Wireless Locationbased Services Technologies, Applications and

69 Slides4.98 MB

Wireless Locationbased Services Technologies, Applications and Management By Graham Chen

Contents Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 2

Let’s Begin. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 3

A Fundamental Paradigm Shift By 2005 most wireless devices will be locationaware This means that over 500 million people (consumers, employees and employers) will be able to access where they are, and use location based services This is possibly the most fundamental paradigm shift in spatial information usage since the invention of the map Dr. Graham Chen 2002 4

Wireless Market Overview McKinsey’s definition of 3 waves: Wireless Internet Access Location-based personalized services 3G Dr. Graham Chen 2002 5

Wireless Market Overview The reality: Wireless Internet access is only a novelty Wireless applications still live in a virtual world (hard to compete against internet) LBS shows no sign of reaching maturity, revenue prediction a wide range (3.7b to 20b by 2006) 3G is a question mark. What do you want bandwidth on your phone for if there are no contents? (Strategic Analytics predicts 2.5G will dominate for the next decade) Dr. Graham Chen 2002 8

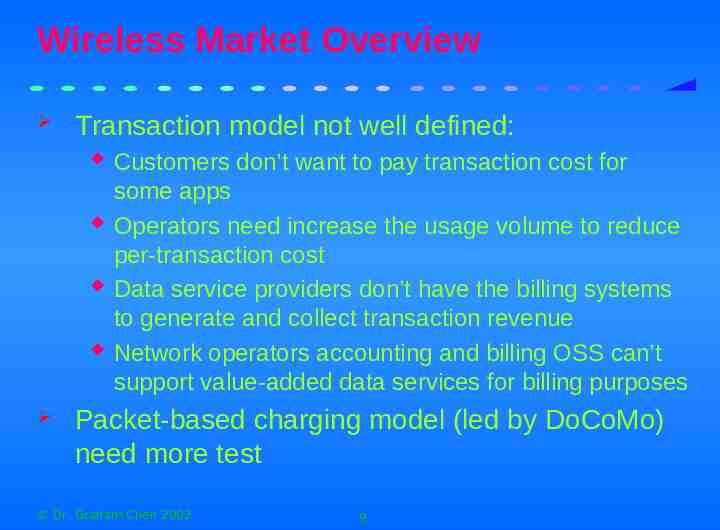

Wireless Market Overview Transaction model not well defined: Customers don’t want to pay transaction cost for some apps Operators need increase the usage volume to reduce per-transaction cost Data service providers don’t have the billing systems to generate and collect transaction revenue Network operators accounting and billing OSS can’t support value-added data services for billing purposes Packet-based charging model (led by DoCoMo) need more test Dr. Graham Chen 2002 9

LBS Market Overview. Ovum predicts the LBS market will reach 20 billion p.a. by 2006 Ovum findings: Personalize contents by location information the key No clear dominance of location technology yet No clear-cut business model emerged Accuracy not very important Analysys says 18.5 billion pa by 2006 BWCS says, pessimistically 3.7 billion pa by 2006 Dr. Graham Chen 2002 10

LBS Market Overview Which one do you believe? Dr. Graham Chen 2002 11

Progress Check. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 12

Business Drivers for Mobile LBS The mandate from the FCC: Government regulations The desire for service providers to recoup the cost Upsurge in interest in wireless data services A perceived future demand for such services Dr. Graham Chen 2002 13

North America: FCC E911 FCC Timetable (Phase II) Position enabled handsets Accuracy (handset based) 1 October 2001: selling and activating 31 Dec 2001: 25% new handsets 30 June 2002: 50%new handsets 31 Dec 2002: 100% new handsets 67% handsets at 50 meters 95% handsets at 150 meters Accuracy (network based) 67% handsets at 100 meters 95% handsets at 300 meters Dr. Graham Chen 2002 14

