Mutual of Omaha’s Annuity Portfolio and Certification 2016

83 Slides1.99 MB

Mutual of Omaha’s Annuity Portfolio and Certification 2016

Annuity Overview The main objectives of people planning for retirement are to: Maintain their current lifestyle at retirement and Provide for adequate health care

Annuity Overview The importance of retirement planning has escalated in recent years due to concerns regarding: The inadequacy of Social Security benefits The demise of traditional employer-provided pensions

Annuity Overview Now more than ever people are aware of the need to plan for a financially secure retirement. They recognize that they will have to rely primarily on company pensions, personal savings and investments for retirement.

Annuity Overview Annuities are one of the best ways to accumulate money for retirement and are specifically designed for two important retirement planning aspects: Maximum accumulation of funds before retirement and A reliable source of income after retirement

Annuity Overview Annuities offer your clients important benefits : Lifetime income Security of principal Tax-deferred accumulation Consistent investment return Sound investment management Flexible features of distribution and accumulation Low risk

Annuity Overview Annuities can be a valuable tool in helping your clients succeed in achieving their retirement planning goals.

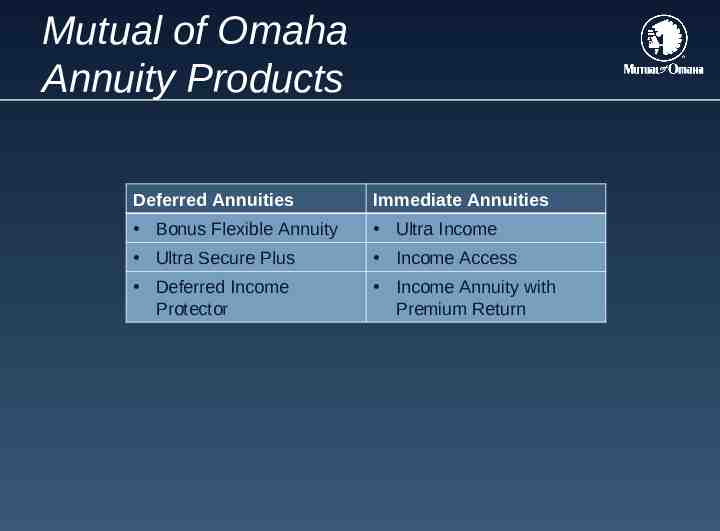

Mutual of Omaha Annuity Products Deferred Annuities Immediate Annuities Bonus Flexible Annuity Ultra Income Ultra Secure Plus Income Access Deferred Income Protector Income Annuity with Premium Return

DEFERRED ANNUITIES

Bonus Flexible Annuity The Bonus Flexible Annuity is designed specifically for the accumulation of funds for both tax-qualified and nonqualified plans. It is a flexible premium deferred annuity with a fixed interest rate and flexible contribution options.

Bonus Flexible Annuity Issue Ages: 0-89 Premium: 1,200 minimum annual contribution for recurring premiums 5,000 minimum for single premium Contributions: Flexible May be increased or decreased at any time subject to a minimum of 100 a month

Bonus Flexible Annuity Cash value accumulates at a current interest rate Contributions receive an additional 1 percent in addition to the current rate during the first 12 months for all new deposits made After 12 months, the deposits receive the stated current interest rate, but no additional 1 percent Additional 0.15 percent* added to interest rate on accumulation values equal to or over 50,000 * These values are subject to change

Bonus Flexible Annuity A 10 percent annual withdrawal of the cash value is allowed with no surrender charge Minimum withdrawal is 100 The accumulation value cannot be less than 5,000 after the withdrawal The accumulation value may be withdrawn, subject to applicable withdrawal fees in the first 8 years

Bonus Flexible Annuity A systematic income feature provides a regular income to annuitants Withdrawal options are interest only or fixed amount The income withdrawals can be as low as 100 and can be monthly, quarterly, semiannually or annually Withdrawal charges apply to systematic income withdrawals that exceed 10 percent of the accumulation value during the first 8 policy years The request for a systematic withdrawals can be made at any time by completing the appropriate form

Bonus Flexible Annuity The death benefit is equal to the accumulation value less any applicable premium taxes.

Ultra-Secure Plus Ultra-Secure Plus is a single premium deferred annuity with either a five-year or a seven-year rate guarantee. It is designed for long-term tax-deferred growth and a competitive long-term interest rate.

Ultra-Secure Plus Issue ages: 0-89 Premiums: 5,000 is the minimum purchase amount Subsequent purchases of 2,500 (nonqualified) or 2,000 (qualified) are allowed Policy additions are allowed within the first year. and the minimum amount is 500.

Ultra-Secure Plus Ultra-Secure Plus interests rates: Five or seven-year fixed rate guarantee period Additional 0.15 percent interest added to purchase payments and accumulation values of 50,000 or higher

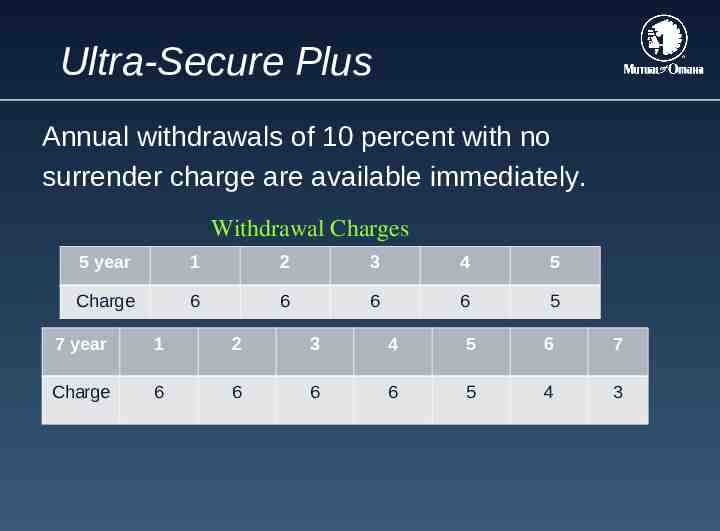

Ultra-Secure Plus Annual withdrawals of 10 percent with no surrender charge are available immediately. Withdrawal Charges 5 year 1 2 3 4 5 Charge 6 6 6 6 5 7 year 1 2 3 4 5 6 7 Charge 6 6 6 6 5 4 3

