Planning for the Future “Life after Graduation”

46 Slides126.00 KB

Planning for the Future “Life after Graduation”

Introductions John McMillan- Lawyer Darren Farwell - Scotia Mcleod Maria Tsiaousidis – Manager Personal Banking. Jim Blair – Snr Manager Toronto Region BNS Graham Flanagan – Centre Manager Q& M

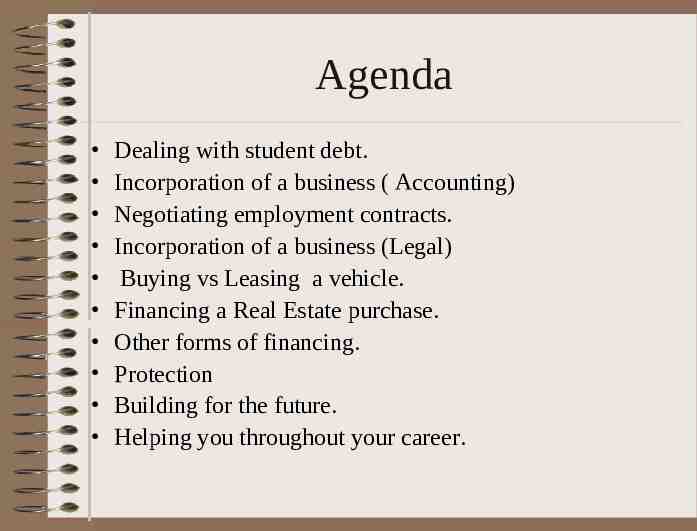

Agenda Dealing with student debt. Incorporation of a business ( Accounting) Negotiating employment contracts. Incorporation of a business (Legal) Buying vs Leasing a vehicle. Financing a Real Estate purchase. Other forms of financing. Protection Building for the future. Helping you throughout your career.

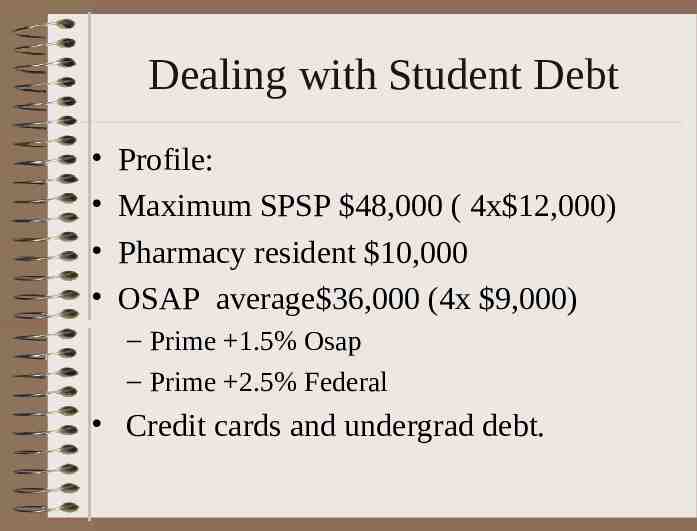

Dealing with Student Debt Profile: Maximum SPSP 48,000 ( 4x 12,000) Pharmacy resident 10,000 OSAP average 36,000 (4x 9,000) – Prime 1.5% Osap – Prime 2.5% Federal Credit cards and undergrad debt.

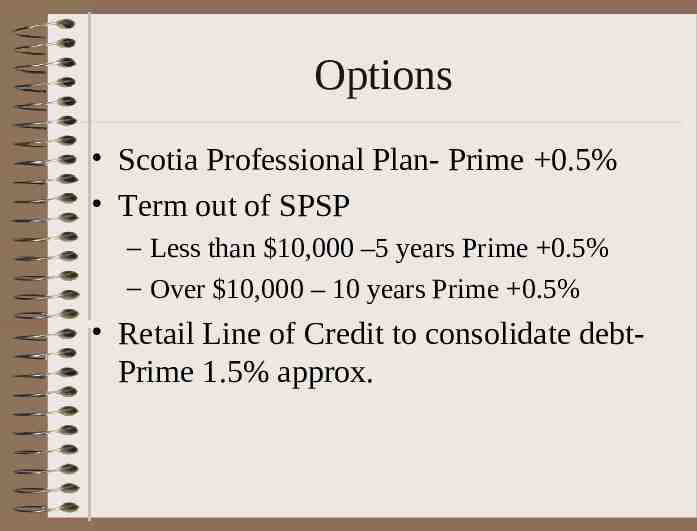

Options Scotia Professional Plan- Prime 0.5% Term out of SPSP – Less than 10,000 –5 years Prime 0.5% – Over 10,000 – 10 years Prime 0.5% Retail Line of Credit to consolidate debtPrime 1.5% approx.

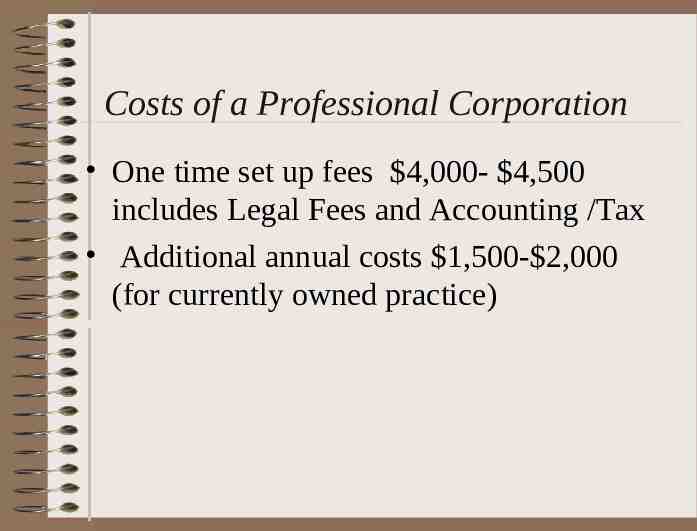

Costs of a Professional Corporation One time set up fees 4,000- 4,500 includes Legal Fees and Accounting /Tax Additional annual costs 1,500- 2,000 (for currently owned practice)