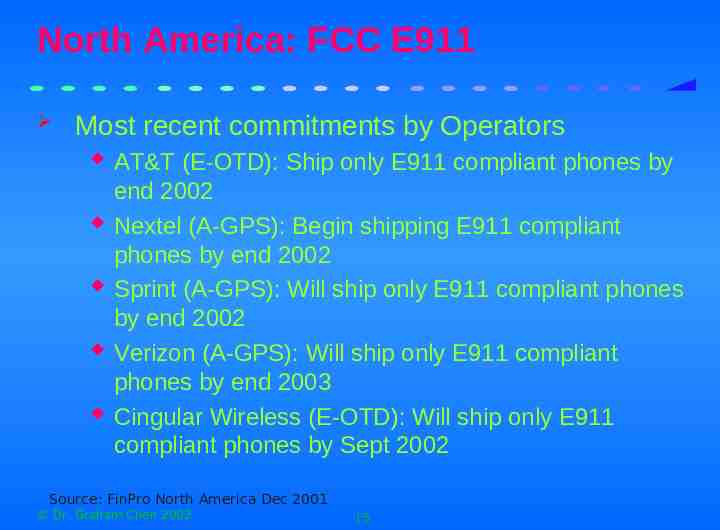

North America: FCC E911 Most recent commitments by Operators AT&T (E-OTD): Ship only E911 compliant phones by end 2002 Nextel (A-GPS): Begin shipping E911 compliant phones by end 2002 Sprint (A-GPS): Will ship only E911 compliant phones by end 2002 Verizon (A-GPS): Will ship only E911 compliant phones by end 2003 Cingular Wireless (E-OTD): Will ship only E911 compliant phones by Sept 2002 Source: FinPro North America Dec 2001 Dr. Graham Chen 2002 15

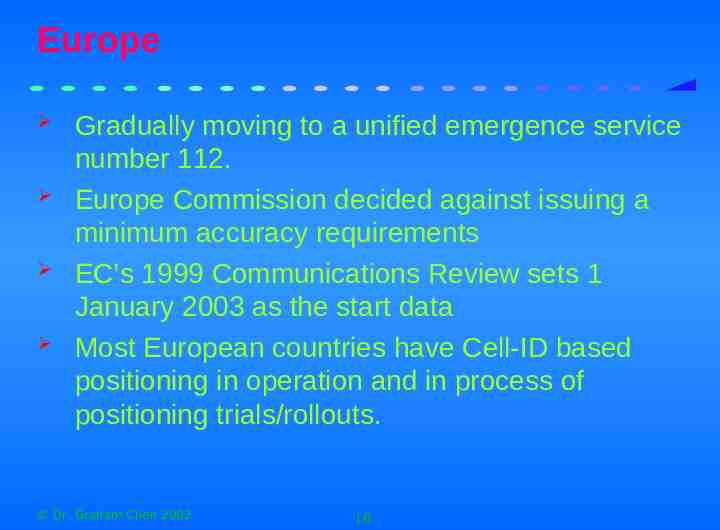

Europe Gradually moving to a unified emergence service number 112. Europe Commission decided against issuing a minimum accuracy requirements EC’s 1999 Communications Review sets 1 January 2003 as the start data Most European countries have Cell-ID based positioning in operation and in process of positioning trials/rollouts. Dr. Graham Chen 2002 16

Asia Pacific Most countries have no formal move towards regulation. Asia Pacific countries have Cell-ID based positioning in operation Singapore leading with high accuracy E-OTD network rollout. Japan and Korea made most progress: Japan already has advanced network positioning on its mobile systems KDDI selling 288,000 GPS and video enabled phones SK completes GPS-based positioning system trial Dr. Graham Chen 2002 17

Handset Drivers Semi-conductor manufacturers diversifying into “internet appliances” Handsets will be the largest population of any electronic device by 2003 (more than TVs or PCs) Handset manufacturers driving for competitive edge in innovative use of new data networks The speed of innovation is astounding with handsets superseded in months! Dr. Graham Chen 2002 18