Ultra-Secure Plus Surrender charges will NOT apply if the withdrawal* is for any of the following: Confinement to a Hospital, Nursing Home or Long-Term Care Facility Unemployment Disability Terminal illness Death of a Spouse or Minor Dependent Damage to Residence Transplant Surgery * Not available in all states

Ultra-Secure Plus A market value adjustment may apply to a cash surrender or partial withdrawal. If the interest rate at the time of the surrender or withdrawal is higher than the multi-year guaranteed interest rate, the market value adjustment will be downward If the interest rate at the time of the surrender or withdrawal is lower than the multi-year guaranteed interest rate, the market value adjustment will be upward There will be no interest rate adjustment if the contract is surrendered, renewed or a payout option is selected during the renewal period

Ultra-Secure Plus Ultra-Secure Plus has a return of premium benefit. Surrender value will never be less than purchase payments* 100 percent of remaining premiums can be returned at anytime* Renews at time of contract renewal and guarantees the client the accumulation value at the time of the most recent renewal date* * Minus any withdrawals and any applicable premium tax

Ultra-Secure Plus Ultra-Secure Plus has a 30-day window at the end of the surrender period. During this 30-day window, clients have three choices: Renew their contract and reinstate it for another full contract Annuitize the contract Surrender (without charge)

Ultra-Secure Plus The death benefit equals the accumulation value on the date of the owner’s death, minus any applicable premium taxes.

Deferred Income Protector The Deferred Income Protector is a “pensionlike” annuity that: Provides clients with a guaranteed fixed amount of monthly income that they will begin receiving several years in the future, and Affords protection against constantly fluctuating interest rates and higher income payments

Deferred Income Protector Individuals can invest some of their assets to secure a portion of their retirement needs. It also serves clients who are looking for a longevity product that provides security against outliving their existing assets at advanced ages.

Deferred Income Protector Qualifying Longevity Annuity Contracts(QLACs): Are fixed-rate deferred annuities that can be sold with certain types of employer-sponsored retirement plans and IRAs Individuals may allocate either 25 percent of total qualifying assets or 125,000, whichever is less, into a QLAC, diverting a portion of their qualified funds for later use Reduces the required minimum distributions (RMDs) he or she must start paying at age 70 ½ Must start taking distributions no later than age 85

Deferred Income Protector Target Market: Ages 55-65 Approaching retirement age Planning to retire in the next 5 to 10 years

Deferred Income Protector Issue ages: Between 40 and 75 for non-qualified and QLAC plans Between 40 and 68 for qualified plans

Deferred Income Protector The minimum initial premium is 5,000 Additional purchase payments may be added at any time until two years before the Income Start Date Subsequent purchases must be at least 2,000 The sum of all purchase payments may not exceed 1,000,000 without home office approval

Deferred Income Protector Surrenders are not allowed. This contract does not provide access to funds prior to the income start date, other than payment of the death benefit, if any.

Deferred Income Protector Deferral Period: 2-40 years Income payments must begin by age 70 ½ if qualified or age 85 if non-qualified or QLAC

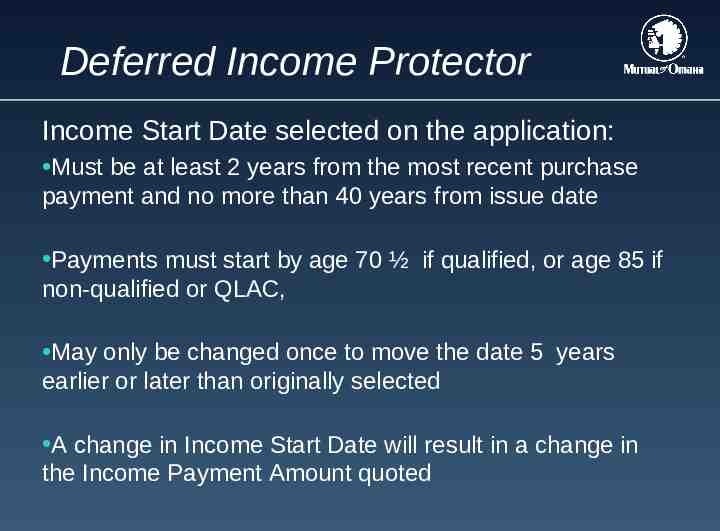

Deferred Income Protector Income Start Date selected on the application: Must be at least 2 years from the most recent purchase payment and no more than 40 years from issue date Payments must start by age 70 ½ if qualified, or age 85 if non-qualified or QLAC, May only be changed once to move the date 5 years earlier or later than originally selected A change in Income Start Date will result in a change in the Income Payment Amount quoted

