Audit of the Revenue Cycle CAS 265 – Communicating deficiencies

62 Slides1.87 MB

Audit of the Revenue Cycle CAS 265 – Communicating deficiencies in internal control to those charged with governance and management CAS 300 – Planning an audit of financial statements CAS 315 – Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and its Environment CAS 320 - Materiality in Planning and Performing an Audit CAS 330 - The Auditor’s Response to Assessed Risk CAS 500 – Audit Evidence CAS 530 – Audit Sampling Revenue Cycle 1

Risk Assessment Must understand the entities method of generating revenues in order to assess the business risk and risk of misstatement. Thus: Also: Revenue Cycle 2

Typical Transactions in the Sales and Collection Cycle Five major classes of Transactions: Sales Cash receipts – collecting and depositing Sales returns and allowances – Technically two distinct transactions The write-off of uncollectible accounts Bad-debt expense Revenue Cycle 3

Typical Activities See the following slides Receiving and processing customer orders. Delivering goods and services to customers. Billing customers and accounting for receivables. Collecting and depositing cash. Reconciling bank accounts. Revenue Cycle 4 LO1

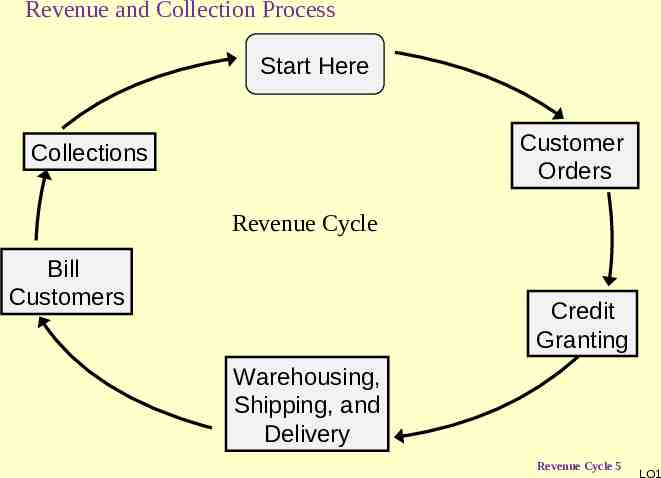

Revenue and Collection Process Start Here Customer Orders Collections Revenue Cycle Bill Customers Credit Granting Warehousing, Shipping, and Delivery Revenue Cycle 5 LO1

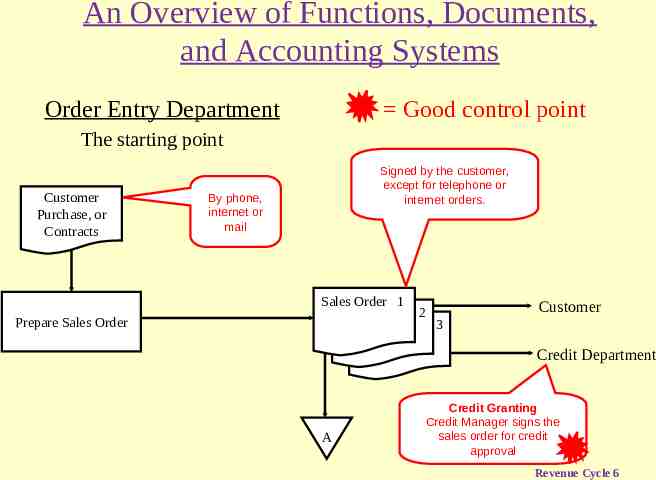

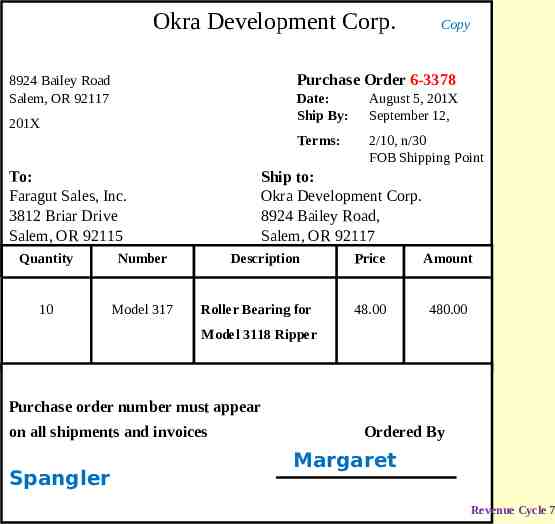

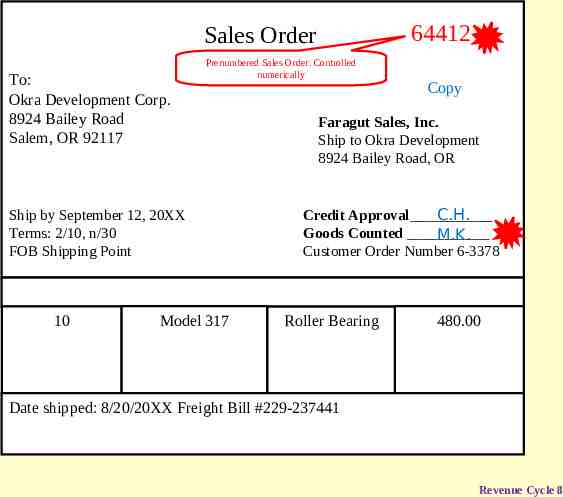

An Overview of Functions, Documents, and Accounting Systems Order Entry Department Good control point The starting point Customer Purchase, or Contracts Signed by the customer, except for telephone or internet orders. By phone, internet or mail Sales Order 1 Prepare Sales Order 2 Customer 3 Credit Department A Credit Granting Credit Manager signs the sales order for credit approval Revenue Cycle 6

Okra Development Corp. Copy Purchase Order 6-3378 8924 Bailey Road Salem, OR 92117 201X To: Faragut Sales, Inc. 3812 Briar Drive Salem, OR 92115 Quantity Number 10 Model 317 Date: Ship By: August 5, 201X September 12, Terms: 2/10, n/30 FOB Shipping Point Ship to: Okra Development Corp. 8924 Bailey Road, Salem, OR 92117 Description Roller Bearing for Price Amount 48.00 480.00 Model 3118 Ripper Purchase order number must appear on all shipments and invoices Spangler Ordered By Margaret Revenue Cycle 7

64412 Sales Order To: Okra Development Corp. 8924 Bailey Road Salem, OR 92117 Prenumbered Sales Order. Controlled numerically Ship by September 12, 20XX Terms: 2/10, n/30 FOB Shipping Point 10 Model 317 Copy Faragut Sales, Inc. Ship to Okra Development 8924 Bailey Road, OR C.H. Credit Approval Goods Counted M.K. Customer Order Number 6-3378 Roller Bearing 480.00 Date shipped: 8/20/20XX Freight Bill #229-237441 Revenue Cycle 8

