A Neural Network Approach to Predict Stock Performance

34 Slides678.00 KB

A Neural Network Approach to Predict Stock Performance Mrutunjaya Rahul Pandey Goutam

Presentation Outline Introduction Problem Description Motivation ECNN Evaluation Empirical study Test Results Conclusion

Introduction Trading is the process of buying and selling of financial instruments Stock market market for the trading one of the most important sources for companies to raise money allows businesses to go public, or raise additional capital for expansion

Incentive Predicting stock performance is a very large and profitable area of study Many companies have developed stock predictors based on neural networks This technique has proven successful in aiding the decisions of investors Can give an edge to beginning investors who don’t have a lifetime of experience

Problem Description Collect a sufficient amount of historical stock data Using the data train a neural network Once trained, the neural network can be used to predict stock behavior

Time Series Analysis Vs NN TS - Instructions and rules are central TS – A Mathematical formula define the dynamics NN - Don't perform according to preset rules. Learns from regularities and sets its own rules NN – Not described explicitly in mathematical terms

Benifits with NN Generalisation ability and robustness Mapping of input/output No assumptions of model has to be made Flexilbilty

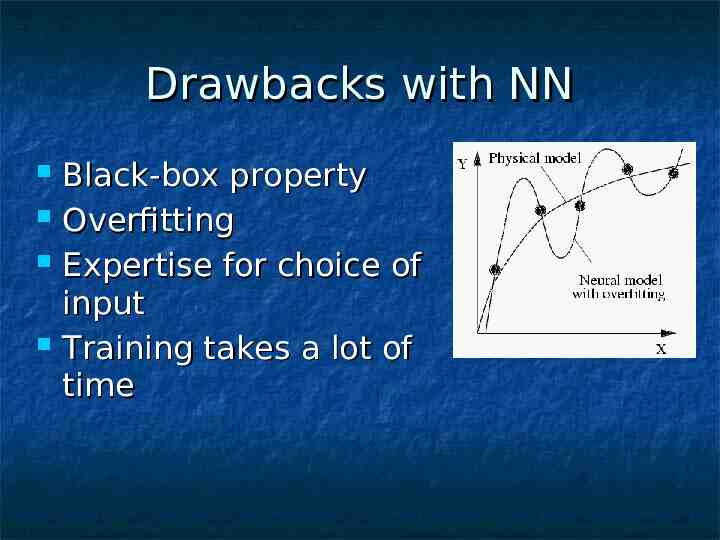

Drawbacks with NN Black-box property Overfitting Expertise for choice of input Training takes a lot of time

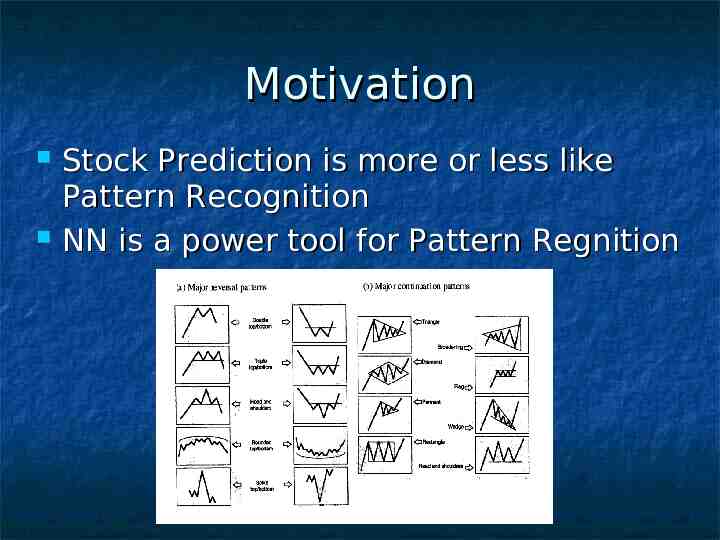

Motivation Stock Prediction is more or less like Pattern Recognition NN is a power tool for Pattern Regnition

Other Reasons Stock data is highly complex and hard to model, therefore a non-linear model is benecial A large set of interacting input series is often required to explain a specfic stock, which suites neural network

