Wyższa Szkoła Przedsiębiorczości i Zarządzania im. Leona Koźmińskiego

44 Slides850.00 KB

Wyższa Szkoła Przedsiębiorczości i Zarządzania im. Leona Koźmińskiego w Warszawie “Strategic management consulting – the A.T. Kearney perspective” Presentation Warsaw, May 28, 2001 an EDS company

Agenda Overview of management consulting A.T. Kearney as a strategic management consulting firm Consultant’s role in A.T. Kearney The future of management consulting A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 2

Overview of management consulting A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 3

Overview of management consulting Today, one is confronted with a variety of consultants . . . . Tax “consultants” Hair “consultants” Image “consultants” Color “consultants” Catering “consultants” What then, is “management consulting? A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 4

Overview of management consulting One definition . . . . Management consulting assisting management in facilitating change to gain and sustain competitive advantage A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 5

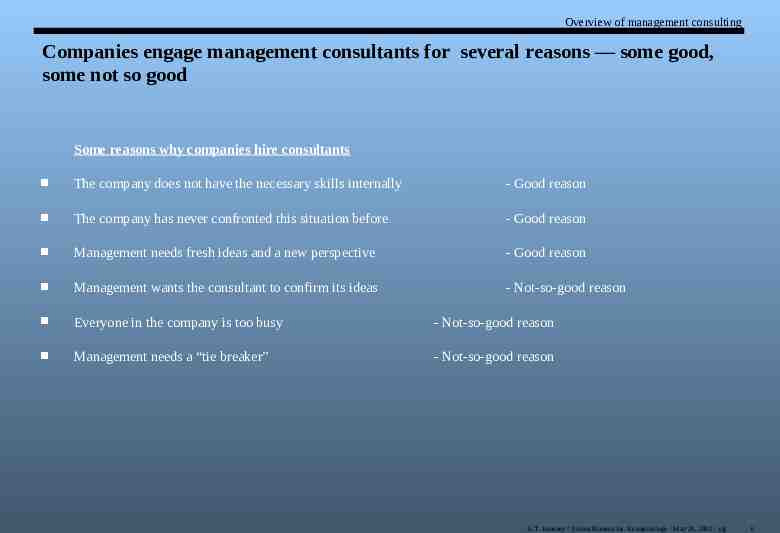

Overview of management consulting Companies engage management consultants for several reasons — some good, some not so good Some reasons why companies hire consultants The company does not have the necessary skills internally - Good reason The company has never confronted this situation before - Good reason Management needs fresh ideas and a new perspective - Good reason Management wants the consultant to confirm its ideas - Not-so-good reason Everyone in the company is too busy - Not-so-good reason Management needs a “tie breaker” - Not-so-good reason A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 6

Overview of management consulting Why does management consulting seem to be growing in importance? The nature of business is changing so rapidly that companies Cannot provide for every eventuality in the organizational structure Find it difficult to maintain permanent staff functions Companies need “tailored” solutions to remain competitive in an increasingly global marketplace The high cost of what management consulting provides can only be justified by companies on an outsourced, as needed basis A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 7

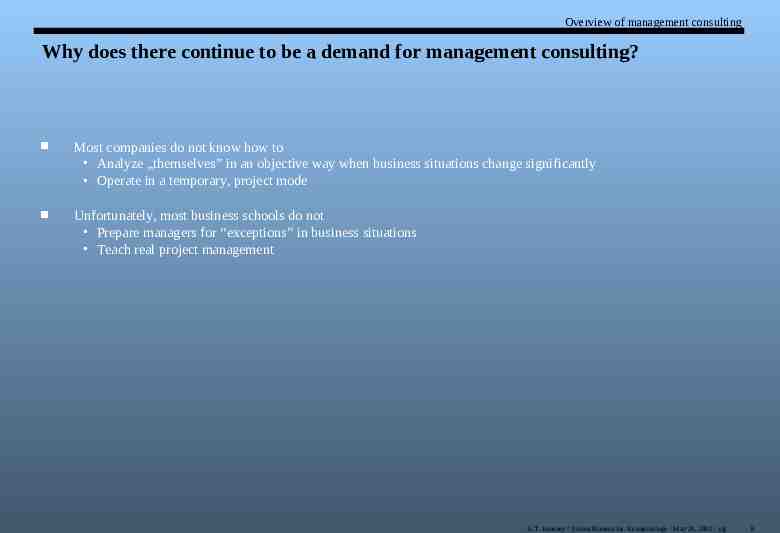

Overview of management consulting Why does there continue to be a demand for management consulting? Most companies do not know how to Analyze „themselves” in an objective way when business situations change significantly Operate in a temporary, project mode Unfortunately, most business schools do not Prepare managers for “exceptions” in business situations Teach real project management A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 8

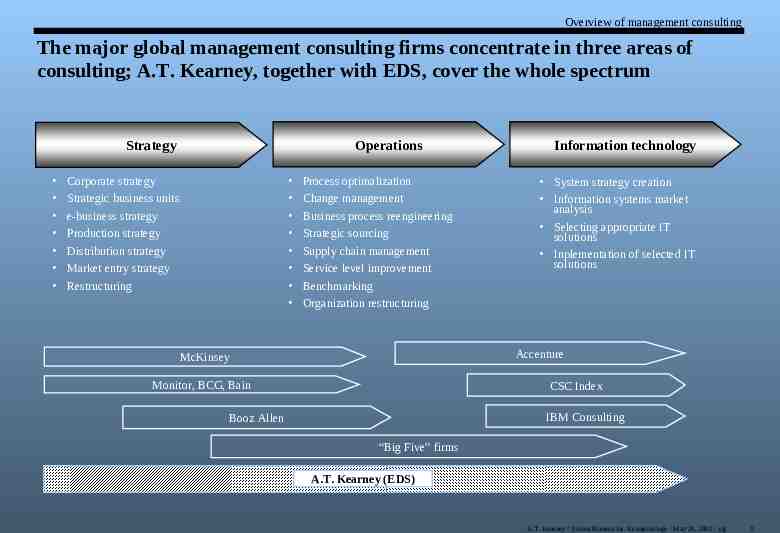

Overview of management consulting The major global management consulting firms concentrate in three areas of consulting; A.T. Kearney, together with EDS, cover the whole spectrum Operations Strategy Corporate strategy Strategic business units e-business strategy Production strategy Distribution strategy Market entry strategy Restructuring Process optimalization Change management Business process reengineering Strategic sourcing Supply chain management Service level improvement Benchmarking Organization restructuring Information technology System strategy creation Information systems market analysis Selecting appropriate IT solutions Inplementation of selected IT solutions Accenture McKinsey Monitor, BCG, Bain CSC Index IBM Consulting Booz Allen “Big Five” firms A.T. Kearney (EDS) A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 9