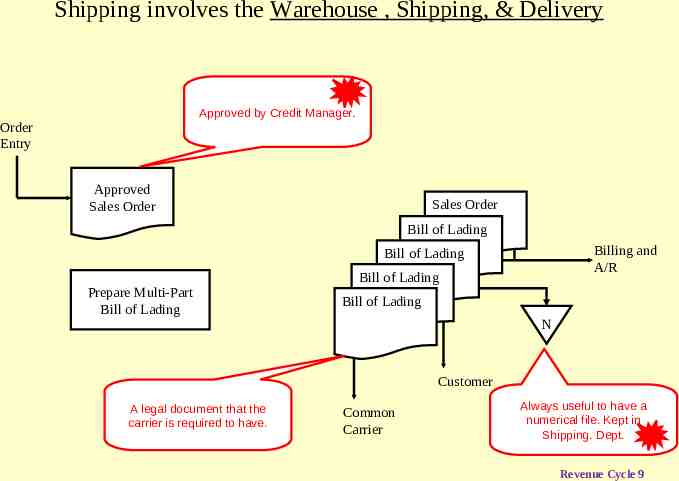

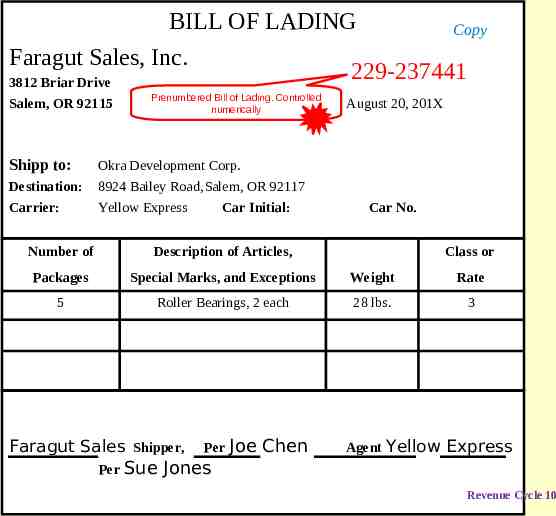

Shipping involves the Warehouse , Shipping, & Delivery Approved by Credit Manager. Order Entry Approved Sales Order Sales Order Bill of Lading Billing and A/R Bill of Lading Prepare Multi-Part Bill of Lading Bill of Lading Bill of Lading N Customer A legal document that the carrier is required to have. Common Carrier Always useful to have a numerical file. Kept in Shipping. Dept. Revenue Cycle 9

BILL OF LADING Copy Faragut Sales, Inc. 229-237441 3812 Briar Drive Salem, OR 92115 Shipp to: Destination: Carrier: Prenumbered Bill of Lading. Controlled numerically Okra Development Corp. 8924 Bailey Road,Salem, OR 92117 Yellow Express Car Initial: August 20, 201X Car No. Number of Description of Articles, Packages Special Marks, and Exceptions Weight Rate 5 Roller Bearings, 2 each 28 lbs. 3 Faragut Sales Shipper, Per Sue Per Joe Chen Class or Agent Yellow Express Jones Revenue Cycle 10

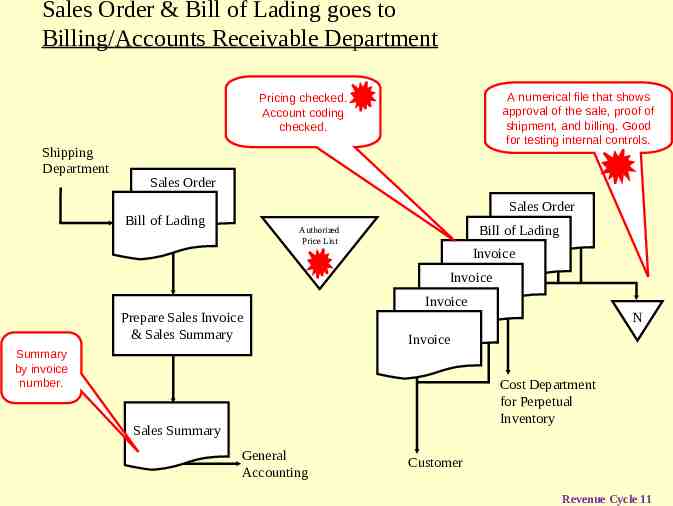

Sales Order & Bill of Lading goes to Billing/Accounts Receivable Department A numerical file that shows approval of the sale, proof of shipment, and billing. Good for testing internal controls. Pricing checked. Account coding checked. Shipping Department Sales Order Sales Order Bill of Lading Bill of Lading Authorized Price List Invoice Invoice Invoice Prepare Sales Invoice & Sales Summary N Invoice Summary by invoice number. Cost Department for Perpetual Inventory Sales Summary General Accounting Customer Revenue Cycle 11

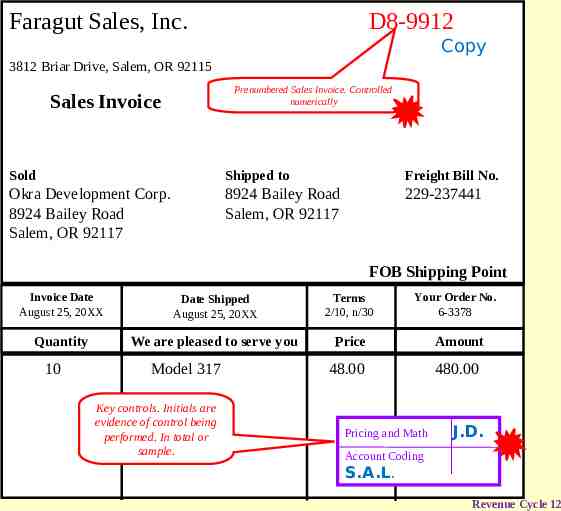

Faragut Sales, Inc. D8-9912 Copy 3812 Briar Drive, Salem, OR 92115 Prenumbered Sales Invoice. Controlled numerically Sales Invoice Sold Shipped to Freight Bill No. Okra Development Corp. 8924 Bailey Road Salem, OR 92117 8924 Bailey Road Salem, OR 92117 229-237441 FOB Shipping Point Invoice Date August 25, 20XX Date Shipped August 25, 20XX Terms 2/10, n/30 Quantity We are pleased to serve you Price 10 Model 317 Key controls. Initials are evidence of control being performed. In total or sample. Your Order No. 6-3378 48.00 Pricing and Math Amount 480.00 J.D. Account Coding S.A.L. Revenue Cycle 12

