BREAKOUT SESSION #12 Administering Title IV Aid for Transfer

57 Slides686.54 KB

BREAKOUT SESSION #12 Administering Title IV Aid for Transfer Students Trevor Summers U.S. Department of Education 2021 Virtual FSA Training Conference for Financial Aid Professionals

AGENDA 1. What is a Transfer Student? 2. Transfer Student Monitoring (TSM) 3. Student eligibility general provisions 4. Administering Federal Pell Grants 5. Administering Federal Direct Loans 6. Overlapping payment periods and Return of Title IV (R2T4) 2

WHAT IS A TRANSFER STUDENT? 3

TRANSFER STUDENT OR MIDYEAR TRANSFER STUDENT? A transfer student is someone who has earned credits for study at School A but wants to transfer to School B and bring over the credits they have earned A student may have attended School A several years ago (or more) and is now transferring to your school ‒ This is a transfer student, but not a mid-year transfer student A student may have attended School A during the same award year and is now transferring to your school ‒ This is a mid-year transfer student and is what we will be discussing today 4

TRANSFER MONITORING AND GENERAL PROVISIONS 5

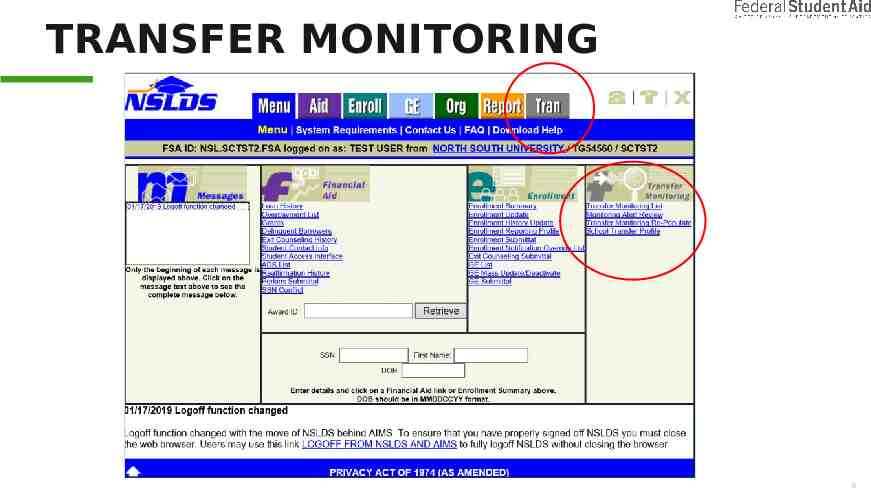

TRANSFER MONITORING 6

TRANSFER MONITORING TRANSFER MONITORING APPLIES TO ANY STUDENT WHO ATTENDED ANOTHER SCHOOL PRIOR TO ATTENDING YOUR SCHOOL IN THE SAME AWARD YEAR. Identify students transferring to your school during the award year Provide identifying information for those students to the National Student Loan Data System (NSLDS ) NSLDS alerts you to any relevant changes in student’s financial aid history 7

THREE-STEP PROCESS INFORM: CREATE A LIST OF TRANSFER STUDENTS THAT YOU NEED NSLDS TO MONITOR. This list can be created on the NSLDS website or can be created in your own software and submitted in batches to NSLDS via the Student Aid Internet Gateway (SAIG) You are encouraged to add students to the list who have received Title IV aid in the past, but will not be receiving it at your school 8

THREE-STEP PROCESS MONITOR: ONCE YOUR LIST HAS BEEN ESTABLISHED, NSLDS WILL MONITOR THE STUDENTS FOR CHANGES IN THEIR FINANCIAL AID HISTORY. NSLDS will monitor students from 30 to 120 days from the enrollment’s begin date, depending on the time frame you established when setting up your school’s transfer profile 9

THREE-STEP PROCESS ALERT: NSLDS WILL NOTIFY YOU WHEN A: New loan or grant is being awarded; New disbursement is made on loan or grant; and Loan or grant (or single disbursement) is revised or cancelled NSLDS also sends an electronic notification to the email address included on the School Transfer Profile setup page. 10

VERIFICATION BY ANOTHER SCHOOL IF A STUDENT IS SELECTED FOR VERIFICATION, AND WAS VERIFIED BY ANOTHER SCHOOL BEFORE TRANSFERRING TO YOURS, VERIFICATION IS NOT REQUIRED PROVIDED THAT: Verification was performed for the same award year; The student’s Free Application for Federal Student Aid (FAFSA ) data has not changed; and A letter is obtained from the previous school confirming verification and the pertinent Institutional Student Information Record (ISIR) transaction number 11

SATISFACTORY ACADEMIC PROGRESS SCHOOLS MUST INCLUDE IN THEIR SATISFACTORY ACADEMIC PROGRESS POLICY HOW TRANSFER STUDENT PROGRESS IS MONITORED. Transfer credits that count toward the student’s current program must be counted as both attempted and completed hours (quantitative measure) Credits not counted toward the student’s program may also be counted at your school’s discretion, as described in your SAP policy At a minimum, transferred hours that count toward a student’s program must be considered attempted and completed in reviewing student pace. 12

WHY ALL THESE STEPS? To ensure the student maintains eligibility as they transfer from School A to School B To ensure the annual Federal Student Aid limits are not exceeded 13

ADMINISTERING FEDERAL PELL GRANTS 14

APPROACHING PELL GRANT CALCULATIONS Always approach Federal Pell Grant awards from an award year perspective (e.g., July 1, 2021 to June 30, 2022) to determine remaining Pell Grant eligibility Use the appropriate formula to determine award amounts on a payment period basis, up to the remaining Pell Grant eligibility amount 15

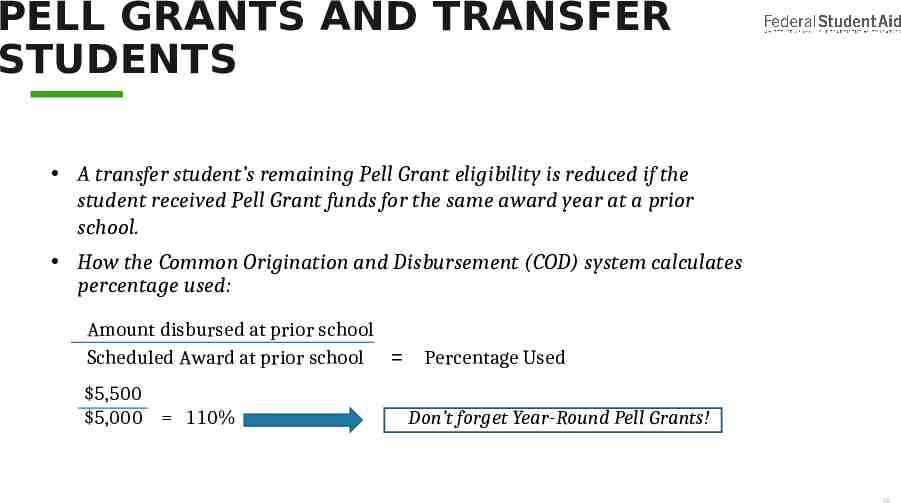

PELL GRANTS AND TRANSFER STUDENTS A transfer student’s remaining Pell Grant eligibility is reduced if the student received Pell Grant funds for the same award year at a prior school. How the Common Origination and Disbursement (COD) system calculates percentage used: Amount disbursed at prior school Scheduled Award at prior school 5,500 5,000 110% Percentage Used Don’t forget Year-Round Pell Grants! 16