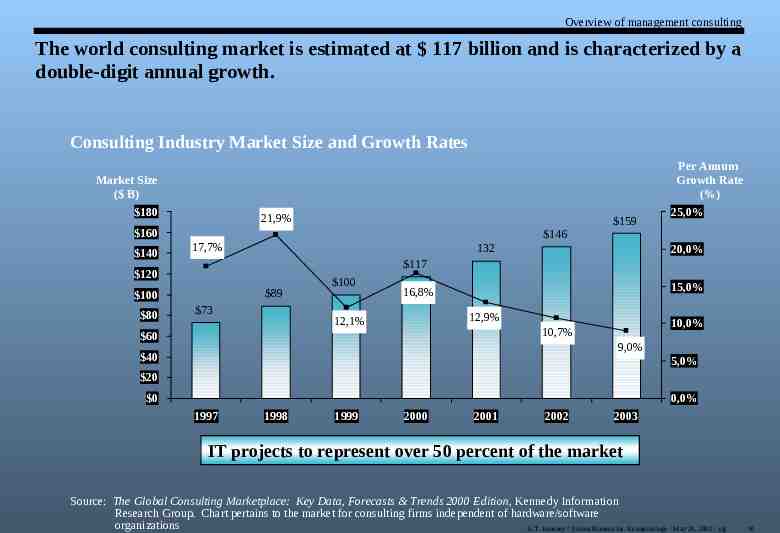

Overview of management consulting The world consulting market is estimated at 117 billion and is characterized by a double-digit annual growth. Consulting Industry Market Size and Growth Rates Market Size ( B) 180 21,9% 159 160 140 146 17,7% 132 20,0% 117 120 89 100 80 Per Annum Growth Rate (%) 25,0% 73 100 15,0% 16,8% 12,9% 12,1% 10,0% 10,7% 60 9,0% 40 5,0% 20 0 0,0% 1997 1998 1999 2000 2001 2002 2003 IT projects to represent over 50 percent of the market Source: The Global Consulting Marketplace: Key Data, Forecasts & Trends 2000 Edition, Kennedy Information Research Group. Chart pertains to the market for consulting firms independent of hardware/software organizations A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 10

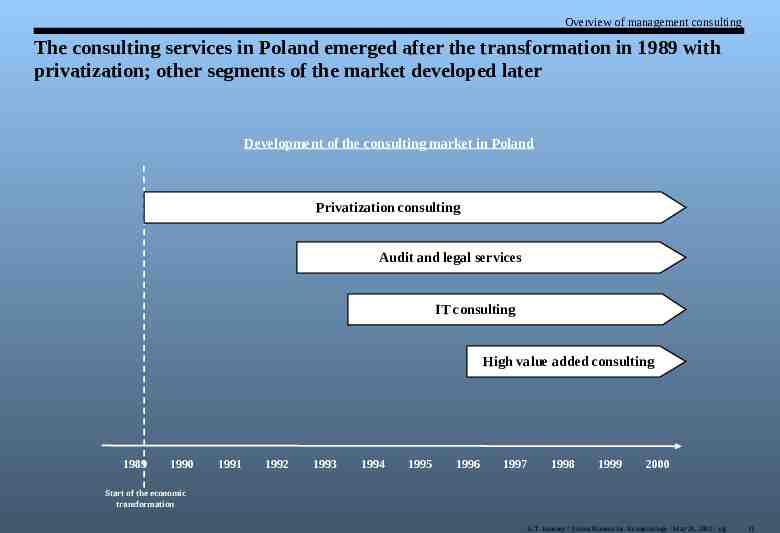

Overview of management consulting The consulting services in Poland emerged after the transformation in 1989 with privatization; other segments of the market developed later Development of the consulting market in Poland Privatization consulting Audit and legal services IT consulting High value added consulting 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 Start of the economic transformation A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 11

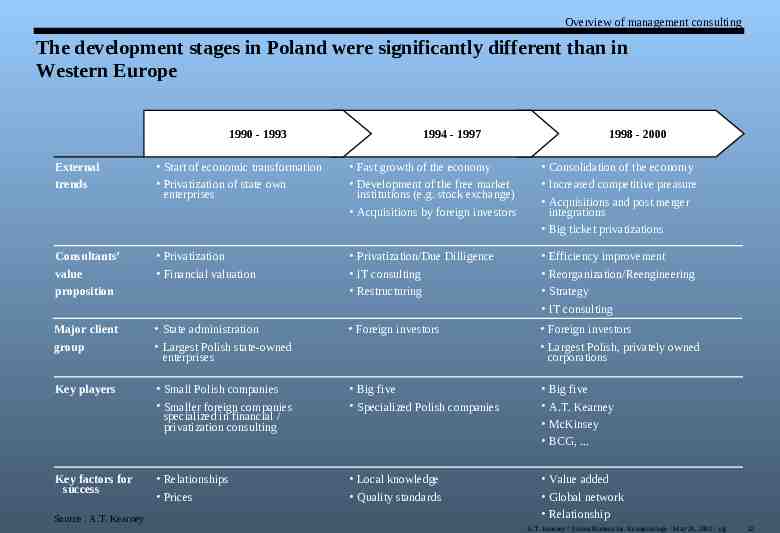

Overview of management consulting The development stages in Poland were significantly different than in Western Europe 1990 - 1993 1994 - 1997 1998 - 2000 External trends Start of economic transformation Privatization of state own enterprises Fast growth of the economy Development of the free market institutions (e.g. stock exchange) Acquisitions by foreign investors Consolidation of the economy Increased competitive preasure Acquisitions and post merger integrations Big ticket privatizations Consultants’ value proposition Privatization Financial valuation Privatization/Due Dilligence IT consulting Restructuring Major client group State administration Largest Polish state-owned enterprises Foreign investors Foreign investors Largest Polish, privately owned corporations Key players Small Polish companies Smaller foreign companies specialized in financial / privatization consulting Big five Specialized Polish companies Key factors for success Relationships Prices Local knowledge Quality standards Value added Global network Relationship Source : A.T. Kearney Efficiency improvement Reorganization/Reengineering Strategy IT consulting Big five A.T. Kearney McKinsey BCG, . A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 12

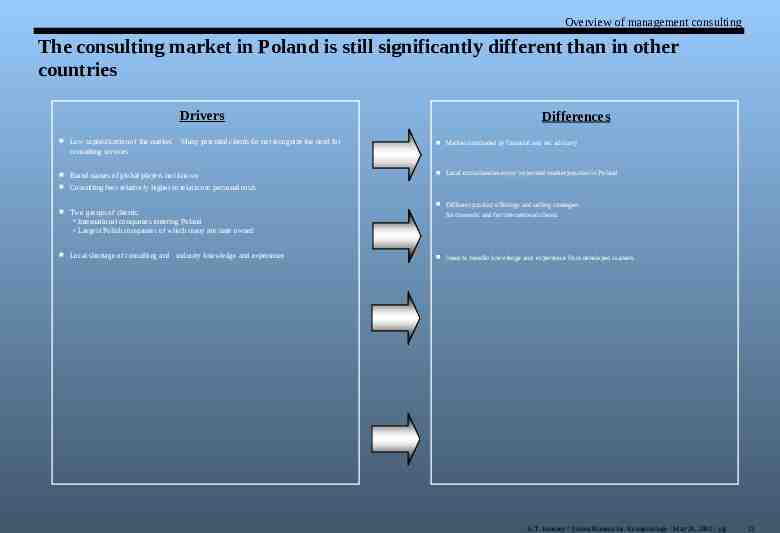

Overview of management consulting The consulting market in Poland is still significantly different than in other countries Drivers Low sophistication of the market. Many potential clients do not recognize the need for consulting services Brand names of global players not known Consulting fees relatively higher in relation to personal costs Two groups of clients: International companies entering Poland Largest Polish companies of which many are state owned Local shortage of consulting and industry knowledge and experience Differences Market dominated by financial and tax advisory Local consultancies enjoy important market position in Poland Different product offerings and selling strategies for domestic and for international clients Need to transfer knowledge and experience from developed markets A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 13