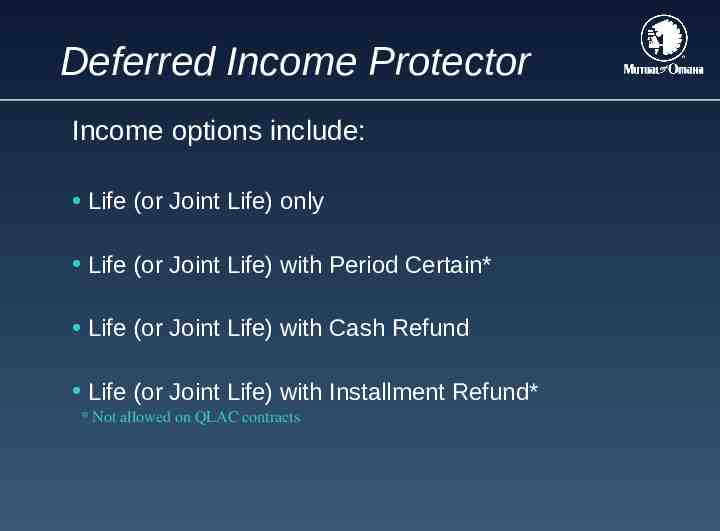

Deferred Income Protector Income options include: Life (or Joint Life) only Life (or Joint Life) with Period Certain* Life (or Joint Life) with Cash Refund Life (or Joint Life) with Installment Refund* * Not allowed on QLAC contracts

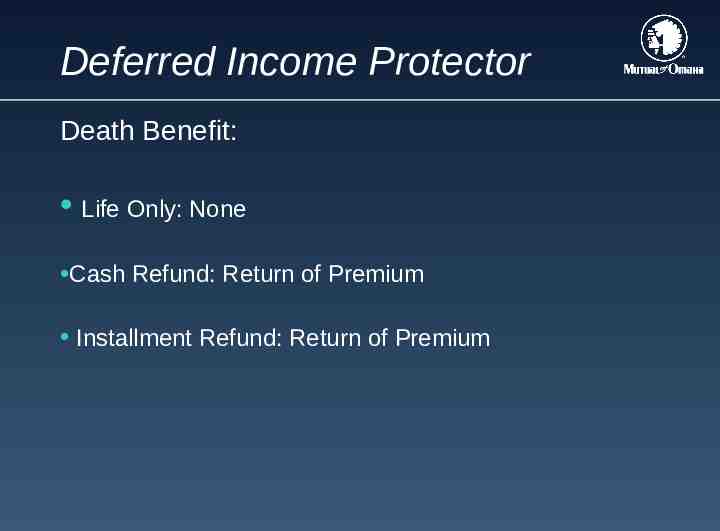

Deferred Income Protector Death Benefit: Life Only: None Cash Refund: Return of Premium Installment Refund: Return of Premium

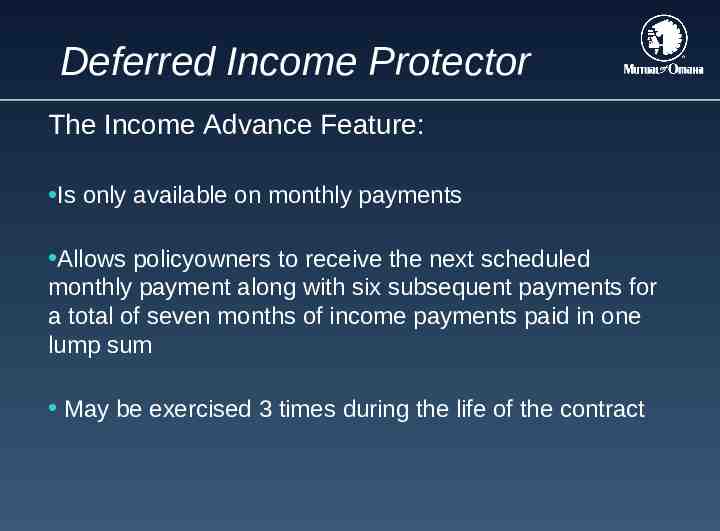

Deferred Income Protector The Income Advance Feature: Is only available on monthly payments Allows policyowners to receive the next scheduled monthly payment along with six subsequent payments for a total of seven months of income payments paid in one lump sum May be exercised 3 times during the life of the contract

Deferred Income Protector Annual Income Increase Option: Must be elected at the time of application Allows policyowners to increase income payments by 1-3 percent annually Annual increases begin on the Income Start Date

Deferred Income Protector Income Reduction for Surviving Spouse allows the income payment to be reduced after the death of one annuitant. There is no contract fee Rated age and impaired risk underwriting are not available

Deferred Income Protector Deferred Income Protector is a versatile annuity that allows individuals to invest a portion of their assets to secure a portion of their retirement needs. It also serves clients who are looking for a longevity product that provides security against outliving their existing assets at advanced ages.