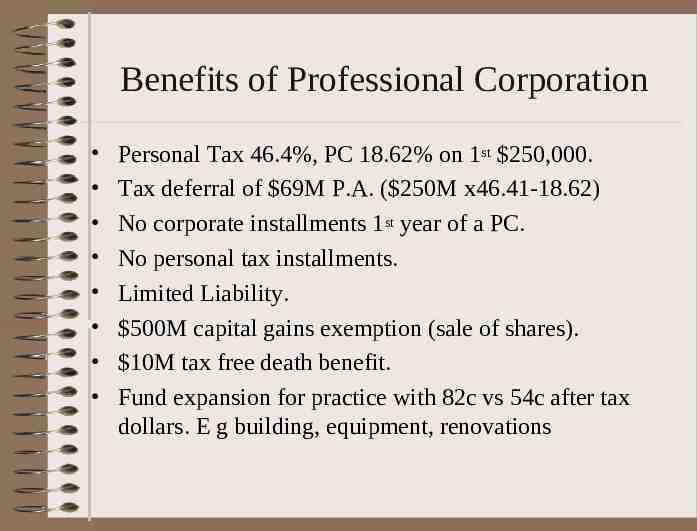

Benefits of Professional Corporation Personal Tax 46.4%, PC 18.62% on 1st 250,000. Tax deferral of 69M P.A. ( 250M x46.41-18.62) No corporate installments 1st year of a PC. No personal tax installments. Limited Liability. 500M capital gains exemption (sale of shares). 10M tax free death benefit. Fund expansion for practice with 82c vs 54c after tax dollars. E g building, equipment, renovations

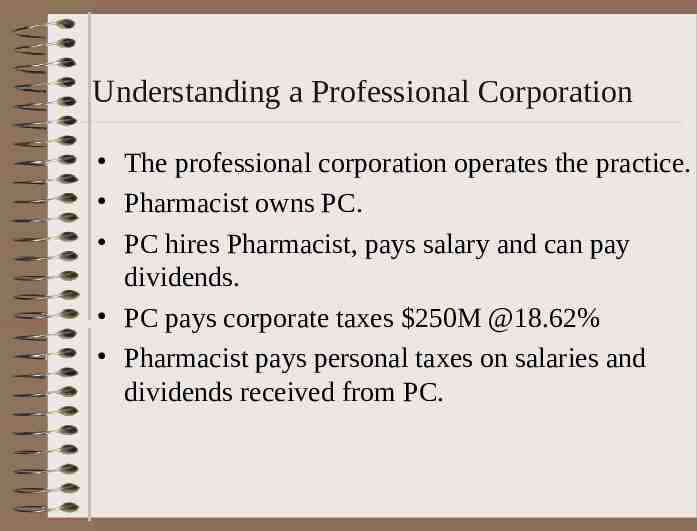

Understanding a Professional Corporation The professional corporation operates the practice. Pharmacist owns PC. PC hires Pharmacist, pays salary and can pay dividends. PC pays corporate taxes 250M @18.62% Pharmacist pays personal taxes on salaries and dividends received from PC.

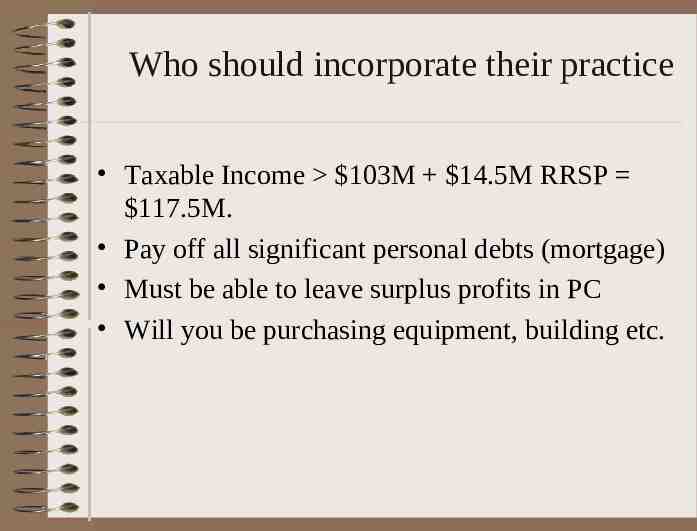

Who should incorporate their practice Taxable Income 103M 14.5M RRSP 117.5M. Pay off all significant personal debts (mortgage) Must be able to leave surplus profits in PC Will you be purchasing equipment, building etc.