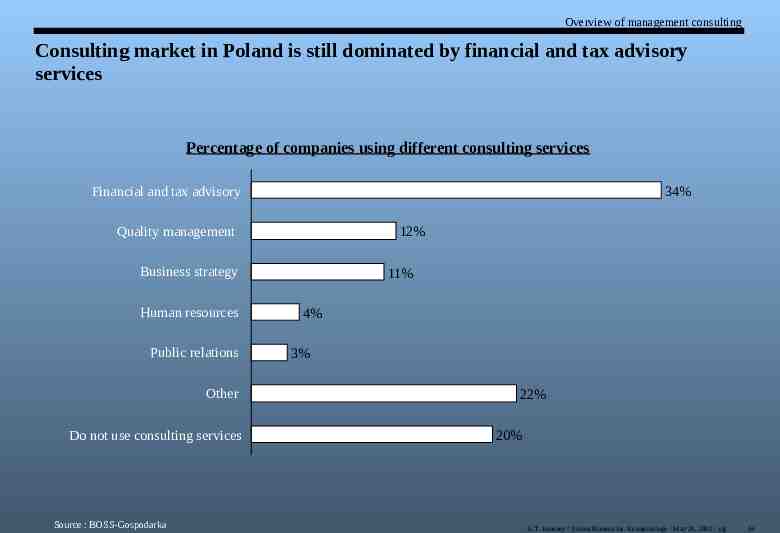

Overview of management consulting Consulting market in Poland is still dominated by financial and tax advisory services Percentage of companies using different consulting services 34% Financial and tax advisory Quality management 12% Business strategy Human resources Public relations Other Do not use consulting services Source : BOSS-Gospodarka 11% 4% 3% 22% 20% A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 14

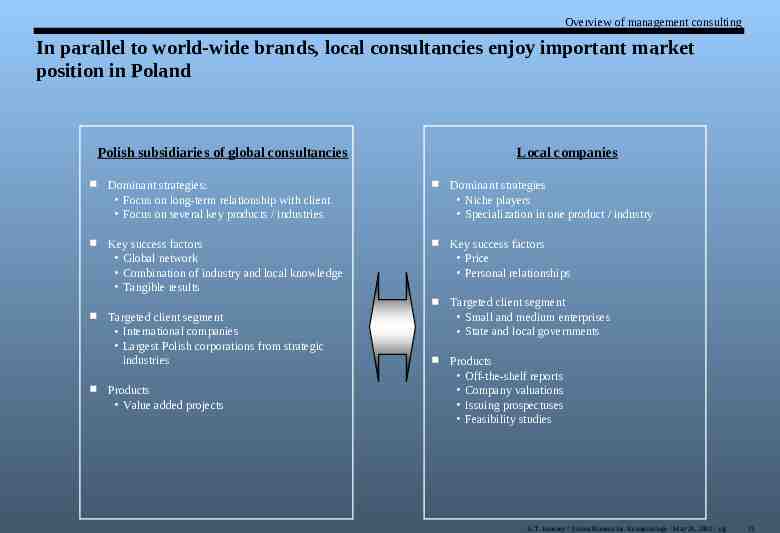

Overview of management consulting In parallel to world-wide brands, local consultancies enjoy important market position in Poland Polish subsidiaries of global consultancies Local companies Dominant strategies: Focus on long-term relationship with client Focus on several key products / industries Dominant strategies Niche players Specialization in one product / industry Key success factors Global network Combination of industry and local knowledge Tangible results Key success factors Price Personal relationships Targeted client segment Small and medium enterprises State and local governments Products Off-the-shelf reports Company valuations Issuing prospectuses Feasibility studies Targeted client segment International companies Largest Polish corporations from strategic industries Products Value added projects A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 15

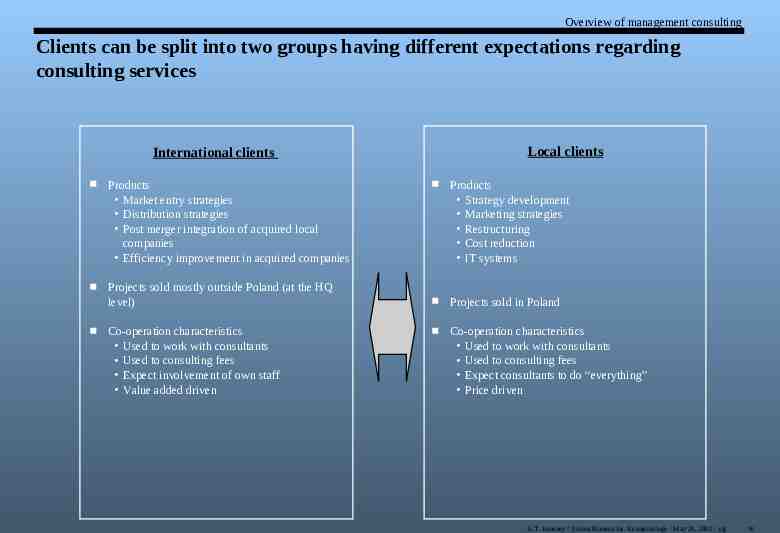

Overview of management consulting Clients can be split into two groups having different expectations regarding consulting services Local clients International clients Products Market entry strategies Distribution strategies Post merger integration of acquired local companies Efficiency improvement in acquired companies Projects sold mostly outside Poland (at the HQ level) Co-operation characteristics Used to work with consultants Used to consulting fees Expect involvement of own staff Value added driven Products Strategy development Marketing strategies Restructuring Cost reduction IT systems Projects sold in Poland Co-operation characteristics Used to work with consultants Used to consulting fees Expect consultants to do “everything” Price driven A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 16

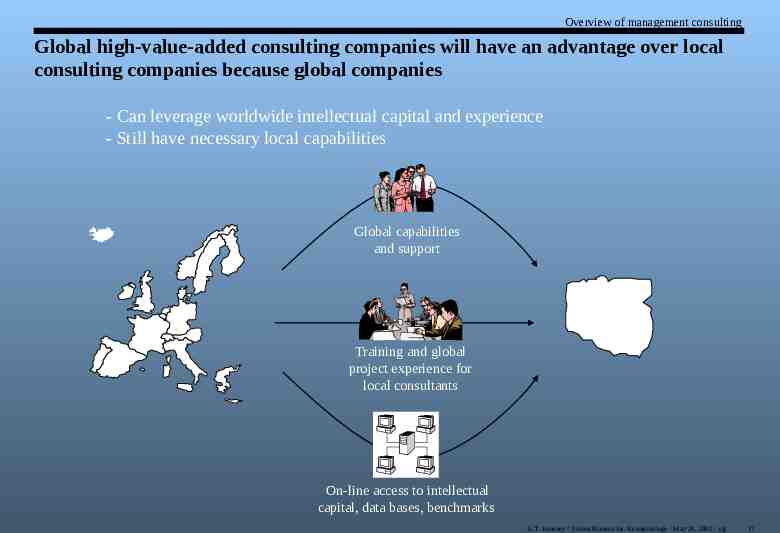

Overview of management consulting Global high-value-added consulting companies will have an advantage over local consulting companies because global companies - Can leverage worldwide intellectual capital and experience - Still have necessary local capabilities Global capabilities and support Training and global project experience for local consultants On-line access to intellectual capital, data bases, benchmarks A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 17

A.T. Kearney as a strategic management consulting firm A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 18