Business Driver Stakeholders Carriers: Return on wireless data network investments Semi-conductor manufacturers: Diversification into huge handset and wireless appliance mass market Network Equipment Vendors: Significant sales in network upgrades – 2.5G, 3G and positioning Dr. Graham Chen 2002 19

Business Driver Stakeholders Electronics Vendors: Handset differentiation & faster handset renewal rates Positioning Technology Vendors: Significant return on positioning technology sales Portals—Chargeable applications Governments: Emergency tracking (E911), government “oversight”, military & overall economy improvements Dr. Graham Chen 2002 20

Technology Drivers 2.5G networks are now extensively deployed North America mobile handset penetration will equal Europe by 2006 Positioning systems are rolling out, with blanket US coverage by 2005 Some handsets are GPS enabled now Handsets are rapidly evolving to color screen, data capable, positioning capable units Extensive spatial & navigation datasets are now available Dr. Graham Chen 2002 21

Business Needs Services and products to : Reduce Costs Reduce asset losses Increase employee and asset safety Increase Revenue and Return on Investment Increase effectiveness in the workforce Increase customer loyalty Fulfill legislative requirements Dr. Graham Chen 2002 22

Consumer Needs Need to feel secure Need to keep loved ones secure Desire for asset/property protection Desire for entertainment Desire for Time and Frustration Saving services Desire for “cool” services and services that create peer bonding Dr. Graham Chen 2002 23

Telematics Many cars in design now will roll off production lines in 2005 with in-built wireless telematics This includes GPS positioning, wireless communications and in-vehicle computer screens. Cars will be a mobile device just like a handset or a PDA Dr. Graham Chen 2002 24

Market Development Market development hindrances Privacy concerns Network evolution Handsets and device interoperability Multi-technology and multi-standards Operators’ caution and lack of speed Other location centric services Dr. Graham Chen 2002 25

Progress Check. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 26

LBS Technologies Network-based position technologies Handset-based positioning technologies Handsets Technology hindrances Dr. Graham Chen 2002 27

Network-based Position Technology Cell-ID Relies on the cell a mobile in connecting to. Different variations exist: with Timing Advance (CELL-ID TA), with SIM Toolkit (STK), with IN and with WAP. All suitable in a home network and roaming environment Poor accuracy (cell size, 500m in large cell size) Dr. Graham Chen 2002 28

Network-based Position Technology Time of Arrival (TOA) triangulation technology requires three or more base stations to locate mobile units Expensive to deploy, requires location measurement unit (LMU) for each base station and Position Calculation functions on each Serving Mobile Location Centre (SMLC) 100m accuracy if 3 base stations are in range Dr. Graham Chen 2002 29

Network-based Position Technology Angle of Arrival (AOA) Requires array of antenna elements to determine the direction of mobile signal Good for tracking continuous signal Very expensive to deploy, accuracy 125m Dr. Graham Chen 2002 30

Handset-based Position Technology. Global positioning system GPS Satellite-based position technologies Navstar of USA, Glonass of Russia Accuracy to 10 metres European based GPS Systems EGNOS and Galileo Dr. Graham Chen 2002 31

Handset-based Position Technology Oberved time difference of arrival (OTDOA) Enhanced observed time difference (E-OTD) Positioning technology with UMTS GSM and UMTS network Bluetooth Other hybrid solutions Dr. Graham Chen 2002 32

