Chapter 7 Income statements: an introduction

22 Slides281.22 KB

Chapter 7 Income statements: an introduction

Learning objectives After you have studied this chapter, you should be able to Explain why income statements are not part of the double entry system Explain why profit is calculated Calculate cost of goods sold, gross profit and net profit Explain the difference between gross profit and net profit

Learning objectives (Continued) Explain the relationship between the trading account and the profit and loss account Explain how the trading account and the profit and loss account fit together to create the income statement Explain how to deal with closing inventory when preparing the trading account section of an income statement Close down the appropriate accounts and transfer the balances to the trading account

Learning objectives (Continued) Close down the appropriate accounts and transfer the balances to the profit and loss account Prepare an income statement from information given in a trial balance Make appropriate double entries to incorporate net profit and drawings in the capital account

The purpose of income statements How will knowing what profits are being made help a business? It will help plan ahead. It will help obtain loans from banks, other businesses and individuals. It will tell prospective business partners how successful the business is. It will tell a prospective purchaser how successful the business is. It will enable the calculation of tax payable to the tax authorities.

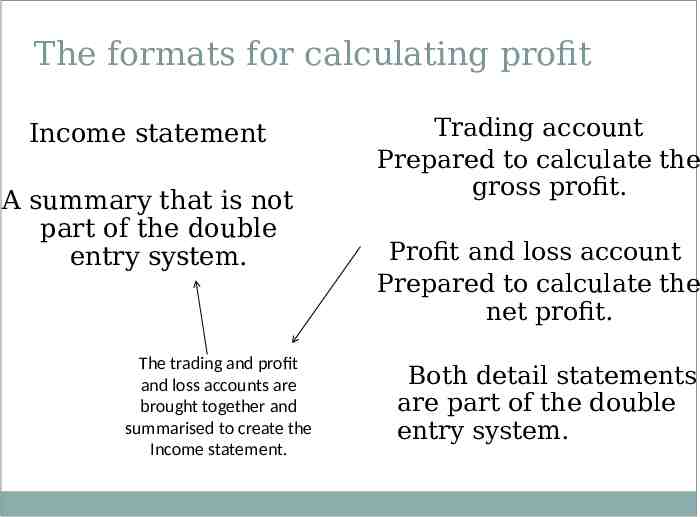

The formats for calculating profit Income statement A summary that is not part of the double entry system. The trading and profit and loss accounts are brought together and summarised to create the Income statement. Trading account Prepared to calculate the gross profit. Profit and loss account Prepared to calculate the net profit. Both detail statements are part of the double entry system.

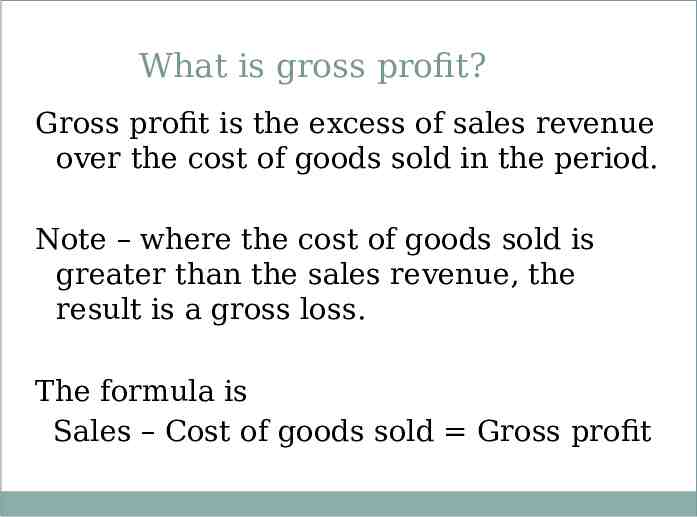

What is gross profit? Gross profit is the excess of sales revenue over the cost of goods sold in the period. Note – where the cost of goods sold is greater than the sales revenue, the result is a gross loss. The formula is Sales – Cost of goods sold Gross profit