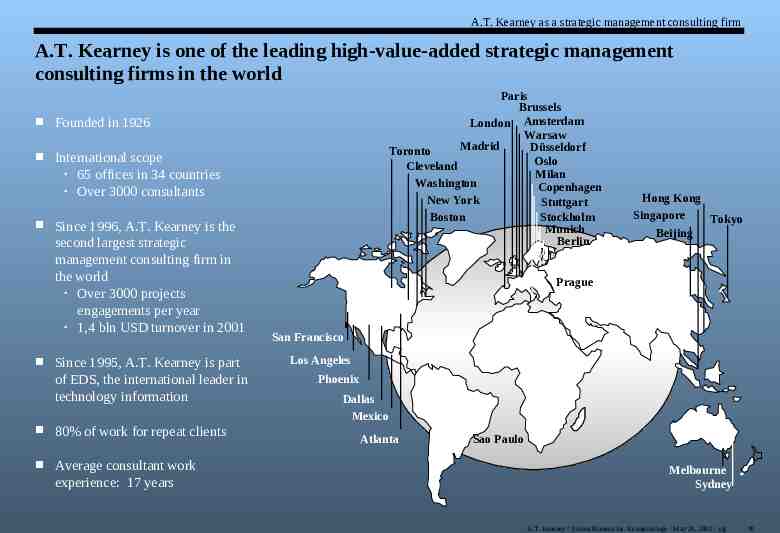

A.T. Kearney as a strategic management consulting firm A.T. Kearney is one of the leading high-value-added strategic management consulting firms in the world Founded in 1926 International scope 65 offices in 34 countries Over 3000 consultants Since 1996, A.T. Kearney is the second largest strategic management consulting firm in the world Over 3000 projects engagements per year 1,4 bln USD turnover in 2001 Since 1995, A.T. Kearney is part of EDS, the international leader in technology information 80% of work for repeat clients Average consultant work experience: 17 years Paris Brussels London Amsterdam Warsaw Madrid Düsseldorf Toronto Oslo Cleveland Milan Washington Copenhagen New York Stuttgart Boston Stockholm Munich Berlin Hong Kong Singapore Tokyo Beijing Prague Chicago San Francisco Los Angeles Phoenix Dallas Mexico Atlanta Sao Paulo Melbourne Sydney A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 19

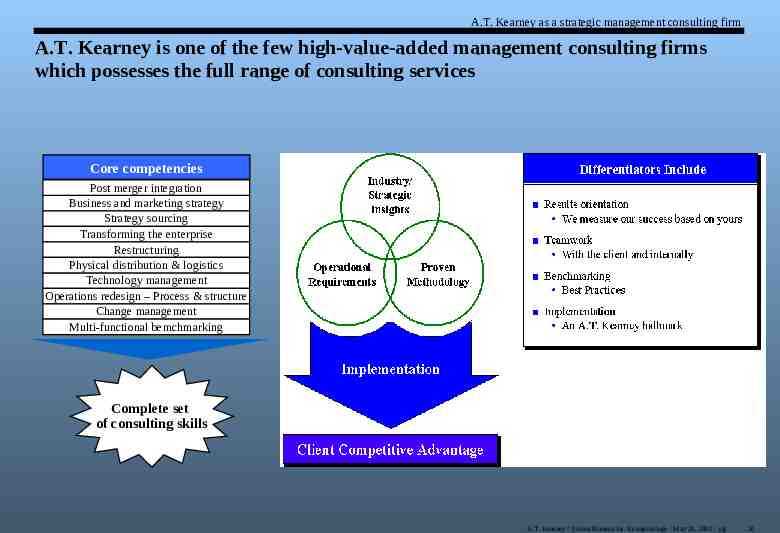

A.T. Kearney as a strategic management consulting firm A.T. Kearney is one of the few high-value-added management consulting firms which possesses the full range of consulting services Core competencies Post merger integration Business and marketing strategy Strategy sourcing Transforming the enterprise Restructuring Physical distribution & logistics Technology management Operations redesign – Process & structure Change management Multi-functional bemchmarking Complete set of consulting skills A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 20

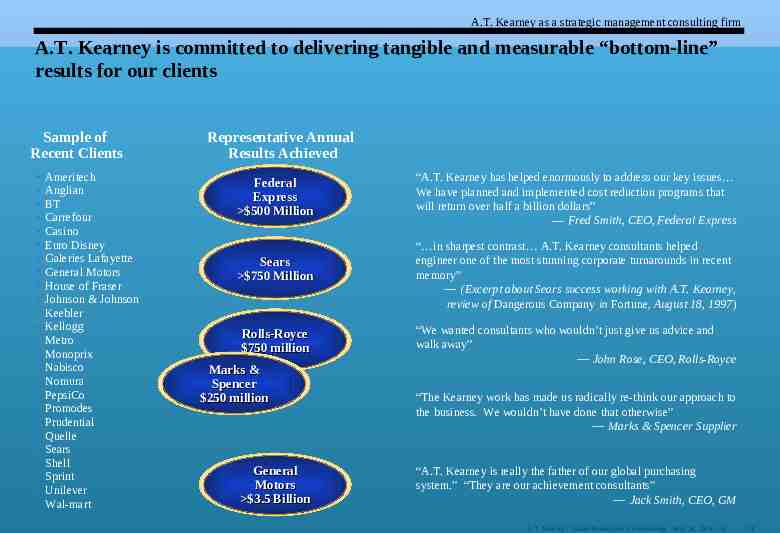

A.T. Kearney as a strategic management consulting firm A.T. Kearney is committed to delivering tangible and measurable “bottom-line” results for our clients Sample of Recent Clients Ameritech Anglian BT Carrefour Casino Euro Disney Galeries Lafayette General Motors House of Fraser Johnson & Johnson Keebler Kellogg Metro Monoprix Nabisco Nomura PepsiCo Promodes Prudential Quelle Sears Shell Sprint Unilever Wal-mart Representative Annual Results Achieved Federal Express 500 Million Sears 750 Million Rolls-Royce 750 million Marks & Spencer 250 million General Motors 3.5 Billion “A.T. Kearney has helped enormously to address our key issues We have planned and implemented cost reduction programs that will return over half a billion dollars” — Fred Smith, CEO, Federal Express “ in sharpest contrast A.T. Kearney consultants helped engineer one of the most stunning corporate turnarounds in recent memory” — (Excerpt about Sears success working with A.T. Kearney, review of Dangerous Company in Fortune, August 18, 1997) “We wanted consultants who wouldn’t just give us advice and walk away” — John Rose, CEO, Rolls-Royce “The Kearney work has made us radically re-think our approach to the business. We wouldn’t have done that otherwise” — Marks & Spencer Supplier “A.T. Kearney is really the father of our global purchasing system.” “They are our achievement consultants” — Jack Smith, CEO, GM A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 21

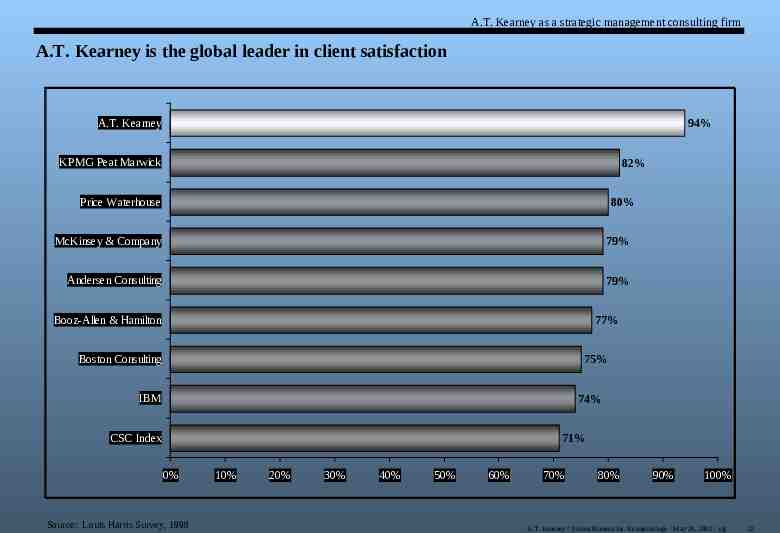

A.T. Kearney as a strategic management consulting firm A.T. Kearney is the global leader in client satisfaction A.T. Kearney 94% KPMG Peat Marwick 82% Price Waterhouse 80% McKinsey & Company 79% Andersen Consulting 79% Booz-Allen & Hamilton 77% Boston Consulting 75% IBM 74% CSC Index 71% 0% Source: Louis Harris Survey, 1998 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 22