LEGAL ISSUES FOR PHARMACISTS John McMillan, LL.B. 416 364 4771 [email protected]

RETAIL Large Chains Employment “Associate Owner” (Shoppers Drug Mart) Franchise Employment Agreements largely uniform

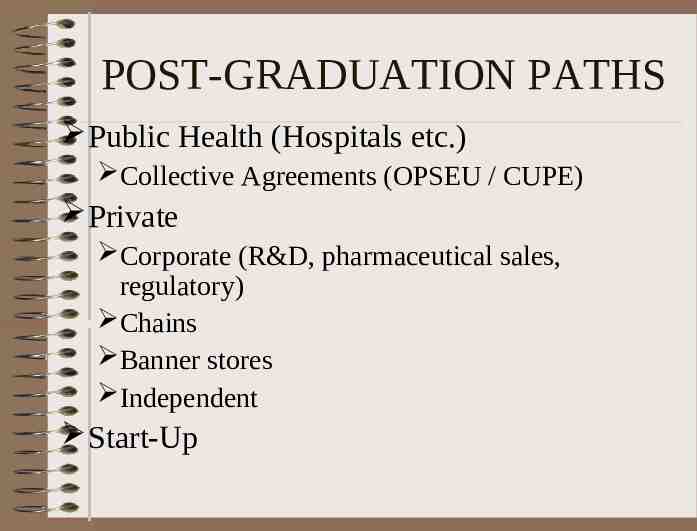

POST-GRADUATION PATHS Public Health (Hospitals etc.) Collective Agreements (OPSEU / CUPE) Private Corporate (R&D, pharmaceutical sales, regulatory) Chains Banner stores Independent Start-Up

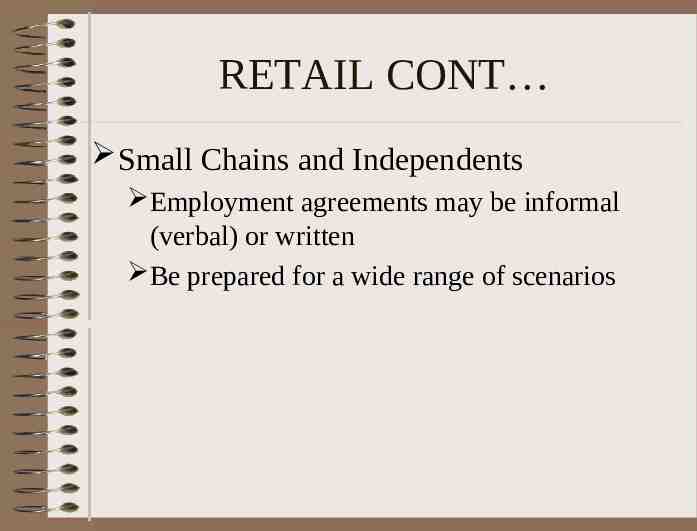

RETAIL CONT Small Chains and Independents Employment agreements may be informal (verbal) or written Be prepared for a wide range of scenarios

EMPLOYMENT AGREEMENTS Most common arrangement for new graduates Written agreements on the increase Heavy competition between employers Written Agreements instrumental in communicating incentives to potential employees Written Agreement also used to secure certain terms for the benefit of the employer

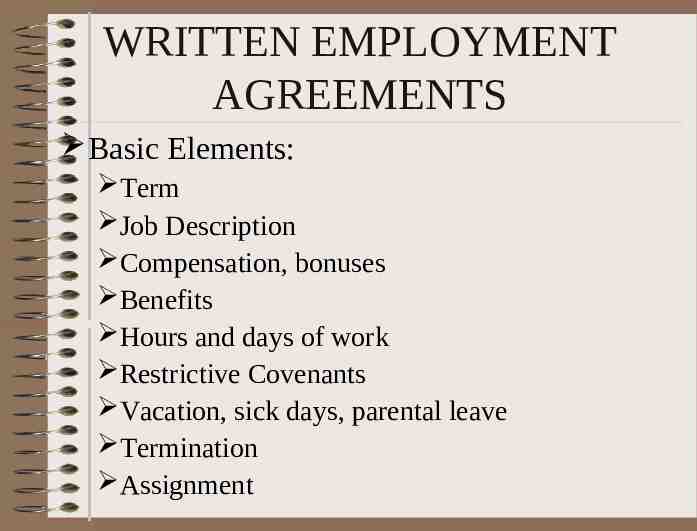

WRITTEN EMPLOYMENT AGREEMENTS Basic Elements: Term Job Description Compensation, bonuses Benefits Hours and days of work Restrictive Covenants Vacation, sick days, parental leave Termination Assignment

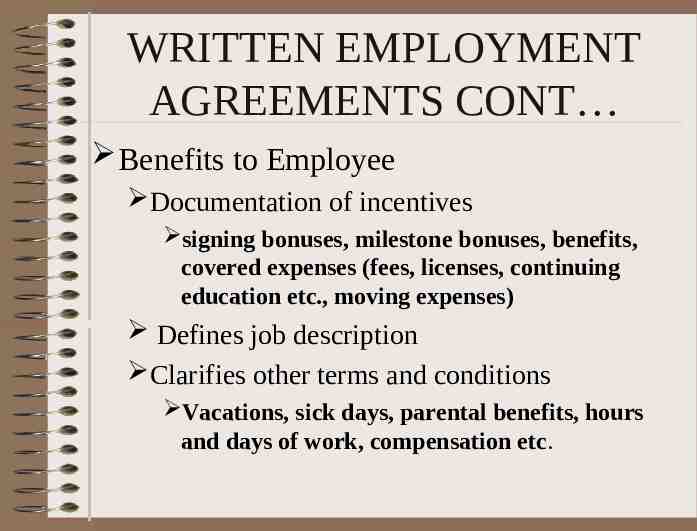

WRITTEN EMPLOYMENT AGREEMENTS CONT Benefits to Employee Documentation of incentives signing bonuses, milestone bonuses, benefits, covered expenses (fees, licenses, continuing education etc., moving expenses) Defines job description Clarifies other terms and conditions Vacations, sick days, parental benefits, hours and days of work, compensation etc.