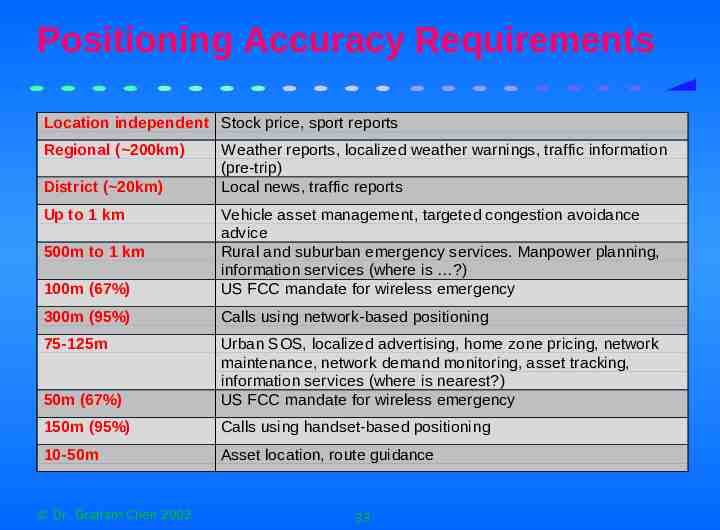

Positioning Accuracy Requirements Location independent Stock price, sport reports Regional ( 200km) District ( 20km) Up to 1 km Weather reports, localized weather warnings, traffic information (pre-trip) Local news, traffic reports 100m (67%) Vehicle asset management, targeted congestion avoidance advice Rural and suburban emergency services. Manpower planning, information services (where is ?) US FCC mandate for wireless emergency 300m (95%) Calls using network-based positioning 75-125m 50m (67%) Urban SOS, localized advertising, home zone pricing, network maintenance, network demand monitoring, asset tracking, information services (where is nearest?) US FCC mandate for wireless emergency 150m (95%) Calls using handset-based positioning 10-50m Asset location, route guidance 500m to 1 km Dr. Graham Chen 2002 33

Handsets Handsets Phones have become “smart” and data capable (and are further evolving), by: Dr. Graham Chen 2002 Integrating advanced graphic screens & PDA functionality Using Bluetooth to give access to other advanced portable devices, like PDAs Adding Java processing functionality to become “smart” on a small device Obeying Moores Law 34

Handsets Handsets are not limited by their screens With Bluetooth handsets become the connection point between a “wireless personal area network” and the “wireless data communications network” Hence the user is free to use any device with the phone providing the connection to the outside world. Dr. Graham Chen 2002 35

Dr. Graham Chen 2002 36

Dr. Graham Chen 2002 37

Dr. Graham Chen 2002 38

Technology Hindrances Complexity Expenses Privacy concerns Network evolution Handsets and device interoperability Multi-technology and multi-standards Dr. Graham Chen 2002 39

Progress Check. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 40

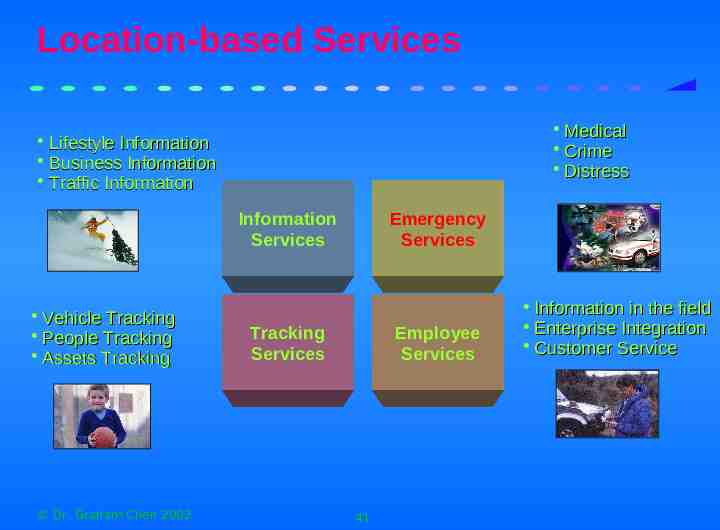

Location-based Services Medical Crime Distress Lifestyle Information Business Information Traffic Information Information Services Vehicle Tracking People Tracking Assets Tracking Dr. Graham Chen 2002 Emergency Services Tracking Services Employee Services 41 Information in the field Enterprise Integration Customer Service