A.T. Kearney as a strategic management consulting firm A.T. Kearney is a leader in the field of Integrated Supply Chain Management Selected Examples Seminars, Research and Leadership Delivered keynote address at the 1999 NRF annual conference on and leadership practices in driving success through consumer-focused supply chains Co-sponsored Asia LOGICON conference for senior logistics professionals (1999) — Addressed supply chain strategies and overcoming logistics obstacles for the Asia-Pacific region — Presented research findings on issues, bottlenecks and IT-related concerns of the Asian supply chain Featured presenter for the Council of Logistics Management: “Why Effective Partnerships Require a Clear Supply Chain Strategy” Delivered keynote address at 1999 Strategic Electronic Commerce Conference, an EDS-sponsored conference Featured speaker at AsiaPorts 1998 conference - “How Shifting Global Sourcing Patterns Are Impacting Port Operations” Hosted CEO Forum on “Challenges in the Digital Future in the 21st Century”, with topics including digital supply chain opportunities and digital demand management Sponsoring future supply chain industry seminars: — "Global Excellence in Operations" with Fortune (2000) — "2000 Supply Chain Management Conference” (2000) A.T.Kearney/European Logistics Association: "Insight to Impact. Results of the Fourth Quinquennial European Logistics Study 1999“ White papers and research studies A.T. Kearney has been cited in several articles on supply chain management Leadership — Past President of Council of Logistics Management — Past President of Canadian Association of Logistics Management A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 23

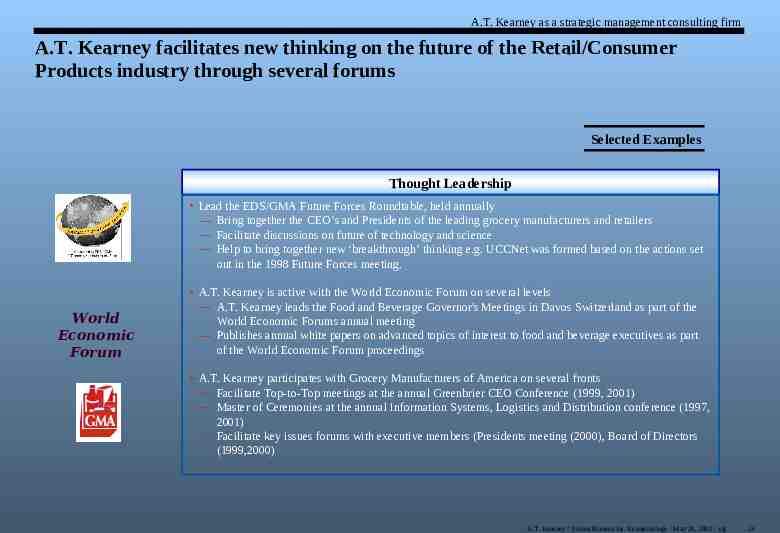

A.T. Kearney as a strategic management consulting firm A.T. Kearney facilitates new thinking on the future of the Retail/Consumer Products industry through several forums Selected Examples Thought Leadership Lead the EDS/GMA Future Forces Roundtable, held annually — Bring together the CEO’s and Presidents of the leading grocery manufacturers and retailers — Facilitate discussions on future of technology and science — Help to bring together new ‘breakthrough’ thinking e.g. UCCNet was formed based on the actions set out in the 1998 Future Forces meeting. World Economic Forum A.T. Kearney is active with the World Economic Forum on several levels — A.T. Kearney leads the Food and Beverage Governor's Meetings in Davos Switzerland as part of the World Economic Forums annual meeting — Publishes annual white papers on advanced topics of interest to food and beverage executives as part of the World Economic Forum proceedings A.T. Kearney participates with Grocery Manufacturers of America on several fronts — Facilitate Top-to-Top meetings at the annual Greenbrier CEO Conference (1999, 2001) — Master of Ceremonies at the annual Information Systems, Logistics and Distribution conference (1997, 2001) — Facilitate key issues forums with executive members (Presidents meeting (2000), Board of Directors (1999,2000) A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 24

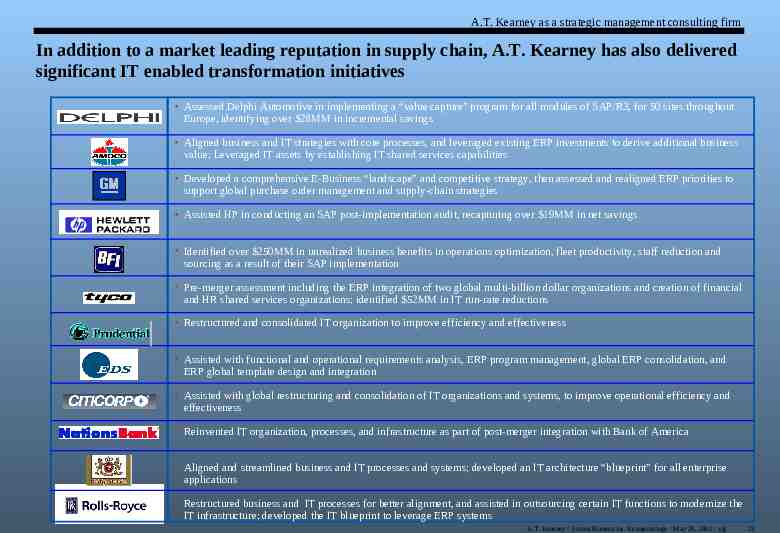

A.T. Kearney as a strategic management consulting firm In addition to a market leading reputation in supply chain, A.T. Kearney has also delivered significant IT enabled transformation initiatives Assessed Delphi Automotive in implementing a “value capture” program for all modules of SAP/R3, for 50 sites throughout Europe, identifying over 28MM in incremental savings Aligned business and IT strategies with core processes, and leveraged existing ERP investments to derive additional business value; Leveraged IT assets by establishing IT shared services capabilities Developed a comprehensive E-Business “landscape” and competitive strategy, then assessed and realigned ERP priorities to support global purchase order management and supply-chain strategies Assisted HP in conducting an SAP post-implementation audit, recapturing over 19MM in net savings Identified over 250MM in unrealized business benefits in operations optimization, fleet productivity, staff reduction and sourcing as a result of their SAP implementation Pre-merger assessment including the ERP integration of two global multi-billion dollar organizations and creation of financial and HR shared services organizations; identified 52MM in IT run-rate reductions Restructured and consolidated IT organization to improve efficiency and effectiveness Assisted with functional and operational requirements analysis, ERP program management, global ERP consolidation, and ERP global template design and integration Assisted with global restructuring and consolidation of IT organizations and systems, to improve operational efficiency and effectiveness Reinvented IT organization, processes, and infrastructure as part of post-merger integration with Bank of America Aligned and streamlined business and IT processes and systems; developed an IT architecture “blueprint” for all enterprise applications Restructured business and IT processes for better alignment, and assisted in outsourcing certain IT functions to modernize the IT infrastructure; developed the IT blueprint to leverage ERP systems A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 25