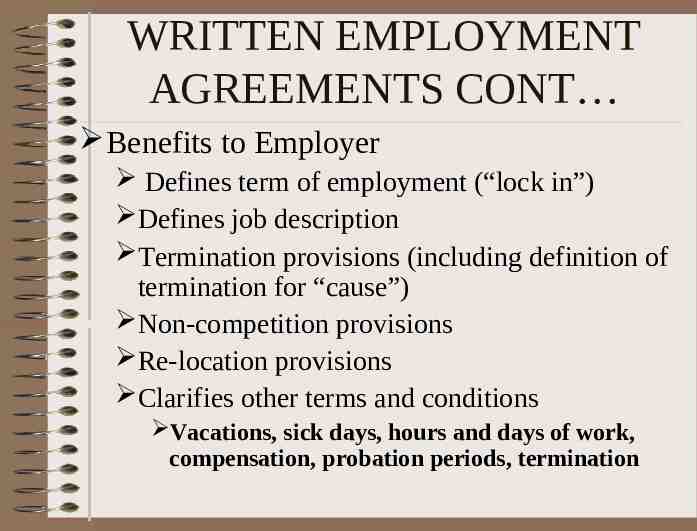

WRITTEN EMPLOYMENT AGREEMENTS CONT Benefits to Employer Defines term of employment (“lock in”) Defines job description Termination provisions (including definition of termination for “cause”) Non-competition provisions Re-location provisions Clarifies other terms and conditions Vacations, sick days, hours and days of work, compensation, probation periods, termination

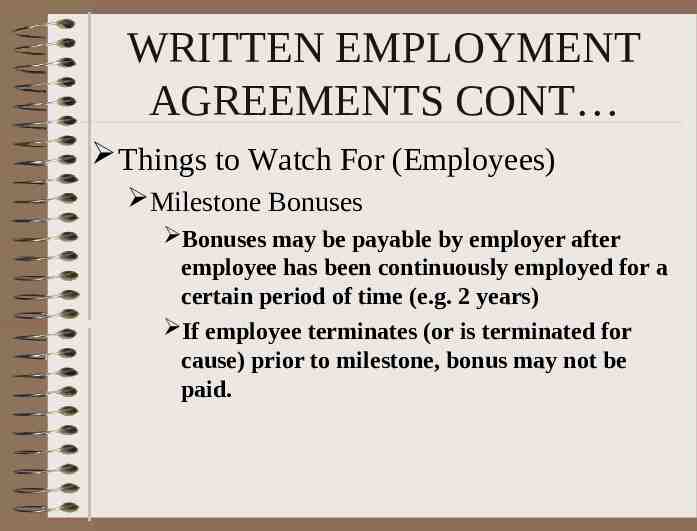

WRITTEN EMPLOYMENT AGREEMENTS CONT Things to Watch For (Employees) Milestone Bonuses Bonuses may be payable by employer after employee has been continuously employed for a certain period of time (e.g. 2 years) If employee terminates (or is terminated for cause) prior to milestone, bonus may not be paid.

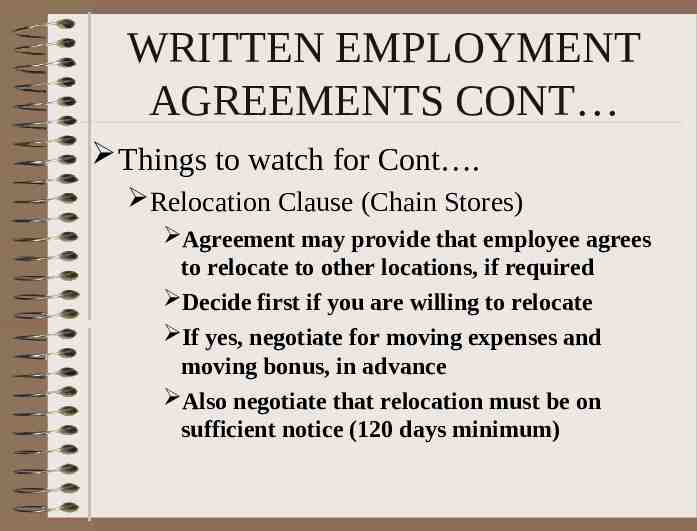

WRITTEN EMPLOYMENT AGREEMENTS CONT Things to watch for Cont . Relocation Clause (Chain Stores) Agreement may provide that employee agrees to relocate to other locations, if required Decide first if you are willing to relocate If yes, negotiate for moving expenses and moving bonus, in advance Also negotiate that relocation must be on sufficient notice (120 days minimum)

WRITTEN EMPLOYMENT AGREEMENTS CONT Things to watch for Cont . Fixed term agreements Protections contained in Employment Standards Act and the common law principle of “reasonable notice” do not apply if there is clear and explicit language to establish a fixed term contract (Ontario Court of Appeal) Note: Employment without written agreement governed by Employment Standards Act and common law Prescribes notice periods for termination

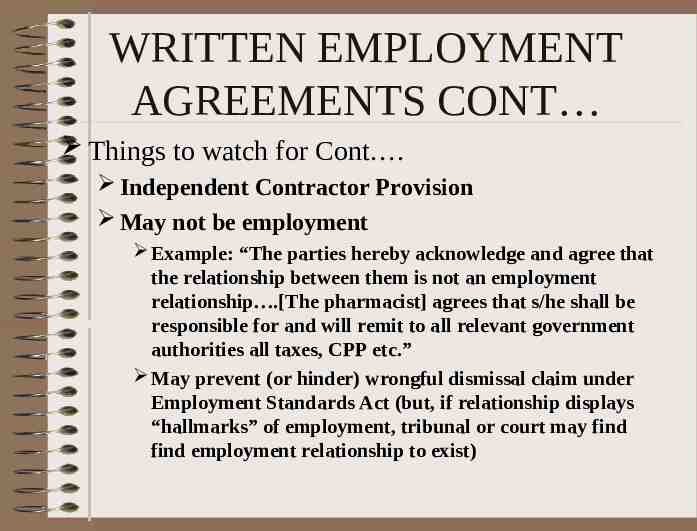

WRITTEN EMPLOYMENT AGREEMENTS CONT Things to watch for Cont . Independent Contractor Provision May not be employment Example: “The parties hereby acknowledge and agree that the relationship between them is not an employment relationship .[The pharmacist] agrees that s/he shall be responsible for and will remit to all relevant government authorities all taxes, CPP etc.” May prevent (or hinder) wrongful dismissal claim under Employment Standards Act (but, if relationship displays “hallmarks” of employment, tribunal or court may find find employment relationship to exist)