Search for Kill Apps Recent Ericsson ConsumerLab survey with 16,000 users in 8 different markets concluded that most desirable LBS is personal safety services: emergency location alarm notification (home break-ins, or car break-ins) road-side assistance Dr. Graham Chen 2002 42

Personal Safety and Security Some trial commercial services: Keep tracking of children or aged relatives Personal locator devices, locating individuals through GPS Tracking family members Dubious long term revenue model (initial device plus subscription) Cumbersome GPS technology and coverage Will remain in very niche market for some time. Dr. Graham Chen 2002 43

Mobile Advertising and mCommerce Push model advertising causes so much annoyance to consumers Some opt-in pull model commercial trials: High operation cost to know how opted to receive what advertising Can easily repeat “junk mail” scenario with much less consumer control Dubious long term revenue model Users reluctance to purchase (mCommerce) Annoyance factor much worse than internet Dr. Graham Chen 2002 44

Traffic and Transport Services Fueled by telematics industry: GM’s OnStar reports 1.8m wireless-enabled cars in more than half of its models Wingcast (JV, Ford and Qualcomm) deal with Verizon DoCoMo and Nissan with advanced telematics service Vodafone with Ford Fiat install in-car wireless systems Ericsson, Volvo and Telia form WirelessCar Mercedes launches TeleAid Dr. Graham Chen 2002 45

Traffic and Transport Services Marriage of convenience between car manufacturers offering in-car wireless equipment, and operators offering services. Basis for revenue model exists for value-added services: roadside assistance traffic information routing information maps on the phone Dr. Graham Chen 2002 46

Personal Find-a-Friend Services Multiple commercial trials SignalSoft Bfound service Omnisky (Nomad IQ) Build on the huge success of Instant Messaging service Extended to groups and communities including to the corporate world May become a sticky service Likely a niche application for youth market Dr. Graham Chen 2002 47

Consumer Market Characteristics. Diversity in its service requirements, handsets, and spending capacity. Most dominant successful applications are still personal messaging service. Difference between “like the service” and “pay for the service” Difference between “use the service” to “stick to the service” Dr. Graham Chen 2002 48

Consumer Market Characteristics Consumer acceptance hurdles: usage cost, hardware and software costs, and satisfactory viewing conditions significant consumer education and marketing exposure significant modification of current systems correlation to basic human needs cultural and social conformity. Dr. Graham Chen 2002 49

Enterprise Market Applications Key demand for LBS for corporate customers: Asset tracking and management CRM tools and sales and marketing tool Fleet management Workforce management Dr. Graham Chen 2002 50

Premises Wireless Market Solutions are location, venue, campus or areabased Support a physical community of interest Numerous Premises wireless infrastructure providers exist but lack the applications Opportunities exist to provide mobile users with access to information and services within a particular geographic area Opportunities are in two segments: venue-based wireless and campus-based wireless. Dr. Graham Chen 2002 51

Venue-based Wireless Target public places to implement premises wireless for broadband localised access. Sports Stadiums—Order popcorn from your seat, view statistics, find concessions and receive promotions. Airports—Internet access, e-mail, travel information, send/receive faxes, get directions, automatically update your pocket organizer. Trade Shows—Find exhibits, monitor session changes, access coupons or special events. Shopping Centres—Directions, specials, coupon sales, locate empty parking spaces. Dr. Graham Chen 2002 52

Campus-based Wireless. Provide services to a community with common interests. Universities—Campus based communications, alerts, administration, faculty and student operations. Hospitals—Nurse call, pharmacy, test results. Hotels, Motels and Resorts—Staff, concierge, rental to guests for premises access, specials, foodbeverage-media, conference planning, ordering, information access. Dr. Graham Chen 2002 53

Campus-based Wireless Provide services to a community with common interests. Shopping Centres—maintenance, security, availability of merchandise check. Large Enterprises—Multi-floor or multi-building environments. Voice mail control and access. Dr. Graham Chen 2002 54