A.T. Kearney as a strategic management consulting firm A.T. Kearney is the recognized European leader in several industries Major clients per practice Financial inst. Deutsche Bank BNL Barclays Societe Generale AXA Automotive FIAT Group VW GM Europe Daimler Chrysler Renault Chemicals/O&G Rohm&Haas Arjo Wiggins BASF Pechiney BP/Amoco Comm/hi-tech Aerospace France Telecom Siemens Deutsche Telekom Lucent Philips Rolls Royce plc. Consumer/retail Carrefour Marks &Spencer Galerie Lafayette Unilever Auchan Utilities VEBA/VIAG Drewag Mainova ENEL ENBW/Neckar Transportation SAir Group Air France Lufthansa KLM Deutsche Bahn Pharma/health Gambro Quintiles Merck Henkel A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 26

A.T. Kearney as a strategic management consulting firm A.T. Kearney has wide experience in many industry sectors in Poland Automotive Fast-moving consumer goods Energy Retirement funds Chemical Food Banking Mining Insurance Shipbuilding Telecommunications Capital markets Logistics and distribution Media Publishing Real estate Steel Government institutions A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 27

A.T. Kearney as a strategic management consulting firm Examples of projects realized by A.T. Kearney in Poland Sele c Industry Telecom Client Alternative fixed line telephony provider Telecom Mobile telephony provider Publishing Number one Polish publisher tion Project Business planning for regional markets Project management Operations improvement Business market diagnostics Loyalty program Strategy MIS Organisational structure Governmental assistance programme development Major Scandinavian bank Market entry strategy Leading automotive components manufacturer SAP implementation Transportatio n Leading shipping company Financial Institutions Automotive A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 28

Consultant’s role in A.T. Kearney A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 29

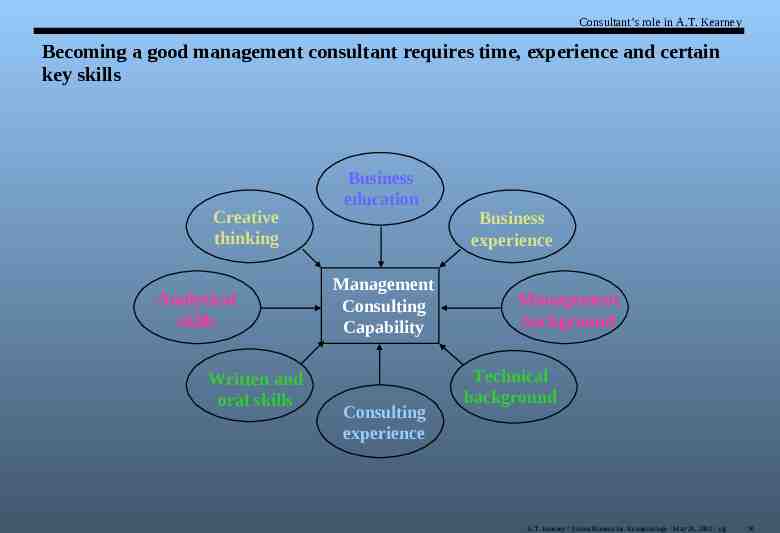

Consultant’s role in A.T. Kearney Becoming a good management consultant requires time, experience and certain key skills Creative thinking Analytical skills Written and oral skills Business education Management Consulting Capability Consulting experience Business experience Management background Technical background A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 30

Consultant’s role in A.T. Kearney Six key rules* must be followed by every good management consultant Know what you’re doing! Don’t act beyond your capabilities Continually add value commensurate with your skill and client expectations Keep to the agreed-upon project scope Hold client information strictly confidential Be ethical at all times *Source: Andrew Thomas Kearney, founder of A.T. Kearney A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 31

Consultant’s role in A.T. Kearney In addition to “time”, experience and basic skills, the good consultant requires three disciplined core consulting capabilities Proposal writing selling the assignment Project management conducting the assignment Report writing the product A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 32

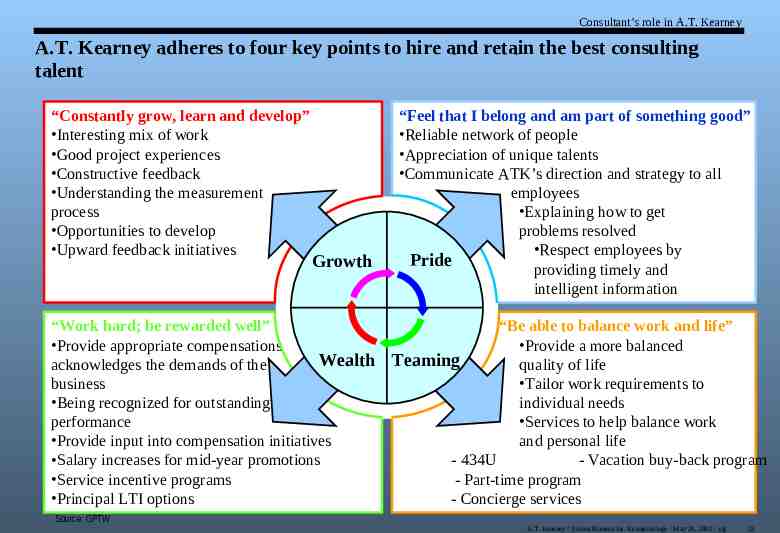

Consultant’s role in A.T. Kearney A.T. Kearney adheres to four key points to hire and retain the best consulting talent “Constantly grow, learn and develop” Interesting mix of work Good project experiences Constructive feedback Understanding the measurement process Opportunities to develop Upward feedback initiatives Growth “Work hard; be rewarded well” Provide appropriate compensations Wealth acknowledges the demands of the business Being recognized for outstanding performance Provide input into compensation initiatives Salary increases for mid-year promotions Service incentive programs Principal LTI options “Feel that I belong and am part of something good” Reliable network of people Appreciation of unique talents Communicate ATK’s direction and strategy to all employees Explaining how to get problems resolved Respect employees by Pride providing timely and intelligent information “Be able to balance work and life” Provide a more balanced Teaming quality of life Tailor work requirements to individual needs Services to help balance work and personal life - 434U - Vacation buy-back program - Part-time program - Concierge services Source: GPTW A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 33

A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 34

The future of management consulting A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 35