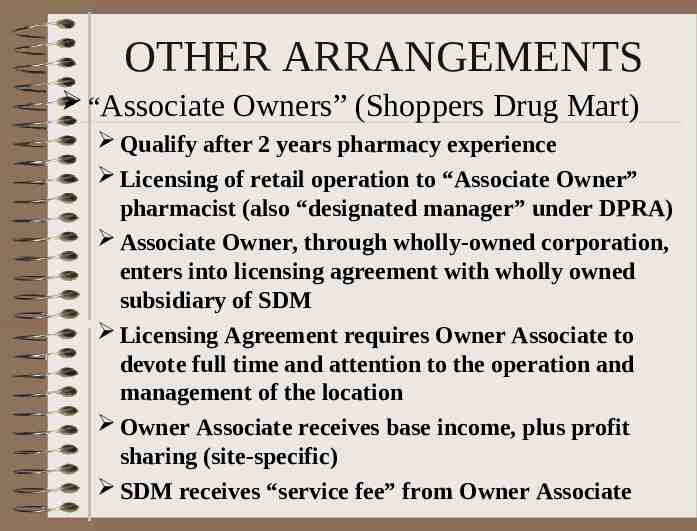

OTHER ARRANGEMENTS “Associate Owners” (Shoppers Drug Mart) Qualify after 2 years pharmacy experience Licensing of retail operation to “Associate Owner” pharmacist (also “designated manager” under DPRA) Associate Owner, through wholly-owned corporation, enters into licensing agreement with wholly owned subsidiary of SDM Licensing Agreement requires Owner Associate to devote full time and attention to the operation and management of the location Owner Associate receives base income, plus profit sharing (site-specific) SDM receives “service fee” from Owner Associate

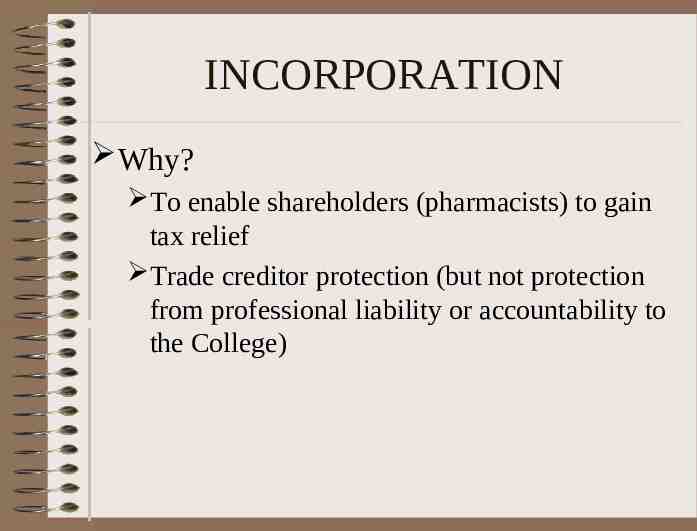

INCORPORATION Why? To enable shareholders (pharmacists) to gain tax relief Trade creditor protection (but not protection from professional liability or accountability to the College)

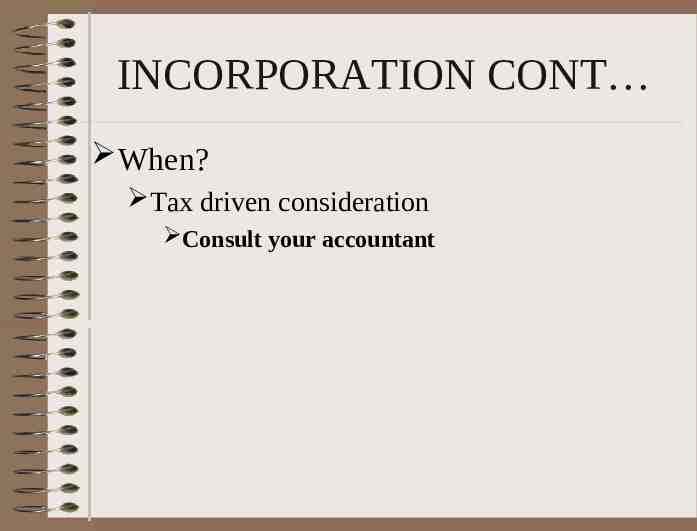

INCORPORATION CONT When? Tax driven consideration Consult your accountant

INCORPORATION CONT Compliant Ownership Structure (Regular Corporation) 51% (or more) held directly by pharmacist or by “J. Smith Pharmacist Professional Corporation” 49% (or less) held by nonpharmacist, family member or holding company Non-Compliant Ownership Structure (Regular Corporation) 51% held by #’ed corporation wholly owned by pharmacist 49% held by nonpharmacist, family member or holding company