New Application Paradigm Personalized services Intelligent personal devices and networks More fusion of physical world (GIS domain) and virtual world (Internet domain) More mixed independent and inter-dependent entities (devices, people, networks) People, places and things model Dr. Graham Chen 2002 55

Progress Check. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 56

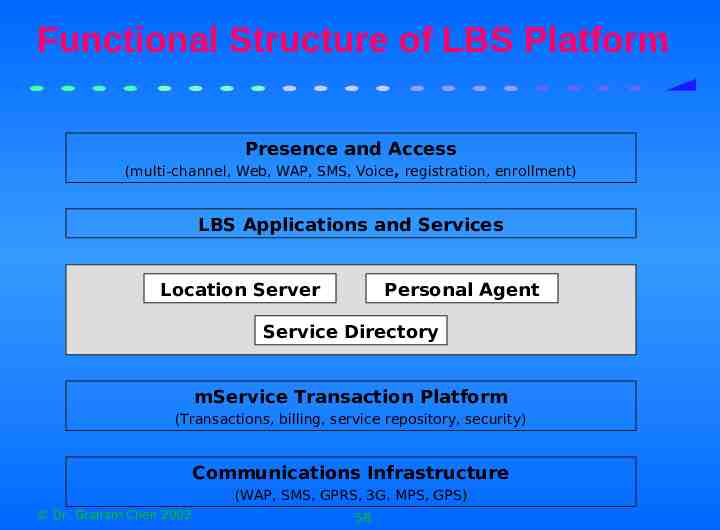

Functional Structure of LBS Platform Presence and Access (multi-channel, Web, WAP, SMS, Voice, registration, enrollment) LBS Applications and Services Location Server Personal Agent Service Directory mService Transaction Platform (Transactions, billing, service repository, security) Communications Infrastructure (WAP, SMS, GPRS, 3G, MPS, GPS) Dr. Graham Chen 2002 58

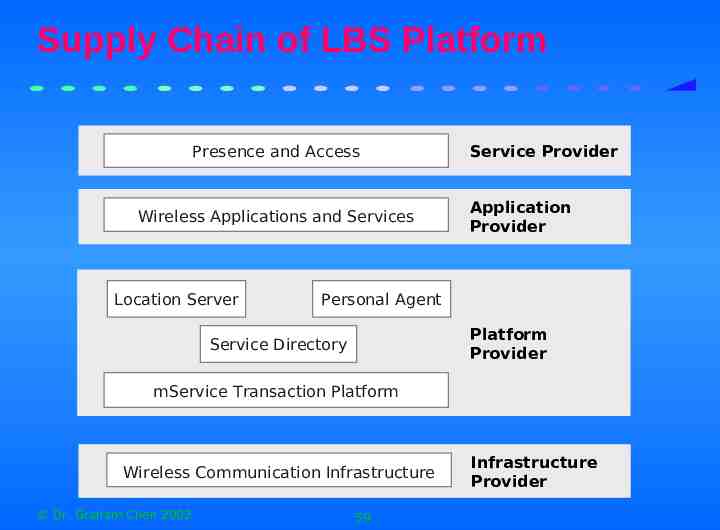

Supply Chain of LBS Platform Presence and Access Wireless Applications and Services Location Server Service Provider Application Provider Personal Agent Platform Provider Service Directory mService Transaction Platform Wireless Communication Infrastructure Dr. Graham Chen 2002 59 Infrastructure Provider