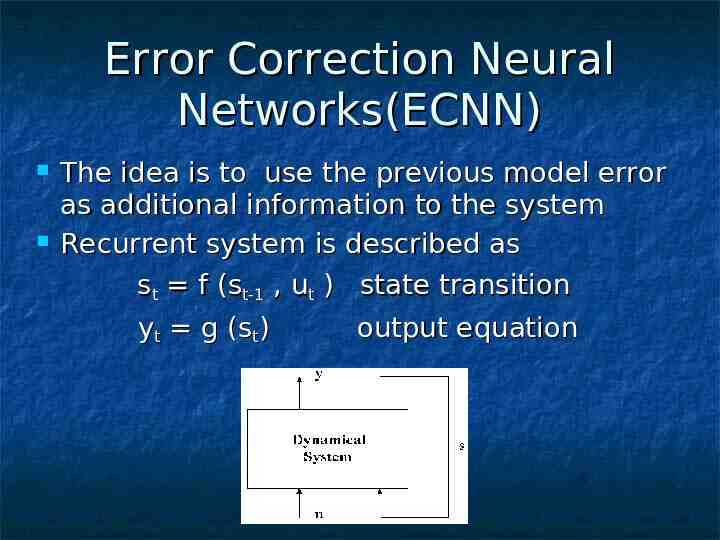

Error Correction Neural Networks(ECNN) The idea is to use the previous model error as additional information to the system Recurrent system is described as st f (st-1 , ut ) state transition yt g (st) output equation

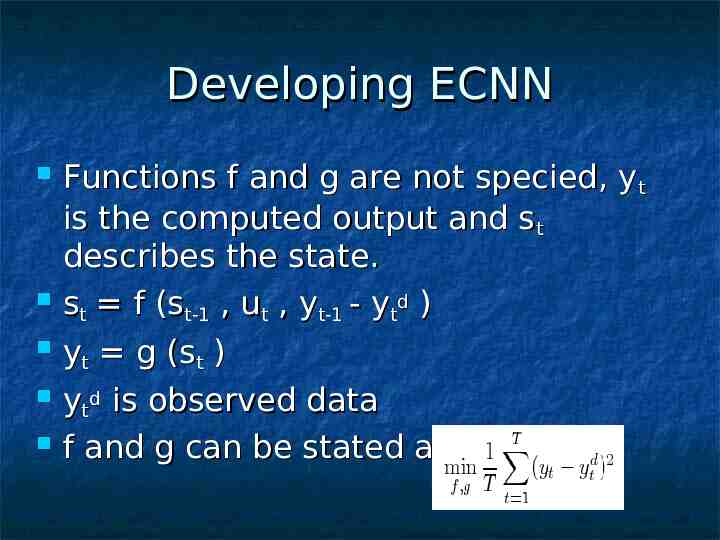

Developing ECNN Functions f and g are not specied, yt is the computed output and st describes the state. st f (st-1 , ut , yt-1 - ytd ) yt g (st ) ytd is observed data f and g can be stated as

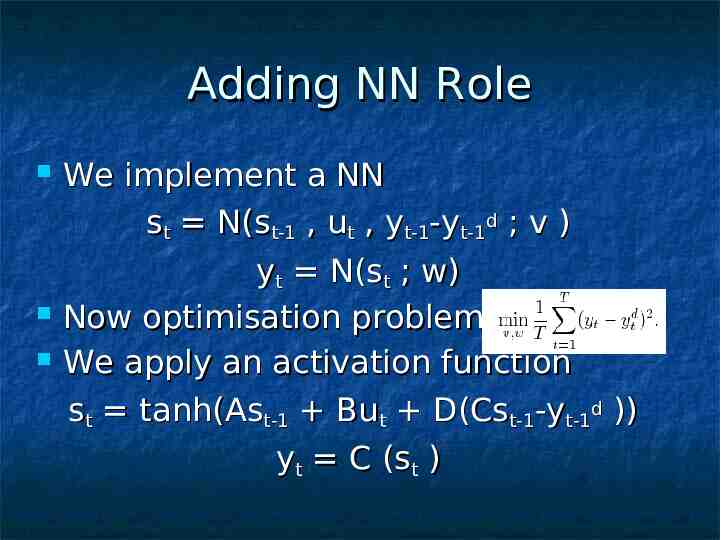

Adding NN Role We implement a NN st N(st-1 , ut , yt-1-yt-1d ; v ) yt N(st ; w) Now optimisation problem is We apply an activation function st tanh(Ast-1 But D(Cst-1-yt-1d )) yt C (st )

