Accelerating Care and Payment Innovation: The CMS Innovation Center

15 Slides2.78 MB

Accelerating Care and Payment Innovation: The CMS Innovation Center

Thank You For the hard work you are doing to improve your care systems every day For your commitment to health care reform, innovation and transformation 2

Health Care Innovation: One Patient’s Story Marie Jones, a high risk patient, with her dedicated nurse case manager. “The idea of the program is to keep me healthy, keep me out of the hospital, and keep costs down. I don’t think I would still be here without this program. It has been my lifeline.” – Marie Jones New York Times, June 21, 2010 3

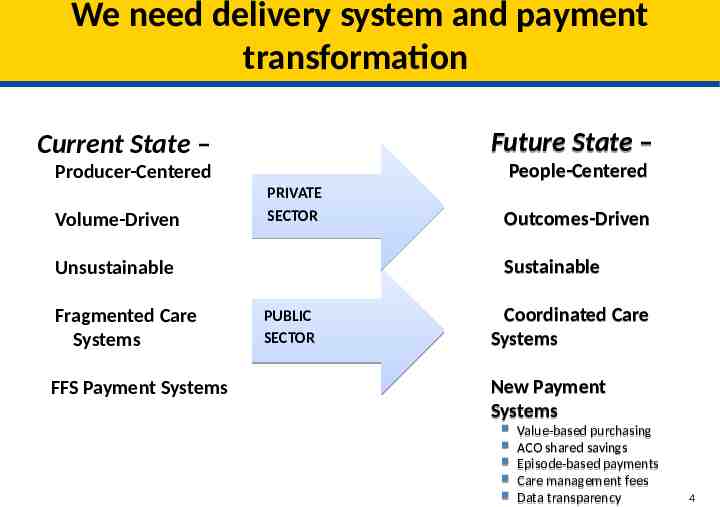

We need delivery system and payment transformation Current State – Future State – Producer-Centered People-Centered Volume-Driven PRIVATE SECTOR Sustainable Unsustainable Fragmented Care Systems FFS Payment Systems Outcomes-Driven PUBLIC SECTOR Coordinated Care Systems New Payment Systems Value-based purchasing ACO shared savings Episode-based payments Care management fees Data transparency 4

Our Strategy: Conduct many model tests to find out what works The Innovation Center portfolio of models will address a wide variety of patient populations, providers, and innovative approaches to payment and service delivery 5

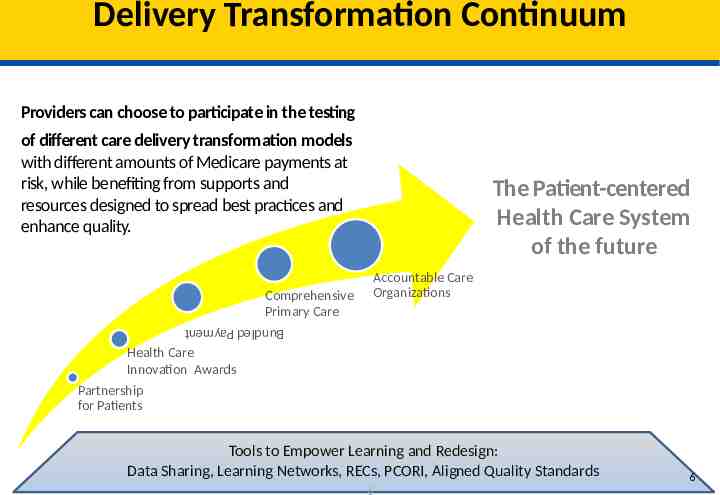

Delivery Transformation Delivery Transformation Continuum Continuum Providers can choose to participate in the testing of different care delivery transformation models with different amounts of Medicare payments at risk, while benefiting from supports and resources designed to spread best practices and enhance quality. The Patient-centered Health Care System of the future Accountable Care Organizations Comprehensive Primary Care Bundled Payment Health Care Innovation Awards Partnership for Patients Tools to Empower Learning and Redesign: Data Sharing, Learning Networks, RECs, PCORI, Aligned Quality Standards 6 6