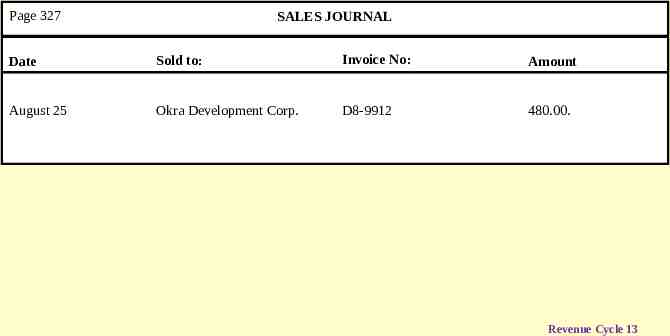

Page 327 SALES JOURNAL Date Sold to: Invoice No: Amount August 25 Okra Development Corp. D8-9912 480.00. Revenue Cycle 13

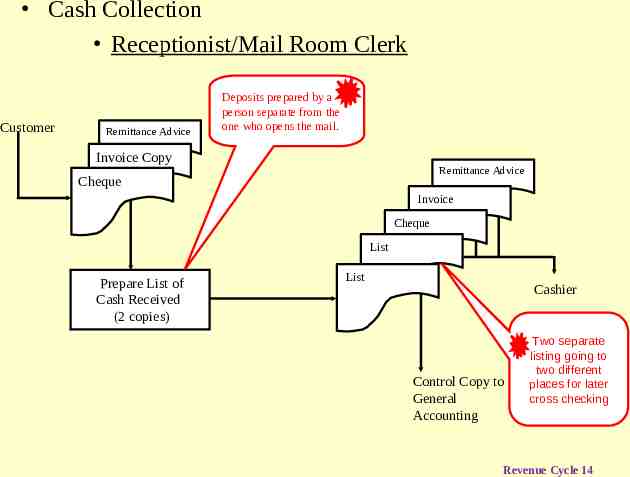

Cash Collection Receptionist/Mail Room Clerk Customer Remittance Advice Deposits prepared by a person separate from the one who opens the mail. Invoice Copy Remittance Advice Cheque Invoice Cheque List Prepare List of Cash Received (2 copies) List Cashier Control Copy to General Accounting Two separate listing going to two different places for later cross checking Revenue Cycle 14

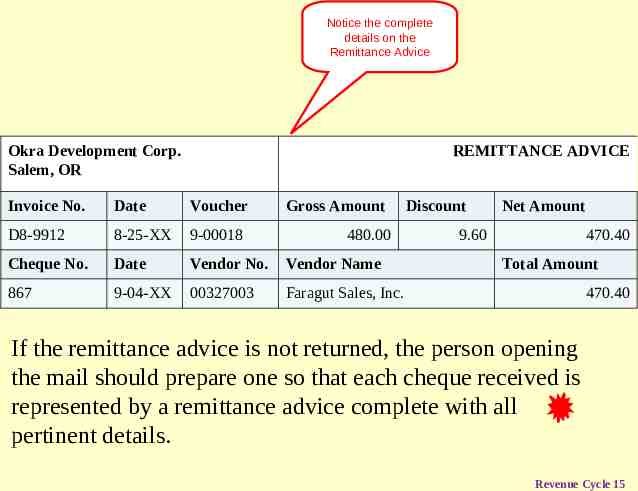

Notice the complete details on the Remittance Advice Okra Development Corp. Salem, OR REMITTANCE ADVICE Invoice No. Date Voucher Gross Amount D8-9912 8-25-XX 9-00018 Cheque No. Date Vendor No. Vendor Name 867 9-04-XX 00327003 Faragut Sales, Inc. 480.00 Discount Net Amount 9.60 470.40 Total Amount 470.40 If the remittance advice is not returned, the person opening the mail should prepare one so that each cheque received is represented by a remittance advice complete with all pertinent details. Revenue Cycle 15

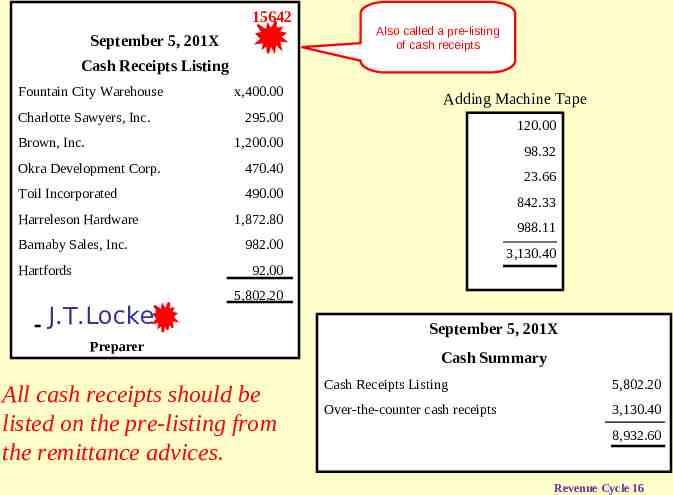

15642 September 5, 201X Also called a pre-listing of cash receipts Cash Receipts Listing Fountain City Warehouse x,400.00 Charlotte Sawyers, Inc. x,295.00 Brown, Inc. 1,200.00 Okra Development Corp. x,470.40 Toil Incorporated x,490.00 Harreleson Hardware 1,872.80 Barnaby Sales, Inc. x,982.00 Hartfords x,x92.00 J.T.Lockett Adding Machine Tape x,120.00 x,x98.32 x,x23.66 x,842.33 x,988.11 3,130.40 5,802.20 Preparer All cash receipts should be listed on the pre-listing from the remittance advices. September 5, 201X Cash Summary Cash Receipts Listing 5,802.20 Over-the-counter cash receipts 3,130.40 8,932.60 Revenue Cycle 16

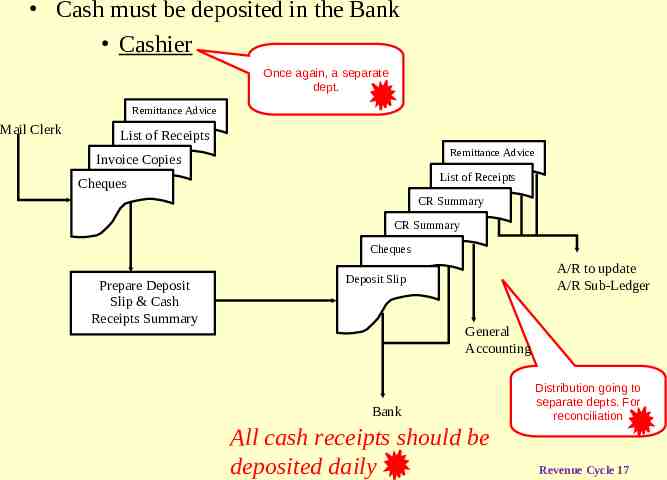

Cash must be deposited in the Bank Cashier Once again, a separate dept. Remittance Advice Mail Clerk List of Receipts Remittance Advice Invoice Copies List of Receipts Cheques CR Summary CR Summary Cheques Prepare Deposit Slip & Cash Receipts Summary A/R to update A/R Sub-Ledger Deposit Slip General Accounting Bank All cash receipts should be deposited daily Distribution going to separate depts. For reconciliation Revenue Cycle 17