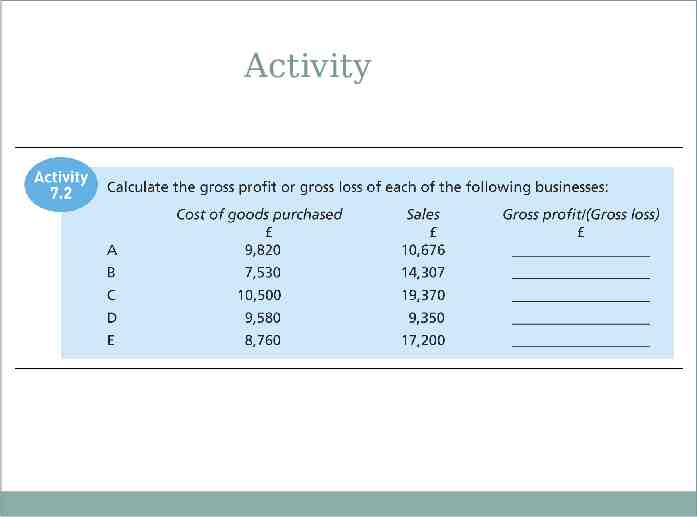

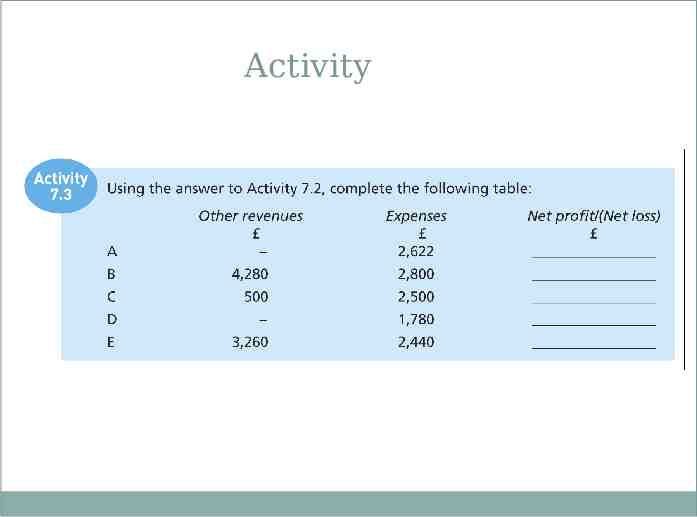

Activity

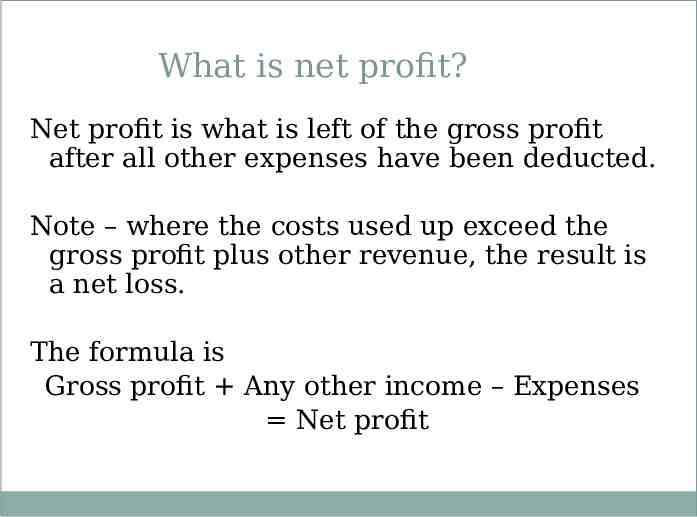

What is net profit? Net profit is what is left of the gross profit after all other expenses have been deducted. Note – where the costs used up exceed the gross profit plus other revenue, the result is a net loss. The formula is Gross profit Any other income – Expenses Net profit

Activity

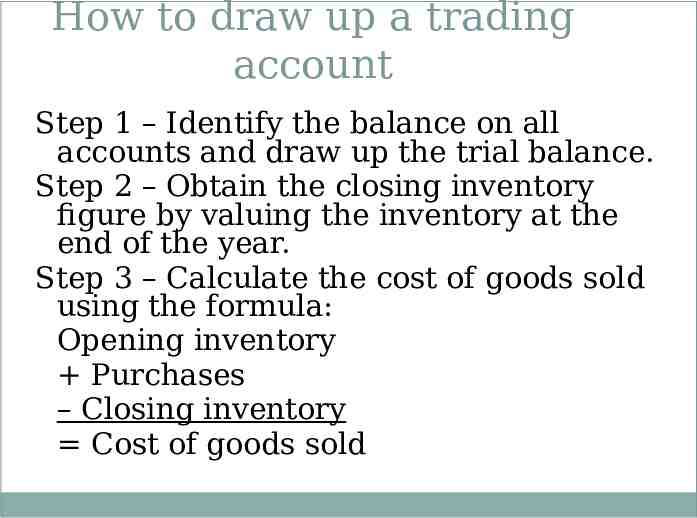

How to draw up a trading account Step 1 – Identify the balance on all accounts and draw up the trial balance. Step 2 – Obtain the closing inventory figure by valuing the inventory at the end of the year. Step 3 – Calculate the cost of goods sold using the formula: Opening inventory Purchases – Closing inventory Cost of goods sold