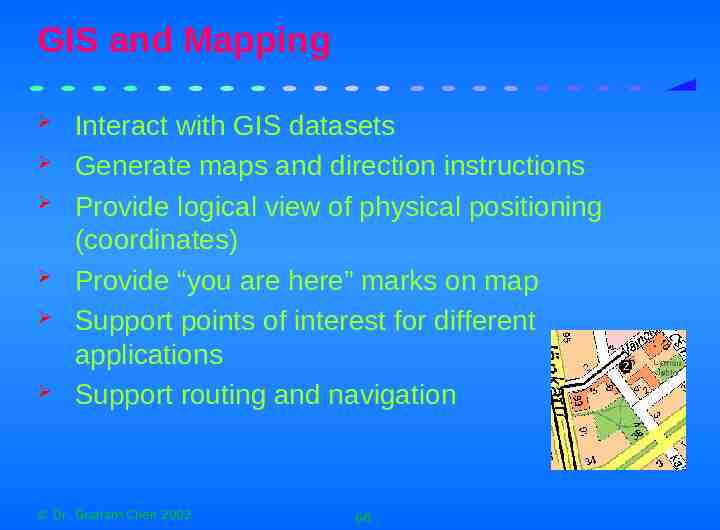

GIS and Mapping Interact with GIS datasets Generate maps and direction instructions Provide logical view of physical positioning (coordinates) Provide “you are here” marks on map Support points of interest for different applications Support routing and navigation Dr. Graham Chen 2002 66

Characteristics: Platforms Fragmented solution portfolio: Physical positioning systems Servers to process the physical location information Middleware for integration apps with positioning equipment Accounting, billing and authentication functions Software components to support application development Maps and contents Directory or database systems Dr. Graham Chen 2002 70

Characteristics: Platforms Too many players Positioning technology vendors, (GPS and MPS) GIS/map vendors Wireless data application providers Startups Contents providers Wireless hardware and software infrastructure providers Middleware platform providers shifting to wireless market Big guys: Microsoft, HP, IBM and Sun Dr. Graham Chen 2002 71

Progress Check. Overview Drivers and markets Wireless positioning technology Applications and services LBS Platform Market outlook Dr. Graham Chen 2002 72

By 2006 Dr. Graham Chen 2002 Convergence will be complete Most mobile users ( 500M) will have location aware devices A vast range of services will exist which take advantage of that location awareness It will be abnormal for a carrier, portal or enterprise service not to capitalize on the location awareness, data delivery and functional capabilities of these new smart devices – its expected as a standard service. 73

By 2006 Dr. Graham Chen 2002 You (and a billion others) will have a smart phone, bluetooth enabled, on at least a 2.5G network Your smart phone will be positioning capable to 50-100m You will have access to a wide range of Location Services, many using accurate, navigable map datasets You, (plus half a billion others), will use these services. 3G may or may not be here . 74

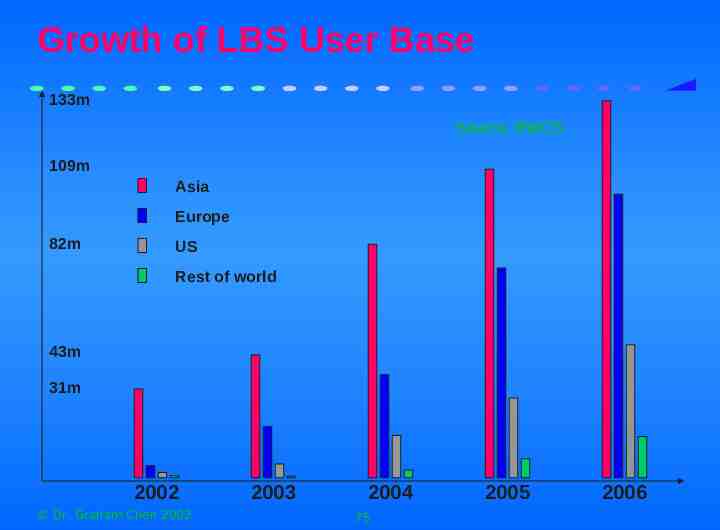

Growth of LBS User Base 133m Source: BWCS 109m Asia Europe 82m US Rest of world 43m 31m 2002 Dr. Graham Chen 2002 2003 2004 75 2005 2006