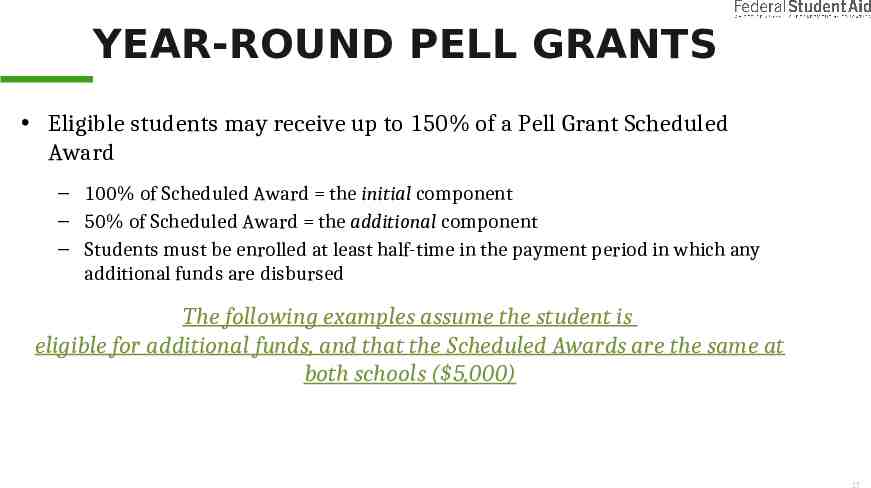

YEAR-ROUND PELL GRANTS Eligible students may receive up to 150% of a Pell Grant Scheduled Award ‒ 100% of Scheduled Award the initial component ‒ 50% of Scheduled Award the additional component ‒ Students must be enrolled at least half-time in the payment period in which any additional funds are disbursed The following examples assume the student is eligible for additional funds, and that the Scheduled Awards are the same at both schools ( 5,000) 17

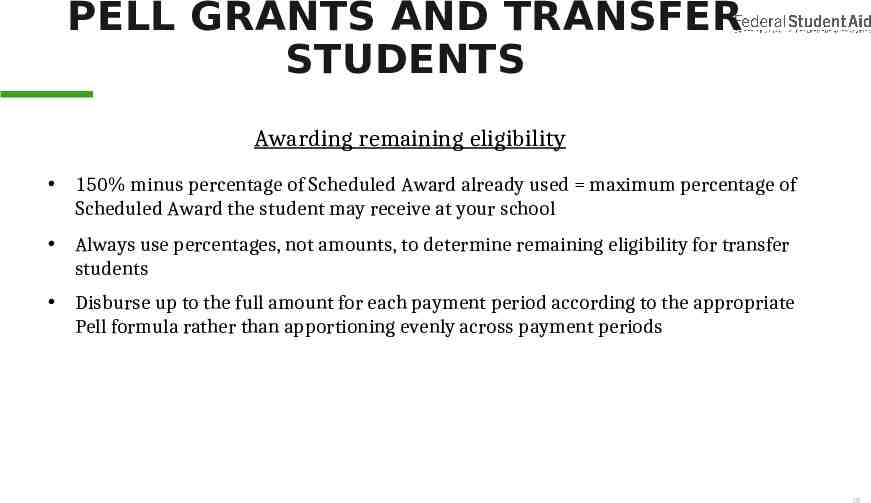

PELL GRANTS AND TRANSFER STUDENTS Awarding remaining eligibility 150% minus percentage of Scheduled Award already used maximum percentage of Scheduled Award the student may receive at your school Always use percentages, not amounts, to determine remaining eligibility for transfer students Disburse up to the full amount for each payment period according to the appropriate Pell formula rather than apportioning evenly across payment periods 18

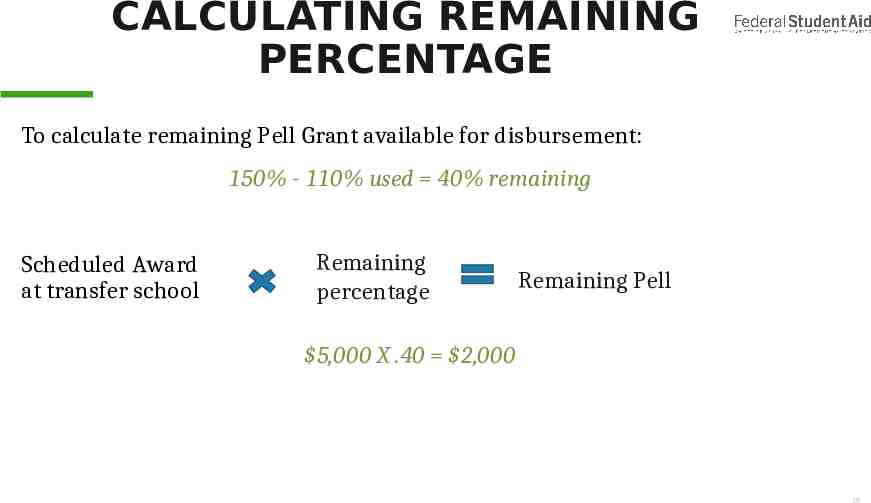

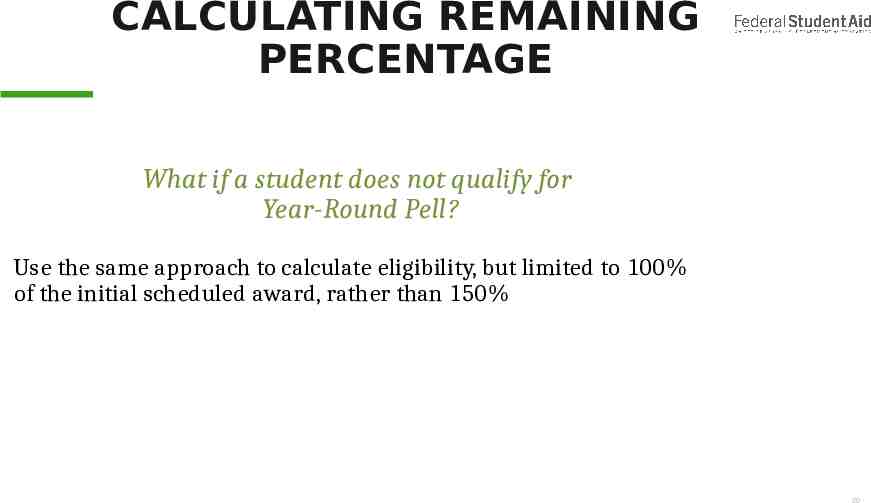

CALCULATING REMAINING PERCENTAGE To calculate remaining Pell Grant available for disbursement: 150% - 110% used 40% remaining Scheduled Award at transfer school Remaining percentage Remaining Pell 5,000 X .40 2,000 19

CALCULATING REMAINING PERCENTAGE What if a student does not qualify for Year-Round Pell? Use the same approach to calculate eligibility, but limited to 100% of the initial scheduled award, rather than 150% 20