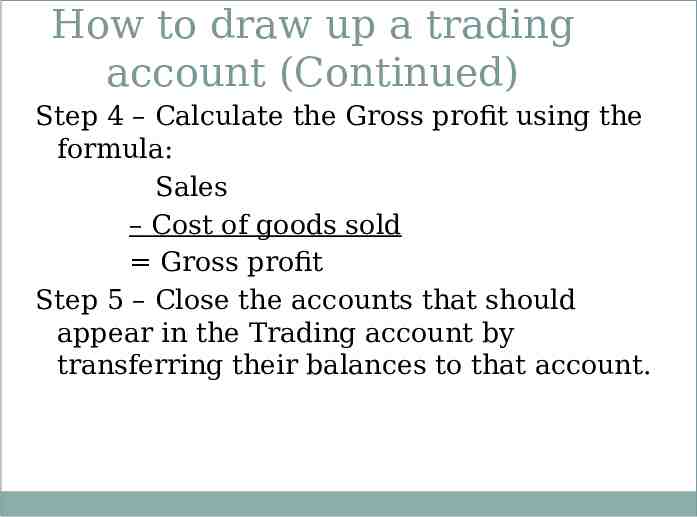

How to draw up a trading account (Continued) Step 4 – Calculate the Gross profit using the formula: Sales – Cost of goods sold Gross profit Step 5 – Close the accounts that should appear in the Trading account by transferring their balances to that account.

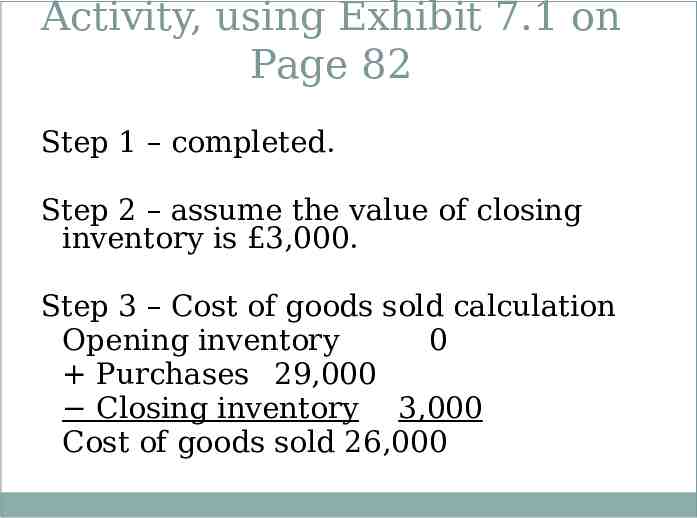

Activity, using Exhibit 7.1 on Page 82 Step 1 – completed. Step 2 – assume the value of closing inventory is 3,000. Step 3 – Cost of goods sold calculation Opening inventory 0 Purchases 29,000 Closing inventory 3,000 Cost of goods sold 26,000

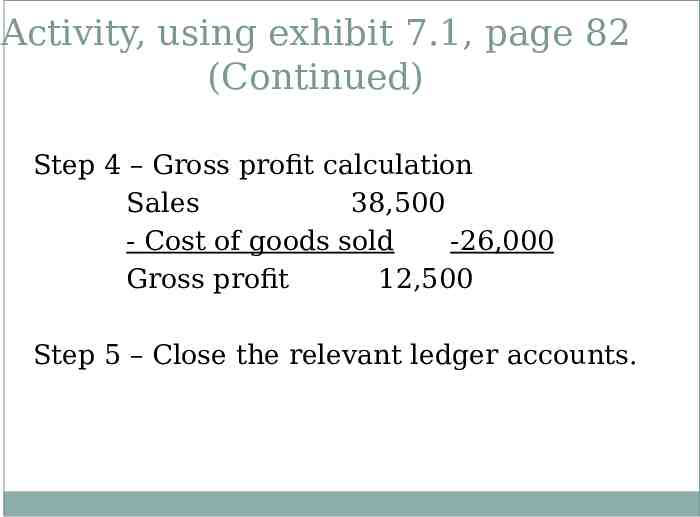

Activity, using exhibit 7.1, page 82 (Continued) Step 4 – Gross profit calculation Sales 38,500 - Cost of goods sold -26,000 Gross profit 12,500 Step 5 – Close the relevant ledger accounts.

