penalty 25 years flat 5% 5 yrs, 5%,.1% after 4% Premium to Bank 1% Loan Fee 40,000 10,000 - 5,000 45,000 Less SBA .5% fee Total Income to Bank 14

Vibrant Secondary Market SBA 504 First Mortgage Loans 1. 2. 3. 4. 5. 6. In 2006, approximately 7.0 billion in new first mortgage loans funded in connection with SBA 504 program, with approximately 840 million, or 12% sold into secondary market Average net interest spread approximately 3.00% Prepayment penalties (“PPP”): 50% flat 5% for 5 yrs, 30% declining 5 yrs 5,4,3,2,1%, 20% declining 10 yrs (10,9.2,1%) Average premium paid 5% ( 35 million paid in ’06) Average origination fee 1% Use PPP, interest rate, loan fees to maximize income 15