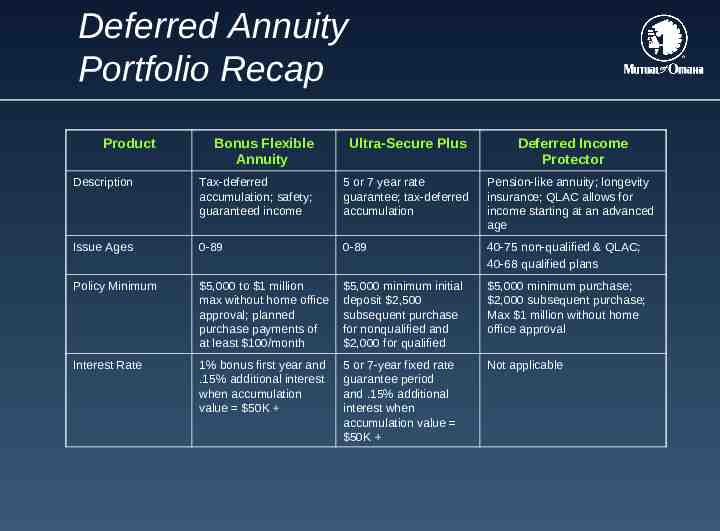

Deferred Annuity Portfolio Recap Product Bonus Flexible Annuity Ultra-Secure Plus Deferred Income Protector Description Tax-deferred accumulation; safety; guaranteed income 5 or 7 year rate guarantee; tax-deferred accumulation Pension-like annuity; longevity insurance; QLAC allows for income starting at an advanced age Issue Ages 0-89 0-89 40-75 non-qualified & QLAC; 40-68 qualified plans Policy Minimum 5,000 to 1 million max without home office approval; planned purchase payments of at least 100/month 5,000 minimum initial deposit 2,500 subsequent purchase for nonqualified and 2,000 for qualified 5,000 minimum purchase; 2,000 subsequent purchase; Max 1 million without home office approval Interest Rate 1% bonus first year and .15% additional interest when accumulation value 50K 5 or 7-year fixed rate guarantee period and .15% additional interest when accumulation value 50K Not applicable

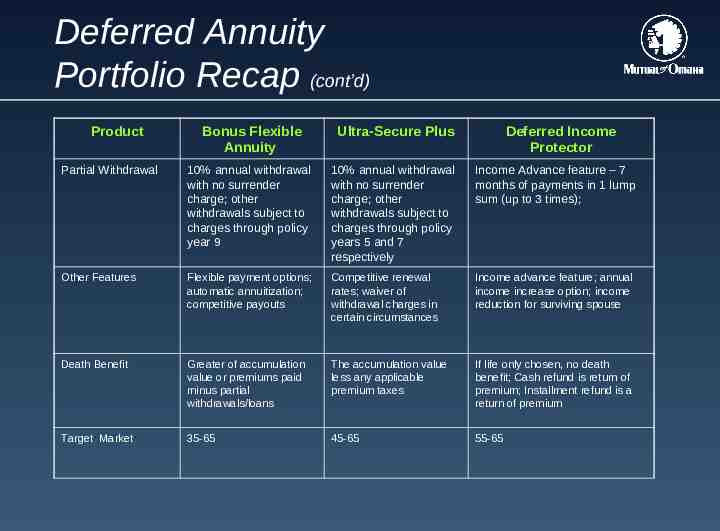

Deferred Annuity Portfolio Recap (cont’d) Product Bonus Flexible Annuity Ultra-Secure Plus Deferred Income Protector Partial Withdrawal 10% annual withdrawal with no surrender charge; other withdrawals subject to charges through policy year 9 10% annual withdrawal with no surrender charge; other withdrawals subject to charges through policy years 5 and 7 respectively Income Advance feature – 7 months of payments in 1 lump sum (up to 3 times); Other Features Flexible payment options; automatic annuitization; competitive payouts Competitive renewal rates; waiver of withdrawal charges in certain circumstances Income advance feature; annual income increase option; income reduction for surviving spouse Death Benefit Greater of accumulation value or premiums paid minus partial withdrawals/loans The accumulation value less any applicable premium taxes If life only chosen, no death benefit; Cash refund is return of premium; Installment refund is a return of premium Target Market 35-65 45-65 55-65

SINGLE PREMIUM ANNUITIES 42

Immediate Annuities Our product portfolio offers three immediate annuities: Income Access Ultra-Income Income Annuity with Premium Return

Income Access The Income Access single premium immediate annuity is a flexible plan that provides a guaranteed income to the annuitant(s). It offers a package of several base plans and optional benefits.

Income Access The Income Access single premium immediate annuity is a flexible plan that provides a guaranteed income to the annuitant(s). It offers a package of several base plans and optional benefits.

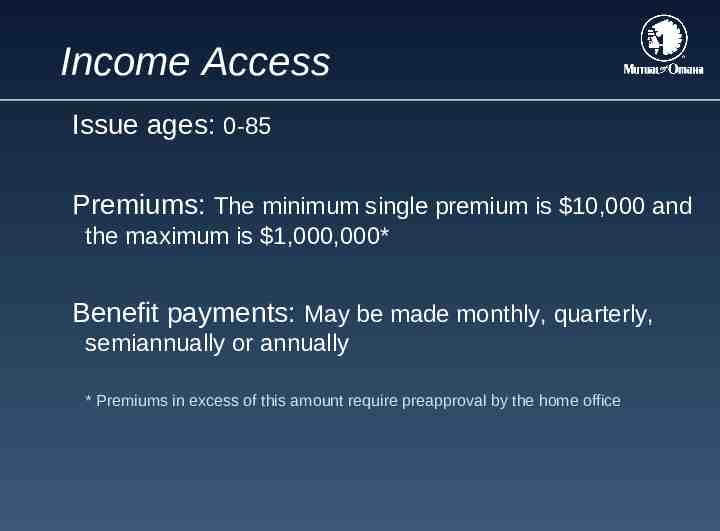

Income Access Issue ages: 0-85 Premiums: The minimum single premium is 10,000 and the maximum is 1,000,000* Benefit payments: May be made monthly, quarterly, semiannually or annually * Premiums in excess of this amount require preapproval by the home office