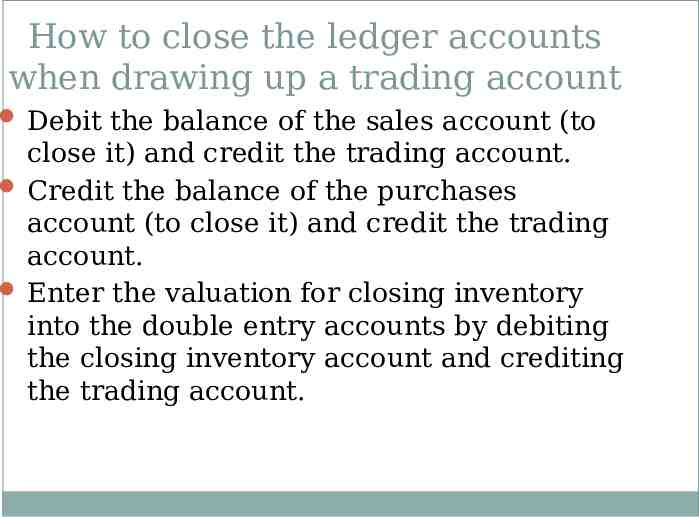

How to close the ledger accounts when drawing up a trading account Debit the balance of the sales account (to close it) and credit the trading account. Credit the balance of the purchases account (to close it) and credit the trading account. Enter the valuation for closing inventory into the double entry accounts by debiting the closing inventory account and crediting the trading account.

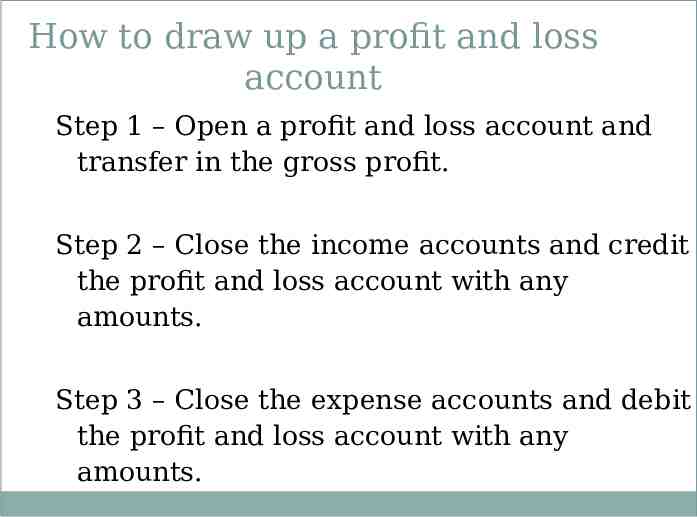

How to draw up a profit and loss account Step 1 – Open a profit and loss account and transfer in the gross profit. Step 2 – Close the income accounts and credit the profit and loss account with any amounts. Step 3 – Close the expense accounts and debit the profit and loss account with any amounts.

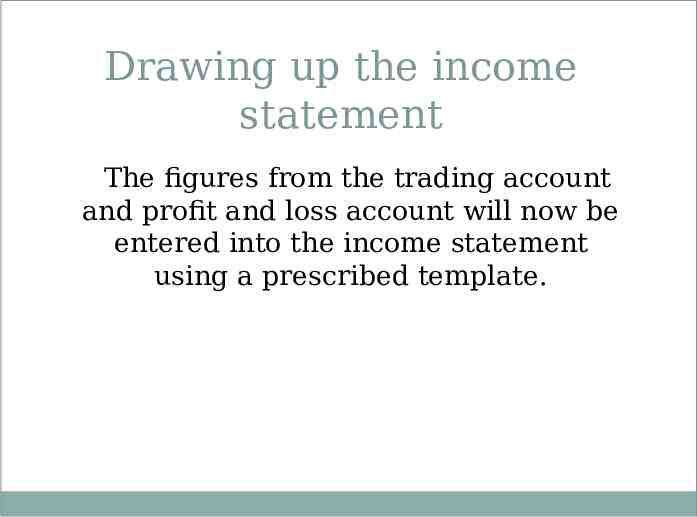

Drawing up the income statement The figures from the trading account and profit and loss account will now be entered into the income statement using a prescribed template.