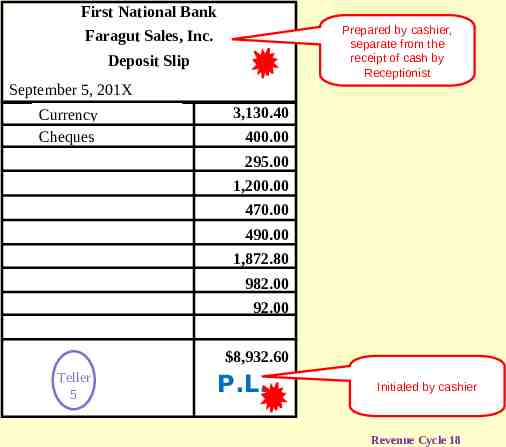

First National Bank Prepared by cashier, separate from the receipt of cash by Receptionist Faragut Sales, Inc. Deposit Slip September 5, 201X Currency Cheques 3,130.40 400.00 295.00 1,200.00 470.00 490.00 1,872.80 982.00 92.00 8,932.60 Teller 5 P.L. Initialed by cashier Revenue Cycle 18

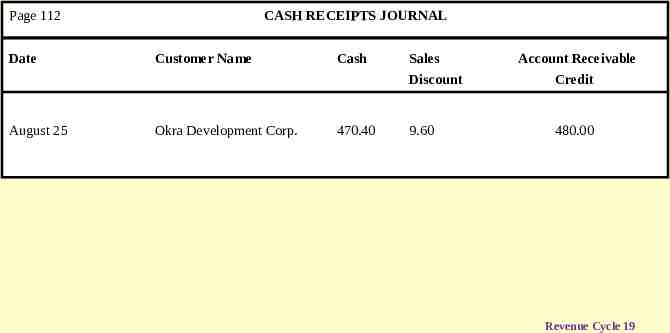

Page 112 Date August 25 CASH RECEIPTS JOURNAL Customer Name Okra Development Corp. Cash 470.40 Sales Account Receivable Discount Credit 9.60 480.00 Revenue Cycle 19

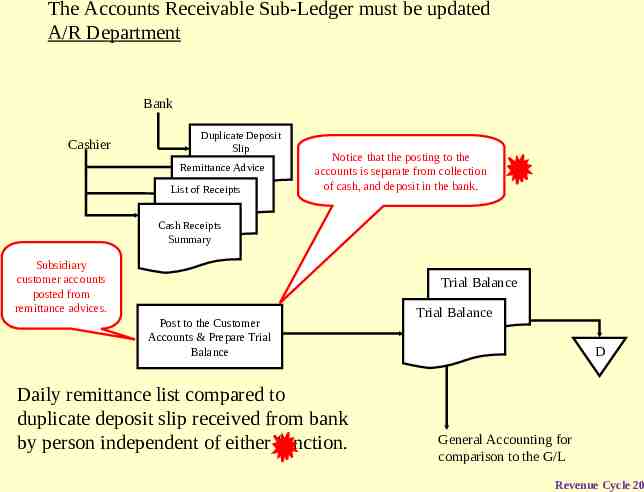

The Accounts Receivable Sub-Ledger must be updated A/R Department Bank Cashier Duplicate Deposit Slip Remittance Advice List of Receipts Notice that the posting to the accounts is separate from collection of cash, and deposit in the bank. Cash Receipts Summary Subsidiary customer accounts posted from remittance advices. Trial Balance Post to the Customer Accounts & Prepare Trial Balance Daily remittance list compared to duplicate deposit slip received from bank by person independent of either function. Trial Balance D General Accounting for comparison to the G/L Revenue Cycle 20

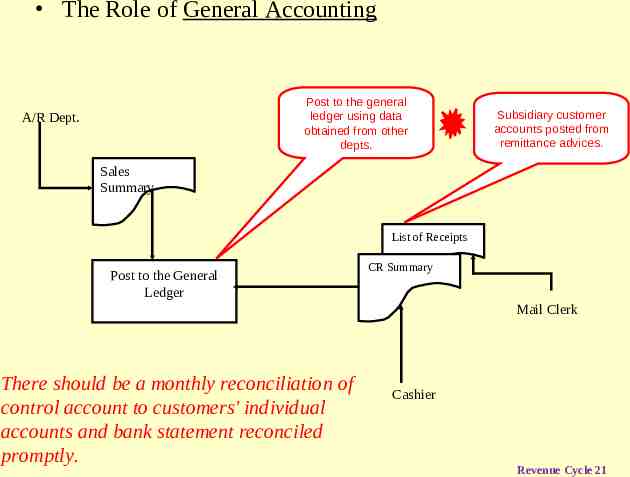

The Role of General Accounting Post to the general ledger using data obtained from other depts. A/R Dept. Subsidiary customer accounts posted from remittance advices. Sales Summary List of Receipts Post to the General Ledger CR Summary Mail Clerk There should be a monthly reconciliation of control account to customers' individual accounts and bank statement reconciled promptly. Cashier Revenue Cycle 21

Typical Documents and Records Sale is initiated with a What documents accompany the sale? Routine reports – include a sales journal – aged accounts receivable trial balance – Anything else? Revenue Cycle 22

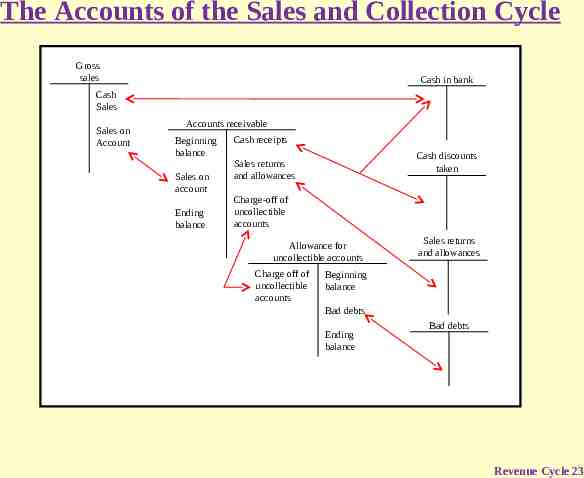

The Accounts of the Sales and Collection Cycle Gross sales Cash in bank Cash Sales Sales on Account Accounts receivable Beginning balance Sales on account Ending balance Cash receipts Cash discounts taken Sales returns and allowances Charge-off of uncollectible accounts Allowance for uncollectible accounts Charge off of uncollectible accounts Sales returns and allowances Beginning balance Bad debts Ending balance Bad debts Revenue Cycle 23