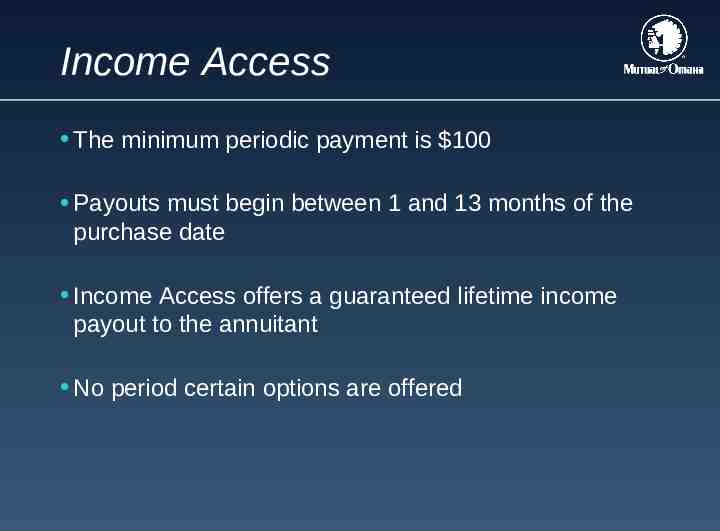

Income Access The minimum periodic payment is 100 Payouts must begin between 1 and 13 months of the purchase date Income Access offers a guaranteed lifetime income payout to the annuitant No period certain options are offered

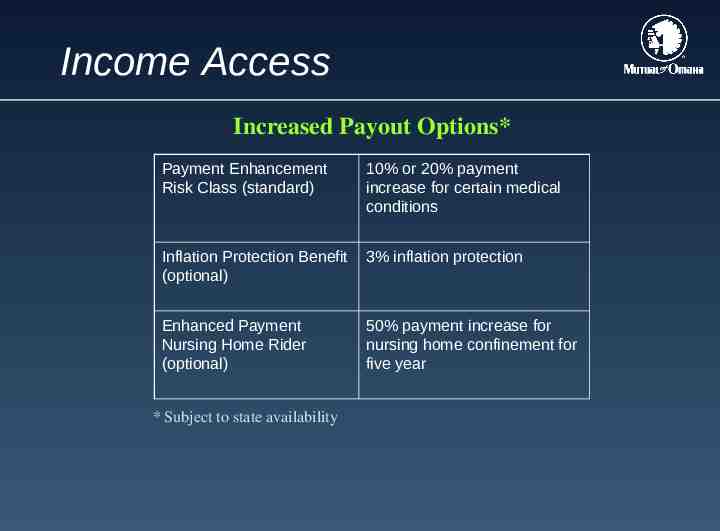

Income Access Increased Payout Options* Payment Enhancement Risk Class (standard) 10% or 20% payment increase for certain medical conditions Inflation Protection Benefit (optional) 3% inflation protection Enhanced Payment Nursing Home Rider (optional) 50% payment increase for nursing home confinement for five year * Subject to state availability

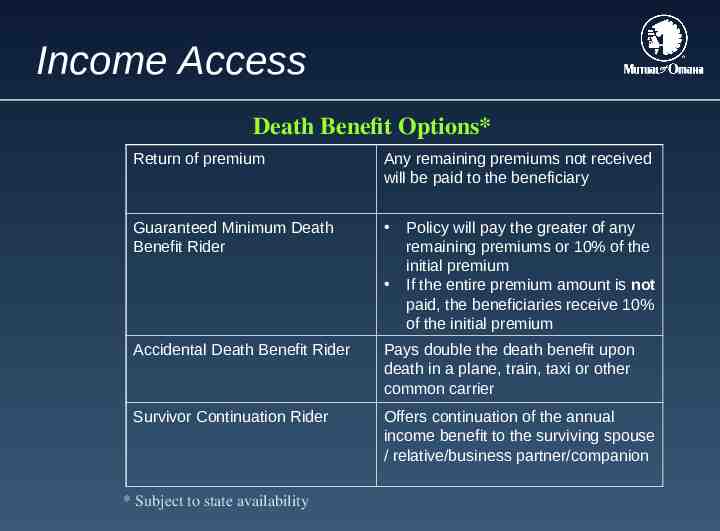

Income Access Death Benefit Options* Return of premium Any remaining premiums not received will be paid to the beneficiary Guaranteed Minimum Death Benefit Rider Policy will pay the greater of any remaining premiums or 10% of the initial premium If the entire premium amount is not paid, the beneficiaries receive 10% of the initial premium Accidental Death Benefit Rider Pays double the death benefit upon death in a plane, train, taxi or other common carrier Survivor Continuation Rider Offers continuation of the annual income benefit to the surviving spouse / relative/business partner/companion * Subject to state availability

Income Access Partial return of premium on cancellation: Allows the owner to cancel the contract and receive a lump-sum of any remaining premium. Only a partial return of premium will be paid in the first several years. Return of premium for terminal illness: Allows the owner to receive the full return of premium death benefit up to 12 months early, without being subject to the vesting schedule.

Ultra-Income Ultra-Income is a single premium immediate annuity. After the initial payment has been made, the client may choose income payments beginning the very next month or the payments may be postponed up to 13 months.

Ultra-Income Issue ages: 0-85 Premiums: The minimum single premium is 10,000 and the maximum is 1,000,000* Benefit Payments: May be made monthly, quarterly, semiannually, or annually * Premiums in excess of this amount require home office approval

Ultra-Income The minimum benefit payment is 100 Payouts must begin between 1 and 13 months of the purchase date The annuitant can elect a cost-of-living adjustment up to 6 percent of the initial annual benefit