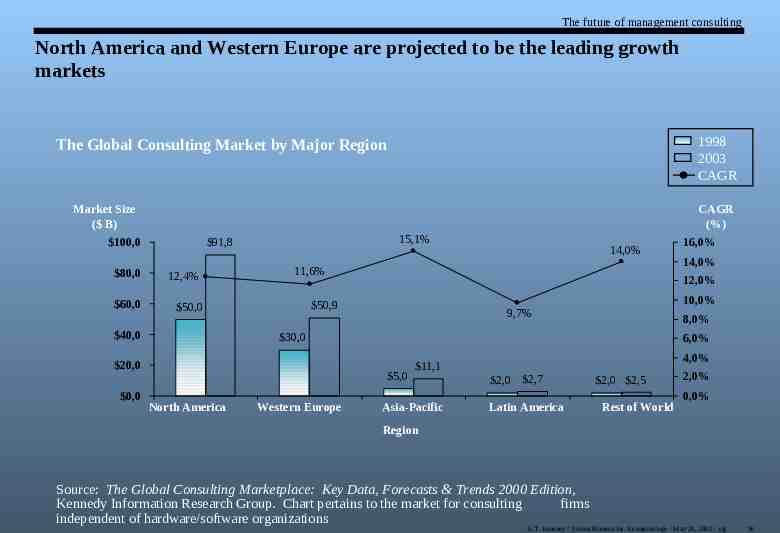

The future of management consulting North America and Western Europe are projected to be the leading growth markets 1998 2003 CAGR The Global Consulting Market by Major Region Market Size ( B) CAGR (%) 100,0 15,1% 91,8 80,0 12,4% 60,0 50,0 40,0 11,6% 9,7% 8,0% 6,0% 5,0 Western Europe 14,0% 10,0% 30,0 North America 16,0% 12,0% 50,9 20,0 0,0 14,0% 11,1 Asia-Pacific 4,0% 2,0 2,7 Latin America 2,0 2,5 Rest of World 2,0% 0,0% Region Source: The Global Consulting Marketplace: Key Data, Forecasts & Trends 2000 Edition, Kennedy Information Research Group. Chart pertains to the market for consulting firms independent of hardware/software organizations A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 36

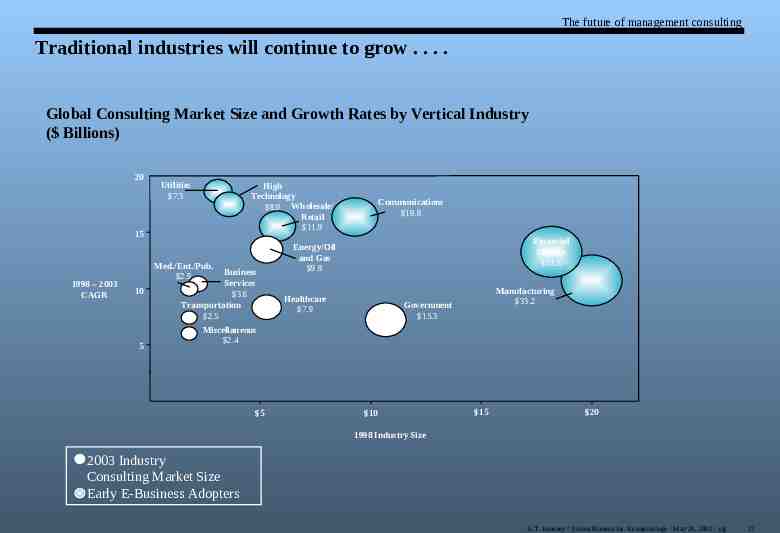

The future of management consulting Traditional industries will continue to grow . . . . Global Consulting Market Size and Growth Rates by Vertical Industry ( Billions) 20 Utilities 7.3 High Technology 8.0 Wholesale/ Retail 11.9 15 1998 – 2003 CAGR Med./Ent./Pub. 2.9 10 5 Business Services 3.6 Transportation 2.5 Communications 19.8 Financial Services 33.8 Energy/Oil and Gas 9.9 Healthcare 7.9 Manufacturing 33.2 Government 15.3 Miscellaneous 2.4 5 10 15 20 1998 Industry Size 2003 Industry Consulting Market Size Early E-Business Adopters A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 37

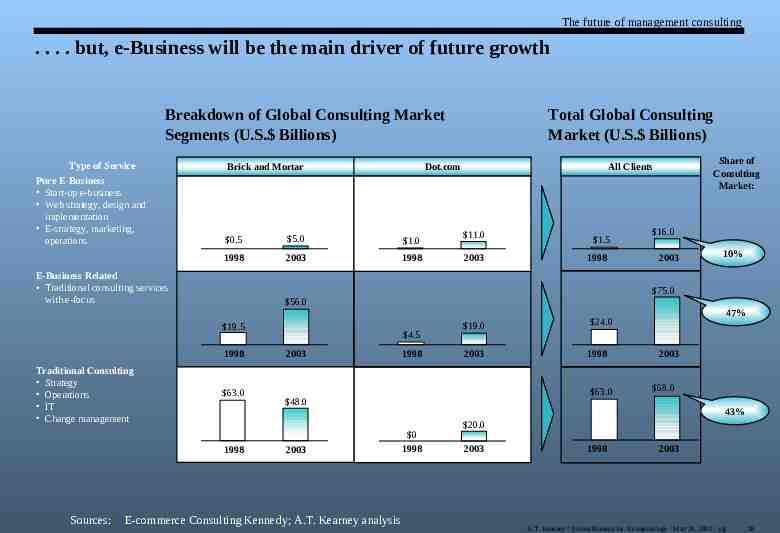

The future of management consulting . . . . but, e-Business will be the main driver of future growth Breakdown of Global Consulting Market Segments (U.S. Billions) Type of Service Pure E-Business Start-up e-business Web strategy, design and implementation E-strategy, marketing, operations Brick and Mortar 5.0 1.0 1998 2003 1998 11.0 2003 1.5 1998 16.0 2003 10% 75.0 1998 63.0 1998 Sources: Share of Consulting Market: All Clients 56.0 19.5 Traditional Consulting Strategy Operations IT Change management Dot.com 0.5 E-Business Related Traditional consulting services with e-focus Total Global Consulting Market (U.S. Billions) 4.5 2003 1998 19.0 2003 2003 E-commerce Consulting Kennedy; A.T. Kearney analysis 1998 63.0 48.0 47% 24.0 2003 68.0 43% 0 1998 20.0 2003 1998 2003 A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 38

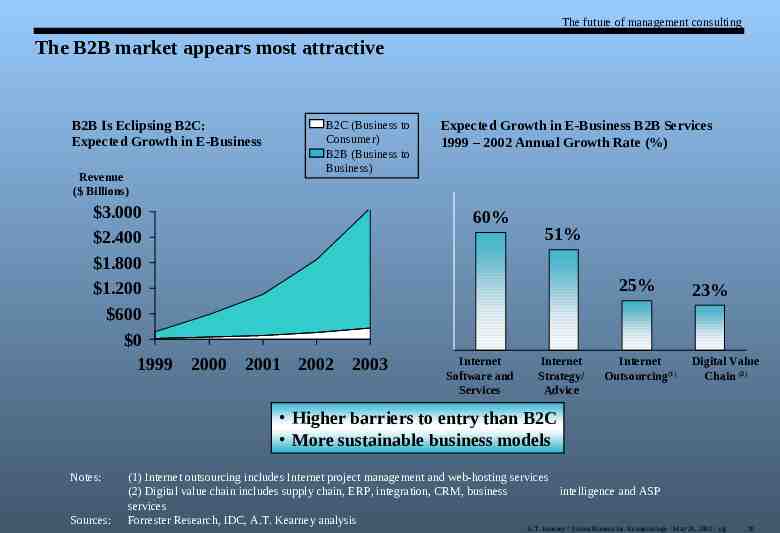

The future of management consulting The B2B market appears most attractive B2B Is Eclipsing B2C: Expected Growth in E-Business Revenue ( Billions) B2C (Business to Consumer) B2B (Business to Business) 3.000 2.400 1.800 1.200 600 0 1999 2000 2001 2002 Expected Growth in E-Business B2B Services 1999 – 2002 Annual Growth Rate (%) 60% 51% 25% 2003 Internet Software and Services Internet Strategy/ Advice Internet Outsourcing(1) 23% Digital Value Chain (2) Higher barriers to entry than B2C More sustainable business models Notes: Sources: (1) Internet outsourcing includes Internet project management and web-hosting services (2) Digital value chain includes supply chain, ERP, integration, CRM, business intelligence and ASP services Forrester Research, IDC, A.T. Kearney analysis A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 39