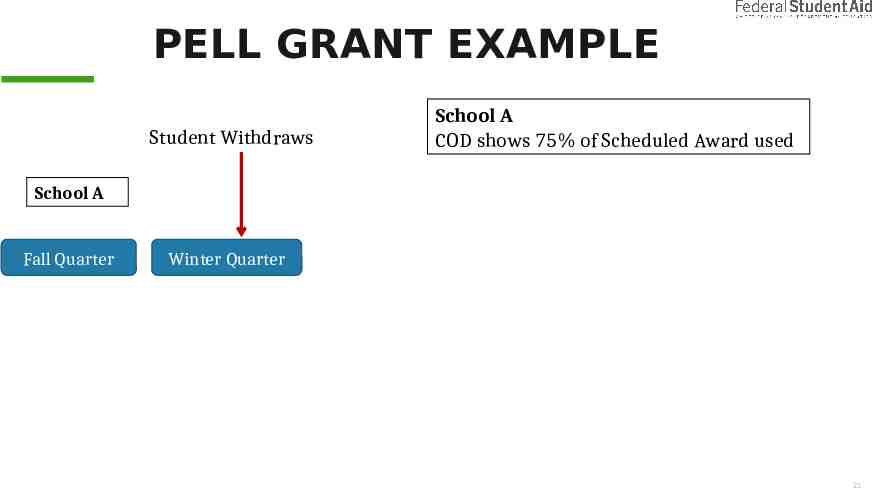

PELL GRANT EXAMPLE Student Withdraws School A COD shows 75% of Scheduled Award used School A Fall Quarter Winter Quarter 21

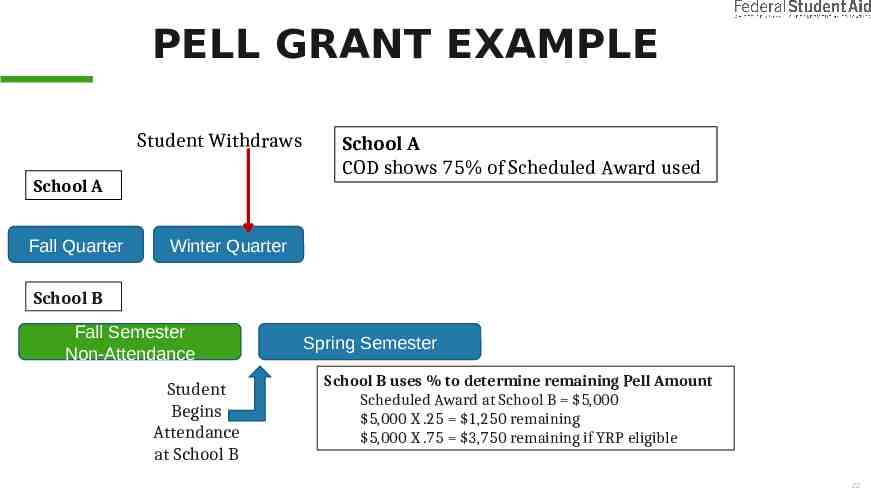

PELL GRANT EXAMPLE Student Withdraws School A Fall Quarter School A COD shows 75% of Scheduled Award used Winter Quarter School B Fall Semester Non-Attendance Student Begins Attendance at School B Spring Semester School B uses % to determine remaining Pell Amount Scheduled Award at School B 5,000 5,000 X .25 1,250 remaining 5,000 X .75 3,750 remaining if YRP eligible 22

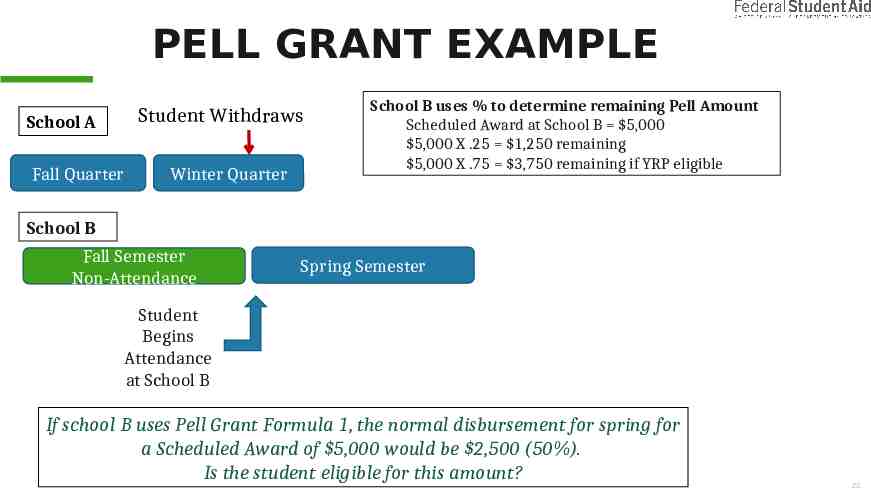

PELL GRANT EXAMPLE School A Fall Quarter Student Withdraws Winter Quarter School B uses % to determine remaining Pell Amount Scheduled Award at School B 5,000 5,000 X .25 1,250 remaining 5,000 X .75 3,750 remaining if YRP eligible School B Fall Semester Non-Attendance Spring Semester Student Begins Attendance at School B If school B uses Pell Grant Formula 1, the normal disbursement for spring for a Scheduled Award of 5,000 would be 2,500 (50%). Is the student eligible for this amount? 23

WHY ALL THESE STEPS? To ensure the annual Federal Pell Grant limits are not exceeded. 24

ADMINISTERING FEDERAL DIRECT LOANS 25

APPROACHING DIRECT LOAN CALCULATIONS Always approach Direct Loan awards from an academic year perspective Use the appropriate annual loan limit for the grade level the student has achieved at your school The period of time for which the Direct Loan is intended may be an academic year or some other period of time, and is referred to as the loan period 26

MINIMUM LOAN PERIODS For credit-hour programs offered in standard terms, or non-standard terms with substantially equal terms of at least nine weeks in length (SE9W), the minimum loan period is the term For clock-hour or non-term credit-hour programs, or non-standardterm programs with terms that are not SE9W, the minimum loan period is the lesser of: The length of the program (if program is shorter than an academic year); The remaining portion of the program (if remaining portion is shorter than an academic year); or The academic year established by the school 27

ACADEMIC YEARS Academic years are defined by the school, but must be at least the minimum length established in the Higher Education Act: Semester or Trimester 30 weeks and 24 credit-hours Quarter 30 weeks and 36 credit-hours Clock Hour 26 weeks and 900 clock-hours 28

ACADEMIC YEARS A borrower is restricted to receiving no more than the annual loan limit amount in any given academic year When the borrower reaches the end of an academic year, and the next academic year begins, the borrower may access the new annual loan limit 29

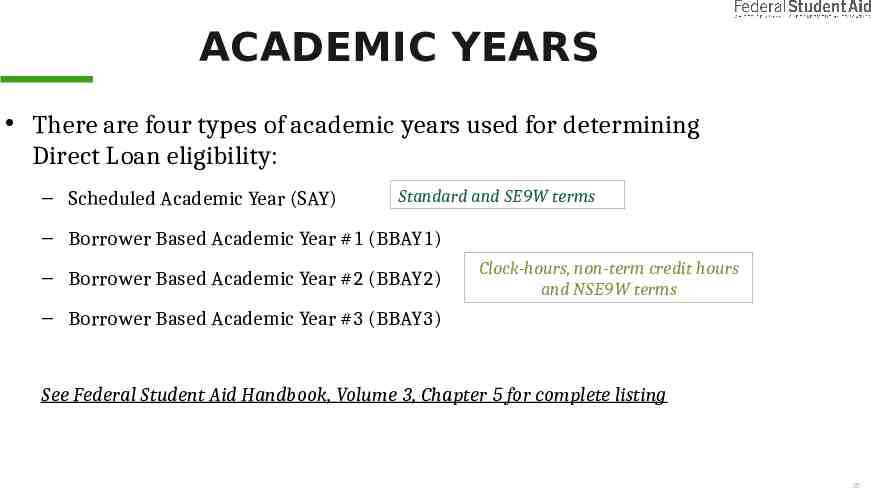

ACADEMIC YEARS There are four types of academic years used for determining Direct Loan eligibility: ‒ Scheduled Academic Year (SAY) Standard and SE9W terms ‒ Borrower Based Academic Year #1 (BBAY1) ‒ Borrower Based Academic Year #2 (BBAY2) Clock-hours, non-term credit hours and NSE9W terms ‒ Borrower Based Academic Year #3 (BBAY3) See Federal Student Aid Handbook, Volume 3, Chapter 5 for complete listing 30