Methods of Recording Transactions Manual recording Recorded one transaction at a time Revenue Cycle 24

Control Differences Between Manual and Online Systems Manual systems: Transactions readily traced Online systems: Transactions recorded one at a time Document sequencing is important Revenue Cycle 25

Control Differences For Error Detection and Correction Manual systems: An erroneous transaction Error follow-up should be done in a timely manner Online systems: Focus is on preventing errors Input edit check for valid customer data and reasonableness Revenue Cycle 26

Manual and Online Systems: Segregation of Duties Manual systems: Online systems: Separate In decentralized systems Use passwords to separate Reconciliation and error follow-up Revenue Cycle 27

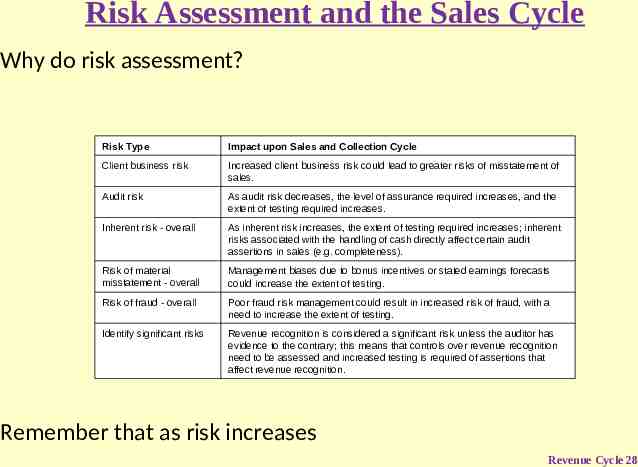

Risk Assessment and the Sales Cycle Why do risk assessment? Risk Type Impact upon Sales and Collection Cycle Client business risk Increased client business risk could lead to greater risks of misstatement of sales. Audit risk As audit risk decreases, the level of assurance required increases, and the extent of testing required increases. Inherent risk - overall As inherent risk increases, the extent of testing required increases; inherent risks associated with the handling of cash directly affect certain audit assertions in sales (e.g. completeness). Risk of material misstatement - overall Management biases due to bonus incentives or stated earnings forecasts could increase the extent of testing. Risk of fraud - overall Poor fraud risk management could result in increased risk of fraud, with a need to increase the extent of testing. Identify significant risks Revenue recognition is considered a significant risk unless the auditor has evidence to the contrary; this means that controls over revenue recognition need to be assessed and increased testing is required of assertions that affect revenue recognition. Remember that as risk increases Revenue Cycle 28

Effect of General Controls General controls – Are pervasive and affect multiple transaction cycles – Typical examples of general controls Revenue Cycle 29

If general controls are good, – the auditor may be able to rely upon them If general controls are poor Revenue Cycle 30

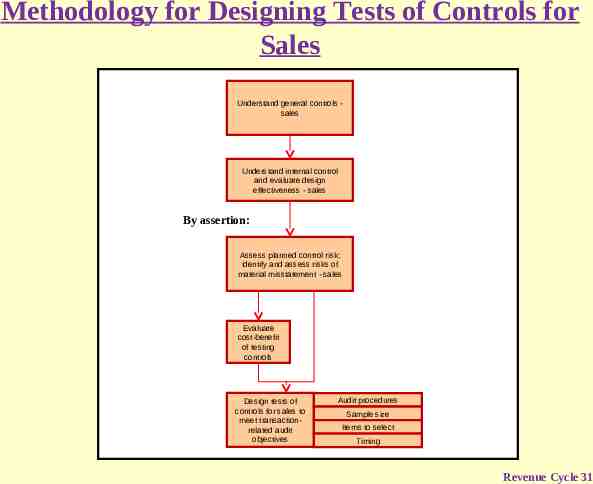

Methodology for Designing Tests of Controls for Sales Understand general controls sales Understand internal control and evaluate design effectiveness - sales By assertion: Assess planned control risk; identify and assess risks of material misstatement - sales Evaluate cost-benefit of testing controls Design tests of controls for sales to meet transactionrelated audit objectives Audit procedures Sample size Items to select Timing Revenue Cycle 31

Documentation of Internal Controls Internal controls need to be documented The auditor focuses on What type of controls can these be? Revenue Cycle 32

Key Controls for Sales Segregation of Duties – requires that different individuals be assigned responsibility for different elements of related activities, particularly those involving authorization, custody, or recordkeeping. Authorization – Proper authorization of transactions and activities helps ensure that all company activities adhere to established guide lines unless responsible managers authorize another course of action. Documents and Records – Adequate documents and records provide evidence that financial statements are accurate. Revenue Cycle 33

Internal verification Prenumbered documents Monthly statements Periodic reconciliation Revenue Cycle 34

Application Controls – These are computer internal controls – Edit checks for key fields can be verified by classifying the transactions on the values for the field. Revenue Cycle 35

Tests of Internal Controls Once the key controls have been identified, the auditor can decide Tests of internal controls will be devised for Revenue Cycle 36

Examples of Internal Control using the Occurrence Assertion Manual Control Key control: credit is approved before shipment takes place. – The manual control? Possible test of control Revenue Cycle 37

Automated Online Occurrence assertion Key control: Orders causing balances to exceed credit limits are held in a separate transaction file Possible test of control: Revenue Cycle 38

Interdependent Occurrence Assertion Key control: Orders causing balances to exceed the credit limit are printed on an exception report and must be approved by a credit manager Possible test of control: Revenue Cycle 39

Manual, Automated and Interdependent Controls From the previous examples, it can be seen that: – Manual controls are controls performed entirely by people – Automated controls (batch or online) are performed only by computerized systems – Interdependent controls rely upon computer processes (automation) but a person must also be involved to fully perform the control Revenue Cycle 40

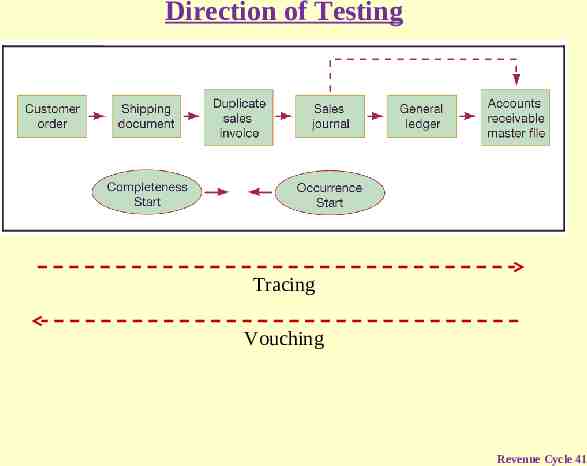

Direction of Testing Tracing Vouching Revenue Cycle 41

Tracing – Goes from the start of the transaction to the posting – Is this a test for overstatement or understatement of sales? Vouching – Goes from the general ledger or sales journal back to the original document Revenue Cycle 42