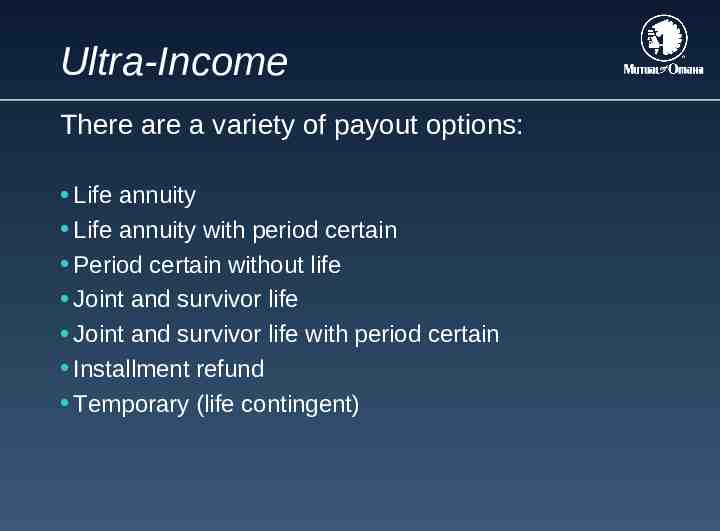

Ultra-Income There are a variety of payout options: Life annuity Life annuity with period certain Period certain without life Joint and survivor life Joint and survivor life with period certain Installment refund Temporary (life contingent)

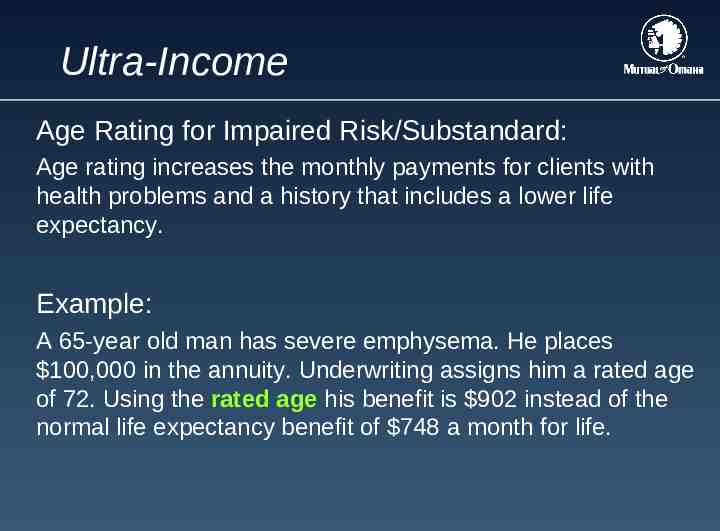

Ultra-Income Age Rating for Impaired Risk/Substandard: Age rating increases the monthly payments for clients with health problems and a history that includes a lower life expectancy. Example: A 65-year old man has severe emphysema. He places 100,000 in the annuity. Underwriting assigns him a rated age of 72. Using the rated age his benefit is 902 instead of the normal life expectancy benefit of 748 a month for life.

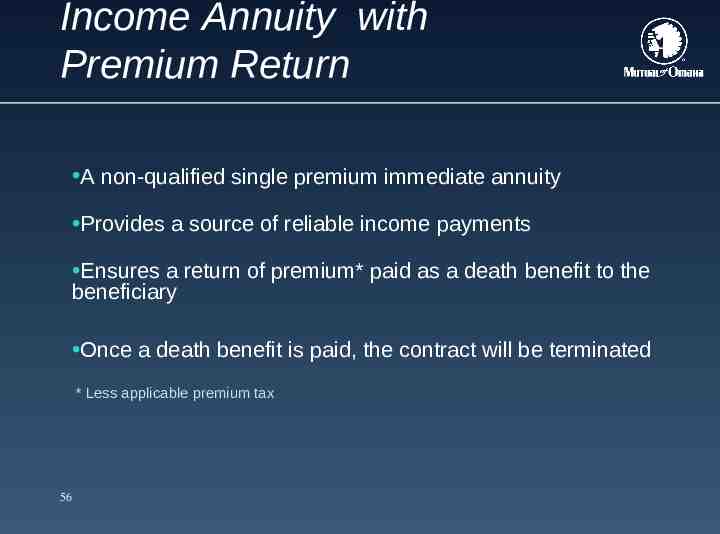

Income Annuity with Premium Return A non-qualified single premium immediate annuity Provides a source of reliable income payments Ensures a return of premium* paid as a death benefit to the beneficiary Once a death benefit is paid, the contract will be terminated * Less applicable premium tax 56

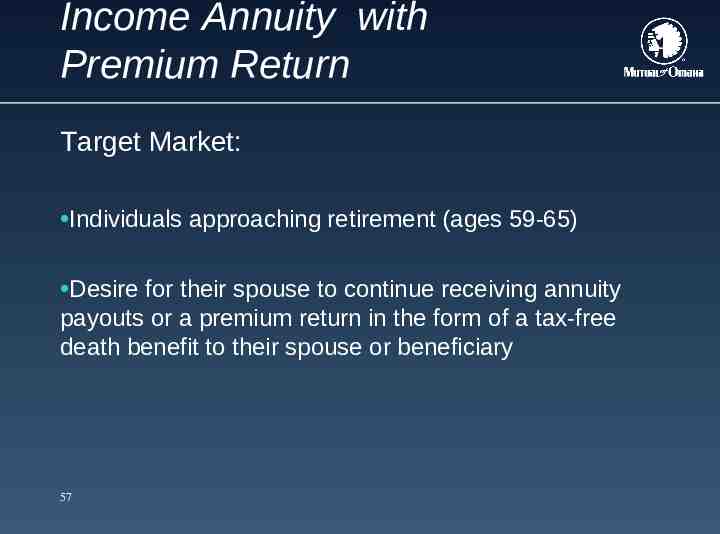

Income Annuity with Premium Return Target Market: Individuals approaching retirement (ages 59-65) Desire for their spouse to continue receiving annuity payouts or a premium return in the form of a tax-free death benefit to their spouse or beneficiary 57