OVERLAPPING ACADEMIC YEARS If a student transfers from one school to another school or changes to a different program at the same school, there may be an overlap of academic years The overlap may affect the amount that the student is eligible to borrow at the new school or for the new program 31

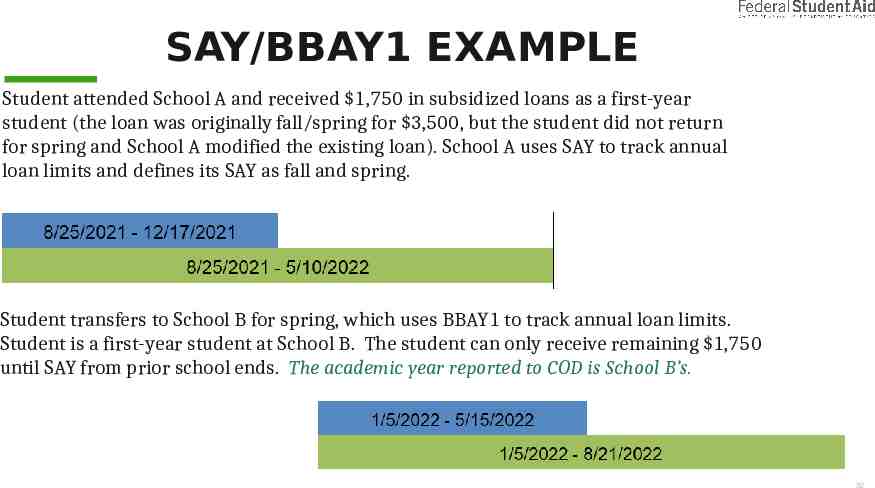

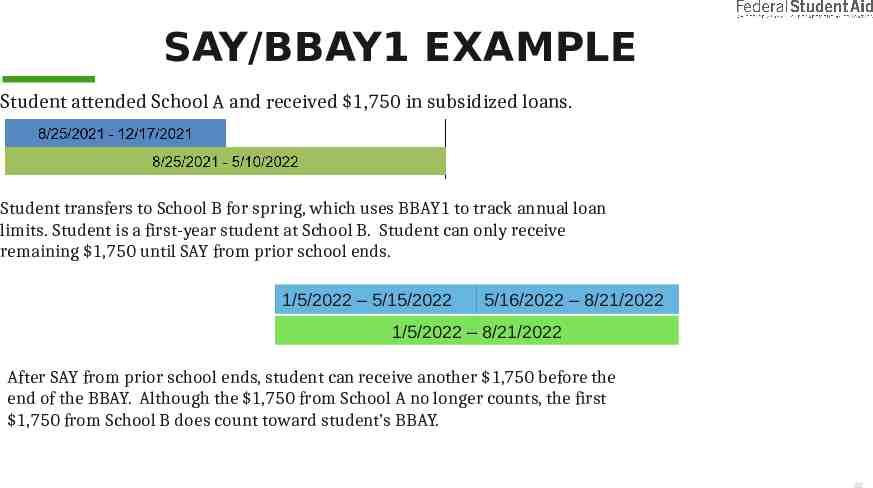

SAY/BBAY1 EXAMPLE Student attended School A and received 1,750 in subsidized loans as a first-year student (the loan was originally fall/spring for 3,500, but the student did not return for spring and School A modified the existing loan). School A uses SAY to track annual loan limits and defines its SAY as fall and spring. Student transfers to School B for spring, which uses BBAY1 to track annual loan limits. Student is a first-year student at School B. The student can only receive remaining 1,750 until SAY from prior school ends. The academic year reported to COD is School B’s. 32

SAY/BBAY1 EXAMPLE Student attended School A and received 1,750 in subsidized loans. Student transfers to School B for spring, which uses BBAY1 to track annual loan limits. Student is a first-year student at School B. Student can only receive remaining 1,750 until SAY from prior school ends. 1/5/2022 – 5/15/2022 5/16/2022 – 8/21/2022 1/5/2022 – 8/21/2022 After SAY from prior school ends, student can receive another 1,750 before the end of the BBAY. Although the 1,750 from School A no longer counts, the first 1,750 from School B does count toward student’s BBAY. 33

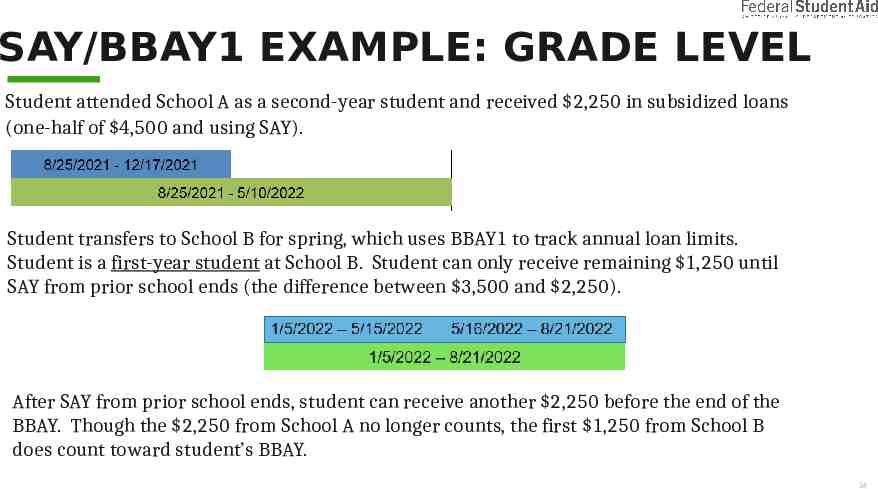

SAY/BBAY1 EXAMPLE: GRADE LEVEL Student attended School A as a second-year student and received 2,250 in subsidized loans (one-half of 4,500 and using SAY). Student transfers to School B for spring, which uses BBAY1 to track annual loan limits. Student is a first-year student at School B. Student can only receive remaining 1,250 until SAY from prior school ends (the difference between 3,500 and 2,250). After SAY from prior school ends, student can receive another 2,250 before the end of the BBAY. Though the 2,250 from School A no longer counts, the first 1,250 from School B does count toward student’s BBAY. 34

BBAY3 AND ABBREVIATED LOAN PERIODS When a student transfers to a school using BBAY3 and the academic years overlap, School B must formally complete School A’s academic year before the student may access a new loan limit. However, the period to complete School A’s year may not meet the regular definition of a minimum loan period. This is called an abbreviated loan period. 35