Typical Concerns for Tests of Sales 1. Recorded sales occurred – Occurrence – – Auditor is concerned with following possible misstatements Recorded sale for which there was no shipment Sale recorded more than once Shipment made to non-existent customer Revenue Cycle 43

2. Existing sales transactions are recorded – Completeness assertion – Want to test for unbilled shipments – Are shipping documents complete? 3. Recorded Sales are accurately recorded – Measurement assertion Revenue Cycle 44

4. Recorded sales are properly classified Ensure correct entry into the general ledger 5. Sales transactions are properly updated in the master file and correctly summarized Accuracy of the master file is essential 6. Sales are recorded on the correct dates Sales must be billed as soon as shipment takes place Remember all the tests can be dome with the same sample of sales invoices and shipping documents Revenue Cycle 45

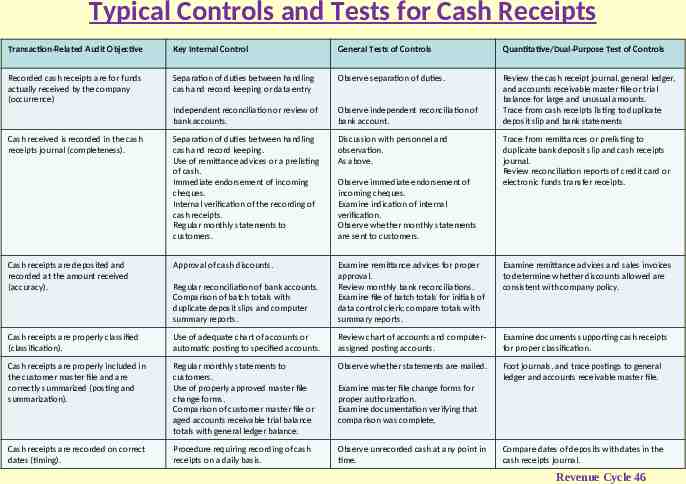

Typical Controls and Tests for Cash Receipts Transaction-Related Audit Objective Key Internal Control General Tests of Controls Quantitative/Dual-Purpose Test of Controls Recorded cash receipts are for funds actually received by the company (occurrence) Separation of duties between handling cash and record keeping or data entry Observe separation of duties. Independent reconciliation or review of bank accounts. Observe independent reconciliation of bank account. Review the cash receipt journal, general ledger, and accounts receivable master file or trial balance for large and unusual amounts. Trace from cash receipts listing to duplicate deposit slip and bank statements Separation of duties between handling cash and record keeping. Use of remittance advices or a prelisting of cash. Immediate endorsement of incoming cheques. Internal verification of the recording of cash receipts. Regular monthly statements to customers. Discussion with personnel and observation. As above. Cash receipts are deposited and recorded at the amount received (accuracy). Approval of cash discounts. Regular reconciliation of bank accounts. Comparison of batch totals with duplicate deposit slips and computer summary reports. Examine remittance advices for proper approval. Review monthly bank reconciliations. Examine file of batch totals for initials of data control clerk; compare totals with summary reports. Examine remittance advices and sales invoices to determine whether discounts allowed are consistent with company policy. Cash receipts are properly classified (classification). Use of adequate chart of accounts or automatic posting to specified accounts. Review chart of accounts and computerassigned posting accounts. Examine documents supporting cash receipts for proper classification. Cash receipts are properly included in the customer master file and are correctly summarized (posting and summarization). Regular monthly statements to customers. Use of properly approved master file change forms. Comparison of customer master file or aged accounts receivable trial balance totals with general ledger balance. Observe whether statements are mailed. Foot journals, and trace postings to general ledger and accounts receivable master file. Cash receipts are recorded on correct dates (timing). Procedure requiring recording of cash receipts on a daily basis. Observe unrecorded cash at any point in time. Cash received is recorded in the cash receipts journal (completeness). Observe immediate endorsement of incoming cheques. Examine indication of internal verification. Observe whether monthly statements are sent to customers. Trace from remittances or prelisting to duplicate bank deposit slip and cash receipts journal. Review reconciliation reports of credit card or electronic funds transfer receipts. Examine master file change forms for proper authorization. Examine documentation verifying that comparison was complete, Compare dates of deposits with dates in the cash receipts journal. Revenue Cycle 46

Frequency of Testing of Internal Controls Is an auditor allowed to use the results of prior testing in a current audit? In this case, which type of controls must be tested annually? Which type of controls could potentially be tested every three years? Revenue Cycle 47

Testing of Interdependent Controls The interdependent control has two parts: – A function performed – A function performed It is only possible to rely upon the automated function if: Both parts of the control must be tested to enable Revenue Cycle 48

What if Control Testing Yielded Many Errors? The first step is to determine whether the errors or exceptions – were due to a particular circumstance – or restricted to a particular time period Revenue Cycle 49

If the errors are systemic If this alternative control achieves the same purpose and is functioning correctly If no compensating control? Revenue Cycle 50

Material Error If there is no compensating control Want to quantify the extent of the error. Revenue Cycle 51

Results of Quantifying the Error If it turns out that the results of the weakness could result in immaterial error If a material error could result Revenue Cycle 52

Communicating Deficiencies in Internal Control (CAS 265) Communicate to those charged with governance and management Those deficiencies in internal control identified by the auditor The auditor shall include a written communication of th significant deficiencies Revenue Cycle 53

Performing the Audit Program The initial audit program is organized by audit assertion In performing for maximum efficiency The use of automated working paper software facilitates this process. Revenue Cycle 54

Computer-Assisted Audit Tests Where there are a large number of transactions E.g. In internal controls testing, the auditor could use automated sampling routines Revenue Cycle 55

Suitability of Test Data Online systems – Test data is useful Revenue Cycle 56

Suitability of Generalized Audit Software Best suited for analytical review, tests of detail, or dualpurpose tests, for example: Revenue Cycle 57