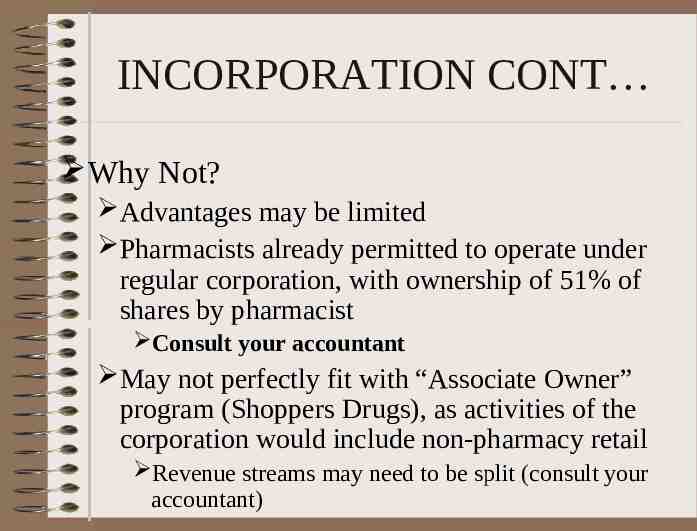

INCORPORATION CONT Why Not? Advantages may be limited Pharmacists already permitted to operate under regular corporation, with ownership of 51% of shares by pharmacist Consult your accountant May not perfectly fit with “Associate Owner” program (Shoppers Drugs), as activities of the corporation would include non-pharmacy retail Revenue streams may need to be split (consult your accountant)

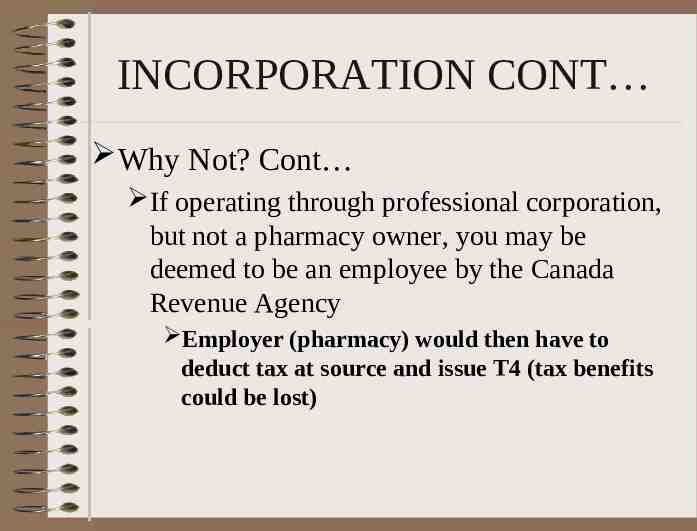

INCORPORATION CONT Why Not? Cont If operating through professional corporation, but not a pharmacy owner, you may be deemed to be an employee by the Canada Revenue Agency Employer (pharmacy) would then have to deduct tax at source and issue T4 (tax benefits could be lost)

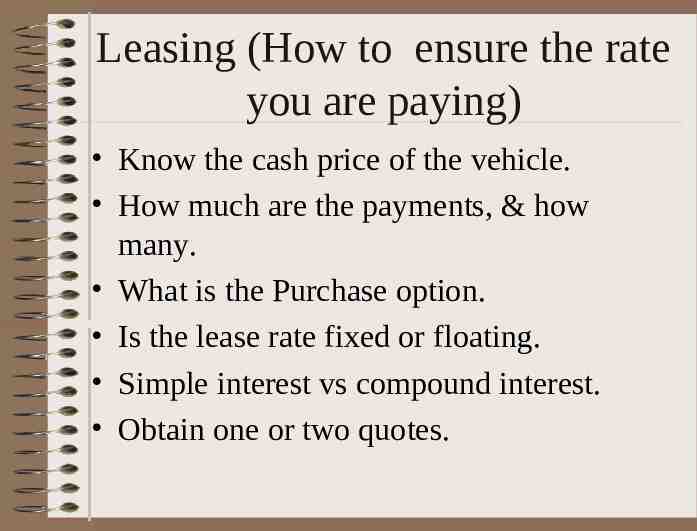

Leasing (How to ensure the rate you are paying) Know the cash price of the vehicle. How much are the payments, & how many. What is the Purchase option. Is the lease rate fixed or floating. Simple interest vs compound interest. Obtain one or two quotes.

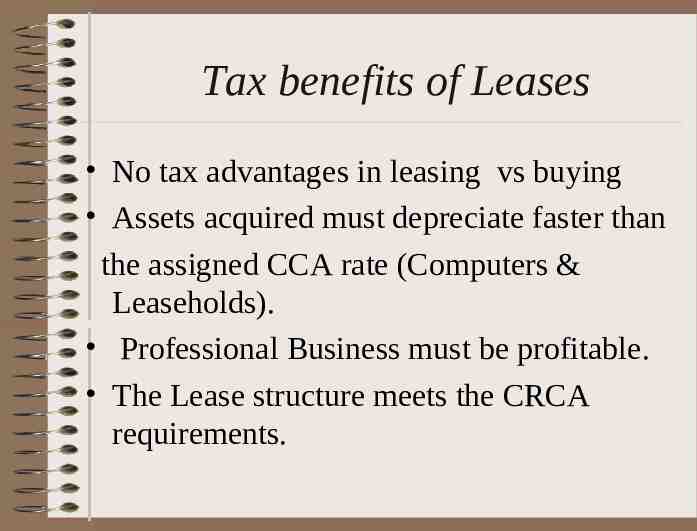

Tax benefits of Leases No tax advantages in leasing vs buying Assets acquired must depreciate faster than the assigned CCA rate (Computers & Leaseholds). Professional Business must be profitable. The Lease structure meets the CRCA requirements.