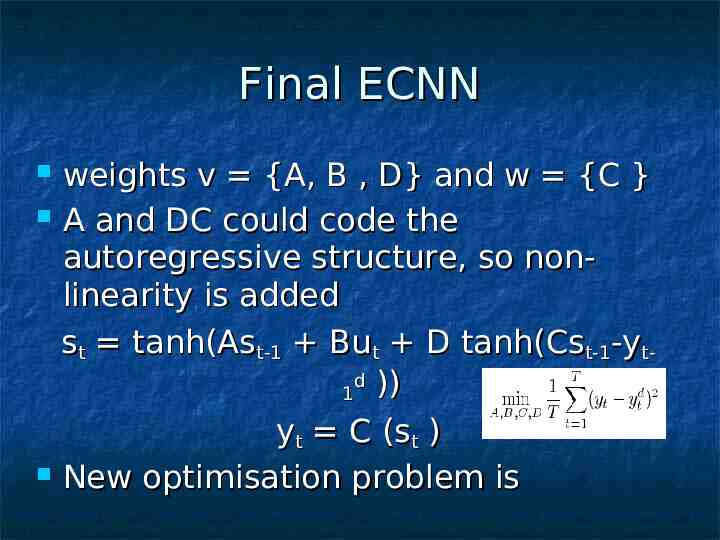

Final ECNN weights v {A, B , D} and w {C } A and DC could code the autoregressive structure, so nonlinearity is added st tanh(Ast-1 But D tanh(Cst-1-ytd 1 )) yt C (st ) New optimisation problem is

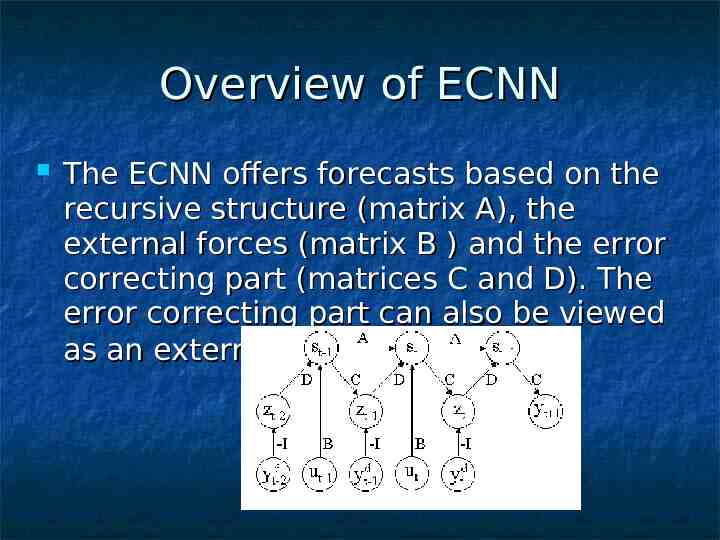

Overview of ECNN The ECNN offers forecasts based on the recursive structure (matrix A), the external forces (matrix B ) and the error correcting part (matrices C and D). The error correcting part can also be viewed as an external input similar to ut .

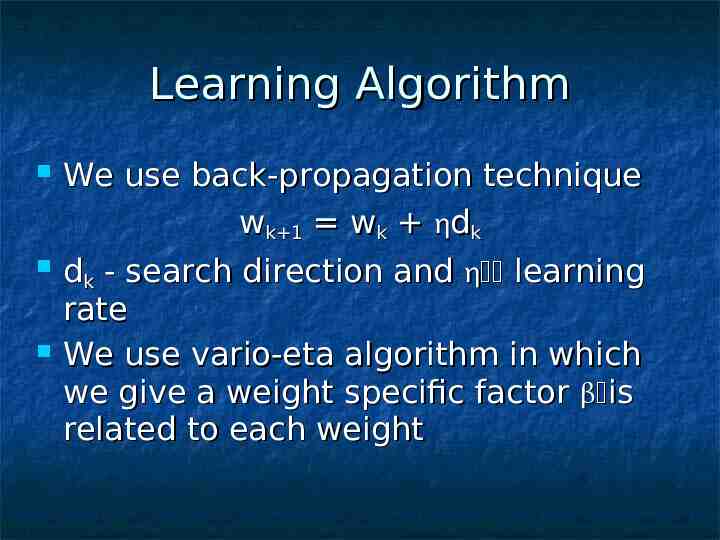

Learning Algorithm We use back-propagation technique wk 1 wk dk dk - search direction and learning rate We use vario-eta algorithm in which we give a weight specific factor is related to each weight