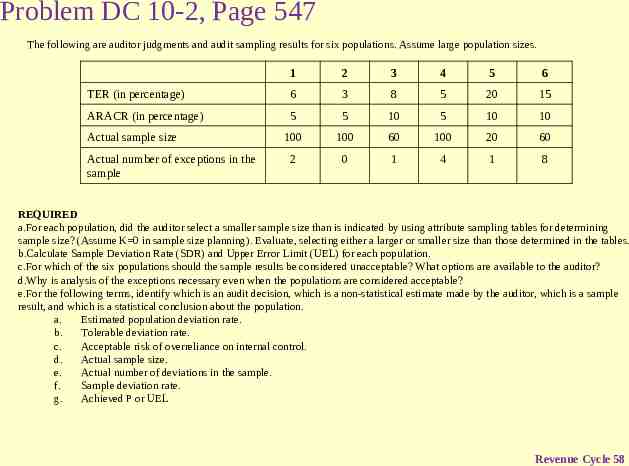

Problem DC 10-2, Page 547 The following are auditor judgments and audit sampling results for six populations. Assume large population sizes. 1 2 3 4 5 6 TER (in percentage) 6 3 8 5 20 15 ARACR (in percentage) 5 5 10 5 10 10 100 100 60 100 20 60 2 0 1 4 1 8 Actual sample size Actual number of exceptions in the sample REQUIRED a.For each population, did the auditor select a smaller sample size than is indicated by using attribute sampling tables for determining sample size? (Assume K 0 in sample size planning). Evaluate, selecting either a larger or smaller size than those determined in the tables. b.Calculate Sample Deviation Rate (SDR) and Upper Error Limit (UEL) for each population. c.For which of the six populations should the sample results be considered unacceptable? What options are available to the auditor? d.Why is analysis of the exceptions necessary even when the populations are considered acceptable? e.For the following terms, identify which is an audit decision, which is a non-statistical estimate made by the auditor, which is a sample result, and which is a statistical conclusion about the population. a. Estimated population deviation rate. b. Tolerable deviation rate. c. Acceptable risk of overreliance on internal control. d. Actual sample size. e. Actual number of deviations in the sample. f. Sample deviation rate. g. Achieved P or UEL Revenue Cycle 58

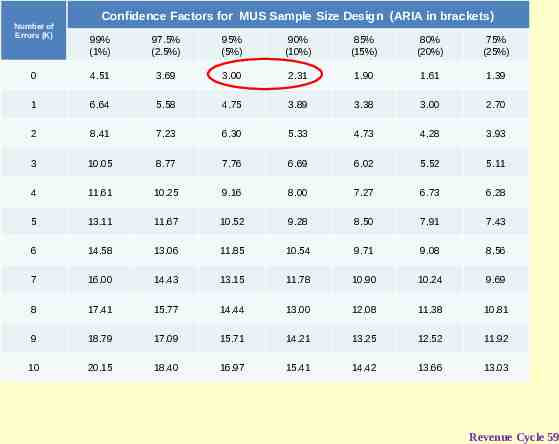

Number of Errors (K) Confidence Factors for MUS Sample Size Design (ARIA in brackets) 99% (1%) 97.5% (2.5%) 95% (5%) 90% (10%) 85% (15%) 80% (20%) 75% (25%) 0 4.51 3.69 3.00 2.31 1.90 1.61 1.39 1 6.64 5.58 4.75 3.89 3.38 3.00 2.70 2 8.41 7.23 6.30 5.33 4.73 4.28 3.93 3 10.05 8.77 7.76 6.69 6.02 5.52 5.11 4 11.61 10.25 9.16 8.00 7.27 6.73 6.28 5 13.11 11.67 10.52 9.28 8.50 7.91 7.43 6 14.58 13.06 11.85 10.54 9.71 9.08 8.56 7 16.00 14.43 13.15 11.78 10.90 10.24 9.69 8 17.41 15.77 14.44 13.00 12.08 11.38 10.81 9 18.79 17.09 15.71 14.21 13.25 12.52 11.92 10 20.15 18.40 16.97 15.41 14.42 13.66 13.03 Revenue Cycle 59

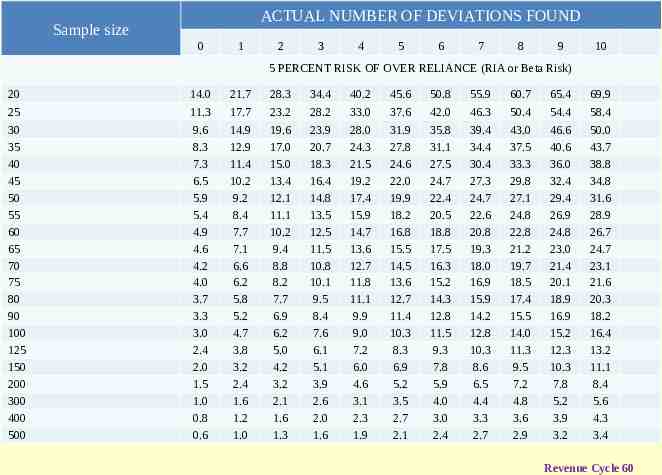

ACTUAL NUMBER OF DEVIATIONS FOUND Sample size 0 1 2 3 4 5 6 7 8 9 10 5 PERCENT RISK OF OVER RELIANCE (RIA or Beta Risk) 20 25 14.0 11.3 21.7 17.7 28.3 23.2 34.4 28.2 40.2 33.0 45.6 37.6 50.8 42.0 55.9 46.3 60.7 50.4 65.4 54.4 69.9 58.4 30 35 40 45 50 55 60 65 70 75 80 90 100 125 150 200 300 400 500 9.6 8.3 7.3 6.5 5.9 5.4 4.9 4.6 4.2 4.0 3.7 3.3 3.0 2.4 2.0 1.5 1.0 0.8 0.6 14.9 12.9 11.4 10.2 9.2 8.4 7.7 7.1 6.6 6.2 5.8 5.2 4.7 3.8 3.2 2.4 1.6 1.2 1.0 19.6 17.0 15.0 13.4 12.1 11.1 10.2 9.4 8.8 8.2 7.7 6.9 6.2 5.0 4.2 3.2 2.1 1.6 1.3 23.9 20.7 18.3 16.4 14.8 13.5 12.5 11.5 10.8 10.1 9.5 8.4 7.6 6.1 5.1 3.9 2.6 2.0 1.6 28.0 24.3 21.5 19.2 17.4 15.9 14.7 13.6 12.7 11.8 11.1 9.9 9.0 7.2 6.0 4.6 3.1 2.3 1.9 31.9 27.8 24.6 22.0 19.9 18.2 16.8 15.5 14.5 13.6 12.7 11.4 10.3 8.3 6.9 5.2 3.5 2.7 2.1 35.8 31.1 27.5 24.7 22.4 20.5 18.8 17.5 16.3 15.2 14.3 12.8 11.5 9.3 7.8 5.9 4.0 3.0 2.4 39.4 34.4 30.4 27.3 24.7 22.6 20.8 19.3 18.0 16.9 15.9 14.2 12.8 10.3 8.6 6.5 4.4 3.3 2.7 43.0 37.5 33.3 29.8 27.1 24.8 22.8 21.2 19.7 18.5 17.4 15.5 14.0 11.3 9.5 7.2 4.8 3.6 2.9 46.6 40.6 36.0 32.4 29.4 26.9 24.8 23.0 21.4 20.1 18.9 16.9 15.2 12.3 10.3 7.8 5.2 3.9 3.2 50.0 43.7 38.8 34.8 31.6 28.9 26.7 24.7 23.1 21.6 20.3 18.2 16.4 13.2 11.1 8.4 5.6 4.3 3.4 Revenue Cycle 60