Income Annuity with Premium Return Issue ages 59 to 85 Minimum single premium of 10,000 and maximum of 1 million* with a minimum periodic payment of 20 Guaranteed Life or Joint Life Only income payout Benefit payments must begin between 1 and 13 months after issue * Premiums in excess of this amount require preapproval by the home office 58

Income Annuity with Premium Return Return of Premium Death Benefit Before the Annuity Start Date: Upon the death of any joint owner, whichever occurs first, or upon the death of the last surviving annuitant, the death benefit is paid to: Any surviving owner* if none then The beneficiary* if none, then The last surviving owner’s estate * Spousal Continuation: If the sole surviving owner or sole beneficiary is the Owner’s spouse and there is at least one surviving annuitant, the surviving spouse may elect to become the new Owner and continue the contract instead of receiving the death benefit. This election must be made by formal request no more than 90 days following the death of the Owner and may only be elected once. 59

Income Annuity with Premium Return Return of Premium Death Benefit On or After Annuity Start Date: Upon the death of the last surviving annuitant, the death benefit is paid to: Any surviving owner if none then The beneficiary if none, then The last surviving owner’s estate Interest will be paid on the death benefit from the date of the death that triggers the death benefit to the date of payment. 60

Income Annuity with Premium Return Example A: One Owner, Different Annuitant At age 60, Theresa purchased an Income Annuity with Premium Return contract and named her spouse John as the Annuitant. Payments started two months later. Unfortunately, John dies six months after the annuity payments begin. The death benefit is paid to the Owner (Theresa) and the contract is terminated. Example B: Two Owners, One is the Annuitant If Theresa and John are joint owners, John is the Annuitant and Theresa dies after the annuity payments start, the contract continues with the one surviving owner/annuitant. 61

Income Annuity with Premium Return 1035 Exchanges are available with this product. All payouts are fully taxable and the death benefit will be tax-free up to the cost basis A formal request can be submitted to change the ownership or to assign the contract. If an irrevocable beneficiary exists, they must also sign the request Commutation (contract value) can be requested at any time. It is equal to the present value of both the projected future income payments and the projected death benefit 62

Income Annuity with Premium Return Terminating the Contract: The commuted value will be distributed as a lump sum payment upon terminating the contract. The commuted value is equal to the present value of both the projected future income payments and the projected death benefit and will always be less than the sum of future income payments and the death benefit If the Owner wishes to pursue commutation, they must notify the home office 63

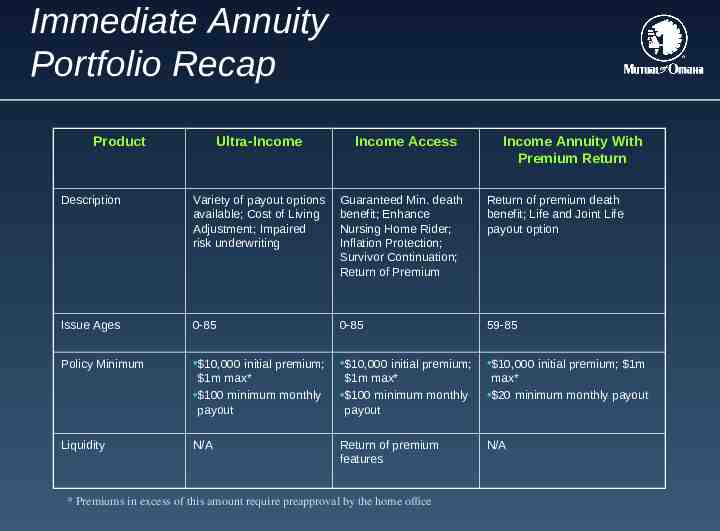

Immediate Annuity Portfolio Recap Product Ultra-Income Income Access Income Annuity With Premium Return Description Variety of payout options available; Cost of Living Adjustment; Impaired risk underwriting Guaranteed Min. death benefit; Enhance Nursing Home Rider; Inflation Protection; Survivor Continuation; Return of Premium Return of premium death benefit; Life and Joint Life payout option Issue Ages 0-85 0-85 59-85 Policy Minimum 10,000 initial premium; 10,000 initial premium; 10,000 initial premium; 1m 1m max* 100 minimum monthly payout 1m max* 100 minimum monthly payout max* 20 minimum monthly payout N/A Return of premium features N/A Liquidity * Premiums in excess of this amount require preapproval by the home office

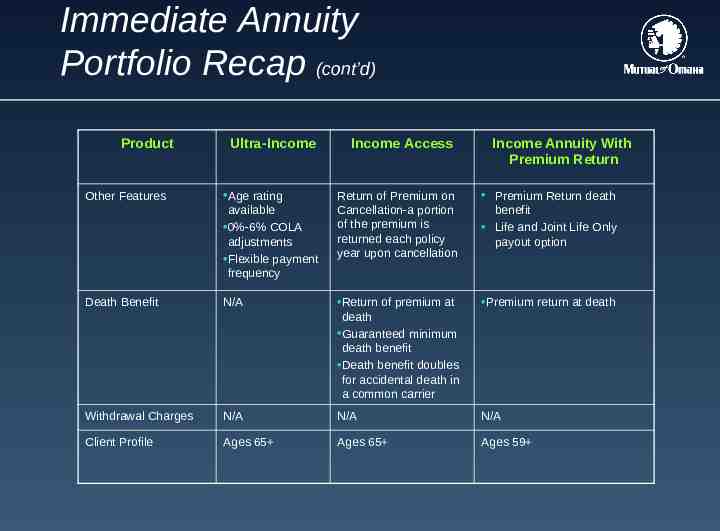

Immediate Annuity Portfolio Recap (cont’d) Product Other Features Ultra-Income Age rating available 0%-6% COLA adjustments Flexible payment frequency Death Benefit N/A Income Access Income Annuity With Premium Return Return of Premium on Cancellation-a portion of the premium is returned each policy year upon cancellation Premium Return death Return of premium at Premium return at death benefit Life and Joint Life Only payout option death Guaranteed minimum death benefit Death benefit doubles for accidental death in a common carrier Withdrawal Charges N/A N/A N/A Client Profile Ages 65 Ages 65 Ages 59