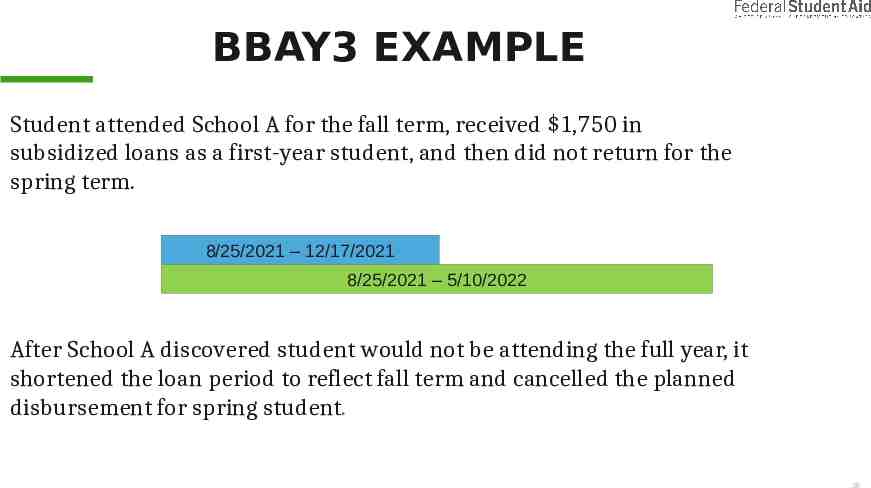

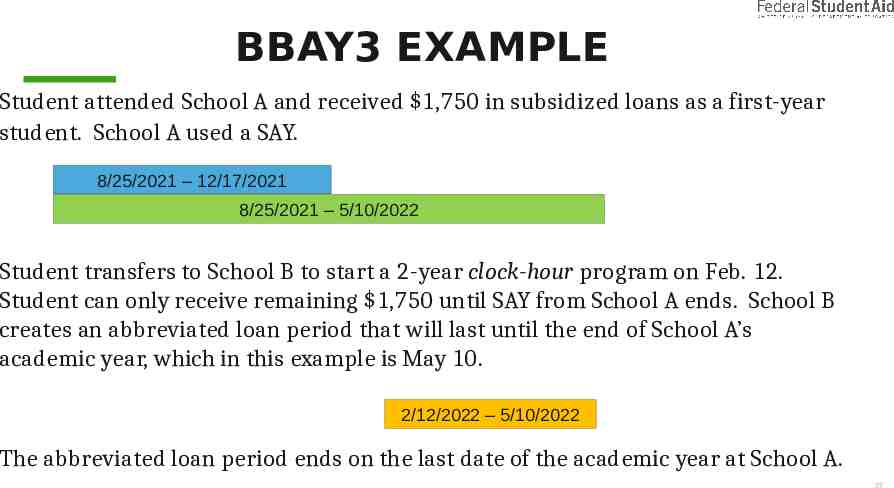

BBAY3 EXAMPLE Student attended School A for the fall term, received 1,750 in subsidized loans as a first-year student, and then did not return for the spring term. 8/25/2021 – 12/17/2021 8/25/2021 – 5/10/2022 After School A discovered student would not be attending the full year, it shortened the loan period to reflect fall term and cancelled the planned disbursement for spring student. 36

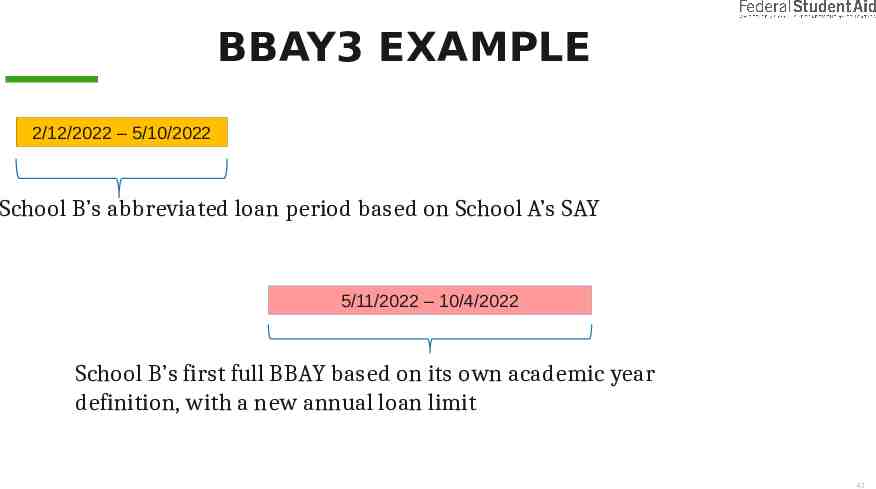

BBAY3 EXAMPLE Student attended School A and received 1,750 in subsidized loans as a first-year student. School A used a SAY. 8/25/2021 – 12/17/2021 8/25/2021 – 5/10/2022 Student transfers to School B to start a 2-year clock-hour program on Feb. 12. Student can only receive remaining 1,750 until SAY from School A ends. School B creates an abbreviated loan period that will last until the end of School A’s academic year, which in this example is May 10. 2/12/2022 – 5/10/2022 The abbreviated loan period ends on the last date of the academic year at School A. 37

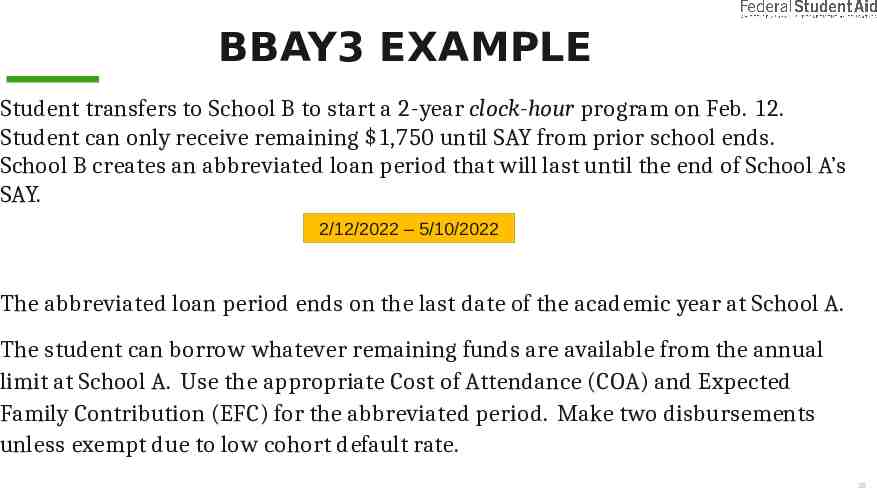

BBAY3 EXAMPLE Student transfers to School B to start a 2-year clock-hour program on Feb. 12. Student can only receive remaining 1,750 until SAY from prior school ends. School B creates an abbreviated loan period that will last until the end of School A’s SAY. 2/12/2022 – 5/10/2022 The abbreviated loan period ends on the last date of the academic year at School A. The student can borrow whatever remaining funds are available from the annual limit at School A. Use the appropriate Cost of Attendance (COA) and Expected Family Contribution (EFC) for the abbreviated period. Make two disbursements unless exempt due to low cohort default rate. 38