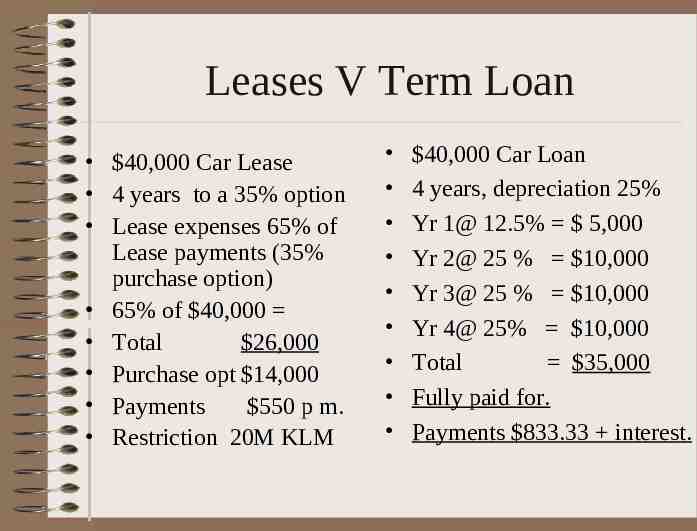

Leases V Term Loan 40,000 Car Lease 4 years to a 35% option Lease expenses 65% of Lease payments (35% purchase option) 65% of 40,000 Total 26,000 Purchase opt 14,000 Payments 550 p m. Restriction 20M KLM 40,000 Car Loan 4 years, depreciation 25% Yr 1@ 12.5% 5,000 Yr 2@ 25 % 10,000 Yr 3@ 25 % 10,000 Yr 4@ 25% 10,000 Total 35,000 Fully paid for. Payments 833.33 interest.

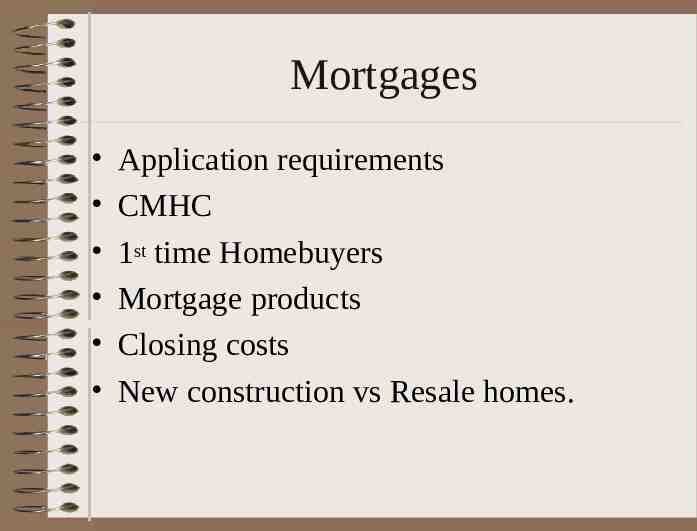

Mortgages Application requirements CMHC 1st time Homebuyers Mortgage products Closing costs New construction vs Resale homes.

Other Credit Products Scotialine & Scotialine Visa Visa – Value – Classic – Gold

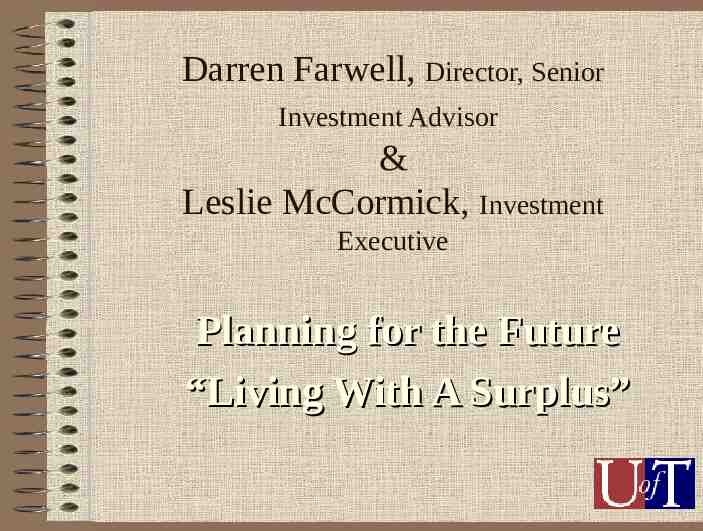

Darren Farwell, Director, Senior Investment Advisor & Leslie McCormick, Investment Executive Planning for the Future “Living With A Surplus”

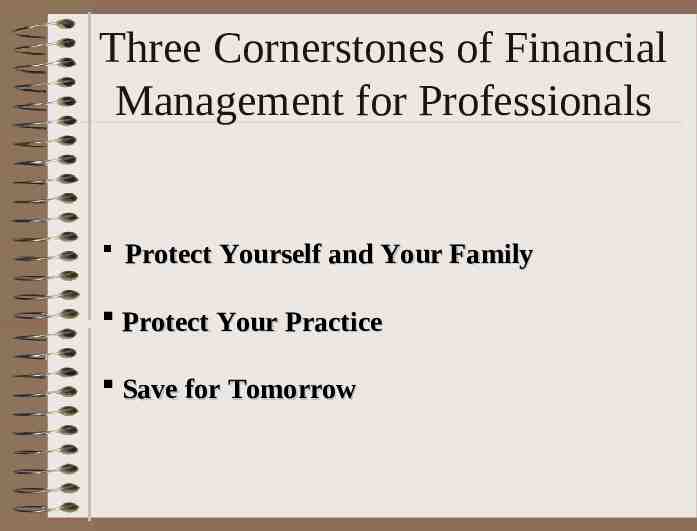

Three Cornerstones of Financial Management for Professionals Protect Yourself and Your Family Protect Your Practice Save for Tomorrow