Resources Fixed Annuities Product Portfolio Overview Bonus Flexible Annuity Policy Highlights Ultra-Secure Plus Highlights Income Annuity with Premium Return Highlights

Suitability

NAIC Suitability Model In recommending the purchase or exchange of an annuity, agents must have reasonable grounds for believing the recommendation is suitable for the customer.

Suitability To determine the product’s suitability, the agent must obtain information concerning: The client’s financial status The client’s tax status The client’s investment objectives and Any other information used or considered to be reasonable in making the recommendation to the client

Annuity Suitability Form This form is required to be completed and signed by the applicant and must be submitted with the application before an annuity can be issued.

Disclosure

Disclosure Clients must be given a disclosure about the specific annuity being offered for purchase. The disclosure reviews important points that the client needs to consider.

Disclosure Some of the topics the disclosure will cover: Type of annuity Benefits Annuity starting date Fees, expenses and other charges Withdrawal charges, if applicable Taxes Miscellaneous information

Disclosure The appropriate disclosure forms must be provided to the client. they must be completed and signed.

Summary It is important as you make a recommendation for an annuity to a client that you have reasonable grounds that the recommendation is suitable for the client based on the facts disclosed by the client.

Replacements

Replacements Replacement of existing coverage should occur only when it is in the best interest of the client. You need to be able to assist the client in evaluating whether replacement is in his or her best interest.

Replacements When completing the application if the applicant answers “yes” to the question regarding existing coverage and coverage will be replaced or used to fund the new contract, the client must be given a replacement notice. In addition, the application should list the name of the insurer, insured or annuitant, and the policy or contract number of the policy being replaced, if available.

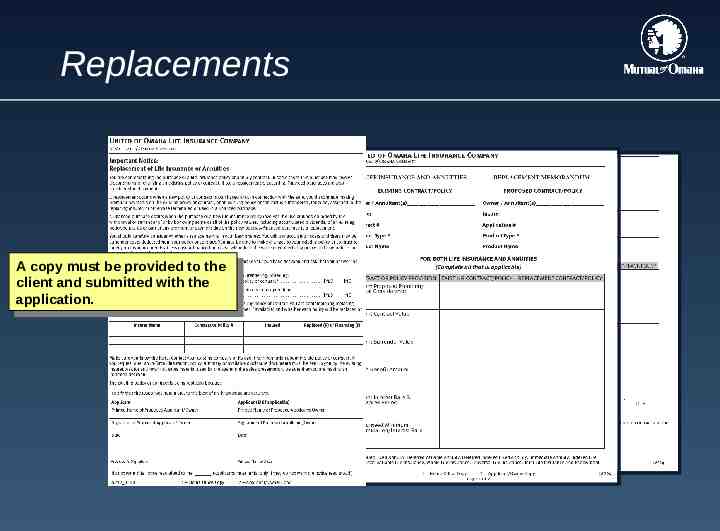

Replacements AAcopy copymust mustbe beprovided providedto tothe the client and submitted with the client and submitted with the application. application.

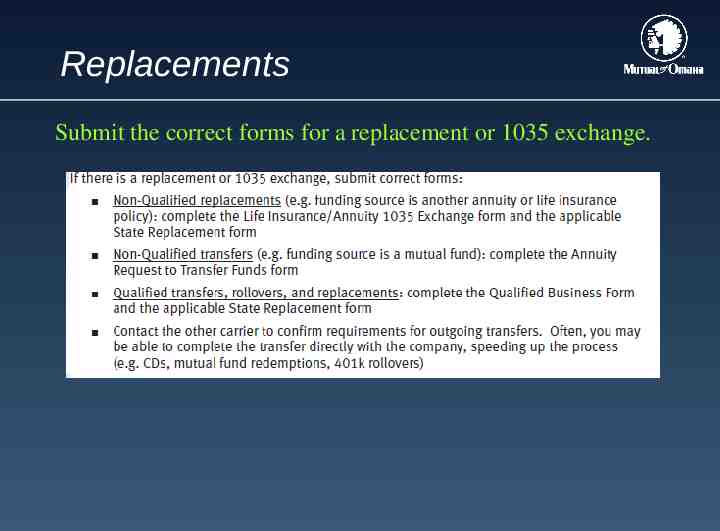

Replacements Submit the correct forms for a replacement or 1035 exchange.

Replacements Remember, in making a recommendation, the agent must have reasonable grounds to believe the recommendation is suitable based on the facts the client has disclosed about his or her financial situation and needs.

Annuity Checklist When selling an annuity be sure to: Submit the completed application Complete and submit the Annuity Suitability form Complete and submit the appropriate Disclosure Statement If there is a replacement or 1035 exchange, submit the correct forms Provide a copy of the “Buyer’s Guide to Annuities” to the client (where required)

Certification and Acknowledgement Congratulations! You have completed the NAIC National Annuity Training course. To receive credit: Log into SPA, Training & Compliance tab, Protect Your Business header, click the NAIC Annuity Suitability link and scroll down to the form titled, “Certificate and Acknowledgement” form. Complete it and email to: [email protected] Questions can be directed to: 1-800-867-6873 83