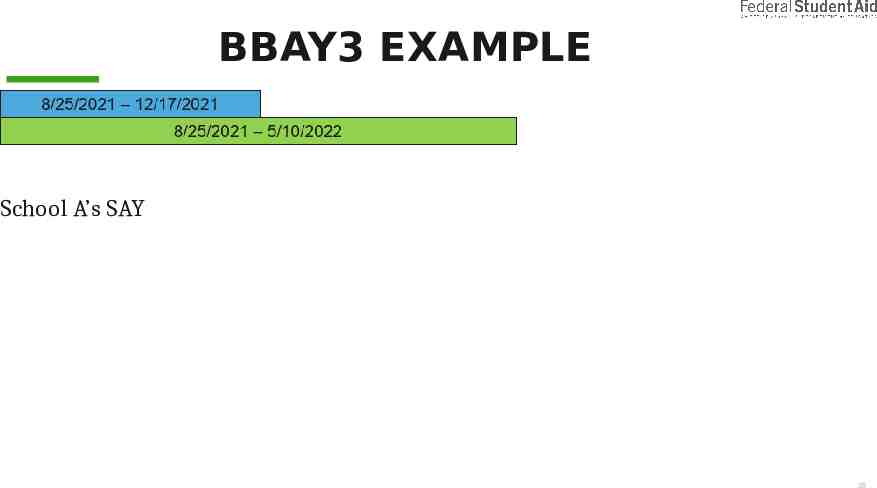

BBAY3 EXAMPLE School A’s SAY 39

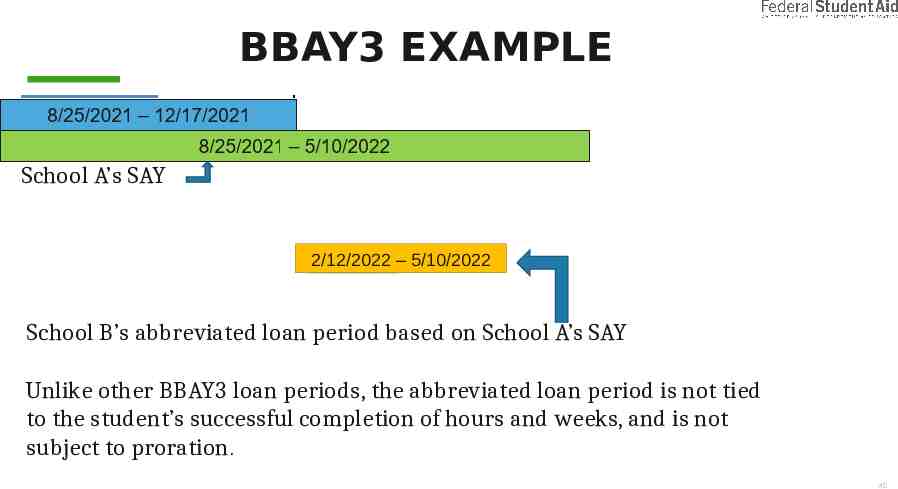

BBAY3 EXAMPLE School A’s SAY 2/12/2022 – 5/10/2022 School B’s abbreviated loan period based on School A’s SAY Unlike other BBAY3 loan periods, the abbreviated loan period is not tied to the student’s successful completion of hours and weeks, and is not subject to proration. 40

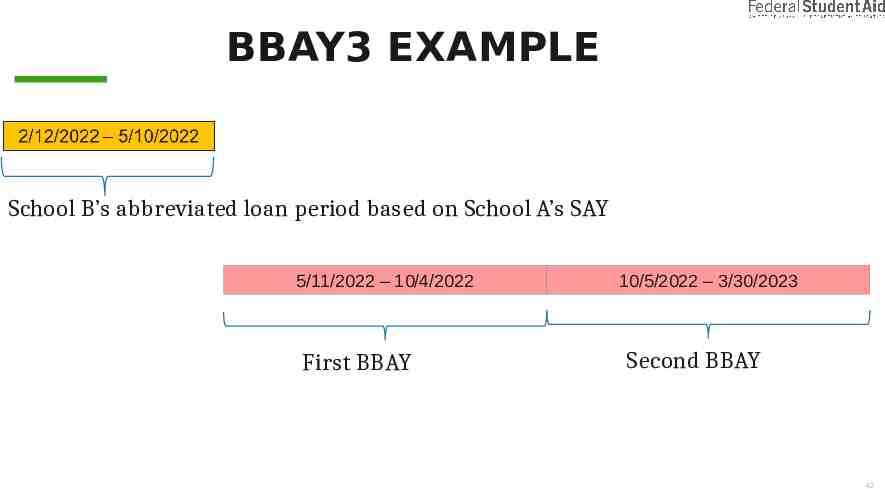

BBAY3 EXAMPLE 2/12/2022 – 5/10/2022 School B’s abbreviated loan period based on School A’s SAY 5/11/2022 – 10/4/2022 School B’s first full BBAY based on its own academic year definition, with a new annual loan limit 41

BBAY3 EXAMPLE School B’s abbreviated loan period based on School A’s SAY 5/11/2022 – 10/4/2022 First BBAY 10/5/2022 – 3/30/2023 Second BBAY 42

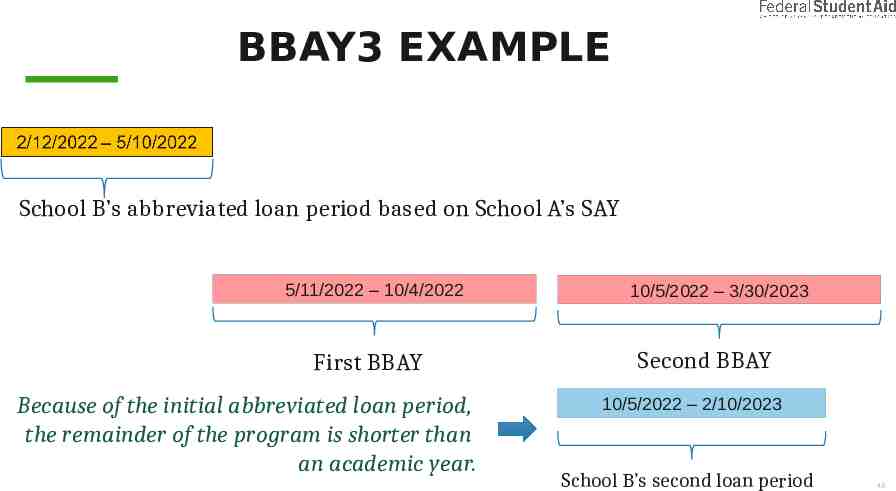

BBAY3 EXAMPLE School B’s abbreviated loan period based on School A’s SAY 5/11/2022 – 10/4/2022 First BBAY Because of the initial abbreviated loan period, the remainder of the program is shorter than an academic year. 10/5/2022 – 3/30/2023 Second BBAY 10/5/2022 – 2/10/2023 School B’s second loan period 43

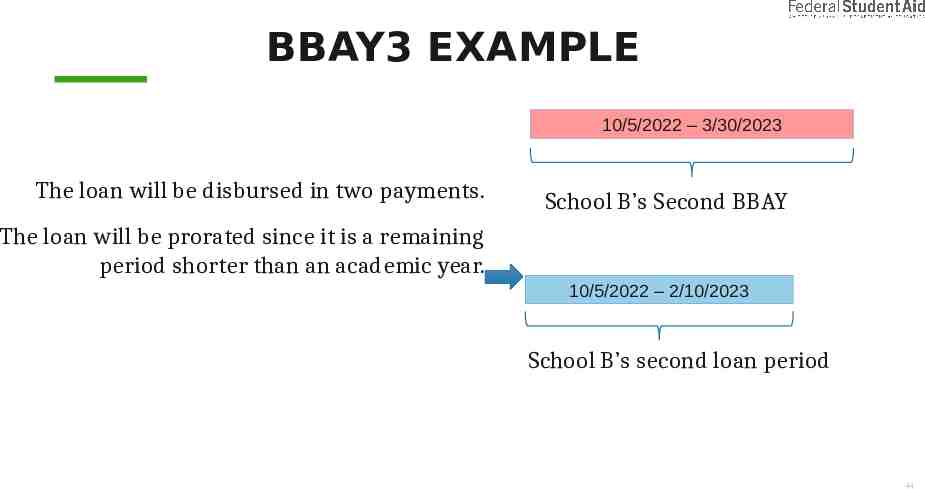

BBAY3 EXAMPLE 10/5/2022 – 3/30/2023 The loan will be disbursed in two payments. School B’s Second BBAY The loan will be prorated since it is a remaining period shorter than an academic year. 10/5/2022 – 2/10/2023 School B’s second loan period 44