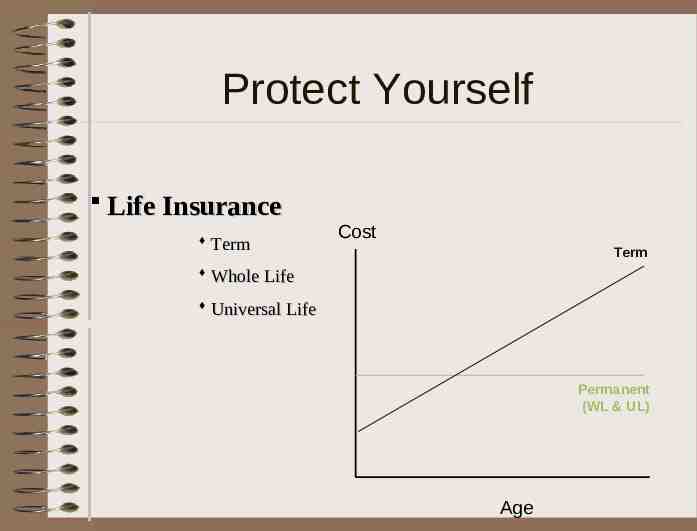

Protect Yourself Life Insurance Term Cost Term Whole Life Universal Life Permanent (WL & UL) Age

Protect Yourself Disability Insurance What is the Definition!!

Protect Your Practice Professional Liability Insurance

Build for Tomorrow Your Personal Savings Pyramid Insurance RRSP RESP Downpayment for a New Home High Cost Debt, (Reduce the highest cost debt first) Mortgage Prepayment, (particularly at today’s rates) Investment Accounts ** Of course, the specific order for your personal circumstances is a function of your lifestyle and objectives and therefore should be considered on an individual basis with professional advice

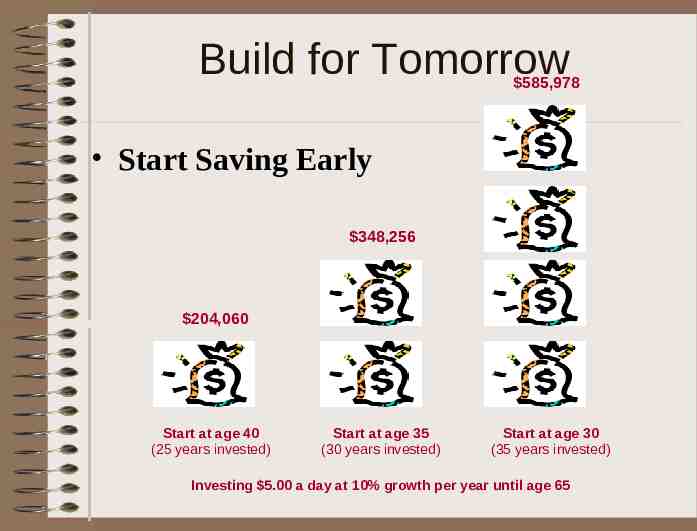

Build for Tomorrow 585,978 Start Saving Early 348,256 204,060 Start at age 40 (25 years invested) Start at age 35 (30 years invested) Start at age 30 (35 years invested) Investing 5.00 a day at 10% growth per year until age 65

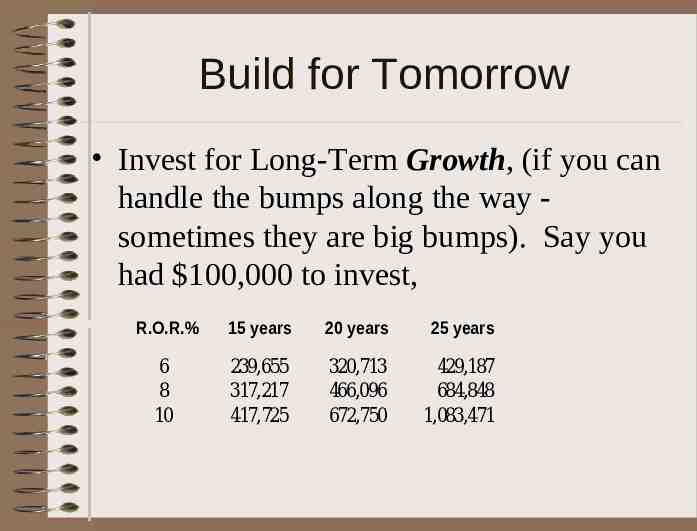

Build for Tomorrow Invest for Long-Term Growth, (if you can handle the bumps along the way sometimes they are big bumps). Say you had 100,000 to invest, R.O.R.% 15 years 20 years 25 years 6 8 10 239,655 317,217 417,725 320,713 466,096 672,750 429,187 684,848 1,083,471

Build for Tomorrow “If You Don’t Know Where You’re Going, You’ll End Up Somewhere Else” Yogi Berra

Building Relationships for Life

History of Scotiabank’s involvement in your Profession Tenure in the Professional field ( 13 years) – We are not about to buy market share. Meeting future needs for Students and Professionals. – Focus Groups – Customers Expectations Team of Experts ( Queen & McCaul) Heart surgery vs General Practitioner Accessibility – Association Endorsement – Specialty Classification for Professionals

My Role Conduit to the health care profession. Keeping abreast of changes in your industry i.e. incorporation, P.I.PE.D.A. tax issues etc. Provide Guidance Throughout your career – Introductions to industry experts i.e. C.A’s, Lawyers, Insurance Experts and Brokers. – Advising which “Centre of Influence” will be best suited to your needs: – Location, Profession, Complexity

My Role (cont’d) Support Continuing Education: – University Involvement. – Professional Faculty Training & Development of “Centre of Influence”. to meet the ever changing industry and meet your future expectations of a financial institutions.

Any Questions ?