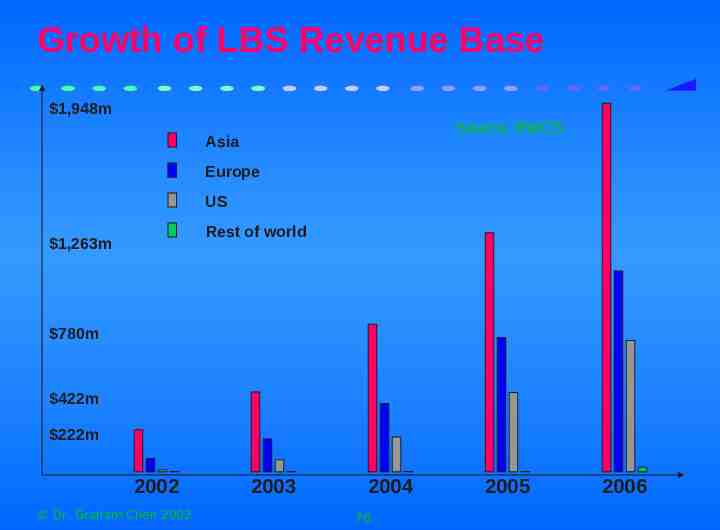

Growth of LBS Revenue Base 1,948m Source: BWCS Asia Europe US Rest of world 1,263m 780m 422m 222m 2002 Dr. Graham Chen 2002 2003 2004 76 2005 2006

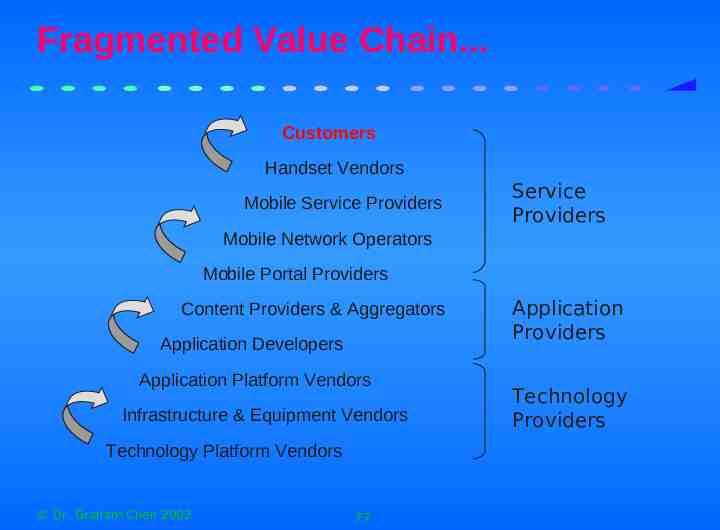

Fragmented Value Chain. Customers Handset Vendors Mobile Service Providers Service Providers Mobile Network Operators Mobile Portal Providers Content Providers & Aggregators Application Developers Application Platform Vendors Infrastructure & Equipment Vendors Technology Platform Vendors Dr. Graham Chen 2002 77 Application Providers Technology Providers

Fragmented Value Chain Current supply chain in LBS market: MPS vendors, GIS vendors Application and content vendors Network operators Systems integrators and IT vendors Lack of integrated LBS platforms Lack of integrated application/service providers Dr. Graham Chen 2002 78

Future LBS Value Chain LBS platform suppliers: MPS vendors, GIS vendors Tools Service development and deployment environment Portal tools Integrated application/service providers Network operators Mobile portals Dr. Graham Chen 2002 79

Continued Search for Applications Personalised services Reflect new interaction model centred on individuals—location is an attribute of a personal property Lowest available technology Offer business values beyond a novelty value. Dr. Graham Chen 2002 80

Further Readings BWCS, Mobile location-based services: where is the revenue? Ovum, Mobile location services: market strategies LOCUS, Overview of location services. FINPRO, North American wireless market review: Personal location-based services. FINPRO, A market study on personal navigation in Japan Dr. Graham Chen 2002 81