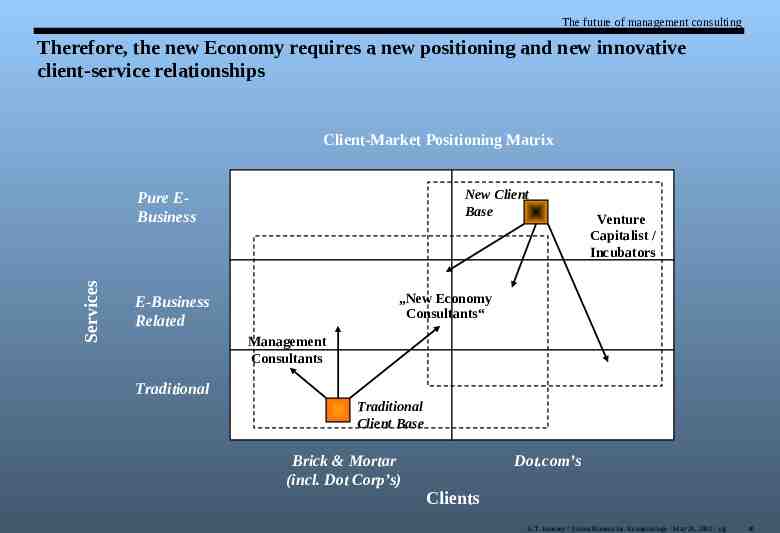

The future of management consulting Therefore, the new Economy requires a new positioning and new innovative client-service relationships Client-Market Positioning Matrix New Client Base Services Pure EBusiness Venture Capitalist / Incubators „New Economy Consultants“ E-Business Related Management Consultants Traditional Traditional Client Base Brick & Mortar (incl. Dot Corp’s) Dot.com’s Clients A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 40

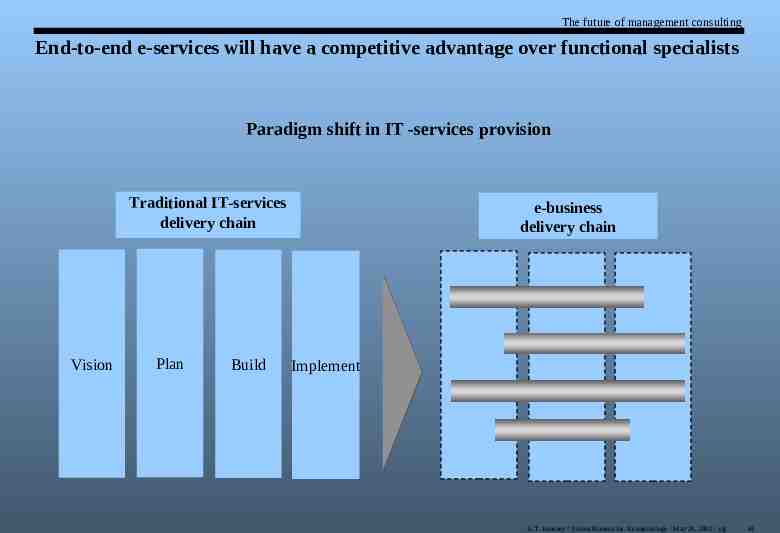

The future of management consulting End-to-end e-services will have a competitive advantage over functional specialists Paradigm shift in IT -services provision Traditional IT-services delivery chain Vision Plan Build e-business delivery chain Implement A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 41

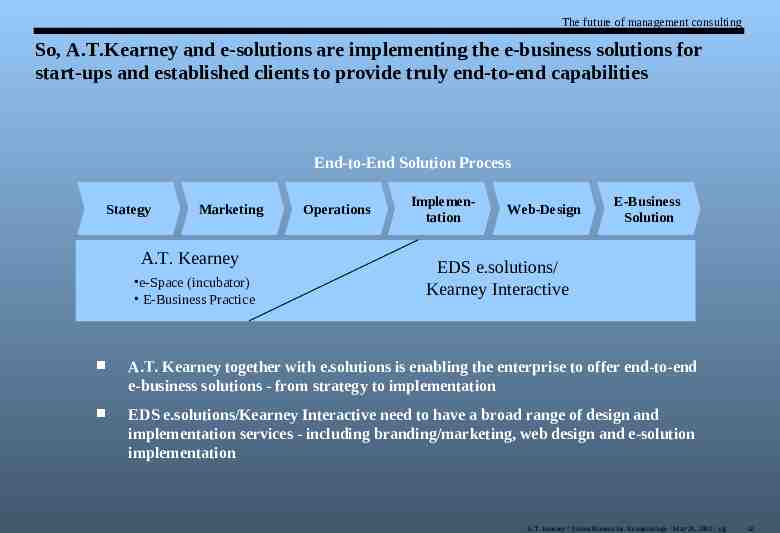

The future of management consulting So, A.T.Kearney and e-solutions are implementing the e-business solutions for start-ups and established clients to provide truly end-to-end capabilities End-to-End Solution Process Stategy Marketing A.T. Kearney e-Space (incubator) E-Business Practice Operations Implementation Web-Design E-Business Solution EDS e.solutions/ Kearney Interactive A.T. Kearney together with e.solutions is enabling the enterprise to offer end-to-end e-business solutions - from strategy to implementation EDS e.solutions/Kearney Interactive need to have a broad range of design and implementation services - including branding/marketing, web design and e-solution implementation A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 42

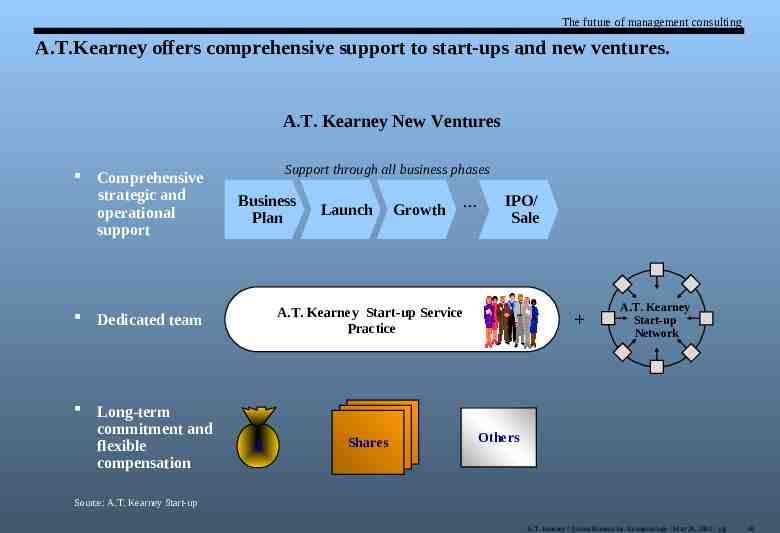

The future of management consulting A.T.Kearney offers comprehensive support to start-ups and new ventures. A.T. Kearney New Ventures Comprehensive strategic and operational support Support through all business phases Business Plan Growth IPO/ Sale A.T. Kearney Start-up Service Practice Dedicated team Long-term commitment and flexible compensation Launch Shares A.T. Kearney Start-up Network Others Source: A.T. Kearney Start-up A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 43

Questions & Answers an EDS company A.T. Kearney / Szkoła Biznesu im. Kozminskiego / May 28, 2001 / shj 44