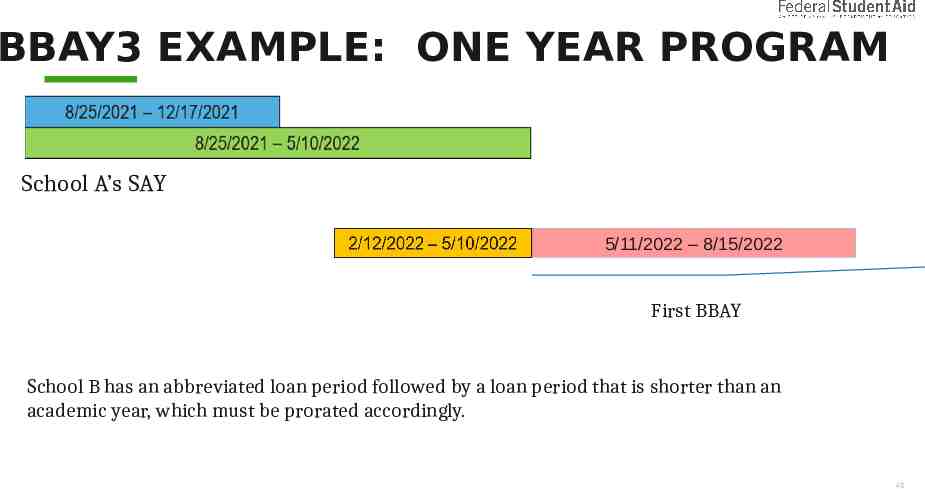

BBAY3 EXAMPLE: ONE YEAR PROGRAM School A’s SAY 5/11/2022 – 8/15/2022 First BBAY School B has an abbreviated loan period followed by a loan period that is shorter than an academic year, which must be prorated accordingly. 45

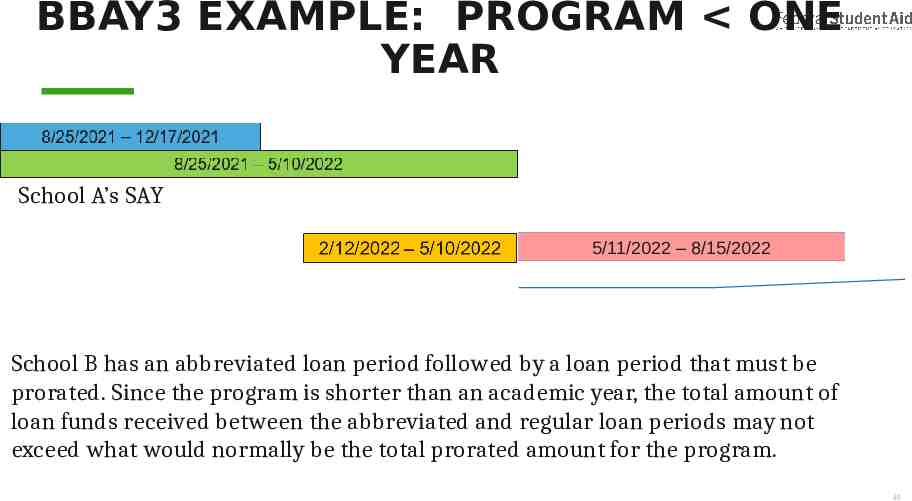

BBAY3 EXAMPLE: PROGRAM ONE YEAR School A’s SAY 5/11/2022 – 8/15/2022 School B has an abbreviated loan period followed by a loan period that must be prorated. Since the program is shorter than an academic year, the total amount of loan funds received between the abbreviated and regular loan periods may not exceed what would normally be the total prorated amount for the program. 46

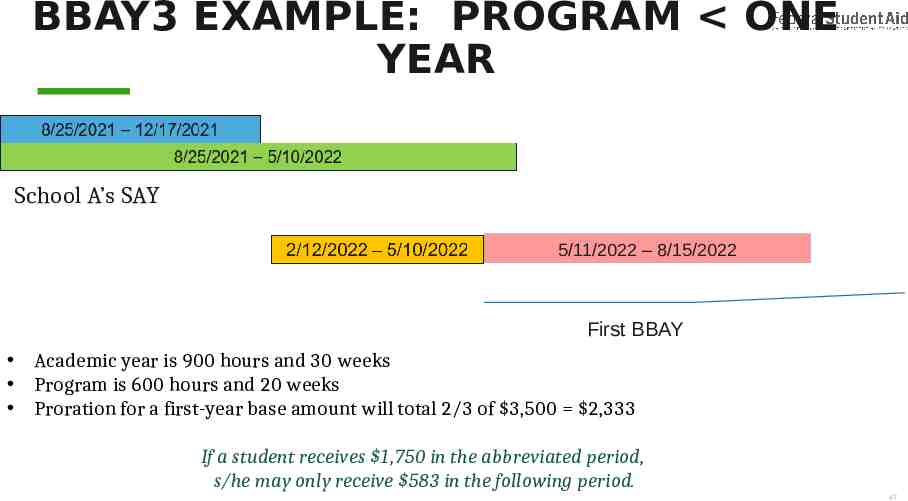

BBAY3 EXAMPLE: PROGRAM ONE YEAR School A’s SAY 5/11/2022 – 8/15/2022 First BBAY Academic year is 900 hours and 30 weeks Program is 600 hours and 20 weeks Proration for a first-year base amount will total 2/3 of 3,500 2,333 If a student receives 1,750 in the abbreviated period, s/he may only receive 583 in the following period. 47

R2T4 AND OVERLAPPING PAYMENT PERIODS 48

OVERLAPPING PAYMENT PERIODS Because payment periods for Pell Grants are defined within an award year and Direct Loan payment periods are defined within an academic year, a student entering into a BBAY 3 environment may appear to have two overlapping payment periods. However, it should be noted that for R2T4 purposes, the school must use a payment period as defined in 668.4(c) when performing the R2T4 calculation. 49

OVERLAPPING PAYMENT PERIODS 668.4(c) defines a payment period as the time it takes the student to complete half the hours and the weeks of instructional time in the program or the defined academic year, whichever is shorter. Therefore, an abbreviated loan period designed to complete a prior school’s academic year does not meet the definition of a payment period as defined in 668.4(c) and should not be used for R2T4 calculation purposes. 50

