INTERNAL AUDIT ACCOUNTS PAYABLE AUDIT University of Washington

5 Slides153.00 KB

INTERNAL AUDIT ACCOUNTS PAYABLE AUDIT University of Washington August 11, 2011 Kim Herrenkohl, Director Western Washington University Office of the Internal Auditor 360-650-3435 [email protected]

Training Objectives Discuss common fraud risks Objectives of an operational accounts payable audit Discuss WWU’s Audit Program Discuss WWU’s Audit Report

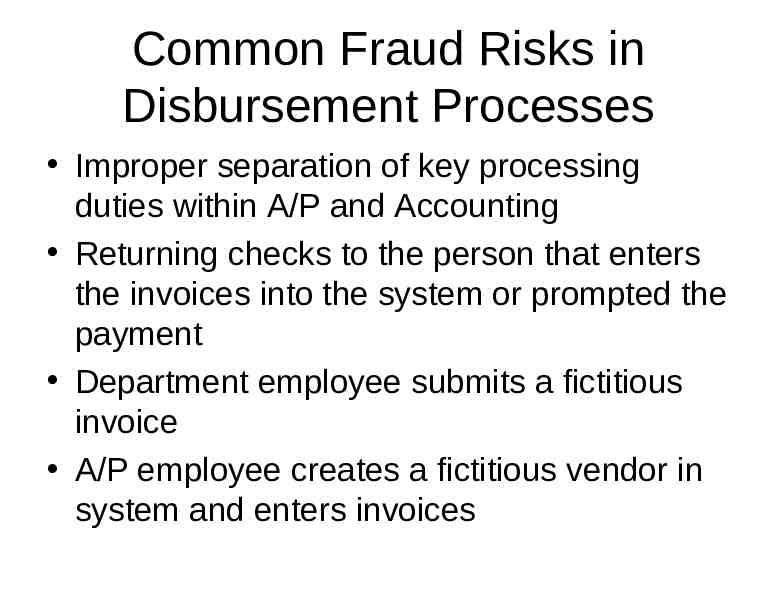

Common Fraud Risks in Disbursement Processes Improper separation of key processing duties within A/P and Accounting Returning checks to the person that enters the invoices into the system or prompted the payment Department employee submits a fictitious invoice A/P employee creates a fictitious vendor in system and enters invoices

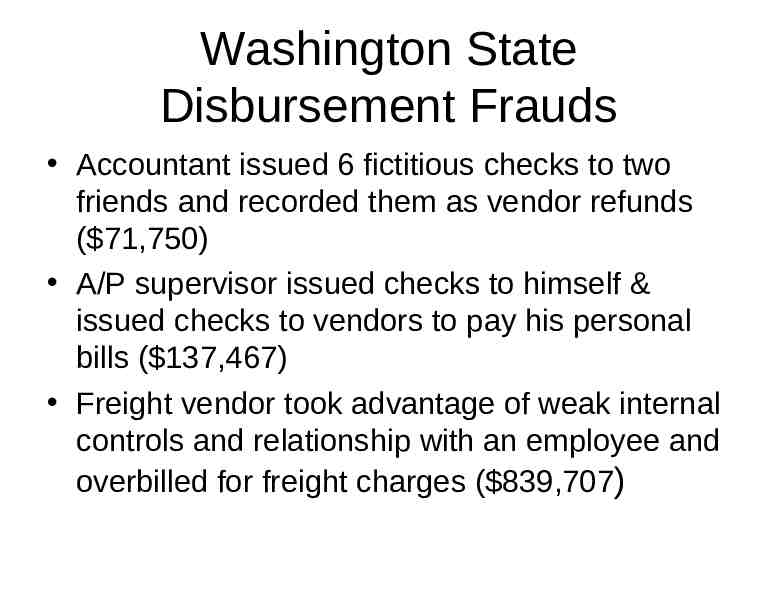

Washington State Disbursement Frauds Accountant issued 6 fictitious checks to two friends and recorded them as vendor refunds ( 71,750) A/P supervisor issued checks to himself & issued checks to vendors to pay his personal bills ( 137,467) Freight vendor took advantage of weak internal controls and relationship with an employee and overbilled for freight charges ( 839,707)

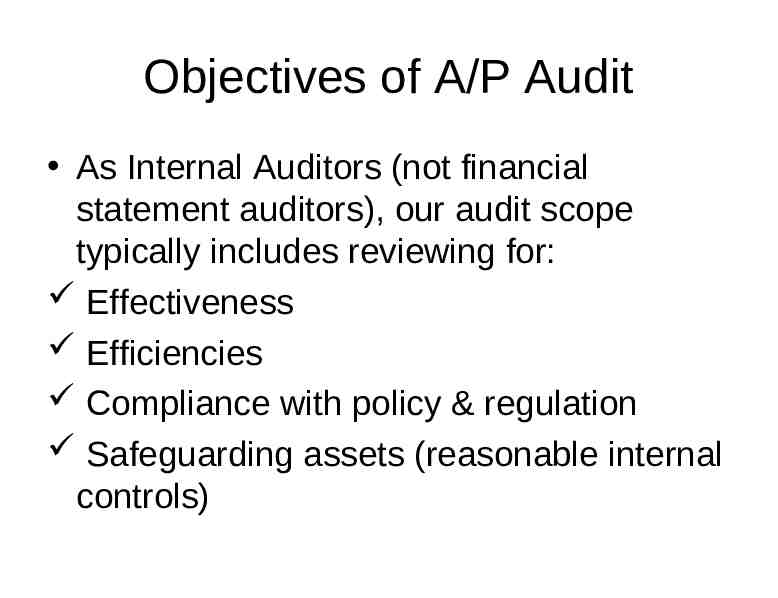

Objectives of A/P Audit As Internal Auditors (not financial statement auditors), our audit scope typically includes reviewing for: Effectiveness Efficiencies Compliance with policy & regulation Safeguarding assets (reasonable internal controls)