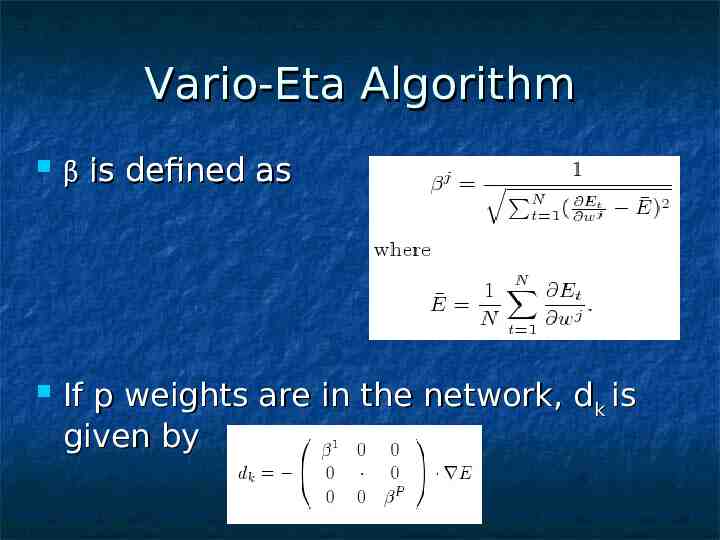

Vario-Eta Algorithm is defined as If p weights are in the network, dk is given by

Stopping Criteria How many epochs? Two paradigms - late and early stopping During learning the progression is monitored and training is terminated as soon as signs of overfitting appear Advantage - the time of training is relatively short Downside - hard to know when to stop

Error Function We have to be aware of outliers in data Outliers typically appear when the economic or political climate is unstable or unexpected information enter the market The ln cosh (.) error function is (1/a) ln cosh(a(oi-ti ) oi - the response from output neuron i and ti - the corresponding target a [3,4] is suitable for financial application

Evaluation A performance method in itself is not sufficient for a satisfying evaluation. Benchmark is a different algorithm used for comparison.

Benchmarks A good prediction algorithm should outperform the naive algorithm, i.e. predicted value of stock in next time step is same as the present value. Naive algorithm is a direct consequence of Efficient Market Hypothesis which states that the current market price is an assimilation of all information available therefore no changes of future changes can be made.

Terms Rkt is the k-step return at time t. The predicted k-step return at time t is given by capped Rkt. sign(x) gives the sign of the x.

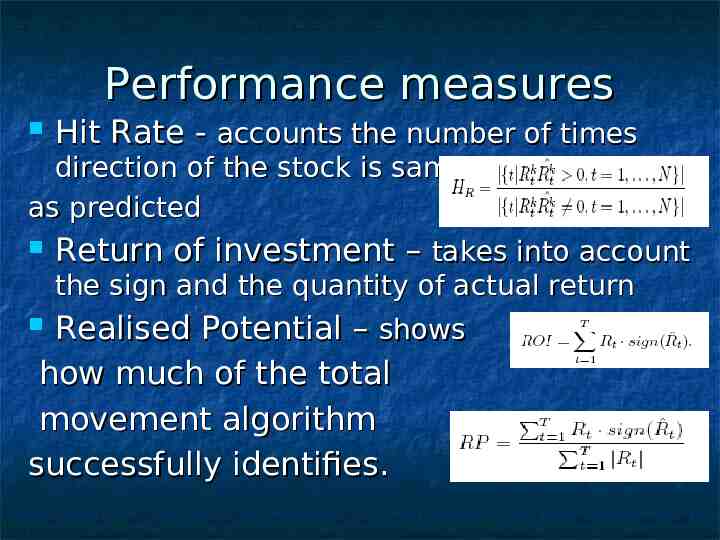

Performance measures Hit Rate - accounts the number of times direction of the stock is same as predicted Return of investment – takes into account the sign and the quantity of actual return Realised Potential – shows how much of the total movement algorithm successfully identifies.

Empirical Study Well traded stocks with a reasonable spread are considered. Certain time invariant structures are identified and learnt quickly so in latter part of the training some weights are frozen. Occurance of invariant structures was more evident in weekly rather than daily structures.

Data series Closing price y Highest price during the day yH . Lowest price during the day yL . Volume V , the total amount of stocks traded during the day.

Training procedure Data was divided into 3 subsets Training set, Validation set, Generalization set. Weights were initialized uniformly in the range [-1,1]. After training waights associated with the best performance in the Validation set were selected and applied to Generalization set to get final results.