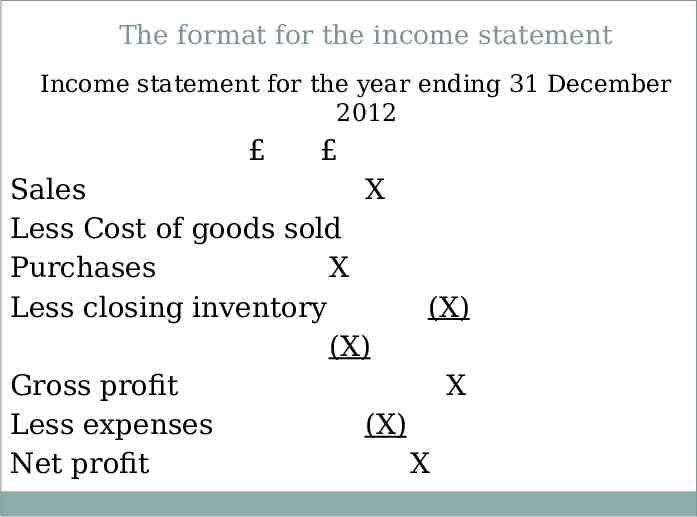

The format for the income statement Income statement for the year ending 31 December 2012 Sales X Less Cost of goods sold Purchases X Less closing inventory (X) (X) Gross profit X Less expenses (X) Net profit X

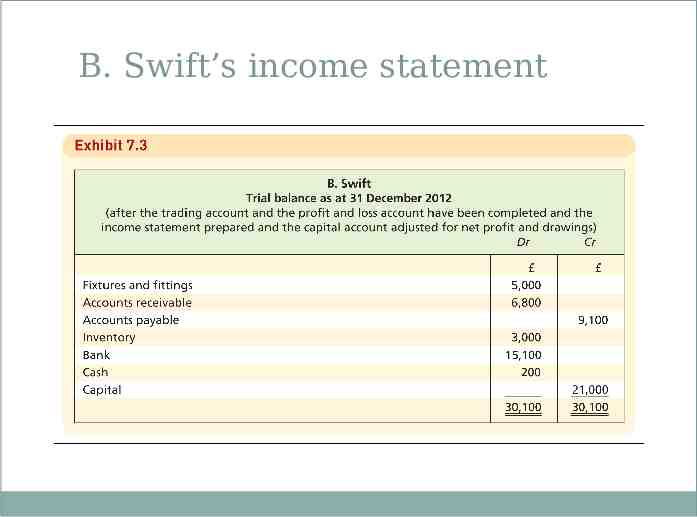

B. Swift’s income statement

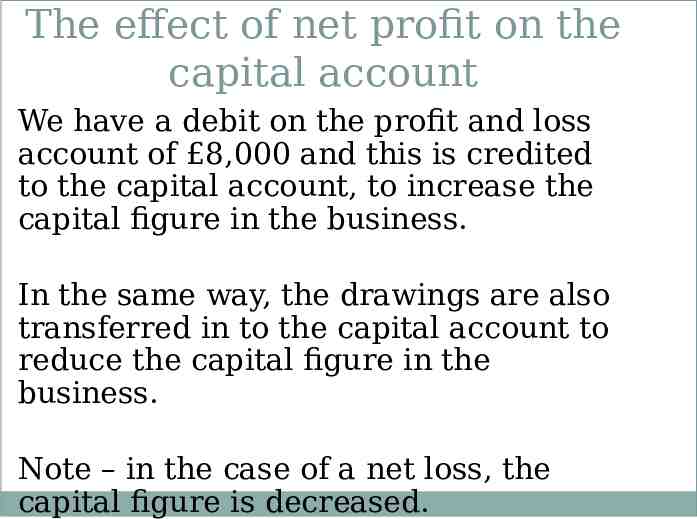

The effect of net profit on the capital account We have a debit on the profit and loss account of 8,000 and this is credited to the capital account, to increase the capital figure in the business. In the same way, the drawings are also transferred in to the capital account to reduce the capital figure in the business. Note – in the case of a net loss, the capital figure is decreased.

Learning outcomes You should have now learnt: Why income statements are not part of the double entry system Why profit is calculated How to calculate cost of goods sold, gross profit and net profit The double entries required in order to close off the relevant expense and revenue accounts at the end of a period and post how to post the entries to the trading account and the profit and loss account

Learning outcomes (Continued) How to deal with inventory at the end of a period How to prepare an income statement from a trial balance How to transfer the net profit and drawings to the capital account at the end of a period That balances on accounts not closed off in order to prepare the income statement are carried down to the following period, that these balances represent assets, liabilities and capital, and that they are entered in the statement of financial position