Providers are Driving Transformation More than 50,000 providers are or will be providing care to beneficiaries as part of the Innovation Center’s current initiatives Over 250 organizations are participating in Medicare ACOs More than 4 million Medicare FFS beneficiaries are receiving care from ACOs More than 1 million Medicare FFS beneficiaries are participating in primary care initiatives 7

million Medicare Medicare beneficiaries beneficiaries having having care care coordinated coordinated by by 44 million 220 SSP SSP and and 32 32 Pioneers Pioneers ACOs ACOs 220 (Geographic Distribution Distribution of of ACO ACO Population) Population) (Geographic 8

The Pioneer ACO Model GOAL: Test payment arrangements with higher risk and reward than MSSP, including partial- and full capitation arrangements, as well as a transition from FFS to population based payments. Designed for health care organizations and providers that are already experienced in coordinating care Requires ACOs to create similar arrangements with other payers. Option for transition from shared savings to population-based payment in Year 3 32 Participating ACOs announced in December 2011 Over 900,000 aligned beneficiaries First performance period began in January 2012. 9

Comprehensive Primary Care Initiative GOAL: Test a multi-payer initiative fostering collaboration between public and private health care payers to strengthen primary care. Collaborating with public and private insurers in purchasing high value primary care in communities they serve. – Requires investment across multiple payers – individual health plans, covering only their members, cannot provide enough resources to transform primary care delivery. Medicare will pay approximately 20 per beneficiary per month (PBPM) then move towards smaller PBPM to be combined with shared savings opportunity. The 7 markets selected: Ohio (Dayton), Oklahoma (Tulsa), Arkansas, Colorado, New Jersey, Oregon, New York (Hudson Valley) 10

Health Care Innovation Awards Round Two GOAL: Test new innovative service delivery and payment models that will deliver better care and lower costs for Medicare, Medicaid, and Children’s Health Insurance Program (CHIP) enrollees. Test models in four categories: 1. Reduce Medicare, Medicaid and/or CHIP expenditures in outpatient and/or post-acute settings 2. Improve care for populations with specialized needs 3. Transform the financial and clinical models for specific types of providers and suppliers 4. Improve the health of populations Letter of Intent due June 28, 2013 Applications due August 15, 2013 11

National Outcomes are Improving 12

We are starting to see results nationally Cost trends are down, Outcomes are Improving & Adverse Events are Falling Total U.S. health spending grew only 3.9 percent in 2011 Medicare 30-day, all-cause readmission rate is estimated to have dropped 1 percent after being at 19 percent for five years 70,000 fewer readmissions in 2012 Expanding coverage with insurance marketplaces gearing up for 2014 13

Results: Medicare Per-Capita Spending Growth at Historic Low 6% 4% 2% 0% 2008-2009 2009-2010 2010-2011 Total Medicare Source: CMS Office of the Actuary, Midsession Review – FY 2013 Budget 2011-2012

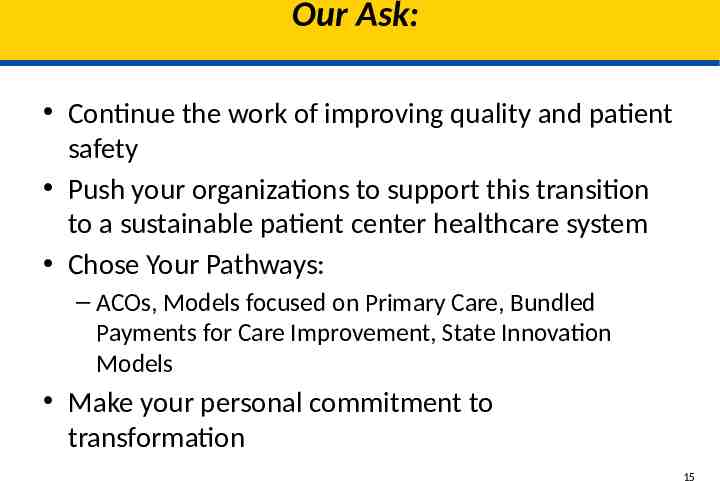

Our Ask: Continue the work of improving quality and patient safety Push your organizations to support this transition to a sustainable patient center healthcare system Chose Your Pathways: – ACOs, Models focused on Primary Care, Bundled Payments for Care Improvement, State Innovation Models Make your personal commitment to transformation 15