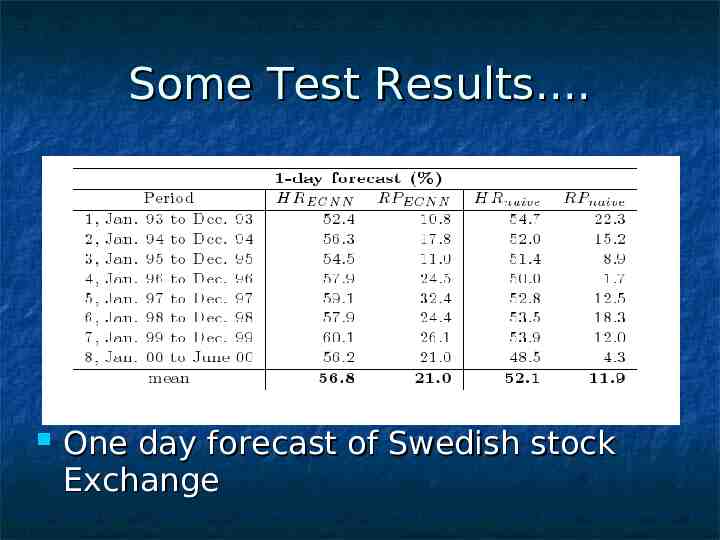

Some Test Results. One day forecast of Swedish stock Exchange

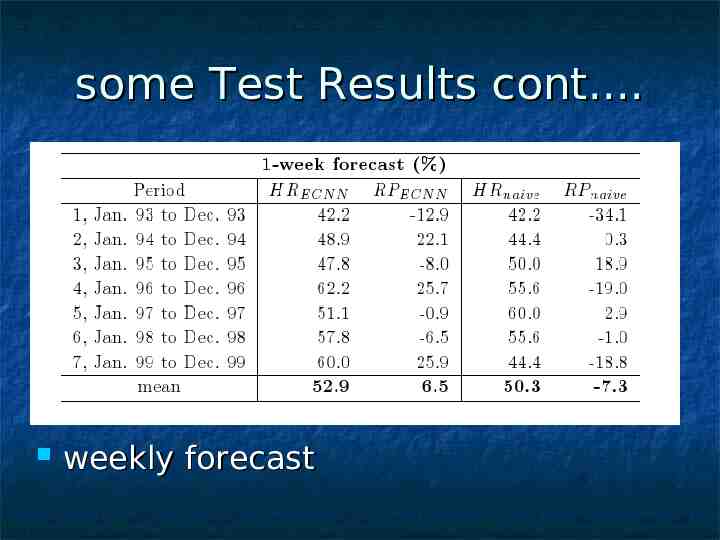

some Test Results cont. weekly forecast

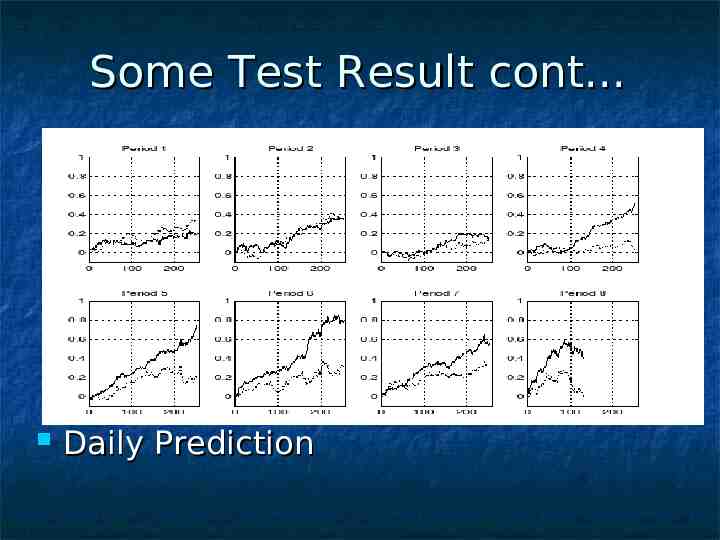

Some Test Result cont. Daily Prediction

success and failures. Adventage Neural network can be trained with a very large amount of data. Years, decades, even centuries Able to consider a “lifetime” worth of data when making a prediction Completely unbiased Disadvantages No way to predict unexpected factors, i.e. natural disaster, legal problems, etc.

Conclusion . No human or computer can perfectly predict the volatile stock market Under “normal” conditions, in most cases, a good neural network will outperform most other current stock market predictors and be a very worthwhile, and potentially profitable aid to investors Should be used as an aid only!

Bibliography. Stock Prediction - A Neural Network Approach - Karl Nygren,KTH,2004 Using Neural Networks to Forecast Stock Market Prices - Ramon Lawrence, 2004 Neural Networks Applications in Finance : A Pratical Introduction – C.R.Krishnaswamy Erika W. Gilbert and Mary M. Pashley

Warning . Stock values are subjected to market risks please read the offer document carefully before investing

Thank you