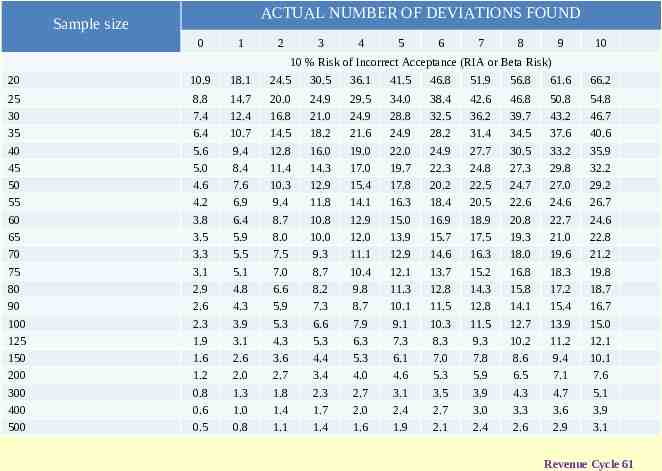

ACTUAL NUMBER OF DEVIATIONS FOUND Sample size 0 1 2 3 4 5 6 7 8 9 10 10 % Risk of Incorrect Acceptance (RIA or Beta Risk) 20 10.9 18.1 24.5 30.5 36.1 41.5 46.8 51.9 56.8 61.6 66.2 25 30 35 40 45 50 55 60 65 70 75 80 90 100 125 150 200 300 400 500 8.8 7.4 6.4 5.6 5.0 4.6 4.2 3.8 3.5 3.3 3.1 2.9 2.6 2.3 1.9 1.6 1.2 0.8 0.6 0.5 14.7 12.4 10.7 9.4 8.4 7.6 6.9 6.4 5.9 5.5 5.1 4.8 4.3 3.9 3.1 2.6 2.0 1.3 1.0 0.8 20.0 16.8 14.5 12.8 11.4 10.3 9.4 8.7 8.0 7.5 7.0 6.6 5.9 5.3 4.3 3.6 2.7 1.8 1.4 1.1 24.9 21.0 18.2 16.0 14.3 12.9 11.8 10.8 10.0 9.3 8.7 8.2 7.3 6.6 5.3 4.4 3.4 2.3 1.7 1.4 29.5 24.9 21.6 19.0 17.0 15.4 14.1 12.9 12.0 11.1 10.4 9.8 8.7 7.9 6.3 5.3 4.0 2.7 2.0 1.6 34.0 28.8 24.9 22.0 19.7 17.8 16.3 15.0 13.9 12.9 12.1 11.3 10.1 9.1 7.3 6.1 4.6 3.1 2.4 1.9 38.4 32.5 28.2 24.9 22.3 20.2 18.4 16.9 15.7 14.6 13.7 12.8 11.5 10.3 8.3 7.0 5.3 3.5 2.7 2.1 42.6 36.2 31.4 27.7 24.8 22.5 20.5 18.9 17.5 16.3 15.2 14.3 12.8 11.5 9.3 7.8 5.9 3.9 3.0 2.4 46.8 39.7 34.5 30.5 27.3 24.7 22.6 20.8 19.3 18.0 16.8 15.8 14.1 12.7 10.2 8.6 6.5 4.3 3.3 2.6 50.8 43.2 37.6 33.2 29.8 27.0 24.6 22.7 21.0 19.6 18.3 17.2 15.4 13.9 11.2 9.4 7.1 4.7 3.6 2.9 54.8 46.7 40.6 35.9 32.2 29.2 26.7 24.6 22.8 21.2 19.8 18.7 16.7 15.0 12.1 10.1 7.6 5.1 3.9 3.1 Revenue Cycle 61

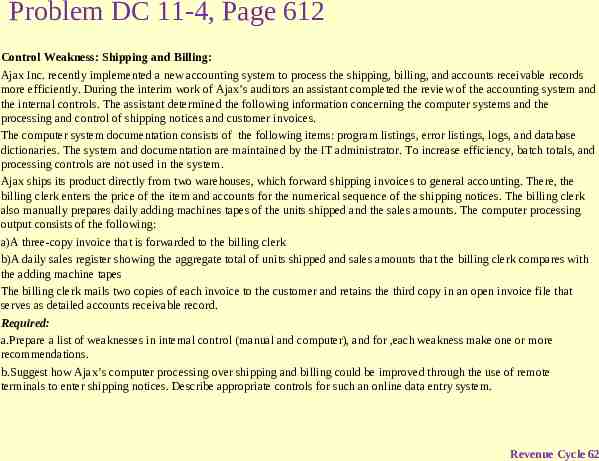

Problem DC 11-4, Page 612 Control Weakness: Shipping and Billing: Ajax Inc. recently implemented a new accounting system to process the shipping, billing, and accounts receivable records more efficiently. During the interim work of Ajax’s auditors an assistant completed the review of the accounting system and the internal controls. The assistant determined the following information concerning the computer systems and the processing and control of shipping notices and customer invoices. The computer system documentation consists of the following items: program listings, error listings, logs, and database dictionaries. The system and documentation are maintained by the IT administrator. To increase efficiency, batch totals, and processing controls are not used in the system. Ajax ships its product directly from two warehouses, which forward shipping invoices to general accounting. There, the billing clerk enters the price of the item and accounts for the numerical sequence of the shipping notices. The billing clerk also manually prepares daily adding machines tapes of the units shipped and the sales amounts. The computer processing output consists of the following: a)A three-copy invoice that is forwarded to the billing clerk b)A daily sales register showing the aggregate total of units shipped and sales amounts that the billing clerk compares with the adding machine tapes The billing clerk mails two copies of each invoice to the customer and retains the third copy in an open invoice file that serves as detailed accounts receivable record. Required: a.Prepare a list of weaknesses in internal control (manual and computer), and for ,each weakness make one or more recommendations. b.Suggest how Ajax’s computer processing over shipping and billing could be improved through the use of remote terminals to enter shipping notices. Describe appropriate controls for such an online data entry system. Revenue Cycle 62