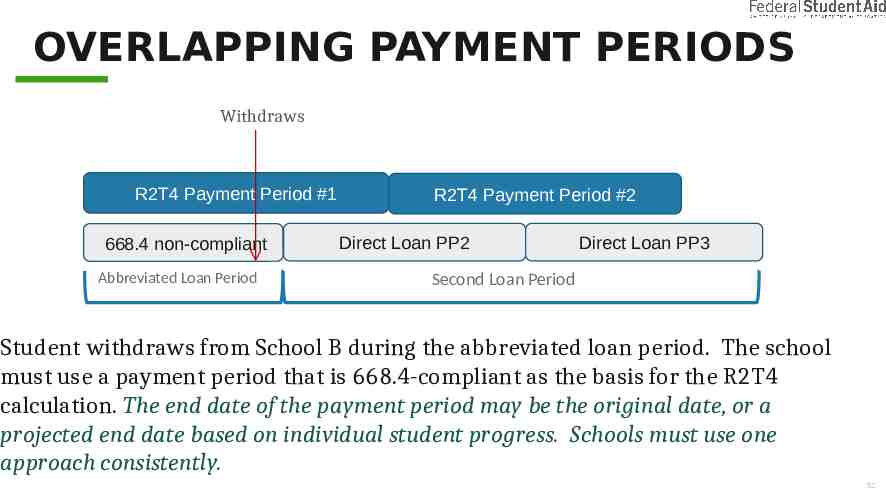

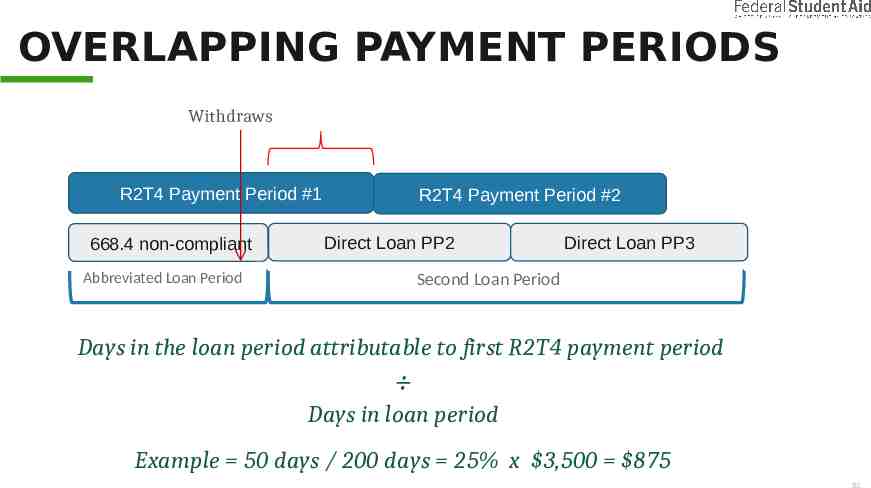

OVERLAPPING PAYMENT PERIODS Withdraws R2T4 Payment Period #1 668.4 non-compliant Abbreviated Loan Period R2T4 Payment Period #2 Direct Loan PP2 Direct Loan PP3 Second Loan Period Student withdraws from School B during the abbreviated loan period. The school must use a payment period that is 668.4-compliant as the basis for the R2T4 calculation. The end date of the payment period may be the original date, or a projected end date based on individual student progress. Schools must use one approach consistently. 51

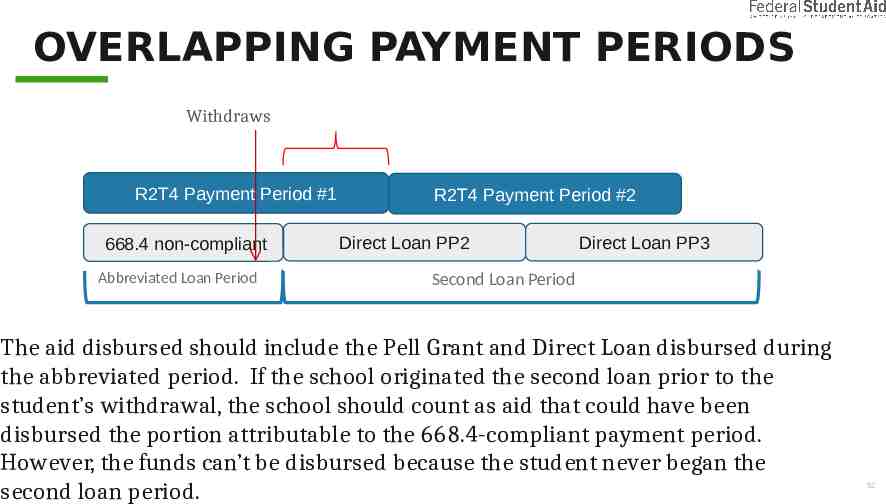

OVERLAPPING PAYMENT PERIODS Withdraws R2T4 Payment Period #1 668.4 non-compliant Abbreviated Loan Period R2T4 Payment Period #2 Direct Loan PP2 Direct Loan PP3 Second Loan Period The aid disbursed should include the Pell Grant and Direct Loan disbursed during the abbreviated period. If the school originated the second loan prior to the student’s withdrawal, the school should count as aid that could have been disbursed the portion attributable to the 668.4-compliant payment period. However, the funds can’t be disbursed because the student never began the second loan period. 52

OVERLAPPING PAYMENT PERIODS Withdraws R2T4 Payment Period #1 668.4 non-compliant R2T4 Payment Period #2 Direct Loan PP2 Abbreviated Loan Period Direct Loan PP3 Second Loan Period Days in the loan period attributable to first R2T4 payment period Days in loan period Example 50 days / 200 days 25% x 3,500 875 53

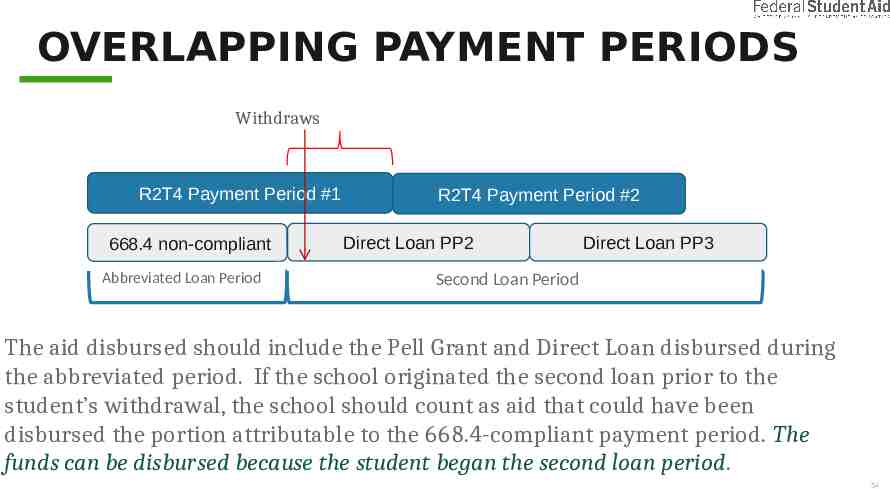

OVERLAPPING PAYMENT PERIODS Withdraws R2T4 Payment Period #1 668.4 non-compliant Abbreviated Loan Period R2T4 Payment Period #2 Direct Loan PP2 Direct Loan PP3 Second Loan Period The aid disbursed should include the Pell Grant and Direct Loan disbursed during the abbreviated period. If the school originated the second loan prior to the student’s withdrawal, the school should count as aid that could have been disbursed the portion attributable to the 668.4-compliant payment period. The funds can be disbursed because the student began the second loan period. 54

RESOURCES 55

REFERENCES NSLDS Transfer Monitoring/Financial Aid History Batch File Layouts (October 2019) ‒ Knowledge Center Home / Library / NSLDS User Resources Transfer Students in the FSA Handbook ‒ ‒ ‒ ‒ General: Volume 3, Chapter 1 Pell: Volume 3, Chapter 3 Direct Loans: Volume 3, Chapter 5 Withdrawals: Volume 5, Chapter 1 Regulations ‒ 34 CFR 668.22 ‒ 34 CFR 685.301 ‒ 34 CFR 690.85 56

QUESTIONS? [email protected] 57